Emission Control Catalysts Market Size, Share & Industry Analysis, By Precious Metal Type (Palladium, Platinum, Rhodium, and Others), By End-Use Industry (Automotive & Transportation, Mining & Power, Oil & Gas, Chemical Industry, and Others), and Regional Forecast, 2026-2034

Emission Control Catalysts Market Size and Future Outlook

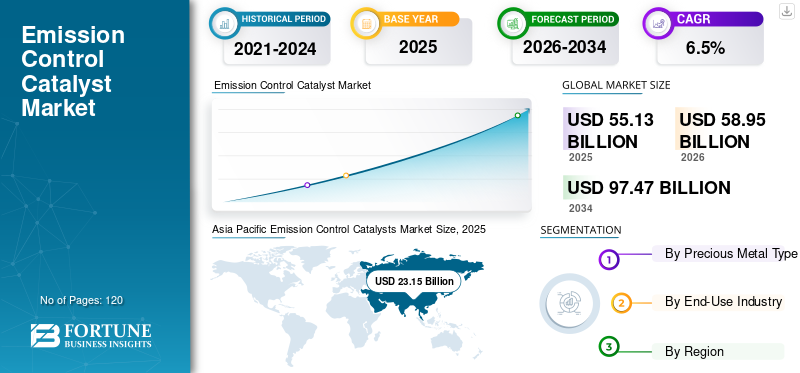

The global emission control catalysts market size was valued at USD 55.13 billion in 2025 and is projected to grow from USD 58.95 billion in 2026 to USD 97.47 billion by 2034, exhibiting a CAGR of 6.5% during the forecast period. Asia Pacific dominated the global market with a share of 41.99% in 2025.

Emission control catalysts are materials used in vehicles and the industrial sector to reduce harmful emissions released into the air during fuel combustion. They work by converting pollutants such as carbon monoxide, nitrogen oxides, and unburned hydrocarbons into less harmful substances before the exhaust is released into the environment. These catalysts are valued as they help meet strict air pollution regulations, improve air quality, and support the cleaner operation of engines and industrial processes. They are widely used in passenger vehicles, commercial vehicles, power plants, and various industrial applications where emission reduction is required. In addition, ongoing upgrades to emission standards and the replacement of older systems with more efficient technologies are driving the growth of the emission control catalysts market.

The market is mainly dominated by a limited number of well-established companies with strong production capabilities and extensive experience in emissions control technologies. Leading players such as BASF, Johnson Matthey, Umicore, Clariant, and Cataler Corporation compete by leveraging large-scale manufacturing, proven technical expertise, and reliable supply networks to meet the needs of automotive manufacturers and industrial emission control applications.

Download Free sample to learn more about this report.

EMISSION CONTROL CATALYSTS MARKET TRENDS

Increasing Focus on Developing Catalyst Boosts Industry Development

A key trend in the market is the growing focus on developing catalysts that deliver higher emission conversion efficiency while using lower amounts of precious metals. Manufacturers are investing in improved catalyst formulations, advanced coatings, and optimized substrate designs to meet stricter emission limits without significantly increasing system costs. As regulatory testing becomes more stringent and closer to real operating conditions, suppliers are prioritizing durability, thermal stability, and consistent performance over the full service life of the catalyst.

- According to the European Commission, the introduction of Real Driving Emissions (RDE) testing requires vehicles to comply with emission limits under real-world driving conditions rather than only laboratory testing, driving the development of more efficient and durable pollution control catalysts with improved real-world performance.

MARKET DYNAMICS

MARKET DRIVERS

Tightening Emission Regulations to Drive Product Demand

Demand for pollution control catalysts is strongly driven by increasingly strict air pollution regulations for vehicles and industrial sources. Governments across major regions are enforcing tougher emission standards to limit harmful gases released from automobiles, power plants, and manufacturing facilities. Pollution control catalysts are widely used as they help convert toxic exhaust gases into less harmful substances, supporting compliance with these regulations and improving air quality. In addition, growing vehicle production, especially in emerging economies, and increased regulatory monitoring of industrial emissions are further supporting steady demand for pollution control catalysts across automotive and industrial applications.

- According to the U.S. Environmental Protection Agency (EPA), finalized multi-pollutant emissions standards for light- and medium-duty vehicles mandate substantially lower limits on nitrogen oxides and other harmful pollutants. This directly increases the need for advanced emission control systems, including catalytic technologies, to ensure compliance with future vehicle regulations.

MARKET RESTRAINTS

High Cost of Precious Metals to Restrain Market Growth

The pollution control catalysts market faces a key restraint due to its reliance on expensive precious metals such as platinum, palladium, and rhodium, which are essential for catalyst performance. Prices of these metals are highly volatile and influenced by mining supply constraints, geopolitical factors, and demand from multiple industries, including the automotive sector and electronics sector. Sudden increases in raw material costs raise production expenses for catalyst manufacturers and can pressure margins or increase system costs for vehicle and equipment producers.

- According to the U.S. Geological Survey (USGS) Mineral Commodity Summaries, prices of platinum group metals such as platinum, palladium, and rhodium have shown significant volatility due to supply concentration and market imbalances, directly impacting production costs for automotive catalysts that rely heavily on these metals.

MARKET OPPORTUNITIES

Electrification and Transition to Cleaner Mobility to Create New Opportunities

The pollution control catalysts market has growing opportunities as the global transport sector transitions toward cleaner mobility, while internal combustion engines remain in use during the transition period. Hybrid vehicles, range-extender engines, and cleaner gasoline and diesel models still require advanced emission control systems to meet tightening regulatory limits. As governments balance electrification goals with near- to medium-term emission reduction needs, demand for high-performance pollution control catalysts is expected to remain strong.

- According to the International Energy Agency (IEA), internal combustion engine vehicles, including hybrids, are expected to remain a significant part of the global vehicle fleet through the 2030s, meaning advanced emission control technologies will continue to be required to reduce exhaust emissions during the transition toward electrification.

MARKET CHALLENGES

Transition Toward Electrification and Declining Long-Term ICE Volumes to Create Market Challenges

The market faces a structural challenge from the accelerating shift toward vehicle electrification and long-term reduction in internal combustion engine production. As governments promote electric vehicles through incentives, mandates, and phase-out targets for combustion engines, future demand growth for emission control systems becomes less predictable. While catalysts remain essential in the near to medium term, uncertainty around the pace of electrification complicates long-term capacity planning and investment decisions for manufacturers.

- According to the International Energy Agency (IEA), rising electric vehicle adoption and long-term policy targets to reduce internal combustion engine usage are expected to gradually lower the share of combustion-engine vehicles, creating long-term demand uncertainty for emission control catalyst applications.

Download Free sample to learn more about this report.

Segmentation Analysis

By Precious Metal Type

Palladium Segment Dominates Due to Its Wide Use in Gasoline Emission Control Systems

Based on precious metal type, the market is segmented into palladium, platinum, rhodium, and others.

The palladium segment holds the largest emission control catalysts market share as it is widely used in gasoline vehicle catalytic converters, which represent a major portion of global vehicle production. It is highly effective in controlling hydrocarbons and carbon monoxide emissions and performs well under typical gasoline engine operating conditions. Compared with platinum, palladium is often preferred due to its strong catalytic activity and, historically, more favorable cost positioning, making it suitable for large-scale automotive applications.

- According to the U.S. Geological Survey (USGS) Minerals Yearbook: Platinum-Group Metals, palladium represents the largest share of platinum-group metal consumption in automotive catalytic converters, reflecting its dominant use in gasoline vehicle emission control systems.

To know how our report can help streamline your business, Speak to Analyst

The platinum segment is expected to grow at a CAGR of 6.3% over the forecast period.

By End-Use Industry

Automotive & Transportation Segment Dominates due to Compliance with Emission Regulations

In terms of end-use industry, the market is categorized into automotive & transportation, mining & power, oil & gas, chemical industry, and others.

The automotive and transportation segment holds the largest share of the market as emission control systems are mandatory for most on-road vehicles. Passenger cars, light commercial vehicles, heavy-duty trucks, and buses all require catalytic converters to comply with emission regulations targeting pollutants such as carbon monoxide, nitrogen oxides, and hydrocarbons.

- According to a Science Direct study, catalytic converters are essential emission control devices used across gasoline and diesel vehicles to reduce carbon monoxide, hydrocarbons, and nitrogen oxides, making the automotive and transportation sector the primary end-use industry for pollution control catalysts.

The mining & power segment is expected to grow at a CAGR of 6.5% over the forecast period.

Emission Control Catalysts Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific Emission Control Catalysts Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant position in the global market in 2025, valued at approximately USD 23.15 billion, and is expected to maintain its leading share in 2026, reaching around USD 24.87 billion. The region’s leadership is supported by high vehicle production volumes, tightening emission regulations, and continued growth in automotive manufacturing across major economies. Rapid urbanization, rising personal vehicle ownership, and expanding commercial transport fleets further sustain demand for emission control systems.

China Emission Control Catalysts Market

Based on Asia Pacific’s strong contribution and China’s position as the world’s largest automotive manufacturing hub, the China pollution control catalysts industry is analytically reached USD 10.42 billion in 2025, accounting for approximately 45% of regional revenues. Demand is driven by large-scale passenger vehicle production, a sizeable commercial vehicle fleet, and strict enforcement of China VI emission standards.

India Emission Control Catalysts Market

The Indian emission control catalysts market in 2025 is estimated at around USD 4.63 billion. Growth is supported by rising vehicle sales, expanding road transport activity, and the nationwide implementation of Bharat Stage VI emission norms. Increasing regulatory focus on air quality, along with ongoing upgrades in both passenger and commercial vehicle segments, is driving consistent demand for pollution control catalysts across the country.

North America

North America remains an important regional market for emission control catalysts, reaching approximately USD 9.92 billion in 2025. Demand is supported by strict vehicle emission regulations, steady automotive production, and ongoing replacement demand for catalytic converters in both passenger and commercial vehicles. The region also benefits from a well-established automotive manufacturing base and strong regulatory enforcement, which ensures consistent adoption of emission control technology across transportation and industrial applications.

U.S. Emission Control Catalysts Market

The U.S. market in 2025 stood at around USD 8.43 billion, accounting for approximately 85.0% of regional revenues. Demand is driven by mandatory use of catalytic converters in gasoline and diesel vehicles, stringent EPA emission standards, and a large on-road vehicle fleet requiring both original equipment and replacement catalysts.

Europe

Europe is projected to record steady growth in the emission control catalysts market, reaching a valuation of approximately USD 14.9 billion in 2025. The region is shaped by stringent emission regulations, strong environmental policy enforcement, and high adoption of advanced emission control technologies. Continuous updates to Euro emission standards and a strong focus on reducing urban air pollution support sustained demand for catalytic converters across passenger cars and commercial vehicles.

Germany Emission Control Catalysts Market

Germany’s market reached around USD 4.47 billion in 2025, accounting for approximately 30.0% of regional demand. Consumption is supported by the country’s strong automotive manufacturing industry, high vehicle ownership levels, and strict compliance with Euro emission standards.

Italy Emission Control Catalysts Market

The Italian market in 2025 is estimated at approximately USD 2.23 billion, representing roughly 15.0% of regional revenues. Demand is driven by widespread use of emission control systems across the passenger vehicle fleet, ongoing vehicle replacement cycles, and regulatory pressure to maintain compliance with European emission norms, particularly in urban and industrial regions.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in the pollution control catalysts market over the forecast period. The Latin America market reached approximately USD 4.41 billion in 2025, supported by rising vehicle ownership, gradual tightening of emission regulations, and growing focus on urban air quality. The Middle East & Africa market is expected to reach around USD 2.76 billion in 2025, driven by expanding vehicle fleets, improving fuel quality standards, and the phased adoption of emission control requirements in key countries.

Brazil Emission Control Catalysts Market

The Brazil market in 2025 is estimated at USD 1.98 billion, accounting for approximately 45.0% of Latin America revenues. Demand is driven by Brazil’s large automotive manufacturing base, widespread use of emission control systems in passenger and commercial vehicles, and enforcement of national emission standards such as PROCONVE, which mandate the use of catalytic converters.

COMPETITIVE LANDSCAPE

Key Industry Players

High Upfront Investment in Precious Metal Handling Shapes Competition in the Market

The pollution control catalysts market is relatively consolidated and capital-intensive as large-scale production requires advanced manufacturing facilities, specialized coating and formulation technologies, and strict compliance with environmental and performance standards. High upfront investment in precious metal handling, process control, and regulatory certification creates high entry barriers and limits the number of new participants in the market.

BASF, Johnson Matthey, Umicore, Clariant, and Cataler Corporation mainly concentrate on improving operational efficiency, upgrading product performance, and strengthening upstream integration rather than aggressively expanding capacity.

LIST OF KEY EMISSION CONTROL CATALYSTS COMPANIES PROFILED

- BASF (U.S.)

- Johnson Matthey (U.S.)

- Umicore (U.S.)

- Cataler Corporation (U.S.)

- Clariant (U.S.)

- CORMETECH. (U.S.)

- Mitsubishi Power Americas, Inc. (Austria)

- Tenneco Inc. (Italy)

- Ecocat India Pvt Ltd. (India)

- DCL International Inc. (India)

KEY INDUSTRY DEVELOPMENTS

- May 2025: Johnson Matthey agreed to sell its Catalyst Technologies business to Honeywell, reshaping Johnson Matthey’s portfolio and expanding Honeywell’s catalysts/process technology position.

- December 2024: BASF (ECMS) launched its VOC2.0 / VOZC cabin-air catalyst technology for installation on the Airbus A320 family, expanding catalyst applications into aircraft cabin air treatment.

- August 2024: BASF (ECMS) inaugurated a new Research, Development & Application (RD&A) lab in Chennai, India, strengthening regional development for automotive emissions control catalysts.

- March 2024: Cataler North America started operations at its new Hickory Plant (North Carolina), expanding production capacity for automotive exhaust emission purification catalysts.

- February 2024: BASF (ECMS) completed the acquisition of Arc Metal AB (Sweden), adding smelting capability linked to processing/recycling of spent automotive catalysts.

REPORT COVERAGE

The global emission control catalysts market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key market developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key market players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.5% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Precious Metal Type, End-Use Industry, and Region |

|

By Precious Metal Type |

· Palladium · Platinum · Rhodium · Others |

|

By End-Use Industry |

· Automotive & Transportation · Mining & Power · Oil & Gas · Chemical Industry · Others |

|

By Geography |

· North America (By Precious Metal Type, End-Use Industry, and Country) o U.S. (By End-Use Industry) o Canada (By End-Use Industry) · Europe (By Precious Metal Type, End-Use Industry, and Country/Sub-region) o Germany (By End-Use Industry) o U.K. (By End-Use Industry) o France (By End-Use Industry) o Italy (By End-Use Industry) o Rest of Europe (By End-Use Industry) · Asia Pacific (By Precious Metal Type, End-Use Industry, and Country/Sub-region) o China (By End-Use Industry) o India (By End-Use Industry) o Japan (By End-Use Industry) o South Korea (By End-Use Industry) o Rest of Asia Pacific (By End-Use Industry) · Latin America (By Precious Metal Type, End-Use Industry, and Country/Sub-region) o Brazil (By End-Use Industry) o Mexico (By End-Use Industry) o Rest of Latin America (By End-Use Industry) · Middle East & Africa (By Precious Metal Type, End-Use Industry, and Country/Sub-region) o Saudi Arabia (By End-Use Industry) o South Africa (By End-Use Industry) o Rest of the Middle East & Africa (By End-Use Industry) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 55.13 billion in 2025 and is projected to reach USD 97.47 billion by 2034.

Recording a CAGR of 6.5%, the market is slated to exhibit steady growth during the forecast period (2026-2034).

The automotive & transportation segment leads the market.

Asia Pacific held the highest market share in 2025.

Tightening emission regulations is the key factor driving the market.

BASF, Johnson Matthey, Umicore, Clariant, and Cataler Corporation are some of the top players in the market

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us