Elderly Care Market Size, Share & Industry Analysis, By Service Facility (Home Care and Public/Private), By Service Type (Personal Care, Companion Care, Homemaking, Rehabilitation/Recovery, and Others), By Care Type (Live in Care, Visting Care, and Respite Care), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

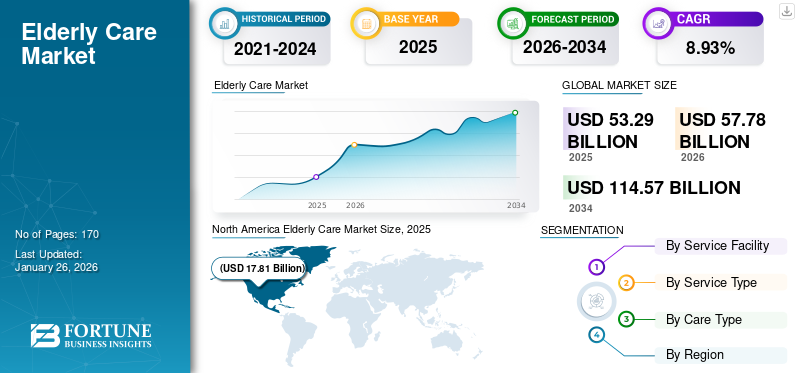

The global elderly care market size was valued at USD 53.29 billion in 2025 and is projected to grow from USD 57.78 billion in 2026 to USD 114.57 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 8.93% over the forecast period. North America dominated the elderly care market with a market share of 33.43% in 2025.

The elderly care services market encompasses a range of services provided to meet the healthcare, daily living, and emotional needs of older adults, typically aged 65 and above. These services aim to assist seniors in maintaining a quality life, often due to age-related physical, cognitive, or emotional challenges. The market includes a wide variety of offerings, such as home healthcare and public/private centers, including assisted living facilities, adult day care centers, and nursing homes. A distinctive aspect of this industry is that, despite the presence of international players, domestic players still have their own space in the market. Therefore, the market is anticipated to remain highly fragmented in the upcoming years.

Download Free sample to learn more about this report.

Global Elderly Care Market Overview

Market Size:

- 2025 Value: USD 53.29 billion

- 2026 Value: USD 57.78 billion in 2025

- 2034 Forecast Value: USD 114.57 billion, with a CAGR of 8.93% from 2026–2034

Market Share:

- Regional Leader: North America held a 33.43% market share in 2025, driven by high healthcare spending, a strong presence of long-term care facilities, and progressive reimbursement policies.

- Fastest-Growing Region: Asia Pacific is expected to witness the highest CAGR, fueled by a rapidly aging population, increasing life expectancy, and expanding healthcare access in countries like China and India.

- Facility Leader: The Home Healthcare segment led the market in 2023, accounting for 58% of the global share, driven by preference for aging in place and lower cost of home-based services.

Industry Trends:

- Rise of At-home Care: Increasing preference among the elderly for receiving care in their homes has accelerated demand for personal care, companionship, and home medical services.

- Telehealth & Remote Monitoring: Adoption of remote patient monitoring (RPM), wearable devices, and virtual consultations is transforming care delivery and improving patient safety.

- Technology-Driven Services: AI-based assistance, smart home integration, and health monitoring tools are enabling autonomy and quality of life for seniors.

Driving Factors:

- Aging Global Population: Rising life expectancy and growth in the population aged 65+ is significantly increasing demand for elderly care services across all regions.

- Chronic Disease Burden: High prevalence of age-related diseases like Alzheimer’s, Parkinson’s, diabetes, and cardiovascular conditions drives long-term care and rehabilitation services.

- Caregiver Support Demand: Increasing need for live-in, visiting, and respite care services amid a shortage of skilled professionals is reshaping the elderly care delivery landscape.

- Digital Transformation: Integration of telemedicine, AI, and health apps enables efficient, continuous care, especially in remote and underserved areas.

- Government & Non-profit Support: Active involvement of public institutions, NGOs, and policy incentives plays a crucial role in making elderly care more accessible and affordable.

Key players such as Helping Hands Home Care, CK Franchising Inc., Home Instead, Inc. and Interim Healthcare Inc., focus on telehealth, remote monitoring, and caregiving platforms to enhance service delivery and customer engagement. These companies appeal to tech-savvy demographics and promote flexible, scalable care options.

ELDERLY CARE MARKET TRENDS

At-home Care to Emerge as a Prominent Trend

The pandemic sidelined some healthcare trends while fast-tracking others, and at-home care services clearly belong to the second category. A key trend in the market is the rise of home-based care services, driven by increasing demand for aging in place. Geriatric individuals prefer staying in their familiar environment rather than moving to assisted living facilities or community care facilities. Thus, home healthcare services, including personal care, companionship, and medical assistance, have witnessed growth in the last couple of years. This trend is supplemented by advancements in telehealth and wearable technologies that enable caregivers to monitor patients remotely. Tools such as RPM (Remote Patient Monitoring) offer a continuous stream of real-time feed, and it is estimated that over 1 in 4 people will use RPM tools by 2025.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Expanding Aging Population and Longevity to Favor Market Expansion

As life expectancy increases globally, the proportion of elderly individuals is rising significantly, contributing to greater demand for senior care services. Older adults often face age-associated health concerns such as chronic diseases, mobility challenges, and cognitive decline, which necessitate a variety of care services. As healthcare improves globally, more people are living longer, leading to a significant rise in the elderly demographic. According to the United Nations Department of Economic and Social Affairs, by 2050, it is anticipated that the global population aged 65 and above will double, particularly in regions such as North America, Europe, and parts of Asia, fueling the need for comprehensive elderly careful planning and solutions.

Rising Incidence of Chronic Diseases and Disabilities to Fuel Market Growth

The elderly population is more prone to chronic conditions such as cardiovascular diseases, diabetes, neurodegenerative disorders such as Alzheimer’s and Parkinson’s, and dementia, requiring long term care and specialized services. Additionally, disabilities related to vision, mobility, and hearing impairments further contribute to the demand for senior care services. As the prevalence of these diseases rises with age, the demand for non-medical care services and rehabilitation services, along with assisted living facilities, grows. This demand is further supported by advances in healthcare technology, which enhance the ability to manage chronic conditions within the comfort of home, driving global elderly care market growth.

Market Restraints

Financial Constraints to Restrict Market Growth

Rising operational costs, including wages for skilled caregivers and healthcare professionals, contribute to higher service fees, making elderly care inaccessible for many individuals. Moreover, government funding and insurance coverage are often insufficient to meet the increasing demand for comprehensive elderly care services, including home healthcare, assisted living, and specialized medical treatments. Consequently, many elderly individuals and their families face challenges in accessing affordable senior care, particularly in low and middle-income regions such as the Middle East & Africa and parts of Asia Pacific, which hampers the overall expansion of the sector.

Market Challenge

Shortage of Skilled Caregivers

One of the significant challenges in the senior care market is the shortage of professional and skilled caregivers. With a growing aging population, the demand for trained professionals outpaces supply, leading to increased costs and inconsistent care quality. This gap highlights the need for workforce development, better compensation, and technology-driven solutions to meet rising needs.

Market Opportunity

Development of Technology-Driven Solutions

With an aging population, demand for smart home devices, health monitoring systems, and telehealth services is rapidly increasing. These innovations enable seniors to live safely at home while maintaining autonomy. Businesses offering wearable devices, remote monitoring, and AI-based assistance can tap into this growing need. Additionally, personalized care platforms and user-friendly designs can enhance the quality of life for elderly individuals and caregivers alike. Thus, developing technology-driven solutions for independent living offers lucrative growth opportunities for elderly care market.s

Impact of COVID-19

The COVID-19 pandemic negatively impacted the global elderly care market share in 2020 as a result of strict lockdown measures across countries, which limited physical movement across and disrupted service providers. However, the demand for home-based care services and telehealth solutions increased during the pandemic as families sought alternatives to institutional care in response to heightened risks in care facilities. This shift led to an increase in demand for at-home care services, while operational costs and staffing shortages further strained providers, making telemedicine crucial for maintaining care continuity. The long-term effects of the pandemic prompted a shift toward more personalized, remote, and technology-driven care models, while also raising awareness of the vulnerabilities within eldercare infrastructure. This shift pushed for reforms and increased investment to enhance service quality and resilience against future health crises.

SEGMENTATION ANALYSIS

By Service Facility

Increasing Popularity of Independent Care Offerings to Boost Demand for Home Healthcare Services

Based on service facility, the market is bifurcated into home healthcare and public/private.

The home care service facility segment is projected to dominate the market with a share of 59.05% in 2026, and is expected to maintain its prominent position during the forecast period. The segment’s growth is fueled by independent care offerings, convenience, and less expenditure of receiving care in the comfort of one’s home.

On the other hand, the public/private service facility segment is forecasted to grow at a considerable CAGR between 2024 and 2032. The public/private service segment includes adult day programs (ADP), adult day health care (ADHC), community care facilities, institutional care facilities, and assisted living facilities. The massive need for effective care services and better lifestyles for aged individuals and rising spending on non-medical care services aid in the segmental growth.

To know how our report can help streamline your business, Speak to Analyst

By Service Type

Increasing Incidences of Impaired Vision and Mobility Issues in Elderly Individuals to Fuel Demand for Homemaking Services

By service type, the market is divided into personal care, companion care, homemaking, rehabilitation/recovery, and others.

The homemaking segment is projected to dominate the market with a share of 32.58% in 2026, contributing the highest market share. This segment includes services such as meal preparation, changing bed linens, doing the laundry, vacuuming carpets or wooden floors, and running other errands. Elderly individuals with impaired vision, mobility issues, and other bedridden health conditions are most likely to require assistance in homemaking services, which reduces the added burden from the individuals on their daily routines.

The personal care service type held the second-largest share of the market in 2023. Elderly individuals with various health disorders often need support for a wide range of personal care needs. These services foster independence and help preserve self-esteem and dignity, allowing individuals to maintain their quality of life in the comfort of their own homes, which drives the segment’s growth.

Companion care is projected to grow at the fastest CAGR of 9.86% over the forecast period. These services offer meaningful companionship that enriches the lives of aged population by understanding their emotional and social well-being, fostering genuine connections, and enriching their experiences.

By Care Type

Increasing Need for Round-the-clock Care to Fuel Demand for Live in Care Services

Based on care type, the market is divided into live in care, visiting care, and respite care.

The live in care segment is projected to account for the 59.88% share of the market in 2026, due to its higher demand among the aged population compared to other care types. Live in care provides constant, round-the-clock care support from a skilled caregiver, allowing seniors to stay in the comfort of their own familiar surroundings while receiving essential support. This kind of care offers an environment full of fond memories, which can improve the care time and plan for an individual.

The visiting care segment is expected to grow exponentially with the fastest compound annual growth rate (CAGR). Such care plans offer support when one needs it while continuing to enjoy an independent, comfortable life at home. Additionally, the flexibility of visiting care services, ranging from just 30 minutes per week to several visits a day, allows to choose according to one's needs, making them ideal for conscious consumers.

The respite care segment is likely to capture 9.58% of the market share in 2025.

Elderly Care Market Regional Outlook

To know how our report can help streamline your business, Speak to Analyst

In terms of geography, the market is divided into North America, Europe, the Asia Pacific, and the rest of the world.

North America

North America Elderly Care Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the highest market share in 2026 due to its large spending on healthcare and non-medical services for the elderly. The North America market was valued at USD 17.81 billion in 2025, capturing 33.43% of global revenue, and is estimated to reach USD 19.26 billion in 2026. Other contributing factors include the presence of a wide variety of long-term care centers across the U.S. and the constant development of reimbursement policies.

The demand for elderly care in the U.S. market has been growing exponentially on account of rising spending on personal health and the overall healthcare industry. The U.S. market is projected to reach USD 16.09 billion by 2026. According to the National Library of Medicine, in 2020, more than 237,400 individuals were enrolled in Adult Day Services Centers (ADSCs) in the U.S.

Europe

Europe is expected to grow considerably, albeit at a slower pace than the Asia Pacific region, in the coming years. In 2025, Europe held 31.95% of the global market, reaching a valuation of USD 17.03 billion, and is projected to grow to USD 18.51 billion in 2026. The growth of the regional market is likely to be driven by the substantial presence of healthcare service providers and senior care centers catering to the aging population. Moreover, favorable compensation policies and an increased aging population prone to chronic ailments consolidate the European market. The UK market is projected to reach USD 2.49 billion by 2026, and the Germany market is projected to reach USD 3.36 billion by 2026.

Asia Pacific

The market in Asia Pacific reached USD 14.02 billion in 2025, representing 26.30% of total market revenue, and is projected to reach USD 15.3 billion in 2026. owing to high unmet medical requirements coupled with the large proportion of the aging population in countries such as China and India. Additionally, supportive healthcare facilities and a rise in the average life expectancy of individuals are likely to steer the growth of the industry in the years to come. The Japan market is projected to reach USD 1.57 billion by 2026, the China market is projected to reach USD 4.27 billion by 2026, and the India market is projected to reach USD 3.77 billion by 2026.

Rest of the World

Rising incidences of illnesses such as Alzheimer's disease, Parkinsons, or dementia among the older population and improving healthcare facilities in regions such as South America and the Middle East & Africa are expected to drive market growth. Furthermore, the role of autonomous charitable units, non-profit clinics, and government-sponsored institutions has been crucial in supporting market expansion. South America recorded a market size of USD 0.65 billion in 2025, capturing 5.22% of the global market share, and is projected to reach USD 0.67 billion in 2026. In 2025, the Middle East & Africa market stood at USD 1.59 billion, representing 2.99% of global demand, and is projected to grow to USD 1.68 billion in 2026.

Competitive Landscape

Key Industry Players

Key Players Emphasize on Digital Health technologies and Telemedicine Services to Stay Competitive

Key players in the market include both established healthcare organizations and emerging statups. Leading companies such as Johnson & Jonhson, Brookdale Senior Living, and Amedisys leverage their brand reputation, established networks, and financial strength to maintain competitive advantages. On the other hand, emerging startups, such as Honor and Homethrive, are harnessing technology to offer innovative solutions.

Key aspects such as compliance with regulatory bodies & policies, investment in research & development, and technological advancements assist in introducing the novel technique. Furthermore, collaboration with technology firms to develop products, such as platforms connecting caregivers with clients, improves transparency and offers easy booking and management.

Major Players in the Elderly Care Market

To know how our report can help streamline your business, Speak to Analyst

Helping Hands Home Care, CK Franchising, Inc., Rosewood Care Group, Living Assistance Services, and Interim HealthCare Inc., are some of the major players in the market. The market is highly modertly fragmented, with the top 5 players accounting for ~20% of the market share.

LIST OF KEY COMPANIES PROFILED IN THE REPORT:

- Helping Hands Home Care (U.K.)

- CK Franchising, Inc. (U.S.)

- Rosewood Care Group (Australia)

- Living Assistance Services (Canada)

- Interim HealthCare Inc. (U.S.)

- Home Instead, Inc. (U.S.)

- Right at Home, LLC (U.S.)

- Exceptional Living Centers (U.S.)

- Care24 Pvt Ltd. (India)

- Visiting Angels (U.S.)

Key Industry Developments:

- November 2024: Bangalore-based listed hospital chain Aster DM Healthcare and US-based private equity major Blackstone-owned Quality Care India reached the final steps of completing a merger, with Blackstone expected to hold a majority stake in the merged entity. This merger is likely to create a substantial healthcare conglomerate in India, enhancing the reach and capabilities of both organizations. In the foreseeable future, this merger would bring significant development to the Indian healthcare sector.

- May 2024: Kites Senior Care, a geriatric care service provider, announced that it has secured USD 5.33 million in a series A funding round, which was led by Ranjan Pai, chairman of Manipal Education and Medical Group (MEMG). This investment is planned to be utilized to deepen its network in cities such as Hyderabad, Bengaluru, and Chennai, while facilitating expansion into three additional cities across Southern India.

- March 2022: Ping An Insurance Company of China, Ltd. announced that its subsidiary, Ping An Life, launched an home-based elderly personalized care services. By combining Ping An's high-quality elderly care resources and healthcare ecosystem, the service brings together a professional "one-stop" elderly care service and insurance protection for customers, providing an easier and more affordable living experience.

- June 2021: Healthforce and Webrock Ventures partnered to launch telehealth products in South Africa. This new venture focuses on offering scheduled and on-demand consultations with nurses, mental health professionals, and practitioners to patients. The venture received a USD 3 million pre-series A round.

- April 2021: Quro Medical, a health tech startup in South Africa, closed a USD 1.1 million investment round, led by Mohau Equity Partners and Enza Capital. With this funding, the company aimed to offer acute patient care at home to improve the patient experience.

Investment Analysis and Opportunities:

Improved Personalized Care Solutions and Supportive Government Policies to Create Growth Opportunities

The elderly care market has noticed significant growth over the last few years, driven by increasing consumer spending on healthcare, improved technological advancements in medical technology, and favorable government policies. Furthermore, the shift toward home and community-based care supports investment in home care service providers and technologies that enable remote monitoring and telehealth. For instance, in February 2024, Caring Co., a South Korean startup offering senior care services, raised USD 30 million in a series B funding round. With this raised funding investment, the company plans to build and expand infrastructure for localized, government-funded diverse senior care services ranging from in-home care to caregiver center operations, nursing and bathing services. Many governments provide subsidies, tax incentives, and funding for elderly care, which boosts market growth and reduces risk for investors. From an investment perspective, investors are focusing on developing or acquiring assisted living and residential care facilities, especially in regions with high elderly populations. Furthermore, investors are also seeking to invest in advanced technologies such as telemedicine, healthcare robotics and AI, and digital health solutions, among others.

REPORT COVERAGE

The market research report provides a detailed analysis of the market and focuses on key aspects such as the competitive landscape, services types, and service facilities. It also offers market trends and highlights key industry developments. In addition to the aforementioned factors, the report on the global market outlook outlines several factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.93% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Service Facility

|

|

By Service Type

|

|

|

By Care Type

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global elderly care market was valued at USD 53.29 billion in 2025 and is projected to reach USD 114.57 billion by 2034, growing at a CAGR of 8.93% during the forecast period.

The market will grow at a CAGR of 8.93% and exhibit a steady growth rate during the forecast period.

Rising life expectancy and a growing aging population are key drivers, along with increased incidences of chronic diseases like Alzheimers and Parkinsons, which raise demand for long-term care services globally.

North America dominated the elderly care market with a market share of 33.43% in 2025.

Elderly care services include personal care, homemaking, companion care, rehabilitation, and live-in or visiting care. Home healthcare is the leading service facility, preferred for its cost-effectiveness and comfort.

Technology-driven solutions like telehealth, remote patient monitoring (RPM), and AI-based care platforms are enabling seniors to receive personalized care at home, enhancing independence and care quality.

A major challenge is the global shortage of skilled caregivers, which limits service scalability and raises operational costs. Financial constraints also restrict access to quality care in low-income regions.

Key players include Helping Hands Home Care, CK Franchising, Interim HealthCare Inc., and Home Instead, Inc. These companies focus on digital health, remote caregiving, and scalable service models.

- 2021-2034

- 2025

- 2021-2024

- 170

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us