Fetal Monitoring Market Size, Share & Industry Analysis, By Method (Invasive and Non-Invasive), By Product (Instrument {Ultrasound Fetal Monitors, Electronic Fetal Monitors (EFM), Fetal Dopplers, and Others}, and Consumables {Electrodes, Ultrasound Gel & Couplants, Disposable Sensors, and Others}), By Application (Antepartum Monitoring and Intrapartum Monitoring), By End-User (Hospitals, Home Care Settings, Diagnostic & Imaging Centers, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

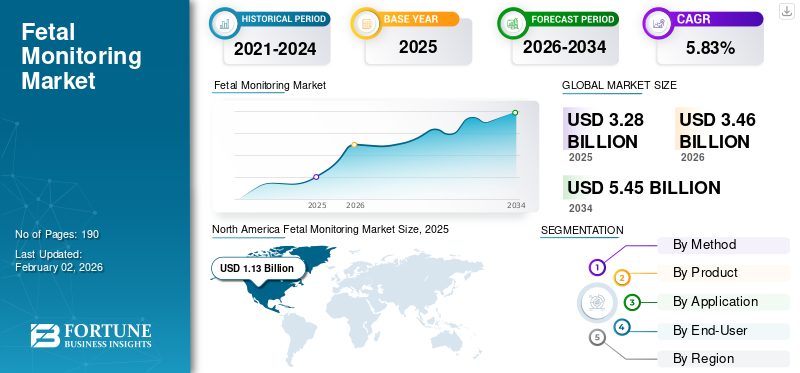

The global fetal monitoring market size was valued at USD 3.28 billion in 2025. The market is projected to grow from USD 3.46 billion in 2026 to USD 5.45 billion by 2034, exhibiting a CAGR of 5.83% during the forecast period. North America dominated the fetal monitoring market with a market share of 34.48% in 2025.

Fetal monitoring devices are used to assess fetal heart rate, fetal movement, uterine contractions, and overall fetal well-being during pregnancy, labor, and delivery. These systems are widely used in hospitals, maternity clinics, and high-risk pregnancy settings to detect fetal distress, guide obstetric decisions, and reduce the risk of adverse birth outcomes. Market growth is driven by the increasing rate of high-risk pregnancies, rising maternal age, growing rate of C-sections, and the demand for continuous real-time monitoring during labor. Adoption of portable, wireless, and non-invasive monitoring solutions is further supporting market expansion.

Major players in this market include Philips Healthcare, GE HealthCare, Mindray Medical, Huntleigh Healthcare (Arjo), and Monica Healthcare. These companies focus on advanced cardiotocography (CTG) platforms, wireless patch-based fetal monitors, and data connectivity features that enable remote surveillance of fetal status. Strong product portfolios, ongoing clinical validation, and seamless integration into labor and delivery workflows enable these players to maintain a dominant position in the global market.

Download Free sample to learn more about this report.

Fetal Monitoring MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 3.28 billion

- 2026 Market Size: USD 3.46 billion

- 2034 Forecast Market Size: USD 5.45 billion

- CAGR: 5.83% from 2026–2034

- North America dominated the fetal monitoring market with a 34.48% share in 2025.

- Non-invasive segment led the market with 67.77% share in 2026.

- Consumables segment dominated with 64.84% share in 2026.

North American

North America held USD 1.13 billion in 2025, accounting for 34.48% share, and is projected to reach USD 1.19 billion in 2026.

Europe

Europe held USD 0.91 billion in 2025, accounting for 27.82% share, and is projected to reach USD 0.95 billion in 2026.

Asia Pacific

Asia Pacific reached USD 0.99 billion in 2025, accounting for 30.06% share, and is projected to reach USD 1.05 billion in 2026.

U.S.

Estimated to reach USD 1.12 billion by 2026, driven by high-risk pregnancy monitoring demand and advanced fetal care adoption.

Japan

Strong hospital-driven adoption supported by advanced maternal healthcare infrastructure and routine prenatal monitoring systems.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Rate of High-Risk Pregnancies to Support Market Growth

Increasing maternal age, higher prevalence of gestational diabetes, hypertension, and preeclampsia, and higher incidence of multiple pregnancies (twins, IVF-related pregnancies) are all contributing to a larger pool of high-risk pregnancies. High-risk pregnancies are monitored more frequently, often with continuous fetal heart rate and uterine activity tracking to identify fetal distress early. Hospitals and maternity centers are standardizing fetal monitoring during labor to guide timely intervention and avoid birth-related complications. This clinical requirement directly drives demand for CTG monitors, transducers, and telemetry-enabled monitoring systems, which will thereby expected to have a positive impact on the global fetal monitoring market growth.

- For instance, according to data published by the Cleaveland Clinic, an estimated 6.0% to 8.0% pregnancies in the U.S. are high-risk pregnancies per year.

MARKET RESTRAINTS

Regulatory and Accuracy Concerns in Non-Invasive Continuous Monitoring to Hamper Market Growth

Non-invasive and wearable devices are gaining attention. Still, they face regulatory scrutiny around signal accuracy, signal loss due to maternal BMI, and correct differentiation between maternal and fetal heart rates. False alarms and ambiguous traces can trigger unnecessary interventions such as unplanned C-sections or assisted delivery. In addition, the cost of advanced CTG and telemetry systems can be high for smaller maternity centers, especially in low- and middle-income regions, which slows broad installation.

MARKET OPPORTUNITIES

Integration of AI and Decision-Support Analytics to Offer Growth Opportunities

There is a growing opportunity in software that can interpret fetal heart rate variability patterns and contraction trends to predict fetal distress earlier and reduce adverse birth outcomes. AI-driven interpretation tools aim to reduce subjectivity and inter-clinician variability in CTG reading, assist obstetricians in making escalation decisions, and document trace quality for compliance purposes. In parallel, connectivity and cloud-based data sharing enable remote obstetric review in near real-time. Vendors that combine hardware (fetal monitor), wireless sensors (belts/patches), and analytics (decision support) are positioned to capture higher-value contracts from hospitals and maternal-fetal medicine practices.

MARKET CHALLENGES

False Alarms and Clinical Liability to Pose Challenges

One of the major challenges in fetal monitoring is overinterpretation of fetal heart rate tracings. Continuous CTG is known for generating frequent “non-reassuring” readings that are sometimes not clinically significant. This can lead to defensive decision-making and higher C-section rates. Hospitals are under pressure to balance safety and intervention: they must catch true fetal distress, but also avoid unnecessary surgical delivery. Another challenge is signal quality in patients with higher BMI or during active movement, which can lead to dropped signals and confusion between maternal and fetal heart rates. Consistent training, validated algorithms, and improved sensor design are still needed to address these issues.

Fetal Monitoring Market Trends

Shift Toward Non-Invasive, Continuous, and Maternal-Friendly Monitoring is a Key Trend

A clear trend in the market is the shift away from fully tethered bedside monitors toward wireless, beltless, or patch-based fetal monitoring systems that prioritize maternal mobility and enhance the patient experience during labor and delivery. Traditional external monitoring relies on ultrasound transducers and tocodynamometers, which are secured by belts around the abdomen. Newer systems utilize wireless sensors and telemetry modules that transmit fetal heart rate and uterine activity data to a central station, enabling patients to ambulate instead of being confined to a bed. This supports lower-intervention birthing approaches and is being promoted in midwifery-led units and progressive labor & delivery centers.

- For instance, in February 2024, GE HealthCare received U.S. FDA 510(k) clearance for the Novii+ Wireless Maternal and Fetal Monitoring Solution. The updated wireless patch can be used in both antepartum and intrapartum monitoring, starting at 34 weeks of pregnancy, and is designed to allow the mother to move freely during labor.

Download Free sample to learn more about this report.

Segmentation Analysis

By Method

Rising Emphasis on Non-Invasive Methods Due to Superior Safety Boosted Segment Growth

On the basis of the method, the market is classified into invasive and non-invasive.

The non-invasive segment held the highest global fetal monitoring market share in 2024 due to its safety, comfort, and ease of use during pregnancy and labor. It includes Doppler ultrasound and external cardiotocography (CTG), which provide accurate data on fetal heart rate and uterine contractions without the need for internal sensors. Moreover, the non-invasive method is widely preferred in hospitals, clinics, and home monitoring due to its reduced risk of infection and maternal discomfort. The non-invasive segment is expected to account for 67.77% of the market in 2026.

- For instance, in January 2024, Bloomlife announced FDA clearance for its Bloomlife MFM-Pro device. This wearable maternal–fetal monitoring system measures both maternal and fetal heart rate and supports remote/high-risk pregnancy monitoring.

The invasive method segment is expected to rise at a CAGR of 4.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Product

Strict Regulations for Fetal Screening Boosted Adoption of Consumables

In terms of product, the market is categorized into instrument and consumables.

The consumables segment captured the largest market share in 2024. In 2025, the segment dominates with a 62.3% share. Consumables dominate the market, owing to their high replacement frequency and continuous usage across hospitals and clinics. These include ultrasound transducers, probes, electrode belts, sensors, paper charts, gel, and disposable accessories required for every monitoring session. Consumables are critical for accurate fetal heart rate and uterine contraction readings, ensuring hygiene and optimal signal quality. The consumables segment is poised to account for 64.84% of the market share in 2026.

The instrument segment is expected to rise at a CAGR of 5.1% over the forecast period.

By Application

High Focus on Prevention of Pre-Birth Complications Accelerated Intrapartum Monitoring Segment Growth

In terms of application, the market is categorized into antepartum monitoring and intrapartum monitoring.

The intrapartum monitoring captured the largest share of the market in 2024. In 2025, the segment dominates with a 54.3% share. Intrapartum monitoring represents the largest application segment, as continuous monitoring during labor and delivery is critical for detecting fetal distress, cord compression, or uterine hyperstimulation. It guides timely clinical decisions, reducing neonatal morbidity and mortality. Moreover, rising C-section rates and the global emphasis on preventing birth-related complications have reinforced the importance of fetal monitoring during labor, cementing this segment’s dominance. The intrapartum monitoring segment is forecast to represent 53.99% of total market share in 2026.

The antepartum monitoring segment is expected to rise at a CAGR of 6.3% over the forecast period.

By End User

High Volume of Patient Visits to Hospitals Accelerated Segment Growth

Based on end-user, the market is segmented into hospitals, home care settings, diagnostic & imaging centers, and others.

In 2024, the hospitals segment dominated the global market. Hospitals handle both routine and high-risk pregnancies, requiring advanced fetal monitoring instruments for continuous, multi-patient surveillance. Hospitals also have higher budgets for integrated monitoring networks, central station displays, and electronic record systems that consolidate maternal and fetal data. The hospitals segment is expected to account for 75.76% of the market in 2026.

In addition, the home care settings segment is projected to rise at a CAGR of 6.6% during the study period.

Fetal Monitoring Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Fetal Monitoring Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market was valued at USD 1.13 billion in 2025, capturing 34.48% of global revenue, and is estimated to reach USD 1.19 billion in 2026. The factors fostering the dominance of the region include considerable technological advancements and product approvals. The U.S. market is estimated to reach USD 1.12 billion in 2026, attributed to growing awareness about high-risk pregnancies, adoption of technologically advanced monitoring devices, and strict implementation of pregnancy care guidelines.

- For instance, in November 2022, EXSALTA received FDA approval for its new peristaltic pump.

Europe

In 2025, Europe held 27.82% of the global market, reaching a valuation of USD 0.91 billion, and is projected to grow to USD 0.95 billion in 2026. Europe is projected to witness notable growth in the coming years. Europe is projected to record a growth rate of 4.7% during the forecast period and reach a valuation of USD 0.95 billion by 2026. This is primarily due to the emphasis on pre-birth care, spreading awareness about fetal monitoring, and a focus on infection prevention. Backed by these factors, countries including U.K., Germany, and France are anticipated to record the valuation of USD 0.15 billion, USD 0.21 billion in 2026. France is aniticipated to record the valuation of USD 0.12 billion, respectively, in 2025.

Asia Pacific

The market in Asia Pacific reached USD 0.99 billion in 2025, representing 30.06% of total market revenue, and is projected to reach USD 1.05 billion in 2026. Asia Pacific is expected to exhibit the fastest CAGR during the forecast period. The market in Asia Pacific is estimated to reach USD 1.05 billion in 2026. In the region, India and China are estimated to reach USD 0.23 billion and USD 0.35 billion, respectively in 2026.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space over the forecast period. Latin America maintained a strong presence in the global market, reaching USD 0.11 billion in 2025, accounting for 3.36% share, and is expected to reach USD 0.11 billion in 2026. The consolidation of healthcare infrastructure, coupled with extensive investments in superior healthcare facilities, is further estimated to drive regional growth during the forecast period. In 2025, the Middle East & Africa market stood at USD 0.14 billion, representing 4.29% of global demand, and is projected to grow to USD 0.15 billion in 2026. In the Middle East & Africa, the GCC is set to reach a value of USD 0.04 billion by 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Clinical Accuracy, Connectivity, and Maternal Comfort to Help Companies Maintain Their Market Positions

The global market exhibits a moderately consolidated structure, comprising a few large multinational companies and several specialized maternal-fetal monitoring players that focus on high-risk pregnancy care, labor and delivery, and remote monitoring. Market participants consistently focus on clinical accuracy, wireless connectivity, maternal comfort during labor, and regulatory compliance to defend or expand their position.

Philips Healthcare, GE HealthCare, Mindray Medical, and Huntleigh Healthcare (Arjo) are among the leading players in the market. These companies benefit from broad fetal and maternal monitoring portfolios, strong penetration in hospital labor & delivery units, and established central surveillance systems. Their product strategies include continuous cardiotocography (CTG), telemetry-based fetal monitoring, integrated maternal–fetal vital monitoring, and remote viewing/alerting capabilities.

In addition to these companies, other notable participants include Monica Healthcare, EDAN Instruments, Bionet, and emerging digital maternal-fetal companies such as Bloomlife. These players are focusing on targeted strategies such as wearable fetal heart rate patches for ambulatory monitoring, AI-assisted interpretation of fetal heart rate variability and uterine activity, and remote monitoring programs for high-risk pregnancies.

LIST OF KEY FETAL MONITORING COMPANIES PROFILED

- GE HealthCare Technologies Inc. (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Mindray Medical International Ltd. (China)

- Nihon Kohden Corporation (Japan)

- Analogic Corporation (U.S.)

- Huntleigh Healthcare Limited (U.K.)

- Bionet Co., Ltd. (South Korea)

- Edan Instruments, Inc. (China)

- Spacelabs Healthcare (U.S.)

- Drägerwerk AG & Co. KGaA (Germany)

KEY INDUSTRY DEVELOPMENTS

- February 2025: Huntleigh Healthcare received U.S. FDA 510(k) clearance (K241368) for the Sonicaid Team3 fetal/maternal monitor.

- November 2024: Bloomlife raised USD 12.2 million to scale its maternal–fetal monitoring platform after FDA clearance of MFM-Pro, and to expand remote monitoring services for high-risk pregnancies.

- June 2024: Clarius Mobile Health announced FDA clearance for its OB AI feature on its handheld wireless ultrasound.

- March 2024: Bloomlife and Valley Perinatal Services announced a partnership to support high-risk maternal care through remote fetal/maternal monitoring, as well as clinical alerts, aiming to intervene earlier in hypertensive and diabetic pregnancies.

- June 2020: Philips launched its Avalon CL Fetal & Maternal Pod and Patch as part of a cableless obstetric monitoring solution.

REPORT COVERAGE

The global market analysis provides an in-depth examination of market size and forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.83% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Method

By Product

By Application

By End-User

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.28 billion in 2025 and is projected to reach USD 5.45 billion by 2034.

In 2025, the market value stood at USD 1.13 billion.

The market is expected to exhibit a CAGR of 5.83% during the forecast period of 2026-2034.

In 2025, the consumables segment led the market by product type.

The key factors driving the market are the increasing incidence of high-risk pregnancies and advancements in technology.

Philips Healthcare, GE HealthCare, Mindray Medical, and Huntleigh Healthcare (Arjo) are some of the prominent players in the market.

North America dominated the market with a share of 34.48% in 2025.

Growing awareness and rising demand for prenatal care are expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us