Dyslipidemia Drugs Market Size, Share & Industry Analysis, By Drug Class (Statins, PCSK9 Inhibitors, Cholesterol Absorption Inhibitors, Fibrates, Prescription Omega-3 Therapies, ATP Citrate Lyase Inhibitors, & Others), By Disease Indication (Mixed Dyslipidemia, Primary/Familial Hypercholesterolemia, Established Cardiovascular Disease, Diabetes/Metabolic Syndrome-associated Dyslipidemia, and Others), By Age Group, By Route of Administration (Oral, Subcutaneous, & Others), By Distribution Channel (Hospital Pharmacies, Drug Stores, Retail or Online Pharmacies), & Regional Forecast, 2026-2034

Dyslipidemia Drugs Market Size and Future Outlook

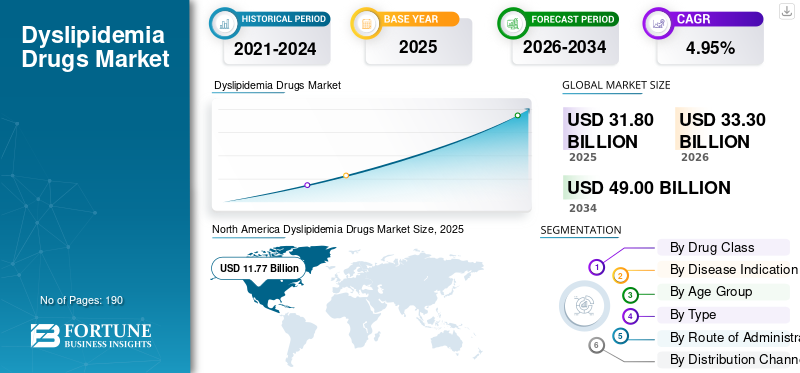

The global dyslipidemia drugs market size was valued at USD 31.80 billion in 2025. The market is projected to grow from USD 33.30 billion in 2026 to USD 49.00 billion by 2034, exhibiting a CAGR of 4.95% during the forecast period. North America dominated the dyslipidemia drugs market with a market share of 37.01% in 2025.

The global dyslipidemia drugs market is expected to witness steady growth, driven by the rising burden of high cholesterol and related cardiovascular risk globally. As screening rates improve and treatment guidelines increasingly emphasize earlier and stronger LDL-C control, more patients are being placed on long-term lipid-lowering therapy. These factors are supporting demand for widely used statins and combination therapies. As a result, pharmaceutical companies are expanding their focus on advanced dyslipidemia therapies, helping improve treatment access, expand physician adoption, and support market growth.

- For instance, in July 2025, Novartis announced that the U.S. FDA approved a label update for Leqvio (inclisiran), enabling its use as monotherapy along with diet and exercise to reduce LDL-C in adults with hypercholesterolemia. This development reflects how companies in the market are broadening the clinical use of next-generation cholesterol-lowering therapies to reach more patients earlier in the treatment pathway, thereby strengthening product uptake and expanding the commercial opportunity in dyslipidemia management.

Furthermore, major players, such as Amgen Inc., Novartis AG, Esperion Therapeutics, Inc., and Regeneron Pharmaceuticals, Inc., are expanding their offerings.

Download Free sample to learn more about this report.

DYSLIPIDEMIA DRUGS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 31.80 billion

- 2026 Market Size: USD 33.30 billion

- 2034 Forecast Market Size: USD 49.00 billion

- CAGR: 4.95% from 2026-2034

- North America secured a 37.01% share of the dyslipidemia drugs market in 2025.

- The ATP citrate lyase inhibitors segment is projected to witness a 20.10% CAGR during the forecast period.

- The familial hypercholesterolemia segment is anticipated to register a 8.84% CAGR during the forecast period.

North America

North America was valued at USD 11.30 billion in 2024 and increased to USD 11.77 billion in 2025 while maintaining its leading position.

Europe

Europe is projected to grow at a CAGR of 4.33% over the coming years, the second-highest among all regions, and reach a valuation of USD 8.73 billion by 2026.

Asia Pacific

Asia Pacific is projected to reach USD 8.62 billion by 2026, retaining its position as the third-largest regional market.

U.S.

The U.S. market is projected to reach USD 11.30 billion in 2026, accounting for approximately 33.95% of the global market.

Japan

The Japanese market is estimated at around USD 1.51 billion in 2026, accounting for approximately 4.53% of the global market.

Read More

DYSLIPIDEMIA DRUGS MARKET TRENDS

Shift Toward Advanced Lipid-Lowering Therapies Beyond Statins is a Prominent Trend Observed

The shift toward advanced lipid-lowering therapies beyond statins is emerging as a key trend in the global market. A large share of patients do not achieve recommended LDL-C targets with statins alone or cannot tolerate high-intensity statin treatment. This is increasing the need for newer options such as PCSK9 inhibitors, siRNA-based therapies, and other non-statin agents that can deliver deeper and more sustained cholesterol reduction. As physicians focus more on residual cardiovascular risk and on guideline-driven intensification of therapy, demand is shifting away from traditional first-line drugs toward targeted, outcome-oriented treatment approaches. As a result, companies are investing more in expanding indications, strengthening evidence, and improving access to next-generation dyslipidemia therapies, which is shaping market trends.

- For instance, in August 2025, Amgen received approval from the U.S. FDA for broadened use of Repatha (evolocumab) to include adults at increased risk for major adverse cardiovascular events due to uncontrolled LDL-C, removing the prior requirement for established cardiovascular diseases. Such development expands treatment adoption and supports future global market growth.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Prevalence of Hypercholesterolemia and Cardiovascular Disorders Driving Market Growth

The rising prevalence of hypercholesterolemia and cardiovascular disorders is a major driver for the global dyslipidemia drugs market growth. A growing number of patients are being identified with elevated LDL-C levels and long-term cardiovascular risk, elevating demand. As cholesterol disorders remain closely linked with heart attack, stroke, and other atherosclerotic conditions, healthcare systems and physicians are placing greater focus on early diagnosis and sustained lipid control. This is increasing the use of both established therapies and newer non-statin drugs for patients who need deeper cholesterol reduction or have persistent uncontrolled lipid levels. As a result, the expanding high-risk patient pool is supporting stronger demand for dyslipidemia drugs across prevention, chronic management, and cardiovascular risk-reduction settings.

- For instance, in March 2026, Esperion received multiple Class 1 recommendations in the 2026 ACC/AHA Multisociety Guideline for Management of Dyslipidemia for bempedoic acid. This development shows that as the burden of dyslipidemia and related cardiovascular complications continues to grow, companies are gaining stronger clinical positioning for therapies that help reduce LDL-C and cardiovascular risk, which supports broader physician adoption and market expansion.

MARKET RESTRAINTS

High Cost and Access Restrictions for Advanced Lipid-Lowering Therapies to Restrain Market Growth

The key restraint that the global market faces is high cost and access restrictions. Although newer therapies such as PCSK9 inhibitors and other advanced non-statin drugs offer strong LDL-C reduction, their higher treatment cost and payer restrictions continue to limit wider adoption. As these therapies often require prior authorization, step edits, or higher patient cost-sharing, many eligible patients face delays in starting treatment or do not receive approval at all. This reduces real-world utilization even when clinical need is high, which slows the commercial uptake of premium dyslipidemia drugs. As a result, market growth remains constrained by the gap between clinical value and practical patient access, especially in reimbursement-sensitive healthcare systems.

- For instance, in April 2025, The Pharmaceutical Journal reported that although NHS England increased funding support for inclisiran (Leqvio), uptake remained slower than expected. The article noted that NHS England had to extend funding arrangements and adjust reimbursement mechanisms, indicating that even clinically valuable dyslipidemia therapies can face practical adoption barriers linked to implementation, funding flows, and access at the provider level.

MARKET OPPORTUNITIES

Expansion of Next-Generation Lipid-Lowering Therapies Creating New Growth Opportunities for Market

The global market is seeing strong growth opportunities, as many patients still do not achieve target LDL-C levels with conventional therapy alone. In contrast, others require more convenient and effective treatment options beyond standard statins. These factors are driving global market demand for next-generation therapies, such as oral PCSK9 inhibitors, siRNA-based drugs, and other novel lipid-lowering agents, to improve cholesterol control across broader patient groups. As these newer therapies move through late-stage development and expand the available treatment pathway, they are creating a meaningful opportunity for companies to expand access, strengthen differentiation, and drive future market growth.

- For instance, in September 2025, Merck announced positive Phase 3 results for enlicitide decanoate, its investigational oral PCSK9 inhibitor, in adults with hypercholesterolemia. The drug met all primary and key secondary endpoints in the pivotal CORALreef Lipids study and described it as the first oral PCSK9 inhibitor to show statistically significant and clinically meaningful LDL-C reduction in Phase 3 trials. Such developments are anticipated to create new market growth opportunities in dyslipidemia management.

MARKET CHALLENGES

Poor Long-Term Patient Adherence Limits Treatment Effectiveness and Market Expansion

The global market faces a challenge as treatment success depends heavily on long-term patient adherence, but many patients discontinue or inconsistently use lipid-lowering therapy over time. Since dyslipidemia is usually a lifelong condition and often remains symptomless in the early stages, many patients do not feel an immediate benefit from continuing daily medication, which weakens persistence. This becomes a greater challenge when patients experience side-effect concerns, pill burden, low risk awareness, or poor follow-up support from healthcare systems. As a result, real-world treatment continuity remains weaker than expected, reducing LDL-C goal achievement, limiting the full value of prescribed therapies, and slowing the overall growth potential of the market.

- For instance, in May 2025, EClinicalMedicine published an article highlighting that poor adherence to lipid-lowering medications remains a barrier to reducing the burden of cardiovascular disease, even though these therapies are well established in practice. Such factors limit prescription continuity and the broader commercial potential of dyslipidemia drugs.

Segmentation Analysis

By Drug Class

Wide Prescription Volume of Statins Led to Segmental Dominance

Based on drug class, the market is categorized into statins, PCSK9 inhibitors, cholesterol absorption inhibitors, fibrates, prescription omega-3 therapies, ATP citrate lyase inhibitors, and others.

Among these, the statins dominated the dyslipidemia drugs market share, as they remain the first-line and most widely prescribed treatment for lowering LDL cholesterol across a broad patient population. Their long clinical history, strong physician familiarity, proven cardiovascular risk-reduction benefit, and wide availability in low-cost versions make them the most commonly used therapy in routine dyslipidemia management. Since many patients begin treatment with statins before moving to advanced or add-on therapies, prescription volume remains heavily concentrated in this class. As a result, statins continue to hold the largest market share due to their strong clinical acceptance, affordability, and broad use across both primary and secondary prevention settings.

- For instance, in October 2025, Sunshine Biopharma Inc. announced that its Canadian subsidiary, Nora Pharma Inc., launched Pravastatin, a generic version of the cholesterol-lowering medication Pravachol.

The ATP citrate lyase inhibitors segment is expected to grow at a CAGR of 20.10% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

Early Approval of Dyslipidemia Drugs for Primary Hypercholesterolemia Diseases Led to Dominance of Segment

Based on disease indication, the market is segmented into primary hypercholesterolemia, mixed dyslipidemia, hypertriglyceridemia, familial hypercholesterolemia, established cardiovascular disease/secondary prevention, diabetes/metabolic syndrome-associated dyslipidemia, and others.

In 2025, the primary hypercholesterolemia segment dominated the market as it was the most commonly diagnosed and routinely treated dyslipidemia in clinical practice. A high number of patients are identified with elevated LDL-C before they develop major cardiovascular complications, which makes this indication the main entry point for long-term lipid-lowering therapy. Since treatment guidelines strongly emphasize early cholesterol control to reduce future cardiovascular risk, more prescriptions are concentrated in this segment than in narrower or more complex indications. As a result, primary hypercholesterolemia continues to account for the largest share of demand, supported by broad screening, earlier diagnosis, and long-duration therapy use.

- For instance, in July 2025, Novartis AG received U.S. FDA approval for Leqvio (inclisiran), enabling its use as monotherapy with diet and exercise to reduce LDL-C in adults with hypercholesterolemia. This development shows how companies are expanding products directly into the large primary hypercholesterolemia treatment pool, which supports the segment’s leading market position.

The familial hypercholesterolemia segment is projected to grow at a CAGR of 8.84% during the forecast period.

By Age Group

Larger Adult Patient Pool Boosted Segmental Growth

Based on age group, the market is segmented into pediatric, adult, and geriatric.

In 2025, adult segment dominated the market based on age group. The high share is allocated as dyslipidemia is most commonly diagnosed, monitored, and treated in the adult population, where cholesterol abnormalities and long-term cardiovascular risk are much more widely recognized. Adults are also the main group targeted for routine screening, preventive therapy, and long-term prescription use, especially in patients with obesity, diabetes, hypertension, or other cardiometabolic risk factors. As a result, adults represent the largest treated population in the market.

- For instance, in August 2025, Amgen received approval from the U.S. FDA for broadened use of Repatha (evolocumab) to include adults at increased risk for major adverse cardiovascular events due to uncontrolled LDL-C. This reflects the adult population's continued status as the main target for treatment expansion in dyslipidemia care, reinforcing the segment’s dominance.

The geriatric segment is projected to grow at a CAGR of 5.90% during the forecast period.

By Type

Greater Access Provided by Generics Boosted Segmental Growth

Based on type, the market is segmented into branded and generics.

In 2025, the generics type dominated the market. Generics offer affordability in prescribing and patient continuation. Many of the most commonly used lipid-lowering molecules, especially statins, are available in generic form, allowing physicians and payers to manage a large patient pool at lower cost. These factors enable them to offer high accessibility, lower price, and broad everyday use in chronic care. Key pharmaceutical companies are focusing on strategic collaborations and expanding their product offerings.

- For instance, in December 2025, Dr. Reddy’s announced the submission of a U.S. Drug Master File for a continuous manufacturing process for Atorvastatin Calcium Trihydrate API to the U.S. FDA. This development highlights continued investment in the supply chain behind one of the world’s most widely used generic cholesterol medicines, underscoring the role of generic manufacturing strength in supporting dominance in the dyslipidemia market.

The branded segment is projected to grow at a CAGR of 7.06% during the forecast period.

By Route of Administration

Ease of Administration of the Oral Route of Administration Boosted Segmental Growth

Based on route of administration, the market is segmented into oral, subcutaneous, and others.

In 2025, oral drugs dominated the market as they are easier to prescribe, easier for patients to use, and better suited for long-term daily management of chronic lipid disorders. Most first-line dyslipidemia therapies, including statins, cholesterol absorption inhibitors, fibrates, and several newer agents, are taken orally, which supports stronger physician preference and wider patient acceptance. Since oral treatment fits more easily into routine outpatient care and long-duration therapy, it captures a much larger treated population than injectable options. As a result, the oral route continues to dominate the market due to its convenience, familiarity, and broad role in first-line care.

- For instance, in September 2025, Merck announced that its investigational oral PCSK9 inhibitor enlicitide decanoate met all primary and key secondary endpoints in the pivotal CORALreef Lipids Phase 3 study in adults with hypercholesterolemia. This shows that even innovation in advanced lipid-lowering therapies is moving toward oral formulations, further strengthening the dominance of the oral route in the market.

The subcutaneous segment is projected to grow at a CAGR of 13.82% during the forecast period.

By Distribution Channel

Vast Distribution Network of Drug Stores & Retail Pharmacies Led Growth in Segment

Based on distribution channel, the market is segmented into hospital pharmacies, drug stores & retail pharmacies, and online pharmacies.

By distribution channel, the drug stores & retail pharmacies dominated the market as dyslipidemia drugs are mainly used in the outpatient setting and are refilled regularly over long treatment periods. Patients usually obtain cholesterol-lowering medicines through nearby community pharmacies as these channels offer convenience, repeat dispensing, pharmacist support, and broad access to both branded and generic oral therapies. Since dyslipidemia management often does not require hospital-based dispensing, retail outlets handle a larger share of routine prescription volume. As a result, drug stores and retail pharmacies continue to dominate distribution due to their accessibility, refill-based purchasing patterns, and strong role in chronic disease medication supply.

- For instance, in October 2025, CVS Health released its 2025 Rx Report, highlighting how community pharmacy is continuing to expand its role in patient care, supported by CVS Pharmacy’s broad nationwide retail presence.

The online pharmacies segment is projected to grow at a CAGR of 11.42% over the study period.

Dyslipidemia Drugs Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Dyslipidemia Drugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 11.30 billion and maintained its leading position in 2025 at USD 11.77 billion. The market is growing due to the high burden of obesity, diabetes, and cardiovascular risk, along with strong cholesterol screening and updated ACC/AHA dyslipidemia guidelines that support earlier and broader lipid-lowering treatment. Wider use of non-statin therapies and good diagnosis rates also support prescription growth.

U.S. Dyslipidemia Drugs Market

Given North America's substantial contribution, and the U.S. dominance in the region, the U.S. market is estimated to be valued at around USD 11.30 billion in 2026, accounting for roughly 33.95% of the global market.

Europe

Europe is projected to grow at a CAGR of 4.33% over the coming years, the second-highest among all regions, and reach a valuation of USD 8.73 billion by 2026. A large cardiovascular disease burden, strong guideline-led cholesterol management, and increasing focus on newer LDL-lowering therapies in high-risk patients are supporting growth in the region.

U.K. Dyslipidemia Drugs Market

The U.K. market is estimated to be valued at around USD 1.65 billion in 2026, representing roughly 4.96% of the global market.

Germany Dyslipidemia Drugs Market

Germany's market is projected to reach a valuation of approximately USD 2.16 billion in 2026, equivalent to around 6.47% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 8.62 billion in 2026 and secure the position of the third-largest region in the market. The market is expanding as cardiovascular disease remains a major health burden across Asia, while urbanization, diabetes, and lifestyle changes are increasing dyslipidemia risk.

Japan Dyslipidemia Drugs Market

The Japanese market is estimated at around USD 1.51 billion in 2026, accounting for approximately 4.53% of the global market.

China Dyslipidemia Drugs Market

China's market is projected to be one of the largest globally, with 2026 revenues estimated at around USD 3.12 billion, representing approximately 9.35% of global sales.

India Dyslipidemia Drugs Market

The Indian market is estimated at around USD 1.35 billion in 2026, accounting for roughly 4.06% of global revenue.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The market in Latin America is estimated to reach a valuation of USD 2.36 billion during the forecast period. Growth is driven by rising non-communicable disease burden and stronger regional efforts to improve cardiovascular risk management through primary care programs such as HEARTS in the Latin America. This is improving the identification and treatment of cholesterol-related risk in routine care.

GCC Dyslipidemia Drugs Market

The GCC market is set to reach a valuation of USD 0.56 billion in 2026.

South Africa Dyslipidemia Drugs Market

The South African market is projected to reach approximately USD 0.20 billion by 2026, accounting for roughly 0.60% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

New Product Launches by Key Players to Propel Market Progress

The global dyslipidemia drugs market is highly consolidated, with companies such as Amgen Inc., Novartis AG, Esperion Therapeutics, Inc., Regeneron Pharmaceuticals, Inc., Sanofi, and Viatris Inc. holding significant market share. Strategic partnerships, new product launches, and regulatory approvals in the sector drive these companies' market share gains.

- For instance, in July 2025, Novartis AG received a label update from the U.S. FDA for Leqvio (inclisiran), enabling its use as monotherapy, along with diet and exercise,

Other notable players in the global market include Pfizer Inc., Merck & Co., Inc., and Dr. Reddy’s Laboratories Ltd. These companies are expected to prioritize strategic collaborations and new product launches to strengthen their positions during the forecast period.

LIST OF KEY DYSLIPIDEMIA DRUGS COMPANIES PROFILED IN REPORT

- Amgen Inc. (U.S.)

- Novartis AG (Switzerland)

- Esperion Therapeutics, Inc. (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Sanofi (France)

- Viatris Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Reddy’s Laboratories Ltd. (India)

- Lupin Limited (India)

KEY INDUSTRY DEVELOPMENTS

- December 2025: LIB Therapeutics Inc. received approval from the U.S. FDA for LEROCHOL (lerodalcibep-liga) injection for subcutaneous use as an adjunct to diet and exercise to reduce low-density lipoprotein cholesterol (LDL-C) in adults with hypercholesterolemia, including Heterozygous Familial Hypercholesterolemia (HeFH).

- September 2025: Merck & Co., Inc., announced positive topline results from the Phase 3 CORALreef Lipids trial evaluating the safety and efficacy of enlicitide decanoate, an investigational, once-daily oral proprotein convertase subtilisin/kexin type 9 (PCSK9) inhibitor being evaluated for the treatment of adults with hypercholesterolemia on a moderate or high intensity statin (or with documented statin intolerance).

- May 2025: Shanghai Junshi Biosciences Co., Ltd received approval for two supplemental new drug applications for the ongericimab injection, a PCSK9-targeted drug from the National Medical Products Administration for adult patients with heterozygous familial hypercholesterolemia alone or in combination with ezetimibe, in adult patients with non-familial hypercholesterolemia and mixed dyslipidemia who are statin-intolerant or statins contraindicated.

- May 2025: Esperion Therapeutics partnered with HLS Therapeutics to commercialize NEXLETOL and NEXLIZET in Canada.

- March 2025: CSL Seqirus collaborated with Esperion Therapeutics to commercialize Nexletol (bempedoic acid) and Nexlizet (bempedoic acid/ezetimibe) in Australia and New Zealand. Bempedoic acid inhibits adenosine triphosphate-citrate lyase, a factor in low-density lipoprotein cholesterol (LDL-C) synthesis in the liver.

REPORT COVERAGE

The global dyslipidemia drugs market report covers a detailed analysis of the industry across key drug classes, disease indications, age groups, product types, routes of administration, and distribution channels. It evaluates how the rising burden of cholesterol disorders, growing cardiovascular risk, increasing use of long-term lipid-lowering therapy, and expanding adoption of both conventional and advanced drugs are shaping market demand. The study also examines the impact of product innovation, generic competition, treatment access, pricing pressure, and changing prescribing patterns on overall market performance. In addition, it provides regional insights, competitive landscape analysis, and recent company developments such as product launches, approvals, partnerships, and collaborations that are influencing market growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.95% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Drug Class, Disease Indication, Age Group, Type, Route of Administration, Distribution Channel, and Region |

| By Drug Class |

|

| By Disease Indication |

|

| By Age Group |

|

| By Type |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 31.80 billion in 2025 and is projected to reach USD 49.00 billion by 2034.

In 2025, the market value stood at USD 11.77 billion.

The market is expected to grow at a CAGR of 4.95% over the forecast period of 2026-2034.

The statin drug class segment is expected to lead the market.

The market is driven by the rising prevalence of hypercholesterolemia and cardiovascular disorders, elevating demand.

Amgen Inc., Novartis AG, Esperion Therapeutics, Inc., Regeneron Pharmaceuticals, Inc., and Sanofi are the top players in the market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us