Electric Vehicle Charging Station Market Size, Share & Industry Analysis, By Charger Type (Fast and Slow/Moderate), By Application (Commercial and Residential), By Connector (J1772, Mennekes, GB/T, CCS1, CHAdeMO, CCS2, and Tesla), By Level (Level 1, Level 2, and Level 3), By Vehicle Type (Passenger Cars and Commercial Vehicles), By Propulsion (BEV and PHEV), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

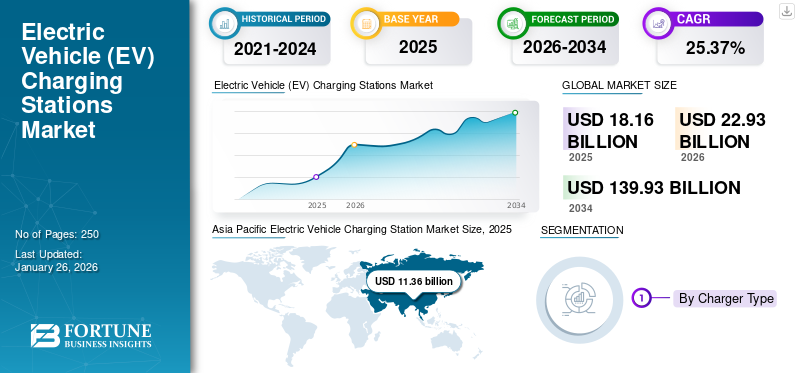

Electric Vehicle Charging Station Market Size and Future Outlook

The global electric vehicle charging station market size was valued at USD 18.16 billion in 2025. The market is projected to grow from USD 22.93 billion in 2026 to USD 139.93 billion by 2034, exhibiting a CAGR of 25.37% during the forecast period. Asia Pacific dominated the electric vehicle charging stations market with a market share of 62.56% in 2025.

Electric vehicle charging stations provide the infrastructure required to recharge electric vehicles, offering AC and DC charging options across residential, commercial, and public locations. Widely deployed for passenger and commercial EVs, these stations enable clean mobility and reduce carbon emissions. The market is driven by the rapid adoption of electric vehicles, government incentives, and expanding charging networks. Technological advancements such as ultra-fast chargers, smart connectivity, and renewable energy integration further accelerate growth. Increasing investments from automakers, utilities, and infrastructure providers, along with innovations such as vehicle-to-grid (V2G) technology, position electric vehicle charging stations as a key enabler of sustainable transportation and next-generation energy ecosystems.

Key players in the electric vehicle charging station market include ABB, ChargePoint, Schneider Electric SE, and Siemens AG. These companies focus on expanding high-performance charging infrastructure, advancing ultra-fast DC charging technologies, and integrating smart energy management systems. Strategic collaborations with automakers, utilities, and governments, along with investments in digital platforms, interoperability, and renewable-powered charging, strengthen their global market presence. Their emphasis on innovation, scalability, and sustainability positions them as leaders in supporting the accelerating transition toward electric mobility and net-zero transportation ecosystems.

Download Free sample to learn more about this report.

Electric Vehicle Charging Stations Market Key Takeaways

- 2025 Market Size: USD 18.16 Billion

- 2026 Market Size: USD 22.93 Billion

- 2034 Forecast Market Size: USD 139.93 Billion

- CAGR: 25.37% from 2026–2034

- Asia Pacific dominated the electric vehicle charging station market with a 62.56% share in 2025.

- The fast charging segment is projected to hold a 77.20% share in 2026.

- The Commercial segment is projected to hold a 82.39% share in 2026.

Asia Pacific

Asia Pacific generated USD 11.36 billion in 2025 and is projected to reach USD 14.87 billion in 2026.

North America

North America generated USD 7.96 billion in 2025 and is projected to reach USD 8.42 billion in 2026.

Europe

Europe accounted for USD 5.81 billion in 2025 and is expected to reach USD 6.04 billion in 2026.

U.S.

The electric vehicle charging station market is projected to reach USD 3.12 billion in 2026.

Japan

The electric vehicle charging station market is projected to reach USD 0.33 billion in 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rising Electric Vehicle Sales to Drive Market Growth

The rapid increase in the number of electric vehicle sales and deeper penetration of electric vehicles into new car markets is a powerful growth for electric vehicle charging infrastructure. As more EVs hit the road, the demand for both public and private charging points increases. This dynamic creates a network effect: more EVs, more charging demand, more incentive to deploy infrastructure, and lowers charging range risk, which further fuels EV adoption.

In August 2025, global EV sales reached 10.7 million year-to-date, representing a 27% increase over the prior period. In July 2025, China’s EV market continued to dominate, with EV sales growing by nearly 40% year-on-year in 2024, and EVs accounting for almost half of all new vehicle sales in the country. In January 2025, China extended its trade-in subsidy program, offering USD 2,750 for buyers who replaced older vehicles with EVs, a measure that stimulated additional EV purchases and thus charging infrastructure demand.

Increasing Number of Government Policies in Favor of Automotive Electrification to Drive Market Growth

The rising number of government policies supporting automotive electrification is a key growth driver for the global market of electric vehicle charging stations. As governments globally accelerate their zero-emission targets, policy support in the form of subsidies, tax incentives, infrastructure grants, and regulatory mandates is directly boosting EV adoption and, consequently, the need for charging infrastructure. In January 2025, China extended its vehicle trade-in subsidy scheme, providing consumers with up to USD 2,730 when scrapping older internal combustion vehicles in exchange for new EVs. This initiative is expected to add nearly 1 million additional EV sales in 2025, substantially increasing the need for urban and intercity fast-charging networks.

MARKET RESTRAINTS

High Initial Costs for Setting Up an Electric Vehicle Charging Stations May Hamper Market Growth

The high initial costs of establishing EV charging stations remain a major factor restraining global market growth. Setting up a charging network requires heavy capital investment (CAPEX) for equipment, construction, grid upgrades, and permits, often with uncertain short-term returns. The challenge is particularly acute in emerging markets where EV adoption is still in early stages, resulting in underutilization of installed chargers and delayed profitability.

Typical setup costs vary widely depending on charger type and region. The total project cost is attributable to various factors such as the number of required hardware, site preparation, installation, grid connection, and maintenance etc. In addition, network operators face recurring operational expenses (OPEX) such as software management, power tariffs, and service maintenance. In July 2025, the Karnataka government (India) cancelled its plan to install 2,500 public electric vehicle charging stations after no private company submitted bids, citing high setup costs, limited utilization potential, and poor return on investment. This highlights investor hesitation caused by steep initial expenses and uncertain demand.

MARKET OPPORTUNITIES

Growth of Vehicle-to-Grid (V2G) and Bi-directional Charging Technology Represents a Transformative Opportunity

The growth of Vehicle-to-Grid (V2G) and bi-directional charging technology represents a transformative opportunity in the global market. These technologies allow EVs not only to draw energy from the grid but also to supply it back, turning vehicles into mobile energy assets. This dual functionality supports grid balancing, renewable integration, and energy cost optimization, creating new business models for utilities, automakers, and charge point operators. In January 2023, a simulation study found that bi-directional V2G could deliver up to 18% additional cost savings compared to conventional smart charging, underscoring its economic potential.

Electric Vehicle Charging Station Market Trends

Rapid Expansion of Fast & Ultra-Fast Charging Networks Accelerates Market Trend

The shift toward fast and ultra-fast charging networks is one of the most visible and powerful trends in the EV charging infrastructure space. These stations deliver significantly higher power, such as 150 kW, 250 kW, 350 kW, and beyond, enabling much shorter charge times. That reduces dwell time barriers where users are reluctant to spend extended time charging, thereby making EVs more competitive with conventional refueling.

With faster electric vehicle charging stations becoming more widespread, EV drivers gain confidence in long-distance travel and spontaneous journeys, especially when highway corridors are sufficiently served. Moreover, hubs that provide multiple high-power chargers can support higher throughput, better utilization, and economies of scale for operators. In April 2025, China’s plan to deploy 1,000 ultra-fast charging stations in Beijing and an additional 4,000 ultra-fast chargers in Chongqing by year’s end signaled that ultra-fast infrastructure is being treated as a national priority in major EV markets.

Download Free sample to learn more about this report.

Emergence of Smart & Connected Charging Infrastructure Boosts Market Development

Beyond raw charging power, the charging ecosystem is rapidly evolving toward smart, connected charging infrastructure where chargers, networks, and grid systems coordinate intelligently. Smart charging enables dynamic load management, real-time communication, demand response, pricing optimization, predictive maintenance, and better integration with the grid and renewables.

Through such connectivity, charging operators can shift loads to off-peak hours, modulate charging power based on grid constraints, and avoid costly grid upgrades. For users, this translates into lower energy costs, improved reliability, and a smoother experience. For grid operators, widespread smart charging enhances flexibility and supports variable renewable integration. In August 2025, ev.energy noted that smarter EV charging could reduce utility bills by up to 10% for U.S. households by 2035, attributing much of that to load shifting and optimization enabled by connected systems.

MARKET CHALLENGES

Lack of Standardization and Interoperability Hinders Market Growth

Lack of standardization and interoperability hinders the electric vehicle charging station market by creating compatibility issues among charging connectors, communication interfaces, and payment systems. This fragmentation limits users’ ability to access different networks seamlessly, reducing convenience and discouraging EV adoption. In July 2025, a Driivz analysis revealed that nearly 45% of charging failures occurred due to mismatched software protocols between vehicles and chargers.

Segmentation Analysis

By Charger Type

Rising Consumer Demand for Reduced Charging Time Boosts Fast Chargers Demand

On the basis of the segmentation of vehicle type, the market is classified into fast and slow/moderate.

Fast chargers represent the dominant and fastest-growing segment in the global EV charging station market, driven by rising consumer demand for reduced charging time and increased long-distance travel convenience. In March 2025, EVgo and Toyota launched co-branded charging sites equipped with 350 kW ultra-fast chargers capable of serving multiple vehicles simultaneously, demonstrating network expansion and interoperability initiatives. In Q2 2025, the U.S. added over 4,200 new DC fast charging ports, marking the highest quarterly deployment to date and reflecting accelerating investment in high-power infrastructure. Governments and private operators continue prioritizing fast-charging corridor installations along highways and urban hubs to enhance accessibility, reduce range anxiety, and improve station utilization rates, making this segment the most lucrative in both capacity expansion and technological innovation. The fast segment is projected to dominate the market with a share of 77.20% in 2026.

By Application

Large-scale Deployment of Public and Fleet Charging Networks Fuels Commercial Segment

In terms of application, the market is categorized into commercial and residential.

The commercial segment dominates the global electric vehicle charging station market and is expected to grow with the highest CAGR, due to large-scale deployment of public and fleet charging networks. In June 2025, EVgo and Toyota launched a network of co-branded ultra-fast charging stations across the U.S., equipped with 350 kW chargers to serve public users and fleet vehicles efficiently. Similarly, in April 2025, China’s State Grid Corporation announced a nationwide expansion of public charging infrastructure to support buses, taxis, and logistics fleets. The rise of fleet electrification, ride-hailing services, and commercial logistics electrification is driving significant investments in high-capacity public charging hubs globally. The commercial segment is projected to dominate the market with a share of 82.39% in 2026.

By Connector

Strong Government Standardization and Extensive Deployment Drive GB/T Demand

Based on connector, the market is divided into J1772, mennekes, GB/T, CCS1, CHAdeMO, CCS2, and tesla.

The GB/T connector type dominates the global market of electric vehicle charging stations, primarily due to strong government standardization and extensive deployment across China, the world’s largest EV market. In April 2025, China’s National Development and Reform Commission announced expansion plans for 30 pilot V2G projects using GB/T-compatible chargers in cities such as Beijing and Shanghai. The government’s consistent support through subsidies and mandatory GB/T adoption ensures widespread compatibility across domestic EV manufacturers such as BYD, SAIC, and NIO, reinforcing the connector’s dominant market position globally. The CHAdeMO connector segment is the fastest-growing, driven by its advanced bi-directional power flow and vehicle-to-grid (V2G) capability. The GB/T segment is expected to lead the market, contributing 50.25% globally in 2026.

To know how our report can help streamline your business, Speak to Analyst

By Level

Rising Demand for Ultra-Fast DC Charging Infrastructure Caters to Level 3 Segment's Prominence

Based on level, the market is segmented into level 1, level 2, and level 3.

The Level 3 segment dominates the market and is also the fastest-growing, driven by rising demand for ultra-fast DC charging infrastructure. In March 2025, EVgo and Toyota inaugurated high-power 350 kW DC fast-charging sites across the U.S., designed to serve multiple vehicles simultaneously. Similarly, in April 2025, China’s State Grid Corporation initiated plans to install 1,000 ultra-fast Level 3 charging stations in Beijing, enhancing intercity connectivity. The expansion of long-range EVs, commercial fleets, and public highway networks continues to propel the large-scale deployment of high-power DC charging stations globally. The level 3 segment will account for 77.2% market share in 2026.

By Vehicle Type

Rapid Consumer Adoption of Electric Cars Drives Passenger Cars Segment

On the basis of vehicle types, the market is segmented into passenger cars and commercial vehicles.

The passenger car segment dominates the global electric vehicle charging station market, supported by rapid consumer adoption of electric cars and expanding urban charging infrastructure. In August 2025, global EV sales reached 10.7 million units year-to-date, a 27 percent increase over the previous year, driven mainly by passenger car demand. In April 2025, China’s Ministry of Industry and Information Technology announced plans to build over 4,000 ultra-fast public charging stations in Chongqing and Beijing to support private EV users. The widespread availability of residential, commercial, and highway charging facilities reinforces passenger cars as the leading driver of market demand. The commercial vehicle segment is the fastest-growing in the global market of electric vehicle charging stations, driven by the electrification of logistics, public transport, and ride-hailing fleets.

By Propulsion

Strong Sales Momentum and Expanding Public and Private Charging Networks Propel BEV Segment

Providing to the demand by propulsion of the vehicle, the market is segmented into BEV and PHEV, PHEVs are also referred as plug in electric vehicles.

The BEV segment dominates and is the fastest-growing over the electric vehicle charging station market forecast period. The growth of the segment is driven by strong sales momentum and expanding public and private charging networks. In August 2025, global BEV registrations exceeded 8.5 million units, accounting for nearly 80 percent of total EV sales, led by markets such as China, Europe, and the U.S. In April 2025, China’s Ministry of Industry and Information Technology announced plans for 4,000 ultra-fast BEV-compatible stations across key urban centers to strengthen nationwide coverage. This surge in BEV adoption continues to accelerate demand for high-power DC charging infrastructure and integrated smart-grid solutions globally.

Electric Vehicle Charging Station Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

ASIA PACIFIC

Asia Pacific Electric Vehicle Charging Station Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific generated USD 11.36 billion, contributing 62.56% to global market revenue, and is projected to grow to USD 14.87 billion in 2026. The Asia Pacific region dominates and remains the fastest-growing market for electric vehicle charging stations, fueled by aggressive government policies and large-scale infrastructure development. In April 2025, China’s National Development and Reform Commission initiated 30 pilot vehicle-to-grid (V2G) projects across major cities such as Beijing, Shanghai, and Guangzhou, reinforcing its leadership in EV infrastructure deployment. Likewise, India’s PM E-DRIVE scheme, launched in September 2025, allocated USD 1.1 billion to install 72,000 public charging stations nationwide. With robust investments, rapid EV adoption, and a strong domestic manufacturing base, the region continues to lead global electric vehicle charging station market growth, accounting for the highest charger installations and technological advancements. The Japan electric vehicle charging stations market is anticipated to reach USD 0.33 billion by 2026, the China electric vehicle charging stations market is set to attain USD 13.91 billion by 2026, and the India electric vehicle charging stations market is likely to reach USD 0.01 billion by 2026.

EUROPE

In 2025, Europe generated USD 5.81 billion, contributing 32.20% to global market revenue, and is projected to grow to USD 6.04 billion in 2026. Europe holds the second-largest electric vehicle charging station market share, driven by strict emission targets and large-scale public infrastructure funding. In July 2025, the European Commission allocated USD 85 million under the Alternative Fuels Infrastructure Regulation (AFIR) to accelerate residential, depot, and public charger installations. Major countries such as Germany, France, and the Netherlands are investing in ultra-fast corridor networks and mandating EV-ready building codes, creating a strong policy framework that sustains steady market growth across the continent. The United Kingdom electric vehicle charging stations market is estimated to reach USD 1.13 billion by 2026, while the Germany electric vehicle charging stations market is forecast to reach USD 1.10 billion by 2026.

NORTH AMERICA

North America maintained a strong presence in the global market, reaching USD 7.96 billion in 2025, accounting for 44.20% share, and is expected to reach USD 8.42 billion in 2026. The North American market is growing rapidly due to strong federal funding and network expansion. In August 2025, the U.S. Federal Highway Administration added over 4,200 new DC fast charging ports under the NEVI program, strengthening interstate coverage. Collaborations among ChargePoint, EVgo, and Tesla, alongside the widespread adoption of the North American Charging Standard (NACS), are improving interoperability and driving large-scale infrastructure modernization across the region.

The U.S. dominates the North American market, driven by extensive federal infrastructure investment and rapid network expansion. The implementation of the National Electric Vehicle Infrastructure (NEVI) program continues to accelerate nationwide deployment. The United States electric vehicle charging stations market is expected to reach USD 3.12 billion by 2026.

REST OF THE WORLD

The Rest of the World market is witnessing steady growth supported by rising EV adoption and renewable-linked charging projects. In July 2025, the United Arab Emirates launched Phase 3 of its EV Green Charger Initiative, targeting new public stations by 2026. Similarly, in March 2025, Brazil’s National Electric Mobility Plan promoted private investments in AC and DC chargers, accelerating infrastructure expansion across emerging economies.

COMPETITIVE LANDSCAPE

Key Industry Players:

Investment in High-Power DC Technology, AI-Driven Load Management Defines Competitive Landscape

The global electric vehicle charging station market includes major players such as ABB Ltd., Siemens AG, Schneider Electric SE, ChargePoint Inc., and EVBox Group. These companies collectively capture a significant portion of the market through technology leadership, manufacturing scale, and global presence. ABB Ltd. has a large international footprint, advanced Terra and Megawatt charging platforms, and strong integration with grid and renewable systems. Siemens AG follows, leveraging its industrial automation expertise and digitalized charging solutions through its SICHARGE and VersiCharge product lines. Schneider Electric SE holds third place, focusing on smart energy management and EVlink solutions embedded into sustainable infrastructure projects globally. These top players are investing heavily in high-power DC technology, AI-driven load management, and open-network interoperability. They are also expanding through strategic partnerships with automakers, utilities, and governments to secure long-term contracts. Mid-tier players such as ChargePoint, EVBox, Blink Charging, and Kempower emphasize software innovation, predictive maintenance, and modular hardware design to differentiate from large conglomerates.

LIST OF KEY ELECTRIC VEHICLE CHARGING STATION COMPANIES PROFILED:

- Siemens AG (Germany)

- Eaton (Ireland)

- ChargePoint Inc. (U.S.)

- ABB (Switzerland)

- Schneider Electric SE (France)

- EVBox (Netherlands)

- Kempower Oyj (Finland)

- Tesla Inc. (U.S.)

- Blink Charging Co. (U.S.)

- EO Charging (U.K.)

KEY INDUSTRY DEVELOPMENTS:

- In October 2025, Siemens unveiled SICHARGE FLEX, a megawatt-era DC charging system delivering 480 kW-1.68 MW with dynamic power distribution and modular dispensers, designed for highway and depot use, enabling ultra-fast, multi-vehicle charging and supporting large fleet electrification projects; pilot order announced with OMV.

- In May 2025, Eaton and ChargePoint formalized an industry-first partnership to streamline EV charging project design, procurement, and deployment, bundling Eaton power gear, site services, and ChargePoint chargers as turnkey offerings to reduce cost and time-to-deploy.

- In December 2024, ChargePoint and General Motors announced plans to install up to 500 ultra-fast charging ports across the U.S., using the Omni Port solution to support both CCS and NACS connectors, and deploying ChargePoint’s Express Plus platform (up to 500 kW).

- In December 2024, ChargePoint and Colorado Energy Office completed six EV fast-charging corridors in Colorado, delivering 33 DC fast charging sites with over 80 ports, doubling corridor coverage in the state.

- In September 2023, Siemens eMobility began full production of its VersiCharge Blue Level-2 AC charger at its Carrollton, Texas, factory. The charger is designed for broad applications such as offices, parking garages, and fleets, is Buy American compliant, and features integrated smart features (mobile setup, cloud connectivity) to accelerate U.S. charger deployment.

- In January 2023, ABB introduced Terra Home, a residential AC charger unveiled at CES 2023. It supports features such as renewable energy prioritization, remote firmware updates, and smart grid integration for homes and light fleet use.

REPORT COVERAGE

The global electric vehicle charging station market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 25.37% from 2026-2034 |

| Unit | Value (USD Billion) and Volume (Thousand Units) |

| Segmentation | By Charger Type, By Application, By Connector, By Level, By Vehicle Type, By Propulsion, and By Region |

| By Charger Type |

|

| By Application |

|

| By Connector |

|

| By Component |

|

| By Vehicle Type |

|

| By Propulsion |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market was valued at USD 18.16 billion in 2025 and the global market is projected to reach USD 139.93 billion by 2034.

The market is expected to register a CAGR of 25.37% during the forecast period (2026-2034).

The rising sales of electric vehicles and growing EV penetration are expected to drive global market growth.

Asia Pacific is poised to lead during the forecast period.

Level 2 chargers offer faster charging speeds than level 1 chargers and are primarily designed for home, workplace, and public charging stations.

- 2021-2034

- 2025

- 2021-2024

- 250

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us