Feed Phosphates Market Size, Share & Industry Analysis, By Product Type (Monocalcium Phosphate (MCP), Dicalcium Phosphate (DCP), MDCP, and Others), By Form (Granular and Powder), By Livestock (Poultry, Swine, Ruminants, Aquaculture, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

Feed Phosphates Market Size and Future Outlook

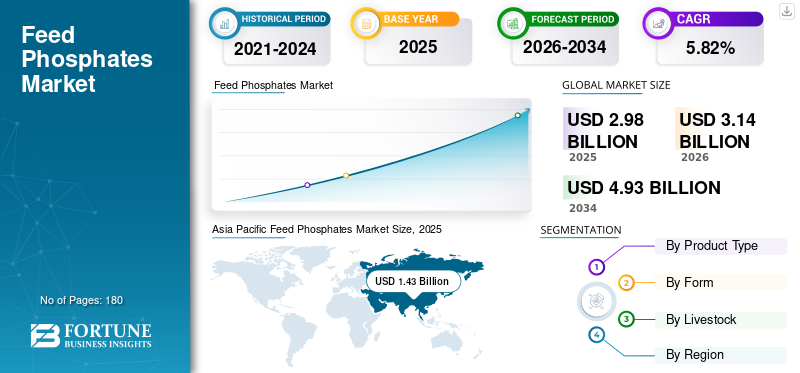

The global feed phosphates market size was valued at USD 2.98 billion in 2025. The market is projected to grow from USD 3.14 billion in 2026 to USD 4.93 billion by 2034, exhibiting a CAGR of 5.82% during the forecast period. Asia Pacific dominated the feed phosphates market with a market share of 47.99% in 2025.

Feed phosphates are mineral supplements, mainly monocalcium and dicalcium phosphate, that are added to animal feed to supply phosphorus and calcium in a form animal can use. These supplements help with bone development, growth, metabolism, and feed efficiency in livestock. They are especially important for poultry and pigs, where getting the right mineral balance is key for good results. Phosphate rock serves as the primary raw material for feed phosphates, with supply concentration and mining cost volatility significantly influencing global pricing and competitive dynamics.

Companies such as The Mosaic Company, Nutrien Ltd., OCP Group, and others are key players in this market. Mergers and acquisitions are a key strategy impacting the global market growth.

Download Free sample to learn more about this report.

FEED PHOSPHATES MARKET TRENDS

Environmental Regulations Promote Efficient Phosphorus Utilization Strategies

Changes in product forms are also worth noting. Feed mills are becoming more automated and consolidated, accelerating the shift from powder to granular phosphates, especially in industrialized areas. Granular forms flow more easily, produce less dust, and enable more accurate batching. These benefits meet today’s feed manufacturing standards.

Sustainability is becoming a bigger focus. Tougher environmental rules on phosphorus runoff are prompting producers to find ways to use nutrients more efficiently and reduce their environmental impact. Also, as phosphate rock supplies are concentrated and subject to geopolitical risks, companies are working to diversify their supply chains and integrate more steps in-house, thereby influencing the market trend.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Protein Consumption to Boost Feed Phosphate Demand

The global market is primarily growing due to increased poultry, swine, and aquaculture production, especially in Asia Pacific, South America, and parts of Africa. As people eat more protein, move to cities, and earn higher incomes, demand for industrial compound feed is rising. This also increases the use of inorganic phosphates. Poultry remains the main driver as it uses feed efficiently and requires more digestible phosphorus than other animals. Aquaculture is also becoming increasingly important, especially in Southeast Asia and Latin America. As fish and shrimp farming become more intensive, the need for balanced mineral nutrition increases. This is driving the feed phosphates market growth.

MARKET RESTRAINTS

Phytase Adoption Lowers Inclusion Rates and Limits Inorganic Phosphate Demand Growth

The market faces several ongoing challenges that could slow its long-term growth. A major challenge is that phytase enzymes are now widely used in animal health nutrition. Phytase helps animals digest phosphorus from plant-based feeds, which means there is less need for extra inorganic phosphates. As feed recipes become more precise, the use of monocalcium and dicalcium phosphate continues to decline. This limits growth in phosphate volumes, even if total feed production goes up. Environmental rules are another big challenge. As phosphorus runoff can cause water pollution, governments, especially in Europe and North America, have set stricter standards for managing nutrients. These rules aim for lower phosphorus levels in feed and greater use of systems that help animals better digest phosphorus. This directly reduces demand for inorganic phosphates. In some areas, following these rules also increases producers' costs.

MARKET OPPORTUNITIES

Rising Protein Demand and Aquaculture Intensification Increase Demand for Bioavailable Phosphates

The market offers several growth opportunities, especially in regions where the livestock sector is modernizing. A key opportunity comes from the growing demand for animal protein in Asia, Africa, and parts of the Middle East. As incomes rise and diets shift toward more poultry, eggs, dairy, and aquaculture products, commercial feed production is also growing. This transition from small-scale or subsistence farming to industrial feed systems increases the need for standardized mineral supplements, such as inorganic phosphates.

Segmentation Analysis

By Product Type

Higher Phosphorus Bioavailability Drives Preference for Monocalcium Phosphate (MCP)

By product type, the market is segmented into Monocalcium Phosphate (MCP), Dicalcium Phosphate (DCP), MDCP, and others.

The Monocalcium Phosphate (MCP) segment held the largest feed phosphates market share in 2025. Monocalcium Phosphate (MCP) is the top choice in the market as it provides more available phosphorus and better nutritional value than other inorganic phosphate sources. MCP typically provides more digestible phosphorus, allowing feed producers to meet nutrient goals with smaller quantities. As feed production now emphasizes digestible phosphorus rather than total phosphorus, MCP is suitable for precise nutrition. Its higher solubility helps poultry and swine absorb nutrients more effectively.

The Dicalcium Phosphate (DCP) segment holds the second-largest market share and is expected to grow at a CAGR of 6.07% during the forecast period. It offers a good balance between cost and performance, making it popular in markets where price matters most. Although DCP has lower phosphorus bioavailability than MCP, it is still a dependable and affordable mineral source, especially in areas where keeping feed costs low is important. Emerging markets in Asia, Latin America, and Africa still prefer DCP as it is affordable and easy to source through existing supply chains. Other products such as Tricalcium phosphate, represent a niche feed phosphate segment, primarily used in specific livestock and specialty applications due to its lower phosphorus bioavailability compared to MCP and DCP.

By Form

Granular Segment Led Market Due to Its Superior Flowability

Based on form, the market is segmented into granular and powder.

The granular segment accounted for the largest market share in 2025. Granular feed phosphates are the most popular product form. It forms flow better, are less likely to cake, and are easier to handle than powders. This makes them a good fit for automated batching systems in large commercial feed mills. Moreover, granular phosphates help prevent separation during transport and storage. This improves dosing accuracy and ensures nutrients are spread evenly in the finished feed.

The powder segment holds the second-largest share of the market and is expected to grow at a CAGR of 5.98% over the forecast period. Powdered feed phosphates are the second most common product form as they cost less to produce and are popular in markets where price matters most, and industries are less developed. In areas where feed mills are smaller or use only limited automation, powder is still common as handling efficiency is less important. Emerging markets in Africa, South Asia, and Latin America still use powder as it is affordable and fits their usual supply methods.

By Livestock

To know how our report can help streamline your business, Speak to Analyst

Poultry Segment Dominated Market as It is Fastest-growing Protein Source

By livestock, the market is segmented into poultry, swine, ruminants, aquaculture, and others.

The poultry segment led the global market in 2025. Poultry is the biggest consumer in the market since it is the most industrialized and fastest-growing protein source globally. Urbanization, population growth, and changing diets toward affordable animal protein have steadily increased demand for poultry meat and eggs. Poultry production has short cycles, efficient feed conversion, and integrated supply chains, all depending on carefully formulated compound feed. Poultry diets need exact amounts of digestible phosphorus for healthy bones, growth, and egg production, so inorganic phosphates such as monocalcium and dicalcium phosphate are essential.

Swine is another major segment that has a CAGR of 5.92% during the forecast period. It is widely produced worldwide and requires balanced mineral nutrition for healthy growth and reproduction. Swine diets need enough phosphorus to help with bone growth, weight gain, and metabolism, especially when the animals are young. Although swine production is not as widespread as poultry and can be affected by diseases such as African Swine Fever, it is still highly industrialized in key areas such as China, the U.S., and parts of Europe.

Feed Phosphates Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Feed Phosphates Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market was valued at USD 1.43 billion in 2025 and is the leading region in the world. Asia Pacific leads as the largest and fastest-growing market, driven by growth in poultry, swine, and aquaculture production. China, India, and Southeast Asia are major demand centers as people are eating more protein, and feed production is becoming more industrialized.

Although more producers are using phytase, demand for inorganic phosphate remains high, as the region has a large base of compound feed. Growth in aquaculture also increases the need for mineral supplements. The market is diverse, with varying levels of automation and cost sensitivity.

India Feed Phosphates Market

The India market in 2025 was valued at around USD 0.09 billion, accounting for roughly 2.91% of global market revenues. India’s market is growing steadily, driven by the rapid expansion of the poultry sector and increased activity in aquaculture. Higher demand for protein and more industrialized feed production are boosting the market, but buyers remain highly cost-sensitive.

China Feed Phosphates Market

China’s market in 2025 was valued at around USD 0.51 billion, representing roughly 17.09% of the global market share. China leads the world in feed phosphates, thanks to its large poultry and swine industries and a strong aquaculture sector. The swine industry’s recovery and ongoing feed industrialization keep demand steady. Although using phytase reduces the amount of phosphate added to feed, total consumption remains high due to the industry’s size. Local phosphate production also affects regional prices.

Japan Feed Phosphates Market

The Japan market in 2025 reached a valuation of around USD 0.06 billion, accounting for roughly 1.92% of global market revenues. Japan has a well-developed and stable market, shaped by its advanced industry and strict quality requirements. Most of the demand comes from the country’s established poultry and swine industries.

North America

The market in North America reached a valuation of USD 0.66 billion in 2025. The North American market is well-established and highly developed, mainly due to large-scale poultry and swine farming. The U.S. leads the region in demand, due to its large compound feed production and integrated livestock industry. Widespread use of phytase has reduced the need for inorganic phosphate, thereby limiting overall growth in volume. Market growth is steady but modest, largely driven by trends in protein consumption and poultry and pork exports.

U.S. Feed Phosphates Market

In 2025, the U.S. market reached USD 0.53 billion. The U.S. market is well-established and values efficiency, largely due to its large poultry and swine industries. Automation in feed mills and the use of phytase have helped lower the need for inorganic phosphate. Demand remains steady but is not growing fast. It is mainly driven by protein exports and domestic consumption trends.

Europe

The European market reached a valuation of USD 0.49 billion in 2025. Europe has a well-developed market that focuses on efficiency. Strict environmental rules and advanced feed formulation are key features. Widespread use of phytase has greatly lowered the need for inorganic phosphate. As a result, market growth now depends more on feed production than on the amount of nutrients added. Poultry and swine remain the main users of feed phosphates, but in some countries, ruminants also account for a significant share of demand.

Germany Feed Phosphates Market

The market in Germany in 2025 reached around USD 0.04 billion, representing roughly 1.51% of global market revenues.

U.K. Feed Phosphates Market

The U.K. market reached approximately USD 0.04 billion in 2025, equivalent to around 1.24% of global market sales.

South America and Middle East & Africa

Over the forecast period, South America is expected to experience significant growth in this market. The South America market in 2025 recorded USD 0.22 billion. South America is a medium-sized market with strategic importance, mainly due to Brazil’s poultry and swine export industries. The region’s growing protein production and solid agricultural infrastructure are key advantages. The Middle East & Africa region reached a valuation of USD 0.17 billion in 2025. The Middle East & Africa market is smaller but growing steadily. Most of this growth comes from the poultry sector and the rise of commercial feed production. Countries in the Middle East, especially those in the Gulf and Turkey, use more industrialized feed systems. In contrast, many areas of Africa still have fragmented markets and are more price-sensitive. A growing population and new food security programs are driving the expansion of the compound feed market. But the market’s overall size is limited as there are fewer industrial operations and a greater dependence on imports.

UAE Feed Phosphates Market

The UAE market is set to grow at a CAGR of 3.52% during the forecast period. The UAE’s market is smaller but industrial, mainly driven by poultry production and efforts to improve food security. Heavy reliance on imports and automated feed systems favors granular, high-quality feed. Modernizing livestock production is helping drive demand, but the market is still smaller than in other regional countries.

COMPETITIVE LANDSCAPE

Key Industry Players

Feed Industry Consolidation Favors Large-Scale Phosphate Suppliers

The feed phosphates market is fairly consolidated, shaped by who owns phosphate rock resources and how the feed industry is integrated. Global competition is led by vertically integrated producers such as OCP Group, Mosaic, Nutrien, and EuroChem, which benefit from direct access to phosphate rock reserves and large-scale processing capabilities. These companies use cost advantages, global distribution, and long-term supply contracts to stay competitive. In addition to the large integrated companies, specialized producers such as Phosphea and Ecophos compete by focusing on product quality, technical support, and reaching regional markets.

LIST OF FEED PHOSPHATE COMPANIES PROFILED IN REPORT

- The Mosaic Company (U.S.)

- Nutrien Ltd. (Canada)

- OCP Group (Morocco)

- Phosphea (Groupe Roullier) (France)

- Yara International (Norway)

- EuroChem Group (Switzerland)

- Ecophos (Belgium)

- Fosfitalia Group (Italy)

- Quimpac S.A. (Peru)

- R. Simplot Company (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: The Global Feed team signed a new agreement with a logistics partner in Elbląg. With this partnership, Global Feed will operate a new warehouse capable of holding over 4,000 tons. This facility will supply feed phosphates to the Polish market and nearby countries.

- October 2025: Paradeep Phosphates Ltd announced its merger with Mangalore Chemicals & Fertilizers Ltd (MCFL). This merger has helped the company expand its presence in southern India and has added to its established markets in the north, west, central, and eastern regions.

- February 2025: OCP Group, a global leader in phosphate-based plant and animal nutrition, and Fertinagro Biotech S.L, a leading Spanish fertilizer producer, announced that OCP Group has acquired another 25% of GlobalFeed S.L. This brings OCP Group’s total ownership to 75%.

- April 2024: Solevo partnered with Phosphea, a global leader in animal feed solutions. Together, they launched a partnership to improve animal nutrition across Africa. This partnership brought together Solevo’s wide distribution network and Phosphea’s innovative products, including Monocalcium Phosphate (MCP), Monodicalcium Phosphate (MDCP), Dicalcium Phosphate (DCP), and special nutritional formulas containing macro-minerals.

- June 2021: OCP Group, the world's largest phosphate mining and leading global fertilizer group, and IFC signed a USD 100 million financing agreement. This partnership supported OCP in expanding its value chain in Africa.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.82% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, By Form, By Livestock, and Region |

| By Product Type |

|

| By Form |

|

| By Livestock |

|

| By Region |

North America (By Product Type, By Form, By Livestock, and Country)

Europe (By Product Type, By Form, By Livestock, and Country)

Asia Pacific (By Product Type, By Form, By Livestock, and Country)

South America (By Product Type, By Form, By Livestock, and Country)

Middle East & Africa (By Product Type, By Form, By Livestock, and Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.98 billion in 2025 and is projected to reach USD 4.93 billion by 2034.

In 2025, the Asia Pacifics market value stood at USD 1.43 billion.

The market is expected to exhibit a CAGR of 5.82% during the forecast period.

By product type, the Monocalcium Phosphate (MCP) segment led the market in 2025.

Rising protein consumption to boost feed phosphate demand.

The Mosaic Company, Nutrien Ltd., and OCP Group are key players in the market.

Asia Pacific held the largest market share in 2025.

Environmental regulations promote efficient phosphorus utilization strategies, which is the key market trend.

- 2021-2034

- 2025

- 2021-2024

- 180

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us