Dredging Equipment Market Size, Share & Industry Analysis, By Product Type (Mechanical Dredgers, Hydraulic Dredgers, and Others), By Application (Navigational Channel Maintenance, Port & Harbor Expansion, Land Reclamation, Environmental Remediation, Offshore Renewable Energy Construction, and Others), By End-User (Government Agencies, Private Port Operators, EPC / Marine Contractors, Mining & Energy Companies, and Others), and Regional Forecast, 2026-2034

Dredging Equipment Market Size and Future Outlook

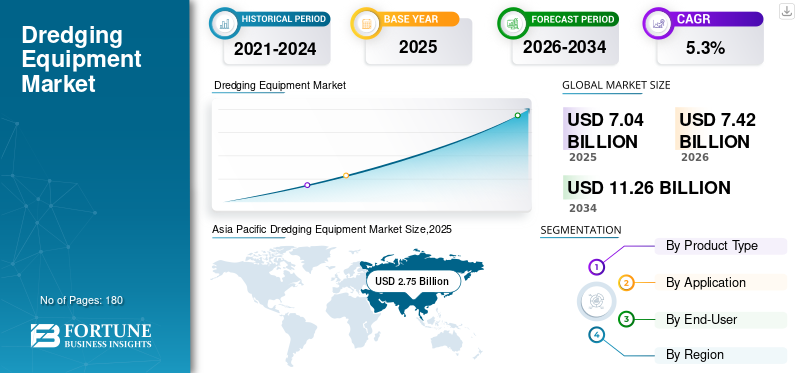

The global dredging equipment market size was valued at USD 7.04 billion in 2025. The market is projected to grow from USD 7.42 billion in 2026 to USD 11.26 billion by 2034, exhibiting a CAGR of 5.3% during the forecast period. Asia Pacific dominated the global dredging equipment market with a market share of 39.06% in 2025.

Dredging equipment is specialized machinery and tools used for transporting, excavating, and disposing of underwater debris, sediments, and waste materials from various water bodies, including lakes, harbors, coastal areas, and rivers. It is primarily used for performing dredging operations. Dredging equipment has also found applications in construction, mining, navigation, and environmental rehabilitation. With increasing maritime trade and rising investment in port infrastructure, there is a growing need to maintain and deepen existing ports and harbours, which drives the demand for dredging equipment to ensure safe navigation and efficient cargo handling. The growing urbanization and rising investment in development projects in coastal areas create demand for such equipment for land reclamation projects. Additionally, the exploration of offshore oil & gas, as well as rising investment in pipeline and energy infrastructure across the globe, required dredging products.

Furthermore, the market is dominated by several major players, including Royal IHC, Damen Shipyards Group N.V., Qingzhou Julong Environment Technology Co., Ltd., and others, who are expanding their global presence through partnerships and acquisitions. For instance, Royal IHC collaborated with major port authorities for long-term dredger supply contracts, while DEME and Boskalis continuously acquire regional dredging firms to strengthen their market reach.

Download Free sample to learn more about this report.

Dredging Equipment Market key takeaways

- 2025 Market Size: USD 7.04 Billion

- 2026 Market Size: USD 7.42 Billion

- 2034 Forecast Market Size: USD 11.26 Billion

- CAGR: 5.3% from 2026–2034

- Asia Pacific dominated the dredging equipment market with a 39.06% share in 2025.

- The hydraulic dredgers segment is expected to register the fastest growth during the forecast period.

- The offshore renewable energy construction segment is projected to grow at the highest CAGR of 6.7% during the forecast period.

Asia Pacific

Asia Pacific held the largest market share in 2025 and is projected to remain the fastest-growing regional market.

North America

North America is witnessing steady growth, supported by port deepening, coastal resilience projects, and offshore wind development.

Europe

Europe continues to expand at a stable pace, driven by channel maintenance, environmental regulations, and offshore wind activities.

U.S.

The country leads regional demand, supported by major port-deepening projects and coastal infrastructure investments.

Japan

Rising investments in port modernization and coastal infrastructure are supporting demand for dredging equipment.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Demand for Advanced Dredging Equipment to Accelerate Market Growth

The dredging equipment market growth is fueled by increasing demand for advanced dredging equipment. The adoption of advanced dredging technologies, such as automated control systems, GPS-guided operations, and real-time monitoring, is enhancing dredging precision, fuel efficiency, and operational productivity across diverse applications. It includes coastal protection, harbor deepening, and land reclamation projects.

Modern dredging vessels are equipped with digital sensors and eco-friendly propulsion mechanisms that ensure higher operational efficiency, reduced downtime, and minimized environmental footprint. These advancements align with global sustainability standards such as the IMO 2020 regulations, which encourage the use of cleaner and more energy-efficient dredging equipment. For instance,

- In October 2025, Boskalis launched its new mega Trailing Suction Hopper Dredger (TSHD), Seaway, marking a significant advancement in dredging technology. The vessel boasts a high dredging capacity and is designed with energy-efficient features, including a full diesel-electric propulsion system, which aims to reduce CO₂ emissions.

MARKET RESTRAINTS

High Capital Costs, Environmental Restrictions, and Operational Complexities to Hamper Market Growth

The market faces several structural and regulatory constraints that hinder its expansion pace, despite increasing global demand. Dredging vessels, such as Trailing Suction Hopper Dredgers (TSHDs) and Cutter Suction Dredgers (CSDs) require capital investments ranging from USD 30 million to USD 150 million per unit, depending on capacity and configuration. Smaller operators find it financially challenging to procure such high-end equipment, especially in developing regions. In the first half of 2025, many small contractors in Southeast Asia reported delays in dredger acquisition due to limited financing support and rising steel and marine component prices. Dredging operations in harsh marine environments frequently result in wear and tear of suction pipes, cutter heads, and hydraulic systems, leading to operational downtime.

Authorities such as the International Maritime Organization (IMO), European Environment Agency (EEA), and national governments impose strict standards regarding turbidity control, sediment disposal, and noise pollution.

MARKET OPPORTUNITIES

Expansion of Port Infrastructure and Offshore Renewable Energy to Create Lucrative Market Opportunities

Large-scale coastal and port infrastructure projects in Asia Pacific and the Middle East further propel the dredging equipment market demand. Governments in India, China, and Saudi Arabia are investing heavily in expanding ports and reclaiming land for industrial and residential purposes under national initiatives such as Sagarmala (India) and Vision 2030 (Saudi Arabia). For Instance,

- India's largest commercial port, Mundra, is undergoing an approximately USD 500 million (Rs 45,000 crore) expansion to more than double its capacity from approximately 250 Million Metric Tons Per Annum (MMTPA) in 2024 to 514 MMTPA by 2030. This expansion includes dredging operations to accommodate larger vessels and increase cargo handling capacity.

The convergence of port expansions, coastal infrastructure projects, and offshore wind developments is significantly boosting the product demand. Together, these initiatives highlight how the energy transition and growth in trade are driving long-term investments in high-capacity, sustainable dredging solutions.

DREDGING EQUIPMENT MARKET TRENDS

Digitalization, Automation, and Sustainability to Shape the Future of Dredging Equipment

The dredging industry is undergoing a paradigm shift driven by digital transformation, environmental responsibility, and the adoption of energy-efficient technologies. There is an increasing trend of reusing dredged materials for land reclamation and beach nourishment. For instance, the Singapore Land Authority reused over 90 million cubic meters of dredged sand for the Tuas Port Development project.

The Integration of digital twins and Remote Operation Centers (ROC) allows operators to simulate dredging environments and monitor performance remotely, enhancing project efficiency and reducing downtime.

Sustainability-focused innovations such as electric and hybrid propulsion systems, low-carbon engines, and biodegradable hydraulic fluids are being rapidly adopted to meet environmental compliance and carbon neutrality targets. For instance,

- In March 2025, Royal IHC launched the electric Cutter Suction Dredger (CSD) Sandra at its Kinderdijk shipyard in the Netherlands. This vessel, along with its sister dredger CSD Calen, is designed for sustainable mining operations at Kenmare Resources' Moma Mine in Mozambique.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Type

Hydraulic Dredgers Lead Market Growth as Cutter Suction Dredgers Emerge as Fastest-Expanding Segment Globally

In terms of product type, the market is categorized into hydraulic dredgers, mechanical dredgers, and others.

The hydraulic dredgers are the fastest-growing segment, supported by increasing demand for high-capacity, continuous dredging solutions needed for large port-deepening, land reclamation, and coastal protection projects. Within this category, Cutter Suction Dredgers (CSDs) represent the highest-growing sub-segment, recording the strongest CAGR due to their versatility in handling compact soils and their extensive use in major capital dredging and reclamation works across the Asia Pacific and the Middle East. Trailing Suction Hopper Dredgers (TSHDs) also contribute significantly as the largest hydraulic sub-segment, driven by rising maintenance dredging and beach nourishment needs.

In contrast, mechanical dredgers show moderate growth, reflecting their continued but more limited role in confined or hard-soil environments. Overall, technological upgrades and stricter environmental standards further reinforce the shift toward advanced hydraulic systems.

By Application

Increasing Seabed Preparation and Cable-Laying Demand Drives Offshore Renewable Energy Construction Segment Growth

In terms of application, the market is categorized into navigational channel maintenance, port & harbor expansion, land reclamation, environmental remediation, offshore renewable energy construction, and others.

The dredging equipment market shows varied growth across applications, with offshore renewable energy construction segment registering the strongest CAGR of 6.7% during the forecast period. This surge is driven by the rapid global build-out of offshore wind farms, which require extensive seabed preparation, trenching, and cable-laying support.

Port and harbor expansion remains another high-growth area supported by increasing maritime trade, larger vessel sizes, and global port modernization initiatives.

Land reclamation continues to benefit from coastal urbanization, tourism development, and major reclamation megaprojects in the Asia Pacific and the Middle East. At the same time, navigational channel maintenance remains the largest application category, reflecting the essential but routine nature of ongoing maintenance dredging. Overall, energy transition, coastal infrastructure development, and urban expansion are key factors shaping application-level demand.

By End-User

Rising Marine Infrastructure Projects Accelerate EPC/Marine Contractors Segment Growth

Based on end-user industry, the market is segmented into government agencies, private port operators, EPC / marine contractors, mining & energy companies, and others.

To know how our report can help streamline your business, Speak to Analyst

EPC/Marine contractors is emerging as the fastest-growing segment, expected to register a notable CAGR of 6.7% during the forecast period. Their rapid expansion is driven by increasing involvement in large-scale port development, increasing demand for coastal protection works, offshore energy installations, and turnkey marine infrastructure projects that require advanced, high-capacity dredging systems.

Private port operators follow with a solid 5.2% CAGR over the forecast period, supported by rising privatization of port assets, higher container throughput, and growing investment in berth deepening, terminal expansion, and maintenance dredging.

Mining and energy companies, growing at a CAGR of 5.3% during the forecast period, continue to adopt dredging equipment for offshore oil & gas pipelines, extraction activities, and tailings management.

Meanwhile, government agencies remain the largest end-user group, reflecting their responsibility for national waterways, coastal protection, and port maintenance, though their growth is steadier at a CAGR of 4.3% during the forecast period. Overall, the continued development of infrastructure and energy transition initiatives continues to shape end-user demand.

Dredging Equipment Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Regionally, Asia Pacific dominates the dredging equipment market share and records the fastest growth, with a 6.1% CAGR (2025–2032). This reflects aggressive port capacity additions, large-scale land reclamation, and coastal industrial zone development in China, India, Southeast Asia, and other emerging economies. Intensifying container traffic and government-backed infrastructure programs are contributing directly into higher demand for large hydraulic dredgers and supporting equipment.

Asia Pacific Dredging Equipment Market Size,2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America and Europe

North America, growing at a CAGR of 5.5% during the forecast period, benefits from port deepening for larger vessels, coastal resilience projects, and the build-out of offshore wind capacity along the U.S. East Coast. Europe shows steady 4.6% growth, supported by stringent environmental requirements, channel maintenance, and mature offshore wind activity. The U.S. dominates regional demand, accounting for nearly 70% of the market in 2024, driven by U.S. Army Corps of Engineers (USACE) programs and major port-deepening works.

- In 2023, the USACE announced over USD 1.7 billion in dredging and harbor-maintenance allocations under the Bipartisan Infrastructure Law, underscoring the long-term federal commitment to waterway infrastructure.

Middle East & Africa and South America

Middle East & Africa (4.0% CAGR) over the forecast period, continues to invest in flagship ports, logistics hubs, and artificial islands, though spending is more cyclical. South America expands more moderately at a CAGR of 3.6% during the forecast period, driven by selective port upgrades and commodity export corridors.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Companies’ Wide Range of Product Offerings with a Strong Distribution Network Supported their Leading Position

The global dredging equipment market is moderately fragmented, with a mix of established international players and specialized regional manufacturers.

Established manufacturers such as Royal IHC and Damen Shipyards Group hold strong strategic importance due to their extensive portfolios of advanced hydraulic dredgers, long-term collaborations with port authorities, and proven expertise in large-scale land reclamation and deep-water dredging projects. Emerging Asian companies, including Qingzhou Julong Environment Technology Co., Ltd. and Shandong Haohai Dredging Equipment Co., Ltd., are gaining prominence by offering cost-effective, adaptable solutions that cater to rapidly expanding infrastructure markets across China, Southeast Asia, and Africa.

North American players such as Ellicott Dredges and DSC Dredge remain significant due to their specialized equipment designed for government-led waterway maintenance and industrial applications. Overall, competition is shaped by innovation in eco-friendly engines, automation, and modular dredging systems, as companies strive to meet evolving environmental regulations and rising demand for efficient, high-capacity dredging solutions.

LIST OF KEY DREDGING EQUIPMENT COMPANIES PROFILED

- Damen Shipyards Group N.V. (Netherlands)

- Dragflow S.r.l. (Italy)

- Dredge Yard (UAE)

- DSC Dredge, LLC (U.S.)

- Ellicott Dredges, LLC (U.S.)

- Italdraghe S.p.A. (Italy)

- Leader Dredger Co., Ltd. (China)

- Qingzhou Julong Environment Technology Co., Ltd. (China)

- Royal IHC (Netherlands)

- Shandong Haohai Dredging Equipment Co., Ltd. (China)

- SRS Crisafulli, Inc. (U.S.)

- VMI Dredges, Inc. (U.S.)

- Bell Dredging Pumps B.V. (Netherlands)

- ECTMarine B.V. (Netherlands)

- Shijiazhuang Pump Industry Group Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- May 2025: HID Dreges launched a new Cutter Suction Dredger (CSD) in Saudi Arabia. The CSD features a discharge distance of 1,500 meters, a flow capacity of 1,200 cubic meters per hour, and a dredging depth of up to 10 meters. This addition enhances HID's presence in the Middle East and contributes to the region's dredging capabilities.

- March 2025: The Dutra Group contracted with Eastern Shipbuilding Group to construct the 10,464 cubic yard Trailing Suction Hopper Dredge “Adele”. This new hopper dredge expands Dutra’s fleet capacity for U.S. waterways maintenance and deepening projects.

- October 2024: HID Dredges announced the upcoming launch of its fourth-generation amphibious dredger scheduled for mid-October 2024. The new amphibious machine is designed to offer innovative solutions for dredging, environmental protection, and construction projects, with a focus on reducing ecological disruption during operations

August 2024: Dredge Yard partnered with Dockyard and Engineering Works Ltd in Bangladesh to construct a Cutter Suction Dredger (CSD400). Dredge Yard supplied key components, such as the dredge pump, gearbox, engine, and cutter system. This collaboration aims to reduce transportation costs, stimulate the local economy, and enhance the skills of local engineers and shipyard workers. - March 2024: Van Oord commenced maintenance dredging operations at the Port of Krishnapatnam, India, with plans to dredge approximately 5 million cubic meters of material.

REPORT COVERAGE

The market analysis provides an in-depth study of the market size and forecast for all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market CAGR during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Application, End-User, and Region |

| By Product Type |

|

| By Application |

|

| By End-User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 7.04 billion in 2025 and is projected to reach USD 11.26 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 2.75 billion.

The market is expected to exhibit a CAGR of 5.3% during the forecast period of 2026-2034.

The hydraulic dredgers segment led the market by product type in 2025.

The key factors driving the market growth are supported by increasing demand for high-capacity, continuous dredging solutions needed for large port-deepening, land reclamation, and coastal protection projects.

Royal IHC and Damen Shipyards Group are of the prominent players in the market.

Asia Pacific dominated the market in 2025 with the largest share.

Rising port expansion needs, coastal urbanization, offshore energy development, and advancements in efficient, eco-friendly dredging technologies are the key factors expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us