Electric Vehicle Power Inverter Market Size, Share & Industry Analysis, By Vehicle Type (Passenger Car and Commercial Vehicle), By Propulsion Type (BEV and PHEV), By Technology (IGBT and SiC), By Power Output (Upto 130kW and Above 131kW) and Regional Forecast, 2026-2034

Electric Vehicle Power Inverter Market Size and Future Outlook

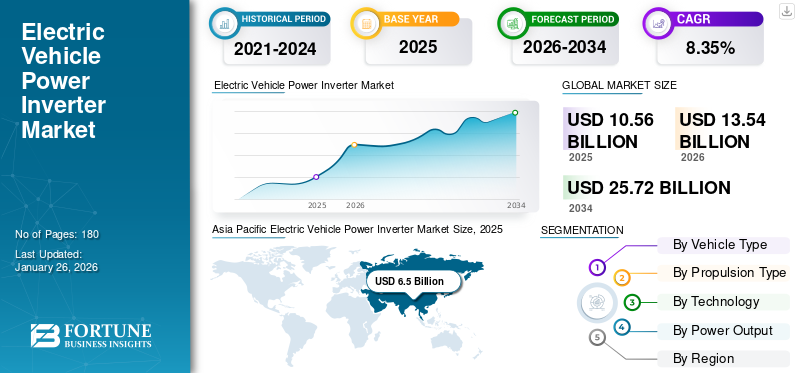

The global electric vehicle power inverter market size was valued at USD 10.56 billion in 2025. The market is projected to grow from USD 13.54 billion in 2026 to USD 25.72 billion by 2034, exhibiting a CAGR of 8.35% during the forecast period. Asia Pacific dominated the global market with a share of 8.35% in 2025.

An electric vehicle power inverter is an electronic device that converts direct current (DC) to alternating current (AC), which is used to drive the electric motor that propels the vehicle.

As a crucial part of electric vehicle powertrains, it significantly impacts the vehicle's overall performance and range. A premium power inverter can improve the efficiency of the EV, lowering energy usage and extending the vehicle's range. The rising demand for high-power inverters propels market growth.

Download Free sample to learn more about this report.

Electric Vehicle Power Inverter Market KEY TAKEAWAYS

- 2025 Market Size: USD 10.56 billion

- 2026 Market Size: USD 13.54 billion

- 2034 Forecast Market Size: USD 25.72 billion

- CAGR: 8.35% from 2026–2034

- Asia Pacific dominated the electric vehicle power inverter market with a 61.58% share in 2025.

- Passenger vehicle segment accounted for the largest market share of 94.26% in 2026.

- BEV (Battery Electric Vehicle) segment held the leading share of 66.66% in 2026.

Asia Pacific

Asia Pacific remained the leading regional market, valued at USD 6.5 billion in 2025 and projected to reach USD 8.39 billion in 2026.

Europe

Europe accounted for 23.48% of the global market in 2025, supported by increasing EV adoption and favorable regulations.

North America

North America accounted for USD 1.16 billion (10.98%) of the global market in 2025 and is expected to reach USD 1.47 billion in 2026.

U.S.

The market is projected to reach USD 1.28 billion by 2026.

Japan

The market is expected to reach USD 0.08 billion by 2026

Read More

Electric Vehicle Power Inverter Market Trends

Advancement in Bi-Directional Inverters Is a Latest Market Trend

Bidirectional inverters are gaining prominence in the electric vehicle (EV) market due to their ability to facilitate two-way energy transfer, allowing vehicles to draw power from the grid for charging and return excess energy to the grid or supply external loads. Bidirectional inverters convert AC (alternating current) to DC (direct current) during charging and reverse this process during discharging. This capability is essential for applications such as Vehicle-to-Grid (V2G), Vehicle-to-Home (V2H), and Vehicle-to-Load (V2L), where EVs can act as energy storage units, providing power during peak demand.

The incorporation of bidirectional inverters with V2G technology enables electric vehicles (EVs) to both draw power from the grid and return stored energy to it. This effectively converts EVs into portable energy resources, contributing to grid stability and providing users to lower electricity expenses or generate investment through in demand response initiatives. Such advancements are pivotal in fostering market growth.

In October 2024, Nissan announced plans to launch affordable bi-directional charging for selected electric vehicles models by 2026. EVs equipped with V2G technology can play a crucial role in integrating renewables energy into the grid. By storing electricity from wind or solar and directing it when needed, these vehicles help reduce dependency on fossil fuels.

Download Free sample to learn more about this report.

Market Drivers

Rising Demand for Electric Vehicles to Propel Market Growth

A major driving factor the electric vehicle power inverter market is the swift rise in EV demand. Research conducted by multiple industry analysts indicates that worldwide electric vehicle sales are projected to hit millions each year within the next ten years. Driven by environmental issues and government incentives, consumers are increasingly choosing electric vehicles over conventional gasoline-powered cars.

Each of these vehicles necessitates a power inverter, driving demand for the electric vehicle power inverter market. Advancements in battery technology are enhancing EV range and reducing charging time, making them more appealing and accessible to consumers. Battery efficiency is closely linked to the effectiveness of power inverters, resulting in improvements in inverter design and performance. This advancement propels market expansion throughout the forecast period.

Leading automotive manufacturers are increasing their production capabilities to meet the growing demand for electric vehicles. Consequently, the demand for power inverters is on the rise, as they are essential components in electric vehicle manufacturing. For instance, in January 2025, BYD announced the opening of a new overseas EV plant with an annual 150,000-vehicle capacity. The new facility in Indonesia can produce 150,000 vehicles annually, supporting BYD global expansion.

Market Restraints

High Complexity of Power Electronics May Hamper the Growth of the Market

Inverters are complex power electronic devices that require specialized understanding of both hardware and software systems. The intricate design and integration of components, along with the necessity for efficient thermal management solutions, add layers of complexity that can deter new players from entering the market. Furthermore, as technology quickly evolves, keeping pace with innovations and maintaining competitiveness can be a significant challenge for manufacturers. This complexity may hamper market growth. Higher switching frequencies and greater power density result in more heat generation, creating cooling challenges. Efficient thermal management systems are critical for maintaining performance and reliability, further increasing system complexity and cost.

Market Opportunity

Rising Growth of Electric Commercial Vehicle to Propel Market Demand

Electric commercial vehicles encompass a wide range of applications, including delivery vans, buses, trucks, and specialized vehicles for industries such as construction and logistics. Governments globally are implementing stringent emissions regulations and offering incentives to promote electric vehicles adoption. As cities aim to reduce air pollution and meet climate goals, fleets are transitioning away from traditional fossil fuel-powered vehicles. Advancements in battery technologies, including increased energy densities and cost reductions, have significantly influenced the viability of ECVs. Coupled with innovations in electric drivetrains and vehicle management systems, the performance and efficiency of electric commercial vehicles increased. Thus, increasing adoption and devolvement of electric commercial vehicles drive demand for power inverters, fostering market growth.

Segmentation Analysis

By Vehicle Type

Passenger Vehicle Segment Dominated due to Increasing Global Awareness About Environmental Concerns

Based on vehicle type, the market is segmented into passenger car and commercial vehicle.

In 2026, the passenger vehicle is expected to hold the largest share of the electric vehicle power inverter market contributing 94.26% globally in 2026. The increasing global consciousness about environmental problems and the enforcement of stricter emissions laws have resulted in a notable shift in consumers for electric vehicles, especially in the passenger car segment. This trend is bolstered by improvements in battery technology and enhanced charging infrastructure, increasing the accessibility and attractiveness of electric cars for consumers. This advancement drives demand in the power inverter market throughout the forecast period. The segment held 95% of the market share in 2024.

The commercial vehicle sector accounts for the second-largest market share due to swift electrification. The commercial vehicle industry is witnessing rapid expansion, especially in public transit and logistics. Transit agencies and logistics firms are progressively shifting their fleets to electric vehicles in order to lower operational expenses and adhere to strict emission standards. This advancement boosts the demand for electric vehicle power inverters.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion Type

Rising Investment by Automotive Manufacturers Encouraged BEV Segment Growth

By propulsion type, the market can be segmented into BEV and HEV.

The BEV (Battery Electric Vehicle) segment is projected to hold the maximum market with a share of 66.66% in 2026. Major automotive manufacturers are making significant investments in electric vehicle technologies. For instance, companies such as Volkswagen and Ford are allocating substantial resources to expand their electric vehicle portfolios, directly increasing the demand for efficient power inverters necessary for their operation. For instance, In March 2024, Volkswagen AG announced that the company would launch an entry-level electric vehicle by 2027. The company plans to launch 11 new electric vehicles over the next three years, including the ID.2, scheduled for launch in 2026 and priced at around USD 27,335.85 and models developed jointly with Chinese manufacturer Xpeng for the Chinese market. This devolvement drives the market growth. The segment is anticipated to capture 67.40% of the market share in 2025.

The PHEV segment holds the second-largest market share. Ongoing improvements in hybrid technology continue to improve vehicle performance and efficiency. Innovations in battery technology, such as solid-state batteries, offer increased range and reduced costs, making hybrids more appealing to consumers. This segment is likely to grow with a considerable CAGR of 15.50% during the forecast period (2026-2034).

By Technology Type

IGBT Segment Dominates due to High Efficiency and Performance

Based on technology, the market is segmented into IGBT and SiC.

The IGBT segment is expected to dominant the market with a share of 62.49% in 2026. IGBTs are crucial for converting direct current (DC) from electric vehicle batteries into alternating current (AC) to power electric motors. Their ability to operate at high voltages and provide fast switching capabilities makes them ideal for electric vehicle applications, significantly enhancing overall efficiency and performance. The segment is poised to attain 63% of the market share in 2025.

The SiC segment is anticipated to experience significant growth with a CAGR of 13.90% throughout the forecast duration due to its superior performance characteristics. SiC devices offer significant advantages over traditional silicon-based semiconductors, including higher thermal conductivity, greater breakdown voltage, and faster switching frequencies. These properties enhance the efficiency of power inverters, which is crucial for maximizing the range and performance of electric vehicles.

By Power Output

Upto 130kW segment Leads due to Swift Expansion of Affordable EVs Segment

Based on power output, the market is segmented into Upto 130kW and above 131 kW

The Upto 130kW segment is estimated to holds the maximum share of the market contributing 73.97% globally in 2026. Vehicles with power outputs up to 130 kW are commonly used in electric cars, which dominate the market. This power range is suited for most electric cars, making it a critical segment as consumer demand for electric passenger vehicles continues to grow. The surge in demand is further driven by the rapid expansion of affordable EV segments, including compact SUVs, family sedans, and light commercial vehicles. The segment is foreseen to grow with a share of 73.90% in 2025.

The Above 131KW segment holds the second-largest electric vehicle power inverter market share. Growth in this segment is attributed to technological advancement in power inverters. Continuous improvements in inverter technology have enhanced efficiency and performance, making them more attractive for mid-range electric vehicles. These advancements help manufacturers to optimize energy management and performance, further solidifying the market position. The segment is forecasted to register a substantial CAGR of 13.00% during the forecast period (2026-2034).

Electric Vehicle Power Inverter Market Regional Outlook

Based on the region, the market is studied across Asia Pacific, Europe, North America, and Rest of the World.

Asia Pacific

Asia Pacific Electric Vehicle Power Inverter Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific contributed 61.58% to the global market in 2025, with a valuation of USD 6.5 billion, and is projected to reach USD 8.39 billion in 2026. The Asia Pacific region is currently dominating the market and is expected to show highest CAGR during the forecast period. The regional growth is driven by high sales of EVs in emerging markets such as China, India, Japan, and South Korea. As the largest market within the Asia Pacific, China's dominance is attributed to its extensive EV production capacity and strong domestic demand. China is estimated to reach USD 6.16 billion in 2025. The Chinese government actively promotes electric vehicle adoption through various incentives, which has led to a substantial increase in EV exports and local manufacturing capabilities. This development increases the demand for the EV power inverter. The Japan market is expected to value at USD 0.08 billion by 2026, the China market is expected to value at USD 7.94 billion by 2026, and the India market is expected to value at USD 0.12 billion by 2026.

Europe

The Europe market generated USD 2.48 billion in 2025, representing 23.48% of the global market landscape, and is expected to reach USD 3.17 billion in 2026. The market for electric vehicle power inverters has grown significantly in Europe in recent years due to stricter emissions regulations, government support and incentives, and investment from OEMs. The European market is second largest in the overall market.

The U.K. market continues to grow, anticipated reach a market value of USD 0.39 billion in 2025. European countries are implementing strict emissions regulations to combat climate change and reduce air pollution. These regulations compel automotive manufacturers to transition from internal combustion engines to electric vehicles, thereby increasing the demand for EV power inverters, which are essential components of electric drivetrains. The UK market is expected to value at USD 0.5 billion by 2026, and the Germany market is expected to value at USD 0.97 billion by 2026, while France is poised to grow with a value of USD 0.33 billion in the 2025.

North America

In 2025, North America represented USD 1.16 billion, accounting for 10.98% of the worldwide market, and is projected to grow to USD 1.47 billion in 2026. North America is a growing market for EV power inverters, demonstrating increasing momentum in recent years. While historically lagging behind Asia Pacific and Europe, North America is witnessing a surge in EV interest and investment, fueled by government initiatives and automaker commitments. Increasing government incentives at both federal and state levels (especially in the U.S.), rising consumer awareness, growing charging infrastructure investment, and the entry of established automotive giants into the EV space are driving electric vehicle power inverter market growth. The U.S. market is expected to value at USD 1.28 billion by 2026.

Rest Of The World

Rest of the World contributed approximately USD 0.42 billion to the global market in 2025, accounting for 3.96% share, and is expected to reach USD 0.52 billion in 2026. In the rest of the world, the market is witnessing notable growth attributed to the growing urbanization and e-commerce growth. This has resulted in the heightened demand for commercial electric vehicles, which require efficient power inverter systems. As logistics companies seek to modernize their fleets with electric options, the need for reliable power inverters will increase significantly.

Competitive Landscape

Key Industry Players

Use Of Latest Innovation And Implementation Of Technology From Denso Are Contributing To The Market Growth

Key players in this market include Denso Corporation, Marelli Holdings Co., Ltd., and Mitsubishi Electric. Denso Corporation specializes in developing cutting-edge inverter technologies and plays a significant role in the power electronics segment for electric vehicles. Its inverters are known for their compact design and excellent performance. Denso Corporation is investing in next-generation technologies with higher efficiency rates to meet the evolving needs of the EV market.

List Of Key Electric Vehicle Power Inverter Companies Profiled:

- Denso Corporation (Japan)

- Toyota Industries Corporation (Japan)

- VALEO Limited (France)

- Continental AG (Germany)

- Marelli Holdings Co. Ltd. (Japan)

- Robert Bosch GmbH (Germany)

- Hitachi Astemo, Ltd. (Japan)

- Mitsubishi Electric (Japan)

- Nissan Motor Co. Ltd. (Japan)

- Vitesco Technologies Group AG (Germany)

- Meidensha Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS:

- September 2024- DENSO Corporation announced that it would start inverter production at DENSO Fukushima Co., Ltd. to reinforce its manufacturing capability in Japan and enhance the DENSO Group’s competitiveness in the electrification field. DENSO Fukushima, a subsidiary of the DENSO Group, specializes in manufacturing automotive thermal products, such as air conditioners, Engine Cooling Modules (ECMs), and fuel system components for gasoline engines.

- May 2024- Mitsubishi Electric signed a joint venture agreement with Aisin Corporation for EV components. The joint venture would focus on developing, producing, and selling traction motors, power converters, and their control software, optimizing them for vehicles and relevant systems. These components will be used in next-generation EVs, including battery EVs (BEVs) and plug-in hybrid vehicles (PHEVs).

- March 2024- DENSO CORPORATION unveiled its first inverter featuring silicon carbide (SiC) semiconductors. This inverter, integrated into the eAxle, an electric driving module created by Blue Nexus Corporation, will be utilized in the new Lexus RZ, the automaker’s inaugural dedicated battery electric vehicle (BEV) model, set to launch on March 2030.

- September 2023- LG Magna e-Powertrain announced that it is expanding its new facility in the city of Miskolc in north-eastern Hungary.

- July 2023- A leading automotive supplier “Marelli” has developed 800 Volt Silicon Carbide (SiC) inverters with improvement in inverters’ size, weight and especially efficiency. The innovative structural and cooling channel designs reduce the thermal resistance between the SiC components themselves and the cooling liquid . This will help to extract more energy from the battery at a higher efficiency and secure a significant increase in the driving range of a vehicle.

REPORT COVERAGE

The market research report provides a detailed analysis of the market and focuses on crucial aspects such as leading companies, vehicle types, and leading product types. Besides this, the report offers insights into the market trends and highlights vital industry developments. In addition to the factors above, the report encompasses several factors contributing to the market's growth over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.35% over 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type

|

|

By Propulsion Type

|

|

|

By Technology

|

|

|

By Power Output

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was valued at USD 10.56 billion in 2025 and is projected to reach USD 25.72 billion by 2034.

In 2025, the Asia Pacific market size stood at USD 6.5 billion.

The market is projected to grow at a CAGR of 8.35% and exhibit steady growth during the forecast period.

The battery electric vehicle (BEV) is the leading segment in global market.

Rising demand for electric vehicles is a key factor propelling market growth.

Major players in this market include Denso Corporation, Marelli Holdings Co., Ltd., and Mitsubishi Electric.

Asia Pacific dominated the market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us