Electroplating Market Size, Share & Industry Analysis, By Plating (Metals and Plastics), By End-use Industry (Automotive, Consumer Electronics, Aerospace & Defense, Medical Devices, Jewelry, and Others), and Regional Forecast, 2026-2034

Electroplating Market Size & Future Outlook

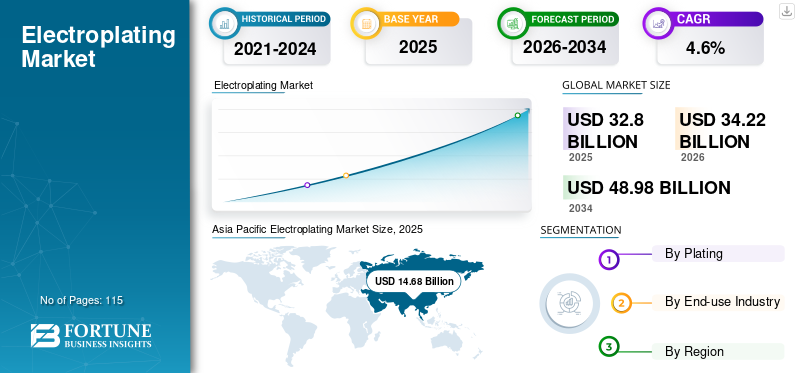

The global electroplating market size was valued at USD 32.80 billion in 2025. The market is projected to grow from USD 34.22 billion in 2026 to USD 48.98 billion by 2034 at a CAGR of 4.6% during the forecast period. Asia Pacific dominated the electroplating market with a market share of 44.75% in 2025.

Electroplating is a surface-finishing process in which a thin metallic coating is deposited onto a substrate by an electric current. The process is primarily used to enhance corrosion resistance, wear resistance, electrical conductivity, solderability, and aesthetic appearance of components. Common electroplated metals include nickel, chromium, copper, zinc, gold, silver, and tin, applied to a wide range of substrates, including steel, aluminum, plastics, and engineered polymers.

The market growth is supported by the increasing preference for this process across automotive manufacturing, electronics and electrical components, industrial machinery, aerospace parts, and decorative finishing applications. Beyond visual enhancement, plating with electric current delivers functional performance benefits that are difficult to replicate with alternative coating technologies. Key market participants include Atotech (MKS Instruments), MacDermid Alpha Electronics Solutions, DuPont, Coventya (Element Solutions), Uyemura, JCU Corporation, and regional specialty chemical suppliers and plating service providers.

Download Free sample to learn more about this report.

Electroplating Market KEY TAKEAWAYS

- 2025 Market Size: USD 32.80 billion

- 2026 Market Size: USD 34.22 billion

- 2034 Forecast Market Size: USD 48.98 billion

- CAGR: 4.6% from 2026–2034

- Asia Pacific dominated the market with a 44.75% share in 2025.

- Plastic plating segment is projected to grow at a CAGR of 3.9%.

- Others segment is projected to grow at a CAGR of 4.3%.

Asia Pacific

Largest regional market in 2025. Driven by automotive production, electronics manufacturing, and strong export-oriented industrial base across China, Japan, South Korea, and India.

North America

USD 5.83 billion in 2025. Mature industrial base and strong demand from automotive, aerospace, electronics, and medical device sectors drive growth.

Europe

Strong market supported by strict environmental regulations and demand from automotive, industrial machinery, and aerospace sectors.

U.S.

USD 5.83 billion in 2025. Demand driven by automotive, industrial, aerospace, and high-performance manufacturing applications.

Japan

Strong demand supported by advanced automotive and electronics manufacturing ecosystem.

Read More

ELECTROPLATING MARKET TRENDS

Shift Toward Functional and Performance-Driven Plating Systems to Incline Market Growth

A defining trend in the market is the transition from purely decorative coatings toward function-oriented plating systems designed to meet increasingly demanding performance requirements. Electroplated layers are now engineered to deliver precise electrical conductivity, wear resistance, thermal stability, and corrosion protection under harsh operating conditions. This trend is particularly evident in electronics, automotive electrification, and industrial connectors, where plating thickness, uniformity, and adhesion directly affect product reliability.

In electronics manufacturing, miniaturization and higher circuit densities are driving demand for advanced plating systems for copper, nickel, palladium, and gold with tight process control. Similarly, automotive OEMs increasingly specify functional electroplating for connectors, sensors, battery components, and powertrain parts to ensure durability and long service life. As a result, electroplating is positioned less as a commoditized surface treatment and more as a performance-critical enabling technology embedded in complex manufacturing value chains.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Automotive, Electronics, and Industrial Manufacturing Base to Drive Market Growth

The primary driver for the market is sustained growth in downstream manufacturing industries that rely on plated components for performance and durability. Automotive production remains a cornerstone, with electroplating widely used for corrosion protection, decorative finishes, fasteners, connectors, and increasingly for electric vehicle (EV) components such as battery terminals and electronic control units. Rising global vehicle production and the shift toward electrified drivetrains structurally reinforce market demand.

Electronics and electrical equipment manufacturing represent another strong demand pillar. This process of electric printing is indispensable for printed circuit boards, semiconductors, connectors, switches, and consumer electronics, where conductive and corrosion-resistant coatings are essential. Industrial machinery, construction hardware, and aerospace components further contribute to baseline demand, as electroplated surfaces extend component life and reduce maintenance requirements. Together, these end-use sectors provide a stable and diversified demand base that supports long-term electroplating market growth.

MARKET RESTRAINTS

Environmental Regulations and Compliance Cost Pressures to Restrict Market

Environmental and occupational safety regulations represent a significant restraint for the market. Traditional plating processes using electric current involve hazardous substances such as hexavalent chromium, cyanides, and heavy metals, generating wastewater and sludge that require complex treatment and disposal. Regulatory frameworks governing effluent discharge, air emissions, and chemical handling continue to tighten, particularly in North America and Europe.

Compliance with these regulations increases operational complexity and cost, especially for small and mid-sized plating facilities. Investment in wastewater treatment systems, chemical substitution, process monitoring, and worker safety infrastructure raises capital and operating expenditures. In cost-sensitive markets, these factors can delay capacity expansion, encourage consolidation, or push smaller operators out of the market, limiting broader penetration and slowing overall growth.

MARKET OPPORTUNITIES

Transition to Sustainable and Advanced Electroplating Technologies to Surge Market Growth

A major opportunity for the market lies in developing and adopting environmentally improved plating chemistries and processes. Trivalent chromium systems, cyanide-free baths, low-toxicity additives, and closed-loop water recycling technologies are gaining traction as manufacturers seek regulatory compliance without sacrificing performance. Suppliers that offer validated, drop-in alternatives to legacy chemistries are well-positioned to capture demand from both OEMs and plating service providers.

In parallel, growth in electric vehicles, renewable energy systems, and advanced electronics creates new application opportunities for precision electroplating. High-reliability connectors, battery components, power electronics, and sensor systems increasingly require specialized plated coatings with exacting specifications. These applications favor higher-value chemical formulations, technical support, and process expertise, enabling suppliers to move up the value chain beyond commodity plating solutions.

MARKET CHALLENGES

Process Complexity, Skill Requirements, and Cost Optimization are Prominent Market Challenges

A persistent challenge in the market is managing process complexity while maintaining consistent quality and cost efficiency. Electroplating outcomes are highly sensitive to bath chemistry, temperature, current density, and substrate preparation. Variability in any of these parameters can lead to defects, rework, and scrap, particularly in high-precision applications such as electronics and aerospace.

Additionally, the industry faces a shortage of skilled operators and process engineers capable of managing advanced plating systems. As plating processes become more automated and digitally controlled, the need for technical expertise increases. Balancing quality assurance, regulatory compliance, and cost competitiveness remains a key operational challenge, especially in regions with limited technical training infrastructure or rising labor costs.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Global trade tensions, energy price volatility, and supply chain disruptions influence the market through upstream raw materials, including nickel, copper, chromium compounds, and specialty additives. Price fluctuations and supply constraints can directly affect plating costs and profitability, particularly for operations that depend on imported chemicals or metals.

At the same time, regionalization of manufacturing and supply chains is reshaping demand patterns. Governments and OEMs increasingly emphasize localized production of automotive, electronic, and industrial components, thereby indirectly supporting the regional expansion of electroplating capacity. This trend benefits domestic plating service providers and chemical suppliers while increasing competitive pressure on globalized supply models.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D activity in the market focuses on improving environmental performance, process efficiency, and application-specific functionality. Key areas include the development of low-toxicity plating baths, improved additive systems for deposit uniformity, and coatings engineered for specific electrical or mechanical properties. Suppliers are also investing in formulations that reduce energy consumption and extend bath life.

Digitalization is emerging as a complementary innovation trend. Automated bath monitoring, real-time analytics, and digitally controlled dosing systems help improve consistency, reduce chemical consumption, and support regulatory compliance. In high-precision segments such as electronics and EV components, R&D increasingly integrates chemistry development with process control and data-driven optimization.

SEGMENTATION ANALYSIS

By Plating

Metal Plating Dominates Due to Structural Role in Corrosion Protection and Electrical Performance

Based on plating, the market is segmented into metals and plastics.

Among these, metal plating accounts for the dominant share of the global market. This dominance is driven by the extensive use of electroplated metal components across automotive, electronics, industrial machinery, construction hardware, and aerospace applications. Electroplating of metals such as steel, aluminum, copper, and zinc alloys is critical for improving corrosion resistance, wear protection, surface hardness, and electrical conductivity. In automotive and industrial applications, metal plating is essential for fasteners, connectors, brackets, housings, and other functional components that are subject to mechanical stress and corrosive environments. The continued expansion of vehicle production, industrial equipment manufacturing, and electrical infrastructure directly sustains demand for metal plating.

The plastic plating segment is a smaller but steadily growing market, driven primarily by lightweighting trends and the integration of aesthetics and functionality in automotive and consumer electronics applications. Electroplated plastics, typically based on ABS and other engineering polymers, are increasingly used for interior and exterior automotive trims, decorative components, appliance housings, and consumer goods. Plastic plating enables manufacturers to achieve a metallic appearance, electromagnetic shielding, and improved surface durability while reducing overall component weight. The segment is anticipated to grow at a CAGR of 3.9% during the study period.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Automotive Segment Leads Due To High Adoption in Panels and Interior Components

Based on end-use industry, the market is segmented into automotive, consumer electronics, aerospace & defense, medical devices, jewelry, and others.

Among these, the automotive segment accounts for the largest global electroplating market share. This dominance is primarily driven by the high volume of plated components used per vehicle and the critical functional role plating plays in automotive manufacturing. The process is widely used on fasteners, connectors, braking components, fuel system parts, decorative trims, and structural hardware to enhance corrosion resistance, wear protection, and long-term durability. In both internal combustion engine vehicles and electric vehicles, electroplated coatings are essential for maintaining component performance under thermal stress, vibration, and exposure to corrosive environments.

The consumer electronics segment accounts for a significant share of the market, driven by strong demand for electroplated printed circuit boards, connectors, and semiconductor packaging. Electroplating is critical for achieving precise conductivity, signal integrity, and corrosion resistance in compact electronic devices. However, high pricing pressure and rapid product life cycles limit margin expansion in this segment despite strong demand for volume.

The aerospace & defense segment is a smaller but high-value market where plating with electric current is used to provide wear-, corrosion-, and high-reliability-resistant coatings on aircraft components, landing gear, fasteners, and defense hardware. Stringent certification requirements, long qualification cycles, and low production volumes constrain overall market share but support premium pricing.

The others segment includes fasteners and tools, energy equipment, and household appliances. These uses are highly application-specific and are influenced by regional industrial activity, cost considerations, and the availability of alternative surface-finishing technologies. The others segment is expected to grow at a CAGR of 4.3% during the forecast period.

ELECTROPLATING MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Electroplating Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for the leading market share in 2025. The region benefits from large-scale automotive production, extensive electronics manufacturing capacity, and a dense network of metal-finishing and plating service providers. China, Japan, South Korea, and increasingly India and Southeast Asian countries form the core demand base, driven by automotive components, consumer electronics, industrial machinery, and export-oriented manufacturing.

China remains the single most influential market in the region due to its integrated automotive and electronics supply chains and extensive domestic plating capacity. While environmental regulations are tightening, especially around wastewater discharge and hazardous chemicals, demand remains robust as manufacturers invest in compliant and upgraded plating technologies.

China Electroplating Market

China’s market is one of the largest worldwide, with 2025 revenue recorded at USD 8.12 billion, representing roughly 24.7% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America represents a mature, technology-driven market characterized by strong demand from automotive, aerospace & defense, electronics, and medical device manufacturing. The U.S. accounts for the majority of regional demand, supported by a well-established industrial base and high standards for product reliability and surface performance.

U.S. Electroplating Market

In 2025, the U.S. represented USD 5.83 billion market in North America, driven primarily by strong demand from the industrial and automotive sectors. The U.S. accounts for roughly 17.8% of global market sales.

Europe

Europe’s market is shaped by stringent environmental regulations, high manufacturing standards, and a strong automotive and industrial base. Germany, Italy, France, and the U.K. are key contributors, with demand concentrated in automotive components, industrial machinery, and aerospace applications.

Germany Electroplating Market

The Germany market value in 2025 was recorded at USD 1.85 billion, representing roughly 5.6% of global market revenues.

U.K. Electroplating Market

The U.K. market size in 2025 was at around USD 1.46 billion, representing roughly 4.4% of global market revenues.

Latin America

The Latin America market is moderate in size but is gradually expanding, supported by automotive assembly, industrial manufacturing, and consumer goods production. Brazil and Mexico are the primary demand centers, benefiting from their automotive manufacturing ecosystems and proximity to North American supply chains.

Middle East & Africa

The Middle East & Africa market is relatively small and highly fragmented, with demand concentrated in industrial maintenance, construction hardware, automotive aftermarket, and limited manufacturing applications. The Gulf Cooperation Council (GCC) countries and South Africa represent the most developed markets, supported by industrial activity, infrastructure development, and localized manufacturing.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

China-Led Giants Dominate Global Market as Overcapacity Pressures Margins Worldwide

Large multinational players with strong engineering capabilities and global manufacturing footprints characterize the market. Leading companies focus on material innovation, end-use industry engineering, and long-term OEM partnerships to maintain a competitive advantage. Leading producers, such as Atotech, MacDermid Alpha Electronics Solutions, Uyemura & Co. Ltd., JCU Corporation, and Coventya Holding SAS, are directing capital toward process optimization, product quality enhancement, and environmentally aligned manufacturing practices. Innovation efforts are increasingly focused on enhancing purity consistency, reducing the environmental footprint, and developing grades suitable for advanced products.

LIST OF KEY ELECTROPLATING COMPANIES PROFILED

- Atotech (MKS Instruments) (Germany)

- MacDermid Alpha Electronics Solutions (U.S.)

- Uyemura & Co., Ltd. (Japan)

- JCU Corporation (Japan)

- Coventya Holding SAS (Element Solutions Inc.) (France)

- DuPont de Nemours, Inc. (U.S.)

- BASF SE (Germany)

- DOW Inc. (U.S.)

- Technic Inc. (U.S.)

- Heraeus Precious Metals (Germany)

KEY INDUSTRY DEVELOPMENTS

- April 2025: JCU announced enhancements to its electroplating additives and process control technologies designed for high-speed PCB and package substrate manufacturing. The developments aim to improve line stability and reduce chemical consumption, aligning with sustainability and cost-efficiency objectives.

- March 2025: Atotech continued to expand its advanced electroplating chemistry portfolio for automotive electronics and semiconductor packaging applications, emphasizing environmentally compliant systems with enhanced deposit uniformity and bath stability. The company reinforced its positioning in EV-related connectors and high-density electronics through targeted process optimization solutions.

- January 2025: Element Solutions, through its MacDermid Alpha and Coventya businesses, advanced integration of surface finishing technologies aimed at electronics, automotive, and industrial markets. The company highlighted increased investment in sustainable electroplating chemistries and digital process control tools to improve customer yield and regulatory compliance.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, plating, and the end-use industry. Additionally, it offers valuable insights into the market and current industry trends, and highlights key developments. In addition to the factors mentioned above, the report encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) |

| Growth Rate | CAGR of 4.6% from 2026 to 2034 |

| Segmentation | By Plating, End-use Industry, and Region |

| By Plating |

|

| By End-use Industry |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 32.80 billion in 2025 and is projected to reach USD 48.98 billion by 2034.

Recording a CAGR of 4.6%, the market is slated to exhibit steady growth during the forecast period.

Based on end-use industry, the automotive segment led in 2025.

Asia Pacific held the highest market share in 2025.

The expanding automotive, electronics, and industrial manufacturing base is driving the market growth.

- 2021-2034

- 2025

- 2021-2024

- 115

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us