Electric Ship Market Size, Share & Industry Analysis, By Ship Type (Commercial Ship and Passenger Ship), By Mode of Operation (Semi-autonomous and Fully Autonomous), By Power Output (Up to 745 kW, 746-7560 kW, and Above 7560 kW), By Propulsion Type (Hybrid and Fully Electric), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

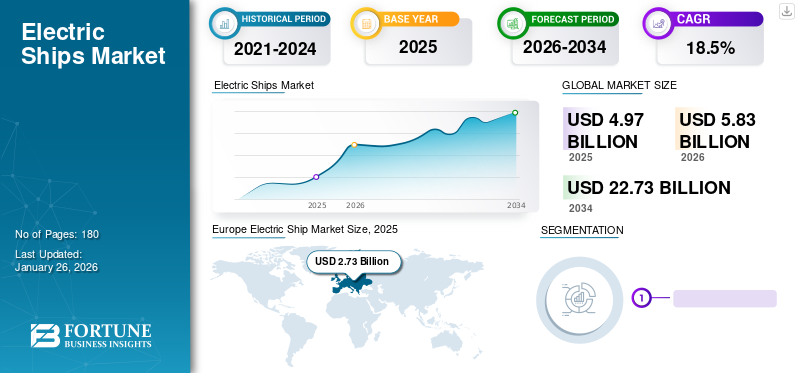

The global electric ship market size was valued at USD 4.97 billion in 2025 and is projected to grow from USD 5.83 billion in 2026 to USD 22.73 billion by 2034, exhibiting a CAGR of 18.5% during the forecast period. Europe dominated the electric ship market with a market share of 54.90% in 2025.

An electric ship is powered by an electric drive system, such as full battery electric and electric hybrid ship. Electric vessels use renewable energy sources such as wind turbines and solar panels. A hybrid ship consists of a fuel-powered engine as the primary source and an electric motor as an auxiliary power source. The market expansion is driven by rising demand for hybrid and fully electric vessels such as ferries, yachts, cruise ships, container ships, and cargo ships. The major factors contributing to the market growth include reducing carbon emissions, push for zero-emission transport systems, and advances in energy storage systems. Moreover, the adoption of electric ships is increasingly becoming popular due to their environment-friendliness, energy efficiency, and cost of running efficiency.

Driving Factors:

- Stringent environmental regulations and global decarbonization targets driving the maritime sector toward cleaner propulsion systems.

- Increasing investment in electric and hybrid marine technologies to reduce operational costs and maintenance.

- Rising popularity of zero-emission vessels, especially in passenger transport and inland shipping sectors, supported by government and private sector initiatives.

The need for electric ship will arise as conventional ships emit more gasoline substances that cause environmental pollution. Also, most gas carriers, oil tankers, cruises, general cargo, and container ships utilize heavy diesel oil for operation. The worldwide fleet of around 90,000 ships produces nearly 20 million tons (Mt) of sulfur dioxide and consumes about 370 Mt of fuel yearly. Similarly, marine vessels (diesel) are used for inland shipping, which is less polluting than heavy oil. The growing maritime trade and tourism will result in the increased emission of exhaust gases by these ships. Thus, this will result in clean (green-electric) transporting ships in the coming years.

The electric ship market witnessed significant challenges during the COVID-19 pandemic. The pandemic had majorly impacted the shipping and maritime industry from the ports of China and across the globe. The electric shipping industry had been majorly influenced due to the port closures, less demand for cargo, disputes in laytime settlement and bank factors that affected the overall shipping industry.

Download Free sample to learn more about this report.

ELECTRIC SHIP MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 4.97 Billion

- 2026 Market Size: USD 5.83 Billion

- 2034 Forecast Market Size: USD 22.73 Billion

- CAGR: 18.5% from 2026–2034

- Europe dominated the electric ship market with a 54.90% share in 2025.

- The hybrid propulsion segment is expected to hold the largest share of 73.48% in 2026.

- The 746–7560 kW power output segment is projected to account for 66.33% of the market in 2026.

North America

North America generated USD 0.55 billion in 2025 and is projected to reach USD 0.63 billion in 2026 due to growing demand for electric ferries and cruise ships.

Europe

Europe led the market with USD 2.73 billion in 2025 and is projected to reach USD 3.21 billion in 2026, supported by strong electric vessel adoption.

Asia Pacific

Asia Pacific accounted for USD 1.36 billion in 2025 and is expected to reach USD 1.60 billion in 2026, driven by shipbuilding activities in major economies.

U.S.

The market is projected to reach USD 0.32 billion by 2026 and USD 0.88 billion by 2032, supported by increasing electrification of marine transport.

Japan

The electric ship market is projected to reach USD 0.40 billion by 2026, driven by regulatory initiatives and advancements in vessel electrification.

Read More

Electric Ship Market Trends

Upsurge in Development of Electric Autonomous Ships is the Ongoing Trend in the Market

Global maritime trade is being transformed by digitalization, artificial intelligence, and developing connectivity, enabling cargo and ships to be remotely monitored in real-time. Digitalization in the marine industry provides operation automation, business process automation, and information processing. In April 2023, Trafikverket Sweden signed a contract with Holland Shipyards Group to provide four autonomous all-electric car ferries – including auto-mooring facilities and charging stations. The first ferry, designed for delivery in the second half of 2024, will run between Ljusteröleden and Vaxholmsleden in the Stockholm archipelago. This development will foster the electric ship market growth during 2026-2034.

DRIVING FACTORS

Increasing Need for Reduced CO2 Emissions and Eco-friendly Ships Propels Demand for Electric Powered Ships

The fundamental driving forces behind electric ship adoption are environmental concerns, energy efficiency, and cost-effectiveness. Ecological problems, driven by the escalating apprehensions of climate change, have increased the demand for eco-friendly modes of transportation. Electric vessels produce no greenhouse gas emissions compared to their traditional fossil fuel-powered counterparts, rendering them an optimal substitute. The adoption of electrified vessels increases due to high fossil fuel prices, tighter population regulation, and others. Improved battery technology is allowing shipping firms to reduce carbon, cost, and pollution. Governments are also executing policies targeting marine insurance and air pollution in port cities, further incentivizing the adoption of electric vessels. The ships offer opportunities to rethink domestic and international transport systems. For instance, in October 2022, Amasus signed a contract with compatriot Handelskade Shipsales and Turkish Boğaziçi Shipyard for a series of four multipurpose (MPP) shortsea cargo ships.

RESTRAINING FACTORS

Current Battery Technology and High Capital Expenditure to Restrain Market Growth

The current battery technology is the primary restraint for adopting fully-electric vessels. Even ships sailing over short distances require a large amount of energy. Current batteries' energy density/capacity cannot accommodate the energy needs of large ships. Similarly, the capital expenditure for ship owners is also extensively high owing to the battery charging infrastructure shortage and high energy storage cost, as the current battery capacity is still low. Hence, these factors are anticipated to restrain the growth of the market. Another challenge is the high initial expenses associated with electric ships, which stem from costly batteries and electric propulsion systems required. Additionally, there are infrastructure complications that need to be resolved. For instance, the current infrastructure for electric vessels, including charging stations, is yet to be widely available, making it difficult to operate them on a large scale.

Download Free sample to learn more about this report.

Segmentation Analysis

By Propulsion Type Analysis

Hybrid Propulsion Technology Dominates the Market Owing to Reduced Risk of Failure

Based on propulsion type, the market is segmented into hybrid and fully electric. The Hybrid segment is expected the highest market share of 73.48% in 2026. Hybrid propulsion can reduce fuel consumption by nearly 20% and lower up to 15% of CO2 emissions from ships. The major factors contributing to the dominance of the hybrid segment include reducing carbon emissions and pushing for zero-emission transport systems. The hybrid propulsion technology combines electric and traditional propulsion systems.

The fully electric segment is anticipated to show significant growth in the market owing to the increased adoption of fully-electric propulsion for small passenger ships and ferries operating on inland waterways. Additionally, its CO2 emissions are only 5%, compared to a conventional ferry. The operating costs are around 80% lower and the ship saves nearly 1 million liters of diesel every year, which is anticipated to foster the market during the forecast period.

By Power Output Analysis

746-7560 kW to Dominate due to Development of Related Power Output and New Expansion Strategy for Higher Capacity Power Output

Based on power output, the market is divided into up to 745 kW, 746-7560 kW, and above 7560 kW. The 746-7560 kW segment will be the highest market share of 66.33% globally in 2026. The segment is projected to grow faster over the forecast period due to the rising adoption of electric/hybrid propulsion in vessels. For instance, In March 2023, Norled and Brødrene signed a contract to construct a new hybrid electric vessel named MS "Bre." The top speed will be around 30 knots, and the vessel's length is 24 meters. It will be equipped with 1.2 MWh of batteries and an all-electric powertrain with diesel-powered range extenders. These factors are anticipated to fuel the segment's growth during the forecast period.

The up to 745 kW segment held the second-largest share of the market in 2023. Vessels with this power have more excellent selection in the shipping industry. However, the increasing emphasis on reducing the carbon footprint has boosted the adoption of propulsion systems that produce minimal emissions and provide advantages such as low engine noise and vibrations. These factors are attributable to the high share of this segment.

To know how our report can help streamline your business, Speak to Analyst

By Mode of Operation Analysis

Semi-autonomous Segment to Dominate Owing to Increasing Retrofitting on Existing Vessels

Based on mode of operation, the market is segmented into semi-autonomous and fully autonomous. The semi-autonomous segment is projected to hold the leading market share of 71.01% in 2026. As fully autonomous vessels are anticipated to be commercialized during the forecast period, the sales have been primarily driven by semi-autonomous ships. The systems can improve the operational efficiency of vessels. Additionally, they can be retrofitted on manually operated existing vessels.

The fully autonomous segment is expected to witness higher CAGR during the forecast period. They allow efficient load transportation using advanced systems and contribute to a reduction in human errors. Also, it decreases operational costs by eliminating labor costs. Faster operation and shortage of mariners are some of the factors expected to fuel the growth of this segment.

By Ship Type Analysis

Commercial Ship Segment Held Largest Share Fueled by Growing Trade Liberalization

Based on ship type, the market is divided into commercial ship and passenger ship. The commercial ship segment is estimated to hold the largest market share of 73.31% in 2026. The growing trade liberalization has improved the maritime trade volume over the last few years. The number of ships, such as oil tankers, bulk carriers, and container ships, added to the existing fleet has also increased considerably.

However, concerns about air pollution, climate change, and fuel efficiency have resulted in the rising adoption of electric vessels, particularly hybrid ships.

REGIONAL ANALYSIS

The global market is analyzed across North America, Europe, Asia Pacific, and the rest of the world.

Europe

Europe Electric Ship Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe contributed 54.90% to the global market in 2025, with a valuation of USD 2.73 billion, and is projected to reach USD 3.21 billion in 2026. Europe holds the largest electric ship market share due to the rising adoption of electric vessels by major countries. For instance, Norway holds the maximum market share while other nations, including Finland, the Netherlands, China, Denmark, and Sweden are also beginning to launch electric ships; this development drives the market growth during the forecast period. The UK market is projected to reach USD 0.54 billion by 2026, and the Germany market is projected to reach USD 0.75 billion by 2026.

For instance, in June 2022, Cochin Shipyard Limited announced that the company delivered two autonomous electric barges for Norway ASKO Maritime AS. The company offers 67m long vessels that are full-electric transport ferries powered.

Asia Pacific

Asia Pacific accounted for USD 1.36 billion in 2025, representing 27.46% of the global market share, and is projected to reach USD 1.6 billion in 2026. Asia Pacific is expected to show substantial growth in the market. According to the International Maritime Organization (IMO), China, Japan, and South Korea account for over 90% of global ship production, including massive merchant vessels such as cargo and tanker vessels. Recent regulatory developments such as the global sulfur cap and voluntary initiatives by OEMs, specifically in Japan and China, to enhance electrification in large vessels are expected to influence the market growth in this region. The electric ships market in the U.S. is projected to grow significantly, reaching an estimated value of USD 0.88 billion by 2032. The Japan market is projected to reach USD 0.4 billion by 2026, the China market is projected to reach USD 0.87 billion by 2026, and the India market is projected to reach USD 0.09 billion by 2026.

North America

The North America market generated USD 0.55 billion in 2025, representing 11.02% of the global market landscape, and is expected to reach USD 0.63 billion in 2026. The market in North America shows sustainable growth due to rising demand for fully-electric cruise ships, yachts, and ferries. The market in the rest of the world is anticipated to exhibit steady growth over the forecast period owing to increasing naval expenditure in countries such as Brazil, the UAE, and Saudi Arabia, with a focus on the procurement of smaller vessels such as all-electric patrol boats and hybrid frigates. The U.S. market is projected to reach USD 0.32 billion by 2026.

Rest of the World

In 2025, the Rest of the World market stood at USD 0.33 billion, representing 6.62% of global demand, and is projected to grow to USD 0.38 billion in 2026.

Key Industry Players

Companies Focus on Development & Acquisitions and Partnerships to Gain Competitive Edge

The major electric ship market players include ABB, Leclanche, Siemens AG, Kongsberg, and MAN Energy Solutions SE. Majority of them are focusing on developing autonomous systems that can increase operational efficiency via features such as advanced navigational systems and comprehensive route planning.

Kongsberg Gruppen supplies technology systems and solutions to customers in the merchant marine, defense, aerospace, offshore oil, gas, renewable, and utility industries. The company operates through three business segments, Kongsberg Maritime, Kongsberg Defense and Aerospace, and Kongsberg Digital. The Kongsberg Maritime segment develops and delivers positioning, monitoring, navigation, and automation systems for merchant vessels and the offshore industry.

List of Key Companies Profiled:

- Kongsberg (Norway)

- Leclanche (Switzerland)

- Corvus Energy (Canada)

- Echandia Marine AB (Sweden)

- Siemens (Germany)

- Vard (part of Fincantieri SpA) (Norway)

- Norwegian Electric Systems (Norway)

- General Dynamics Electric Boat (U.S.)

- MAN Energy Solutions SE (Germany)

- Wartsila (Finland)

- Schottel Group (Germany)

- Anglo Belgian Corporation NV (Belgium)

- Eco Marine Power (Japan)

- Akasol AG (Germany)

KEY INDUSTRY DEVELOPMENTS:

- March 2023 - ABB signed a contract with Fincantieri to deliver eight mid-range Azipod propulsion systems for four medium-sized cruise vessels. The passenger ships will have two 7.7-megawatt Azipod propulsion units per vessel. The company will deliver ships in 2024, 2025, 2026, and 2027. With the electric drive motor accommodated within a pod beyond the ship hull, the Azipod system can turn 360 degrees, allowing vessels to dock in harbors where turning circles are restricted.

- November 2022 - UECC introduced a new Auto Archive vessel at Gothenburg, offering short-sea shipping services. The vessel is almost 170 meters long, and it will have the capacity to transport 3,600 cars. The vessel will also be able to transport other kinds of heavier vehicles and project cargo. The Auto Archive is powered by a hybrid of LNG and battery power. This reduces emissions not only by improving operational efficiency but also by peak shaving.

- November 2022 - ABB announced that it has been selected to provide the shaft generator system with permanent magnet technology for vessels. The Dalian Shipbuilding Industry Company (DSIC) will construct the vessels. The permanent magnet shaft generator system will increase the fuel efficiency of these vessels.

- November 2022 - Echandia signed a contract with Molslinjen to supply energy storage solutions for two new fully-electrified vessels. Echandia has a high degree of battery system of installed capacity utilization, resulting in an overall system size and weight. Also, battery systems will have a total capacity of around 7 MWh.

- October 2022 - Kongsberg Maritime signed a contract with Holland Shipyards Group to deliver control systems and electrification with automated functionalities for up to four new all-electric ferries. The contract also has the option to deliver the systems for two more ferries. The company will also deliver the technology for a remote monitoring and operation center in Stockholm and to secure communication between ferries, ports, and the control center.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading market players, competitive landscape, ship type, and product applications. Besides, the report includes insights into the electric ship market trends and highlights key industry developments. In addition, the report encompasses several factors that contributed to the market's growth in recent years

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 18.5% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Ship Type

|

|

By Mode of Operation

|

|

|

By Power Output

|

|

|

By Propulsion Type

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 4.97 billion in 2025.

The market is expected to grow at a CAGR of 18.5% over the forecast period (2026-2034).

The hybrid segment is expected to lead the market due to the adoption of commercial hybrid ships globally.

The market size in Europe stood at USD 2.73 billion in 2025.

Kongsberg (Norway), Leclanche (Switzerland), and Wartsila (Finland) are some of the top players in the market.

Europe held the largest share of the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us