Energy Drinks Market Size, Share & Industry Analysis, By Product Type (Energy Drinks and Energy Shots), By Packaging Type (Cans & Tins, PET Bottles, and Others), By Flavor (Citrus, Tropical fruits, Berries, Herbs, and Others), By Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail, and Others), and Regional Forecast, 2026–2034

(Offer valid till 15th Aug 2026)

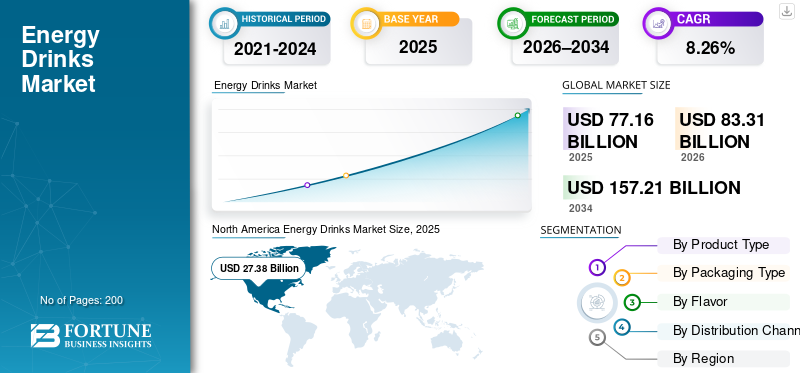

Energy Drinks Market Overview

The global energy drinks market size was valued at USD 77.16 billion in 2025. The market is projected to grow from USD 83.31 billion in 2026 to USD 157.21 billion by 2034, exhibiting a CAGR of 8.26% during the forecast period. North America dominated the energy drinks market with a market share of 35.48% in 2025.

The global energy drinks industry gained popularity due to growing demand for functional beverages that deliver instant energy, improved mental alertness, and enhanced physical performance. Increasing urbanization, longer working hours, growing participation in sports and fitness activities, and expanding consumption among younger demographics are structurally reshaping the global energy drinks market demand. Continuous innovation in formulations, sugar reduction, clean-label positioning, and diversified flavor offerings is further accelerating penetration across developed and emerging markets.

The market growth is expected to be dominated by key players such as Red Bull GmbH, Monster Beverage Corporation, PepsiCo, Inc., The Coca-Cola Company, and Lucozade Ribena Suntory Ltd.

Download Free sample to learn more about this report.

Energy Drinks Market Key Takeaways

- 2025 Market Size: USD 77.16 Billion

- 2026 Market Size: USD 83.31 Billion

- 2034 Forecast Market Size: USD 157.21 Billion

- CAGR: 8.26% from 2026–2034

- North America dominated the energy drinks market with a 35.48% share in 2025.

- The energy drinks segment held the largest market share, valued at USD 71.27 billion in 2025.

- The cans & tins segment led the market, reaching USD 52.59 billion in 2025.

North America

North America led the global market with USD 27.38 billion in 2025 and is projected to grow at a CAGR of 7.77%.

Asia Pacific

Asia Pacific reached USD 19.88 billion in 2025 and is the fastest-growing regional market with a CAGR of 9.13%.

Europe

Europe accounted for USD 22.01 billion in 2025 and is expected to expand at a CAGR of 8.71%.

U.S.

The market was valued at USD 22.15 billion in 2025, driven by strong demand for functional beverages.

Japan

Growing health-conscious consumption and demand for functional energy beverages support market expansion.

Read More

Energy Drinks Market Trends

Functional Positioning and Clean-Label Reformulation Shaping Industry Growth

Organic energy drinks are increasingly positioned as functional lifestyle energy boosting beverages rather than indulgent stimulants. Manufacturers are reformulating products using natural caffeine sources such as green coffee beans, guarana, and yerba mate, alongside reduced sugar and added micronutrients including B-complex vitamins, electrolytes, and magnesium. This shift is particularly strong among millennials and Gen Z consumers who prioritize performance, wellness, and natural ingredient transparency. Demand for sugar-free and low-calorie variants is rising rapidly as awareness around obesity and metabolic disorders increases globally.

- For instance, in November 2024, Red Bull launched Red Bull Zero, a zero-sugar, zero-calorie version of its original energy drink flavor, to expand its sugar-free portfolio. This new variant aims to closely mimic the taste of the original Red Bull while using low- and non-caloric sweeteners such as monk fruit extract, distinguishing it from Red Bull Sugarfree (which uses different sweeteners such as aspartame). It retains the same functional ingredients such as caffeine, taurine, and B-group vitamins, for an energy level boost, concentration, and fatigue reduction.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Expansion of Sports, Fitness, and Active Lifestyle Culture Accelerating Energy Drink Consumption

The global rise in sports participation, gym memberships, endurance activities, and recreational fitness is structurally boosting consumption of energy drinks as pre-workout and performance-support beverages. Energy drinks are increasingly consumed before workouts, sporting events, and physically demanding activities due to their caffeine, electrolyte, and vitamin content. This trend is particularly strong among urban populations and younger health conscious consumers seeking functional benefits beyond hydration, further fueling the global energy drinks market growth.

- According to the World Health Organization (WHO), nearly one-third (31%) of adults globally, approximately 1.8 billion people, did not meet the recommended levels of physical activity in 2022. This has been prompting increased participation in fitness and wellness programs that rely on performance-enhancing beverages.

Market Restraints

Stringent Caffeine Content Regulations and Maximum Intake Limits Constraining Product Formulation

Energy drinks face increasing regulatory pressure due to concerns over excessive caffeine intake. Several countries impose maximum permissible caffeine limits, mandatory warning labels, and usage advisories, forcing manufacturers to reformulate products or limit serving sizes. These regulations reduce formulation flexibility and complicate cross-border standardization of products, particularly for multinational brands.

- The European Food Safety Authority (EFSA) caps caffeine concentration in energy drinks at 320 mg per liter, restricting potency compared to less regulated markets.

Market Opportunities

Innovation in Sustainable and Circular Packaging as a Brand Differentiator to Unlock New Growth Avenues for Market

Sustainability-led innovation in recyclable aluminum, plant-based PET, refillable containers, and carbon-neutral packaging represents both a compliance requirement and a differentiation opportunity. Brands that proactively invest in circular packaging models can enhance premium positioning and consumer trust.

- For instance, in June 2025, Ball Corporation and Açaí Motion have partnered to launch ASI-certified sustainable aluminum cans for the Brazilian natural energy drink brand's products. This initiative emphasizes environmental responsibility in beverage packaging. The collaboration introduces cans certified by the Aluminium Stewardship Initiative (ASI), ensuring high environmental, social, and governance standards from mining to manufacturing.

SEGMENTATION ANALYSIS

By Product Type

Energy Drinks Segment Dominated Due to Broad Consumer Base

Based on product type, the market is segmented into energy drinks and energy shots.

The energy drinks segment dominated the global energy drinks market share, valued at USD 71.27 billion in 2025, supported by mass-market availability, habitual consumption patterns, and strong brand recognition. These products benefit from multipack retailing, on-the-go usage, and extensive flavor diversification.

The energy shots segment is projected to grow at the fastest CAGR of 10.64% during 2026–2034, driven by compact formats, higher caffeine concentration, and rising adoption among working professionals and athletes.

To know how our report can help streamline your business, Speak to Analyst

By Packaging Type

Cans & Tins Segment Led Market Due to Convenience and Shelf Stability

By packaging type, the market is segmented into cans & tins, PET bottles, and others.

Cans & tins dominated the market with a value of USD 52.59 billion in 2025, driven by portability, rapid chilling properties, recyclability, and strong alignment with energy drink branding.

PET bottles continue to see steady demand, with a CAGR of 7.13% over the projected period, while alternative packaging formats are expanding at a moderate pace due to sustainability initiatives and premium positioning.

By Flavor

Citrus Flavor Segment Dominated Due to Mass Appeal

By flavor, the market is segmented into citrus, tropical fruits, berries, herbs, and others.

The citrus segment led the market, valued at USD 23.62 billion in 2025, reflecting consumer preference for refreshing, familiar, and versatile flavor profiles.

Herbs segment is projected to grow at the fastest CAGR of 9.74% during the forecast period, supported by natural positioning and perceived health and wellness benefits.

By Distribution Channel

Supermarkets/Hypermarkets Dominated Due to High Visibility and Volume Sales

By distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, online retail, and others.

Supermarkets/hypermarkets dominated with USD 34.25 billion in 2025, supported by extensive shelf presence, price promotions, and high-volume purchasing behavior.

Online retail is the fastest-growing channel, registering a CAGR of 9.23% during the forecast period, driven by convenience, subscription models, and digital-first consumer engagement.

Energy Drinks Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Energy Drinks Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market and accounted for USD 27.38 billion in 2025 and is projected to grow at a CAGR of 7.77% during 2026–2034. The region benefits from strong brand loyalty, widespread adoption of sugar-free variants, and high consumption among young adults.

U.S. Energy Drinks Market

The U.S. dominated the region with a market size of USD 22.15 billion in 2025, driven by fitness culture, e-sports growth, and demand for functional beverages.

Europe

Europe reached USD 22.01 billion in 2025 and is projected to expand at a CAGR of 8.71% over the projected period. Market growth is supported by reformulation toward reduced-sugar products and increasing demand for natural caffeine sources.

U.K. Energy Drinks Market

The U.K. was valued at USD 5.19 billion in 2025, supported by high per-capita consumption despite increasing regulatory oversight.

Germany Energy Drinks Market

Germany reached USD 4.63 billion in 2025 and is projected to expand 9.76% CAGR during the forecast period. Germany represents one of the most mature and structurally stable ready-to-drink markets in Europe, characterized by high per-capita consumption, strong off-trade penetration, and growing demand for sugar-free and functional variants.

Asia Pacific

Asia Pacific was valued at USD 19.88 billion in 2025 and is the fastest-growing regional market, registering a CAGR of 9.13% during the projected period. Rapid urbanization, a large youth population, and Western lifestyle adoption are accelerating consumption.

China Energy Drinks Market

China was valued at USD 6.40 billion in 2025, driven by functional beverage penetration and strong domestic brand expansion.

India Energy Drinks Market

India reached USD 3.88 billion in 2025, growing at double-digit rates due to rising urban youth consumption and expanding sports culture.

South America and the Middle East & Africa

South America accounted for USD 5.01 billion in 2025, expanding at a CAGR of 6.59%. Energy drink consumption in South America is closely linked to sports culture, outdoor activities, and physically demanding occupations, particularly in Brazil, Argentina, and Chile.

The Middle East & Africa reached USD 2.89 billion in 2025, growing at a CAGR of 5.50%, supported by urban retail growth and tourism-driven consumption.

UAE Energy Drinks Market

The UAE was valued at USD 0.64 billion in 2025, growing at a CAGR of 5.99%, positioning it as the most advanced energy drinks market in the region. Demand is driven by luxury tourism, international events, and premium on-trade consumption.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players are Focused on Product Innovation and Distribution Expansion

The global energy drinks market is moderately concentrated, with leading companies leveraging strong brand equity, global sponsorships, and extensive distribution networks. Competitive strategies focus on sugar-free innovation, functional ingredient enhancement, and digital-first marketing.

Key Players in the Energy Drinks Market

|

Rank |

Company Name |

|

1 |

Red Bull GmbH |

|

2 |

Monster Beverage Corporation |

|

3 |

PepsiCo, Inc. |

|

4 |

The Coca-Cola Company |

|

5 |

Lucozade Ribena Suntory Ltd. |

List of Key Energy Drinks Companies Profiled in Report

- Red Bull GmbH (Austria)

- Monster Beverage Corporation (U.S.)

- PepsiCo, Inc. (U.S.)

- The Coca-Cola Company (U.S.)

- Rockstar Energy Drink (U.S.)

- Lucozade Ribena Suntory Ltd. (U.K.)

- Amway Corp. – XS Energy (U.S.)

- Osotspa PCL (Thailand)

- AJE Group – Volt Energy (Peru)

- Carabao Group PCL (Thailand)

KEY INDUSTRY DEVELOPMENTS

- November 2025: HELL Energy Drink secured a three-year partnership as the Official Energy Drink Partner for Punjab Kings, starting with IPL 2026. The deal features HELL Energy Drink's logo on the back of players' helmets and caps, plus visibility through matchday hydration stations and fan promotions.

- September 2025: 28 BLACK, a premium energy drink brand known for unique flavors and the slogan "The day has 28 hours”. The rollout targets late 2025, handled by exclusive importer Yinbev Beverages India Private Limited, with initial availability via www.28black.in and partnerships with retailers nationwide.

- September 2025: HELL Energy Drink launched its Black Cherry variant in India, as a premium energy drink targeting flavor-seeking consumers. This variant blends intense black cherry taste with the brand's original formula, including multiple B-vitamins and no added preservatives.

- August 2025: Celsius Holdings acquired PepsiCo's Rockstar Energy Drink brand in the U.S. and Canada as part of a strategic partnership expansion. PepsiCo invested USD 585 million in newly issued convertible preferred stock, boosting its ownership in Celsius to about 11% and gaining an extra board seat.

- May 2025: Sting Energy, a PepsiCo brand, became Formula 1's Official Energy Drink Partner. The partnership originated from a viral moment when DJ Armin van Buuren discovered that an F1 engine's roar sounded as "Sting."

REPORT COVERAGE

The global energy drinks market industry report analyzes the market in depth and highlights crucial aspects such as global market trends, supply chain, market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the research report also provides insights into the global market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.26% from 2026 to 2034 |

| Unit | Value (USD Billion |

|

Segmentation |

By Product Type

|

|

By Packaging Type

|

|

|

By Flavor

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was valued at USD 77.16 billion in 2025 and is anticipated to reach USD 157.21 billion by 2034.

At a CAGR of 8.26%, the global market will exhibit steady growth over the forecast period.

By distribution channel, the supermarkets/hypermarkets is the leading segment in the market.

North America held the largest market share in 2025.

Expansion of sports, fitness, and active lifestyle culture is accelerating energy drink consumption.

Red Bull GmbH, Monster Beverage Corporation, PepsiCo, Inc., The Coca-Cola Company, and Lucozade Ribena Suntory Ltd are the leading players in the global market.

Functional positioning and clean-label reformulation are shaping industry growth.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us