Electric Vehicle Aftermarket Industry Size, Share & Industry Analysis, By Vehicle Type (Passenger Car and Commercial Vehicle), By Component (Tire, Brake & Suspension System, Body Parts, Electrical Components, and Others), By Propulsion Type (BEV and HV), and Regional Forecast, 2026–2034

KEY MARKET INSIGHTS

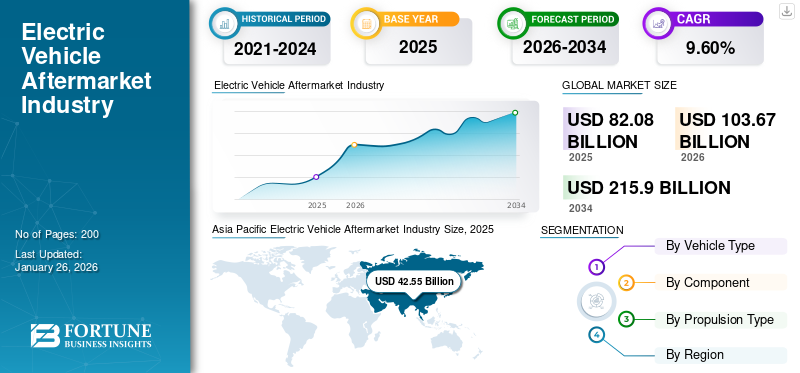

The global electric vehicle aftermarket industry size was valued at USD 82.08 billion in 2025 and is projected to grow from USD 103.67 billion in 2026 to USD 215.90 billion by 2034, exhibiting a CAGR of 9.60% during the forecast period. Asia Pacific dominated the electric vehicle aftermarket industry with a market share of 51.84% in 2025.

The electric vehicle aftermarket refers to a sector that delivers products and services for the maintenance, repair, and customization of electric vehicles after their initial sale. This market is rapidly evolving due to the increasing adoption of Battery Electric Vehicles (BEVs) and Plug-In Hybrid Electric Vehicles (PHEVs). While EVs generally have fewer moving parts than traditional Internal Combustion Engine (ICE) vehicles, they still require regular maintenance. The key service areas include battery maintenance, software updates, charging equipment maintenance, and motor & drivetrain maintenance services.

Electric vehicle tires and suspension are gaining traction in the EV aftermarket. Due to their distinct weight distribution and torque qualities, there is a high demand for tires that provide increased durability, lower rolling resistance, and enhanced energy efficiency. Additionally, custom-designed suspension systems tailored to the specific characteristics of electric vehicles are included in this industry.

The industry is rapidly evolving, and several major players have emerged in the EV market offering a wide range of services, including EV parts, charging infrastructure, software solutions, maintenance, and more. Bosch, Continental AG, and ZF Friedrichshafen AG are the major players in the EV aftermarket industry.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Adoption of Electric Vehicles to Propel Market Growth

The rise in global sales of electric vehicles has led to a larger number of EVs on the road, which increases the demand for electric vehicle aftermarket products and services. As more consumers adopt EVs, there is a corresponding need for parts, repairs, and services specific to EVs, such as battery replacements, charging equipment, and electric motor maintenance. Electric cars accounted for around 18% of all cars sold in 2023, up from 14% in 2022, and only 2%, five years earlier, in 2018. These trends indicate that growth remains robust as electric car markets mature.

Many governments globally offer EV adoption incentives, including subsidies, tax benefits, and charging infrastructure development. The increasing popularity and adoption of electric vehicles result in a more significant need for various aftermarket services, ranging from battery replacements to the maintenance of EV-specific parts. This development fueled the demand for EV aftermarket services.

Download Free sample to learn more about this report.

Market Restraints

Limited Availability of Aftermarket Parts to Hamper Market Growth

The EV aftermarket industry faces numerous barriers despite the high sales of electric vehicles. The restraining factors that can be identified include technological limitations, high costs, regulatory hurdles, limited consumer awareness, and supply chain issues. In the EV industry, manufacturers usually dominate the supply of important parts, including batteries, power electronics, and software upgrades.

Independent companies in the electric vehicle aftermarket frequently face difficulties acquiring specific parts for electric vehicles due to their unique and exclusive characteristics. This OEM control limits access to original parts and impedes competition. Electric vehicles have fewer mechanical parts than internal combustion engines, relying heavily on electrical and electronic components including battery management systems, inverters, and electric motors. These components are more complex and usually require specific expertise to repair or replace, resulting in limited options for aftermarket replacements.

In September 2024, a joint study by Alix Partners and Berylls, in collaboration with CLEPA and FIGIEFA, was unveiled at Automechanika. The study explored two potential scenarios that could greatly influence the cost of vehicle service and maintenance for consumers. The study, which analyzes the competitiveness of the Europe automotive aftermarket up to 2035, considered the impact of new vehicle technologies, cybersecurity requirements, and the shift toward software-defined vehicles. From expert interviews with key stakeholders to Berylls's analysis, the study identifies five key factors that will shape the future of the aftermarket:

- Availability of certain car parts to only vehicle manufacturers

- The need for specific coding or activation for replacement parts

- Challenges in accessing technical information for repairs

- Outdated interfaces for software updates in independent repair shops

- Limited access to in-vehicle data

Market Opportunities

Maintenance and Repair Services to Boost Market Growth in Coming Years

The maintenance and repair services segment of the EV aftermarket industry is emerging as a crucial opportunity driven by the rapid adoption of electric vehicles and their unique requirements. This segment contains various services created specifically for EVs, including battery management, software updates, and specialized repairs.

As the electric vehicle market grows, the demand for specialized maintenance and repair services also increases. In contrast to traditional vehicles, EVs function using intricate systems that necessitate specialized expertise and equipment for efficient maintenance. The growing volume of electric vehicles on the streets increases the need for proficient technicians.

Market Challenges

Market Fragmentation and Limited Standardization to Hamper Market Growth

The electric vehicle market is diverse, with many companies providing a variety of models, each equipped with distinct components and technologies. This fragmentation may make it difficult for the aftermarket to keep compatible parts in stock and provide services for various vehicles. The lack of standardized components from various manufacturers can create challenges in developing universal aftermarket solutions, thereby raising costs and complicating inventory management for providers in the aftermarket industry.

Electric Vehicle Aftermarket Industry Trends

Battery Recycling and Remanufacturing are Current Market Trends

The increasing adoption of EVs has highlighted the importance of recycling, repurposing, and remanufacturing EV batteries. Companies are innovating their processes to retrieve valuable materials from these batteries, such as lithium, cobalt, and nickel. Electric vehicles rely on large, high-capacity lithium-ion batteries, which are known for their high costs and the finite nature of their critical materials. Thus, effective management of these batteries at the end of their lifecycle is becoming increasingly essential. This necessity arises from concerns over resource scarcity, cost management, environmental impact, and sustainability objectives.

The process includes retrieving valuable materials from EV batteries for reuse in new batteries or other purposes. With more electric vehicles is projected to reach their end of life, industry leaders are emphasizing recycling and remanufacturing more strongly. This trend addresses the environmental concerns associated with battery disposal and mitigates the need for new raw material extraction. This creates a more sustainable approach to battery lifecycle management. For instance, in October 2023, Stellantis N.V. signed an MOU with Orano to establish a joint venture for recycling end-of-life electric vehicle batteries and scrap from gigafactories in Europe and North America. This move will strengthen Stellantis' position in the electric-vehicle battery value chain by securing additional access to cobalt, nickel, and lithium necessary for electrification and energy transition. This development will drive the electric vehicle aftermarket industry growth during the forecast period.

IMPACT of COVID-19

The COVID-19 pandemic had a multifaceted impact on the EV aftermarket industry, influencing supply and demand dynamics. The pandemic caused significant disruptions in global supply chains, affecting the availability of critical components for electric vehicles. Lockdowns and restrictions led to temporary closures of manufacturing facilities and delays in producing essential parts, such as batteries and electronic components. This situation made it challenging for aftermarket businesses to source replacement parts, leading to increased costs and longer wait times for consumers.

Despite the early challenges, the pandemic quickened the transition to electric cars. A growing understanding of sustainability and clean transportation choices has sparked renewed consumer interest in EVs. The demand for services related to electric vehicles is expected to increase significantly as more consumers consider buying EVs. The pandemic prompted investments in manufacturing facilities dedicated to EV components. For instance, companies such as Daesol Ausys are expanding their production capabilities to meet the increasing demand for EV parts. Such investments enhance the availability of quality aftermarket products, instilling confidence among consumers in authorized service centers.

Segmentation Analysis

By Vehicle Type

Increasing Adoption of Electric Passenger Cars Fueled Segment Growth

Based on vehicle type, the market is divided into passenger and commercial vehicles.

The passenger car segment is projected to dominate the electric vehicle aftermarket industry, accounting for 91.90% of the global market share in 2026. The growth of the EV aftermarket is closely linked to the rising adoption of electric passenger cars. As more consumers opt for electric vehicles, the demand for aftermarket services, including maintenance, battery replacements, and customization, grows significantly. This shift is particularly due to increasing sales of electric vehicles in key countries including China, India, Norway, and Germany.

While the commercial vehicle segment currently holds a smaller share compared to passenger cars, it is projected to be the fastest-growing segment in the coming years. This rapid growth is fueled by significant savings on fuel and maintenance expenses offered by electric commercial vehicles compared to traditional Internal Combustion Engine (ICE) vehicles, making them an attractive option for fleet operators and driving increased demand in the aftermarket. Many governments are actively promoting the adoption of electric commercial vehicles to reduce greenhouse gas emissions and improve air quality through incentives, subsidies, and grants. Improvements in road infrastructure and the expansion of e-commerce and mining operations are also supporting the sales of commercial EVs. Leading commercial vehicle manufacturers are investing in the development and integration of autonomous features in electric commercial vehicles, further enhancing safety and efficiency and potentially creating new aftermarket opportunities.

Download Free sample to learn more about this report.

By Component

Frequent Use and Wear & Tear of Tire Leading to Replacement, Propels Segment Growth

Based on component, the market is divided into tire, brake & suspension system, body parts, electrical components, and others.

The tire component segment is projected to reach the market, contributing 28.42% globally in 2026. Tires have a limited lifespan, typically ranging from 3 to 5 years for passenger vehicles. As more consumers transition to electric vehicles, the demand for replacement tires in the aftermarket is expected to rise sharply. This creates a consistent revenue stream for tire manufacturers and retailers, further solidifying the tire segment's dominance in the aftermarket. The segment's growth is also attributed to the increasing production volume of tires.

Brake systems in EVs are incorporating high-tech features such as Anti-Lock Braking Systems (ABS), Electronic Stability Control (ESC), and regenerative braking systems, leading to increased demand for advanced brake components in the aftermarket. The overall automotive brake system and parts market is experiencing faster growth, propelled by the rise of electric cars and safety regulations. The EV suspension system market is also growing, with advancements in lightweight suspension technology driving the fastest-growing sub-segment. The demand for EV body parts in the aftermarket is driven by factors such as repairs after accidents and the increasing trend of customizing and personalizing EVs. Aftermarket businesses are providing a variety of products, including body kits, custom lighting, and interior upgrades, allowing EV owners to personalize their vehicles.

Electrical components segment encompasses a wide array of parts specific to electric vehicles, including electric motors, power electronics, transmission components, and others. The electrical components segment also includes infotainment systems, sensors, and wiring harnesses. The increasing complexity of EV systems and the integration of advanced features drive demand for these components in the aftermarket.

Others is a broad segment includes essential EV-specific components and systems such as battery systems (battery cells, cooling systems, and battery packs), charging systems (mobile, public, and wall chargers), thermal management systems (coolant pumps, HVAC units, radiators), and more. Battery-related components are particularly crucial due to their cost, replacement frequency, and technological advancements. The expansion of charging infrastructure and the increasing demand for specialized maintenance and repair services tailored to EVs are key drivers for this segment.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion Type

Operational Efficiency and Consumer Preferences Accelerated BEV Segment Growth

Based on propulsion type, the market is divided into BEV and HV.

The BEV segment holds the maximum market share as BEV registrations increased significantly in 2024. The segment's growing market share showcases strong consumer preference and adoption, directly affecting the aftermarket services related to BEVs. This development is expected to drive the market growth during the forecast period.

The HEV segment is expected to show the highest growth rate during the forecast period, according to some analysts. This is due to the convenience they offer, particularly in regions with limited charging infrastructure, as they can operate on both electricity and fuel

Electric Vehicle Aftermarket Industry Regional Outlook

Based on region, the market is analyzed across Europe, Asia Pacific, North America, and the rest of the world.

Asia Pacific

Asia Pacific Electric Vehicle Aftermarket Industry Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, the Asia Pacific market stood at USD 42.55 billion, representing 51.84% of global demand, and is projected to grow to USD 54.04 billion in 2026 and is anticipated to continue its dominance throughout the forecast period with the fastest-growing CAGR. The increasing adoption of electric vehicles across the region, driven by supportive government incentives policies and a growing consumer base, will significantly contribute to the aftermarket expansion. For instance, in September 2024, the Indian government presented the PM E-DRIVE scheme with an outlay of approximately USD 1.48 million which will be in force from October 2024 to March 2026. This initiative strives to accelerate electric vehicle adoption by delivering subsidies and grants for EVs and charging solutions. The Japan market is projected to reach USD 0.77 billion by 2026, the China market is projected to reach USD 51.18 billion by 2026, and the India market is projected to reach USD 0.61 billion by 2026. The budget for clean energy subsidies in 2024 was USD 0.85 billion, with a maximum subsidy of approx. USD 5,532.05 for an EV and USD 3579.56 for a PHEV, respectively. The subsidy amount is based on the expected vehicle model's energy creation. This development will drive the regional market growth during the forecast period.

Europe

Europe contributed approximately USD 25.36 billion to the global market in 2025, accounting for 30.90% share, and is expected to reach USD 31.98 billion in 2026. Europe holds the second-largest EV aftermarket industry share. The growth is attributed to technological advancements. Integrating advanced technologies in EVs, including connectivity features and enhanced battery systems, will create demand for specialized aftermarket services. This encompasses maintenance, software updates, and battery management solutions crucial for enhancing EV performance. This advancement will drive the electric vehicle aftermarket industry trend throughout the forecast period. The UK market is projected to reach USD 5.02 billion by 2026 and the Germany market is projected to reach USD 9.76 billion by 2026.

North America

The market in North America reached USD 12.94 billion in 2025, representing 15.77% of total market revenue, and is projected to reach USD 16.16 billion in 2026. North America holds a significant market share due to increasing infrastructure investment by key countries, such as the U.S., Canada, and Mexico. Significant investments in charging infrastructure and service facilities are also contributing to the growth of the North American EV aftermarket. These investments will ensure that consumers can access essential services and support, enabling confidence in EV owners. The U.S. EV aftermarket is dynamic and continuously evolving, driven by the increasing shift towards electric vehicles, technological advancements, and the growing needs and preferences of EV owners. The U.S. market is projected to reach USD 14.17 billion by 2026.

Rest of the World

Rest of the World recorded a market size of USD 1.22 billion in 2025, capturing 1.49% of the global market share, and is projected to reach USD 1.48 billion in 2026. The rest of the world holds a significant market share. The market growth is attributed to companies reducing their carbon footprint, leading to a higher adoption of electric fleets. This adoption will drive the industry growth.

Competitive Landscape

Key Industry Players

Companies Focus on Expansion of Product Portfolio to Enhance Their Market Positions

ABB, AISIN Seiki Co., Ltd., and DENSO Corporation are major players operating in the market. AISIN specializes in automotive parts, including those tailored for electric vehicles. Its extensive product range supports various EV components, contributing to its significant market presence. DENSO is a leading global supplier of advanced automotive technologies, systems, and components. The company provides EV aftermarket services, including essential parts, enhancing vehicle performance and efficiency.

List of Key Electric Vehicle Aftermarket Companies Profiled

- 3M (U.S.)

- ABB Ltd. (Switzerland)

- EVBox Group (Netherlands)

- ChargePoint Inc. (U.S.)

- Webasto SE (Germany)

- Siemens AG (Germany)

- Bosch Automotive Service Solution Inc. (Germany)

- Delphi Technologies (U.K.)

- Schneider Electric SE (France)

- AISIN Seiki Co., Ltd. (Japan)

- Continental AG (Germany)

- Denso Corporation (Japan)

- Robert Bosch GmbH (Germany)

Key Industry Development

- In April 2025, Bilstein Group established Ferdinand Bilstein India Private Limited, marking its 23rd international subsidiary. The official opening was scheduled for April 1, 2025, as the company expands its presence in the Indian automotive aftermarket. The Bilstein Group is a German company specializing in the automotive aftermarket. It provides repair solutions for passenger and commercial vehicles through its brands, including febi, SWAG, and Blue Print. The company offers many replacement parts designed for professional vehicle repairs.

- In December 2024, the Automotive Component Manufacturers Association of India (ACMA) hosted the first edition of the Automotive Aftermarket Expo at the Samrat Ashok International Convention Centre in Patna. This two-day event will bring together India's aftermarket industry participants, including manufacturers, distributors, and suppliers. The Automotive Aftermarket Expo aimed to provide a platform for collaboration, business development, and knowledge sharing among professionals in the industry. It also seeks to educate mechanics, dealers, retailers, and wholesalers on the importance of using authentic and high-quality spare parts and replacement components.

- In November 2024, Niterra implemented a strategic approach by adopting a balanced approach, leveraging its global expertise while focusing on local market needs. The company has established a dedicated department to explore new eco-friendly technologies and their potential applications in India, demonstrating its commitment to staying ahead of market trends. Niterra's strategy in the Indian market is deeply rooted in technological innovation and sustainability. The company has introduced several advanced products tailored to the Indian market's specific needs: 1) Oxygen sensors for OBD2 systems; 2) Oval-type Spark Plugs for two-wheeler engines; 3) Double precious IR+Pt fine tip Spark Plugs

- In June 2024, ZC Rubber introduced its most recent Electric Vehicle (EV) tire in Germany. The tire is designed to deliver superior performance with BPOT technology, which improves handling with a 5% larger contact area at high speeds compared to other tires.

- In January 2024, HIM Teknoforge introduced hydraulic axle components for overseas customers, primarily used in the material handling industry and electric vehicles. Additionally, they have expanded their product range to offer brake shaft kits, steering kits, and machine castings.

- In July 2023, Vitesco Technologies, a prominent global developer & producer of advanced drive systems for sustainable transportation, initiated the direct sale of Original Equipment (OE)-manufactured spare parts in the Independent Aftermarket (IAM). The company aims to provide a comprehensive range of spare parts and services for electric vehicles, from passenger to commercial vehicles, all from a unified source.

Report Coverage

The electric vehicle aftermarket industry statistics provides a detailed analysis and focuses on key aspects, such as leading market players, competitive landscape, and vehicle types. Besides, it includes insights into the market trends and highlights key industry developments. In addition to the above mentioned factors, the report encompasses several factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.60% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type

|

|

By Component

|

|

|

By Propulsion Type

|

|

|

By Region

|

Frequently Asked Questions

The Fortune Business Insights study shows that the market size was valued at USD 82.08 billion in 2025.

The market is likely to record a CAGR of 9.60% over the forecast period.

By vehicle type, the passenger car segment led the market in 2025.

The market size in Asia Pacific was valued at USD 42.55 billion in 2025.

ABB, AISIN Seiki Co., Ltd., and Denso Corporation are some of the top players in the market.

Asia Pacific held the largest share of the market in 2024.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us