Direct Reduced Iron (DRI) Market Size, Share & Industry Analysis, By Form (Pellets and Others), By Production Process (Gas-based and Coal-based), By Application (Steel Production, Construction, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

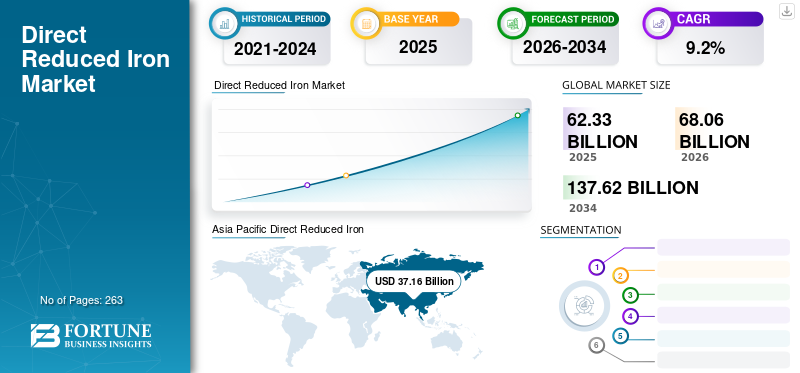

The global direct reduced iron (DRI) market size was valued at USD 62.33 billion in 2025 and is projected to grow from USD 68.06 billion in 2026 to USD 137.62 billion by 2034, exhibiting a CAGR of 9.2% during the forecast period. Asia Pacific dominated the direct reduced iron market with a market share of 59.6% in 2025. Moreover, the direct reduced iron market size in the U.S. is projected to grow significantly, reaching an estimated value of USD 7.68 billion by 2032, driven by significant demand for direct reduced iron from steel used in the oil and gas industry.

Direct reduced iron (DRI) is an iron ore in the form of pellets and lumps, also known as sponge iron. The overall process of reducing iron ore is the removal of oxygen from its ore or other ferrous substances in a solid state without melting, similar to that encountered in the blast furnace. The reducing agents are hydrogen and carbon monoxide, which come from reformed coal, synthesis gas, and natural gas.

Moreover, steel production using blast furnace/basic oxygen furnace (BF/BOF) processes is based on fossil fuels. The reducing gas is obtained from natural gas or coal, producing a large amount of CO2 emissions. Therefore, the companies in this market are increasing R&D capacities in hydrogen-based DRI production, which can be further processed into steel with an Electric Arc Furnace (EAF). Such factors are expected to boost the direct reduced iron market growth during the forecast period.

The spread of COVID-19 in several countries, including India, China, Japan, Germany, Italy, Canada, and the U.S., led to lockdowns, thereby restricting the flow of resources and products. As finished goods distribution and raw material supply were affected, it severely affected the revenue and profitability of manufacturers. However, once the pandemic was under control, governments eased restrictions to support nations and upscale the economic value chains by aiding small-scale and domestic businesses to recommence manufacturing operations. In addition, DRI companies ramped up production to meet the growing demand for steel solutions. The manufacturers also started their activities by first implementing the indicated preventative measures.

Download Free sample to learn more about this report.

Direct Reduced Iron Market KEY TAKEAWAYS

- 2025 Market Size: USD 62.33 billion

- 2026 Market Size: USD 68.06 billion

- 2034 Forecast Market Size: USD 137.62 billion

- CAGR: 9.2% from 2026–2034

- Asia Pacific dominated the direct reduced iron market with a 59.6% share in 2025.

- The pellets segment accounted for the largest market share of 64.21% in 2026.

- The gas-based segment accounted for the largest market share of 76.2% in 2026.

Asia Pacific

Asia Pacific USD 37.16 billion in 2025, driven by rising steel production and increasing demand from construction and manufacturing industries.

North America

North America USD 4.96 billion in 2025, supported by growing steel demand from the oil & gas and construction sectors.

Europe

Europe USD 6.69 billion in 2025, driven by increasing construction activities and rising demand for steel products.

U.S.

U.S. The market is projected to reach USD 7.68 billion by 2032, driven by strong demand for DRI in steel production for the oil & gas industry.

Japan

Japan USD 17.57 billion by 2026, supported by steady demand from the steel, automotive, and manufacturing industries.

Read More

Direct Reduced Iron (DRI) Market Trends

Rising Interest in Developing Technologies to Create the Product is the Major Trend

Steelmaking is still a high-energy and CO2-emitting process. However, the steel sector is dedicated to keeping its operations and product usage as low-impact as possible. According to the World Steel Organization, every tonne of steel produced in 2021 resulted in an average of 1.89 tonnes of CO2 being released into the atmosphere.

Moreover, there has been a rise in industrial and scientific interest in developing technologies to create direct reduced iron due to the need for reduced energy use and greenhouse gas emissions on a global scale. Oxygen is removed from iron ore in its solid state to generate sponge iron. The carbon reductant is replaced with hydrogen in the DRI process, which lowers CO2 emission by using natural gas instead of coal.

Download Free sample to learn more about this report.

Direct Reduced Iron (DRI) Market Growth Factors

Growing Usage of Direct Reduced Iron in Steelmaking to Propel the Market Growth

Increasing technology usage in the steelmaking industry is expected to be a major driving factor behind market growth. The technology is extensively utilized for steelmaking, demonstrating remarkable advantages compared to traditional blast furnace methods. The process has gained traction for steelmaking that addresses the CO2 emission restriction. Changing production dynamics, which requires the start-and-go action, is accomplished with the technology, as it can be stopped and restarted immediately and efficiently.

DRI products and manufacturing have developed throughout the years to keep up with the expanding needs of the steelmaking industry. As electric arc furnace (EAF) steelmaking expands, it gives EAF steelmakers the broad flexibility to customize their furnace charges to market conditions. In addition, it helps enhance the capacity to produce higher-quality steels due to their high metallic iron content, adjustable carbon level, and consistent physical and chemical properties.

Changing downstream requirements for various end-use industries has prompted the demand as it is used to improve product quality. It helps modulate carbon content easily per the product requirement, and the DRI forms a very low residual substance compared to normal scrap. Moreover, it demonstrates several benefits, including lower capital, operating costs, low tramp material content, predictable chemistry, and relatively uninterrupted continuous iron making. The growing steel consumption in various end-use industries is further expected to proliferate the market growth.

RESTRAINING FACTORS

Risks Related to Direct Reduced Iron Handling and Storage May Hinder Market Growth

DRI is susceptible to rusting (re-oxidizing) in the presence of oxygen, just as steel structures. Moreover, heat is produced during the oxidation process, which is significant in bulk DRI cargos. DRI’s sponge structure also prevents heat from dissipating, allowing isolated pockets of DRI to heat up quickly in bulk. In addition, after handling bulk materials, a brief rise in temperature of roughly 30 degrees Celsius caused by self-heating is possible. After coming into contact with water, the material may slowly emit hydrogen. This cargo produces heat and hydrogen when in contact with air, freshwater, or seawater. A concentration of hydrogen and air, which is combustible, can combine to create an explosive mixture.

Direct Reduced Iron (DRI) Market Segmentation Analysis

By Form Analysis

Pellets Segment Dominated due to Ease of Transport

Based on form, the market is bifurcated into pellets and others.

The pellets segment led the market accounting for 64.21% market share in 2026. DRI can be used in a variety of processes in the production of crude steel. Usually, the product is used as a supplement for scrap in the EAF process. In addition, it is typically made from high-quality iron ore pellets, generally reduced by gas, to provide a highly metalized raw material for both traditional blast furnaces and electric arc furnaces. Furthermore, pellets are the most preferred among direct reduced iron mold types as they have better reactivity, are less expensive than lumps, and are easy to transport.

Moreover, pellets-ore motley with coal is transferred into the rotary kilns and then heated by coal burners to produce DRI. Direct reduced pellets are often used in EAF with limited refining capacity; the iron feed and the successively directly reduced iron must be low.

In addition, direct reduced iron is usually made from high-quality iron ore pellets, generally reduced by gas, to provide a highly metalized raw material for traditional blast and electric arc furnaces. Furthermore, pellets are the most preferred among product mold types as they have better reactivity, are less expensive than lumps, and are easy to transport. Moreover, pellets-ore motley with coal is transferred into the rotary kilns and then heated by coal burners to produce DRI. Direct reduced pellets are often used in EAF (electric arc furnaces) with limited refining capacity; the iron feed and the successively directly reduced iron must be low.

By Production Process Analysis

Gas-based Segment Dominated Due to Presence of Fewer Impurities

By production process, the market is segmented into gas-based and coal-based.

The gas-based segment dominated the market accounting for 76.2% market share in 2026 and may continue its dominance till 2034. Gas condensation contains fewer impurities than coal condensation. The resulting iron may be purer and produce higher-quality steel. In addition, the gas-based process produces significantly less carbon dioxide than coal-based processes. For the reduction reaction, the gas-based process uses a shaft furnace, whereas the coal-based process uses one of the four reactor types. The reactors are rotary kiln, shaft furnace, fluidized bed reactor, and rotary hearth furnace. The rotary kiln is the most popular reactor for the coal process.

The coal-based segment is expected to hold a significant market share during the forecast period. Rotary kilns are used in coal-based reduction processes that convert the iron ore directly into metallic iron without melting the materials. In this process, metallic iron is produced by reducing iron oxide below the melting temperature of iron ore, i.e., 1,535°C, using carbonaceous material in the non-coking coal.

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

Steel Production Segment Dominates Due to Growing Production of High-quality Steel

By application, the market is segmented into steel production, construction, and others.

The steel production segment dominated the market accounting for 46.47% market share in 2026 and dominates the market due to a rise in the production of high-quality steel due to the adverse impact of low-quality raw materials on the environment. DRI is experiencing increased demand as a supplement to the improvement in steel quality required by steel manufacturers.

The construction segment is anticipated to register a significant growth rate during the forecast period due to well-performing residential infrastructure and a surge in activity in various non-residential sectors. In recent years, the construction industry has grown significantly. In addition, a rebound in residential construction is anticipated to boost the construction sector, which is expected to impact the market growth.

REGIONAL INSIGHTS

Asia Pacific

Asia Pacific Direct Reduced Iron (DRI) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The market in Asia Pacific reached USD 37.16 billion in 2025, representing 59.60% of total market revenue, and is expected to reach USD 40.83 billion in 2026, owing to increased product demand from numerous applications such as steel production and construction. The construction industry in India is anticipated to witness a significant growth rate during the forecast period. In addition, rising steel production and increasing demand from several end-use industries, such as aerospace and automotive, are expected to drive the market growth in the region. The government support for the expansion of the chemical industry in the region is further anticipated to drive the market growth during the forecast period. The Japan market is valued at USD 17.57 billion by 2026. The China market is valued at USD 32.37 billion by 2026. The India market is valued at USD 41.04 billion by 2026.

To know how our report can help streamline your business, Speak to Analyst

North America

The North America market was valued at USD 4.96 billion in 2025, capturing 8.00% of global revenue, and is estimated to reach USD 5.37 billion in 2026. A major factor driving the market growth is the growing steel industry in the region. Steel is extensively used in multiple industries, including industrial machines, appliances, oil & gas, automotive, and construction. The region is witnessing a significant demand for direct reduced iron from steel used in the oil and gas industry. The regional growth is further driven by improved production of oil and other natural gas, which requires DRI for the fracking process. The U.S. market is valued at USD 4.66 billion by 2026.

A major factor driving the DRI market is the growing steel industry. Steel is extensively used in multiple industries, including industrial machines, appliances, oil & gas, automotive, and construction. The region is witnessing a significant demand for steel from the oil and gas industry. With technological advancements and increasing C02 emission restrictions, several players in the region are increasing the industrial infrastructure, which, on the other hand, will increase the steel demand and consolidate the North American DRI market.

Europe

In 2025, Europe held 10.70% of the global market, reaching a valuation of USD 6.69 billion, and is projected to grow to USD 7.28 billion in 2026. The market in Europe is anticipated to witness a significant growth rate during the forecast period owing to increasing investments in R&D activities and demand for steel products from rising building and construction activities. According to the World Steel Association, the construction industry accounts for more than half of global demand for steel. One of the main factors fueling the interest in steel production is the growing need for housing due to population growth. The UK market is valued at USD 1.61 billion by 2026. The Germany market is valued at USD 5.17 billion by 2026.

Latin America

Latin America maintained a strong presence in the global market, reaching USD 1.15 billion in 2025, accounting for 1.80% share, and is expected to reach USD 1.23 billion in 2026. The Latin America market is expected to see steady growth during the forecast period due to an increase in steel demand to manufacture automotive parts. This growth is associated with the increased production of passenger and light commercial vehicles in the region. Steel is being used in several end-use industries and contributes to overall regional economic development.

Middle East & Africa

In 2025, the Middle East & Africa market stood at USD 12.37 billion, representing 19.80% of global demand, and is projected to grow to USD 13.34 billion in 2026. The Middle East & Africa market is expected to reach moderate growth during the forecast period owing to the rapid expansion of the residential building sector in the region.

List of Key Companies in Direct Reduced Iron (DRI) Market

Key Players are Adopting Business Expansion Strategies to Maintain their Market Position

The global market is moving toward consolidation, with key players operating in the market, such as Qatar Steel, Kobe Steel Ltd, ArcelorMittal, and NUCOR. Most manufacturers are escalating their business to achieve competency in the industry and lessen the threats posed by the new entrants’ threats. Moreover, market participants compete with international and regional players with widespread distribution networks, raw material suppliers, and regulatory know-how. In addition, companies have been signing contracts, strategic partnerships, and acquisitions with other market leaders to expand their existing markets.

LIST OF KEY COMPANIES PROFILED:

- Qatar Steel (Qatar)

- Kobe Steel Ltd (Japan)

- ArcelorMittal (Luxembourg)

- NUCOR (U.S.)

- Midrex Technologies Inc. (U.S.)

- Khouzestan Steel Company (Khuzestan)

- Welspun Group (India)

- Jindal Shadeed Iron & Steel LLC (Oman)

- AM/NS India (India)

- Tosyali Algeria A.S. (Algeria)

KEY INDUSTRY DEVELOPMENTS:

- October 2022- H2 Green Steel established a DRI plant powered by 100% green hydrogen and based on Midrex technology. The Midrex H2 plant has an annual production of 2.1 million tonnes of hot DRI and Hot Briquette Iron (HBI), which feeds the production of an initial 2.5 million tonnes of green steel in the soil of northern Sweden. This unique DRI system is being provided by a consortium of Midrex and Paul Wurth, an SMS group company.

- May 2022- Kobe Steel launched “Kobenable Steel” and became the first company to provide low CO2 blast furnace steel products in Japan. The company significantly reduced CO2 emissions while product manufacturing using the blast furnace ironmaking process. It has also planned to sell the new products in the fiscal year 2023.

- March 2022- ArcelorMittal announced an investment of USD 292 million to create a new production unit for electrical steels at the Mardyck site in the north of France. The facility specializes in producing electrical steel for the engines of electric vehicles, which complements ArcelorMittal’s existing electrical steel plant. The new industrial unit has a 200 kiloton production capacity and strengthened the French electromobility sector.

- February 2022- Tosyali Algeria set a new world record for annual production of DRI through a single modular plant, producing more than 2.28 million tonnes in 2022.

- March 2021- ArcelorMittal expanded its industrial plant at its site in Bremen. This plant offers the direct reduction of iron ore and EAF-based steelmaking. The company also expanded an innovative DRI pilot plant and an EAF in Eisenhüttenstadt.

REPORT COVERAGE

The research report provides a detailed analysis of the market and focuses on crucial aspects such as leading companies and applications. It also offers insights into key trends and highlights vital industry developments. In addition to the factors mentioned above, the report encompasses various factors that have contributed to the market growth in recent years. It further includes historical data and forecasts revenue growth at global, regional, and country levels and analyzes the latest market dynamics and opportunities.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.2% from 2026 to 2034 |

|

Unit |

Value (USD Billion) and Volume (Kiloton) |

|

Segmentation |

By Form

|

|

By Production Process

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 65.85 billion in 2026 and is projected to reach USD 137.62 billion by 2034.

In 2025, the Asia Pacific market size stood at USD 37.16 billion.

Growing at a CAGR of 9.2%, the market is expected to exhibit steady growth during the forecast period (2026-2034).

Based on application, the steel production segment is expected to be the leading segment in the market during the forecast period.

The growing product demand from the steel industry is expected to bolster the market growth.

Qatar Steel, Kobe Steel Ltd, ArcelorMittal, and NUCOR are major players in the global market.

Asia Pacific held a dominant market share in 2026.

The rising demand from the iron and steel industry is expected to drive product adoption.

- 2021-2034

- 2025

- 2021-2024

- 263

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us