Fighter Jet Market Size, Share & Industry Analysis, By Platform Class (Light Fighter, Medium Fighter, and Heavy Fighter), By Propulsion (Single Engine and Twin Engine), By Type (Light Attack, Electronic Warfare, Multirole Fighter, Trainer, and Others), By Take-off and Landing (Conventional Take-off and Landing, Short Take-off and Landing, and Vertical Take-off and Landing), and Regional Forecast, 2026-2034

Fighter Jet Market Size and Future Outlook

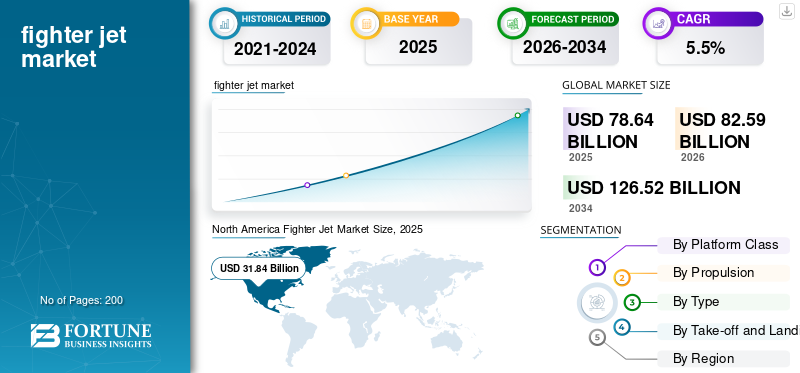

The global fighter jet market size was valued at USD 78.64 billion in 2025. The market is projected to grow from USD 82.59 billion in 2026 to USD 126.52 billion by 2034, exhibiting a CAGR of 5.5% during the forecast period.

The global market represents a critical segment of the aerospace and defense industry, driven by the continuous need of nations to modernize their air combat capabilities and maintain strategic air superiority. Governments worldwide are investing in next-generation aircraft platforms featuring advanced avionics, stealth technologies, supersonic speeds, and precision-guided munitions systems. Geopolitical tensions, evolving threat landscapes, and rising defense budgets are collectively shaping procurement decisions across established air forces and emerging military powers. The market encompasses a broad spectrum of aircraft types, including multirole fighters, air superiority jets, and ground-attack platforms developed through domestic programs as well as international partnerships and export agreements.

Key players in the market include Lockheed Martin Corporation, The Boeing Company, Dassault Aviation SA, Saab AB, BAE Systems plc, Airbus SE, Leonardo S.p.A., United Aircraft Corporation, Aviation Industry Corporation of China (AVIC), and Hindustan Aeronautics Limited (HAL). These companies compete through advanced stealth and avionics integration, expanded multirole combat capabilities, superior thrust-to-weight performance, next-generation radar and sensor fusion systems, and tailored defense partnership models designed for air superiority, strike missions, close air support, and strategic deterrence across domestic and allied defense markets.

Download Free sample to learn more about this report.

FIGHTER JET MARKET TRENDS

Advancing Stealth, Sensor Fusion, and Digital Warfare Capabilities to Redefine Modern Fighter Jet Development

A dominant trend reshaping the market is the rapid integration of stealth architecture, active electronically scanned array (AESA) radars, and artificial intelligence-driven sensor fusion within next-generation platforms. Air forces globally are prioritizing aircraft that can operate in contested electromagnetic environments, execute beyond-visual-range engagements, and network seamlessly within joint combat ecosystems. The rise of sixth-generation fighter programs, unmanned loyal wingman concepts, and directed-energy weapon compatibility reflects a fundamental shift toward digitally connected, multi-domain combat aircraft that extend lethality while reducing pilot cognitive burden and increasing mission survivability.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Geopolitical Tensions and Defense Modernization Mandates to Fuel Product Procurement

Escalating geopolitical rivalries, territorial disputes, and the resurgence of great-power competition are driving nations to accelerate investment in advanced air combat capabilities, propelling fighter jet market growth. Governments are increasing defense budgets with a specific focus on replacing obsolete platforms and achieving technological parity or superiority over potential adversaries. NATO member commitments, Indo-Pacific security dynamics, and Middle Eastern power balances are driving sustained procurement cycles. Additionally, the demonstrated effectiveness of precision air power in modern conflicts reinforces the institutional demand for fighters capable of integrating advanced munitions, electronic warfare systems, and real-time battlefield intelligence within joint and coalition operational frameworks.

MARKET RESTRAINTS

Prohibitive Development and Lifecycle Costs May Hamper Jet Acquisition Decisions

The exceptionally high costs associated with designing, developing, producing, and sustaining advanced fighter aircraft represent a fundamental restraint on market expansion. Fifth-generation platforms demand substantial investment in unit procurement and across decades of maintenance, upgrades, pilot training, and supply chain support. Smaller defense budgets among developing nations limit their ability to commit to premium platforms, often deferring modernization timelines or pursuing lower-tier alternatives. Budget overruns and schedule delays in major fighter programs further erode acquisition confidence, prompting governments to reassess procurement quantities or extend the service life of existing fleets rather than proceeding with new aircraft contracts.

MARKET OPPORTUNITIES

Fleet Modernization Programs and Indigenous Defense Manufacturing Initiatives to Open New Growth Frontiers

Significant market opportunities are emerging from large-scale fleet replacement programs and the growing governmental willingness to develop indigenous fighter capabilities. Countries across Asia, the Middle East, and Eastern Europe are accelerating procurement decisions to replace aging Soviet-era and legacy Western platforms with technologically superior aircraft. Parallel investments in domestic aerospace industrial bases through programs such as India's TEJAS Mk-II and Turkey's KAAN are broadening the competitive landscape. Export markets for proven multirole platforms remain highly lucrative, with allied nations seeking interoperability, technology transfer agreements, and long-term sustainment partnerships as strategic incentives.

MARKET CHALLENGES

Complex Export Regulations and Geopolitical Alignments May Impede Cross-Border Fighter Transactions

Fighter jet manufacturers face substantial challenges navigating the geopolitical sensitivities, export control regimes, and end-user certification requirements that govern international defense transactions. Regulatory frameworks such as the U.S. International Traffic in Arms Regulations impose stringent controls on technology transfer, limiting the market access for prospective buyers and creating competitive disadvantages for Western manufacturers against rivals with fewer restrictions. Additionally, shifting diplomatic alliances, sanctions regimes, and parliamentary approval processes introduce significant uncertainty into procurement timelines. The growing preference for offset agreements and co-production mandates further complicates contract negotiations, demanding greater industrial commitment from exporters and increasing program execution risk.

Segmentation Analysis

By Platform Class

Widening Capability Gaps and Budget-Constrained Modernization to Accelerate Medium Fighter Segment Growth

Based on platform class, the market is segmented into light fighter, medium fighter, and heavy fighter.

The medium fighter segment accounted for the largest market share in 2025. The product demand is rising as defense establishments seek cost-effective platforms that balance operational capability with affordability. Nations with constrained procurement budgets increasingly favor medium fighters offering multirole versatility, reduced logistical footprints, and competitive lifecycle costs, making this platform class central to fleet modernization strategies worldwide.

The heavy fighter segment is anticipated to rise at a CAGR of 5.4% over the forecast period.

By Propulsion

Twin Engine Segment Led the Market driven by their Enhanced Payload Capacity and Thrust Redundancy

Based on propulsion, the market is segmented into single engine and twin engine.

In 2025, the twin engine segment dominated the global fighter jet market share. These fighter aircraft are experiencing a heightened demand due to their superior thrust redundancy, extended range, and enhanced payload capacity critical for high-intensity air operations. Air forces operating in contested, long-endurance maritime, or expeditionary environments consistently prefer twin-engine configurations, reinforcing procurement interest across advanced military programs globally.

The single engine segment is projected to grow at a CAGR of 5.6% over the forecast period.

By Type

Need for Mission Flexibility to Propel the Multirole Fighter Segment Growth

Based on type, the market is segmented into light attack, electronic warfare, multirole fighter, trainer, and others.

The multirole fighter segment is anticipated to witness a dominating market share over the forecast period. These fighters dominate procurement priorities as air forces seek single platforms capable of executing air superiority, ground attack, electronic warfare, and reconnaissance missions. The versatility of multirole aircraft maximizes operational return on investment, enabling smaller air forces to maintain comprehensive combat capability while consolidating fleet complexity and sustainment requirements.

The electronic warfare management segment is projected to grow at a high CAGR of 7.6% over the forecast period.

By Take-off and Landing

To know how our report can help streamline your business, Speak to Analyst

Established Airfield Infrastructure and Operational Simplicity to Support the Conventional Take-Off and Landing Segment Growth

Based on take-off and landing, the market is segmented into conventional take-off and landing, short take-off and landing, and vertical take-off and landing.

The conventional take-off and landing segment dominated the market share in 2025.This dominance is underpinned by existing airfield infrastructure, lower operational complexity, and broader pilot proficiency. Most air forces operating from established land bases continue to specify CTOL configurations, ensuring that this segment retains the largest share of fighter acquisition programs worldwide.

In addition, the vertical take-off and landing segment is projected to grow at a CAGR of 6.0% during the analysis period.

Fighter Jet Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Fighter Jet Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 29.99 billion, and also maintained the leading share in 2025, with a value of USD 31.84 billion. North America leads the global market driven by sustained U.S. defense investment in advanced fifth-generation platforms, allied interoperability programs, and continuous modernization of existing fleets to address evolving strategic threats.

U.S. Fighter Jet Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 31.69 billion in 2026. The market is poised to depict a CAGR of roughly 5.0% during the forecast period. The U.S. drives the global demand through sustained F-35 procurement, next-generation air dominance investments, and extensive allied foreign military sales supporting interoperability across NATO and Indo-Pacific partner nations.

Europe

The Europe market is estimated to reach USD 20.13 billion in 2026 and secure the position of third largest region in the market. The product demand in Europe is rising sharply amid NATO spending commitments, fleet replacement needs, and the urgency created by regional security shifts, with nations investing heavily in domestic platforms and allied procurement programs.

U.K. Fighter Jet Market

The U.K. market is estimated to reach a value of around USD 2.74 billion in 2026 and exhibit a CAGR of roughly 5.1% over the forecast period. The U.K. is investing significantly in fighter modernization through its F-35B fleet expansion and active participation in the sixth-generation Tempest program, reinforcing its commitment to maintaining frontline air combat superiority.

Germany Fighter Jet Market

The Germany market is projected to reach approximately USD 3.77 billion in 2026. The Germany market is evolving through Eurofighter typhoon fleet upgrades and its commitment to the Future Combat Air System program, reflecting broader NATO obligations and national defense reinvestment priorities.

Asia Pacific

The Asia Pacific market is projected reach a valuation of USD 21.73 billion by 2026 and record a CAGR of 5.3% during the forecast period. This regional market is expanding at a moderate pace, propelled by escalating territorial tensions, expanding defense budgets, and ambitious indigenous fighter development programs across China, India, Japan, South Korea, and Australia.

China Fighter Jet Market

The China market is projected to be one of the largest markets in Asia Pacific, with 2026 revenues estimated to reach around USD 8.41 billion. China is rapidly expanding its fighter capabilities through indigenous fifth-generation J-20 production and advanced J-35 naval platform development, underpinned by ambitious military modernization goals and growing regional power projection ambitions.

Japan Fighter Jet Market

The Japan market value is estimated to touch around USD 3.06 billion in 2026. The market in this country is poised to depict a CAGR of 4.3% during the forecast period. Japan is accelerating fighter aircraft investment through F-35 fleet expansion and its domestically led F-X next-generation fighter program, driven by evolving regional threats and strengthened defense alliance commitments with the U.S.

India Fighter Jet Market

The India market is estimated to reach a value of around USD 4.25 billion in 2026. This market is expanding on account of Rafale acquisitions, Tejas Mk-II development, and ongoing fleet modernization under its Atmanirbhar Bharat initiative, which positions the country as a growing indigenous aerospace manufacturing powerhouse.

Rest of the World

The rest of the world includes the Middle East and Africa and Latin America. These regions are expected to witness moderate growth during the forecast period. The Middle East & Africa and Latin America markets are set to reach USD 5.52 billion and USD 1.89 billion, respectively, in 2026. The rest of the world market is witnessing growing fighter aircraft procurement activity, particularly across the Middle East and Latin America, where nations are upgrading aging fleets amid regional security dynamics and diversified defense partnerships.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Focus on Stealth Production Scale-Up and Fleet Modernization to Bolster their Market Positions

The fighter jet market landscape is being strengthened by key players that are depicting a shift from standalone aircraft sales toward long-term combat-air ecosystems built around stealth, sensor fusion, open mission systems, advanced weapons integration, electronic warfare, and lifecycle modernization. Companies such as Lockheed Martin, Boeing, Dassault Aviation, Saab, BAE Systems, Airbus, Leonardo, UAC, AVIC, and Hindustan Aeronautics Limited are focusing on production ramp-ups, export campaigns, local assembly, mission-system upgrades, and next-generation fighter development to secure recurring defense revenues. Lockheed Martin’s F-35 program remains the strongest demand anchor, with the company reporting 191 F-35 deliveries in 2025, showing the scale advantage of fifth-generation fighter production. Boeing is positioning the F-15EX around payload, range, open architecture, electronic warfare, and future collaborative combat aircraft integration, while Dassault is using Rafale export momentum to deepen its backlog, supported by 21 Rafale deliveries in 2024 and continuing international orders.

LIST OF KEY FIGHTER JET COMPANIES PROFILED

- Lockheed Martin Corporation (U.S.)

- The Boeing Company (U.S.)

- Dassault Aviation SA (France)

- Saab AB (Sweden)

- BAE Systems plc (U.K.)

- Airbus SE (Netherlands)

- Leonardo S.p.A. (Italy)

- United Aircraft Corporation (UAC) (Russia)

- Aviation Industry Corporation of China (AVIC) (China)

- Hindustan Aeronautics Limited (HAL) (India)

KEY INDUSTRY DEVELOPMENTS

- May 2026: Israel expanded its USD 34 million F-35I Adir fleet capabilities with a new Elbit Systems avionics contract.

- May 2026: The Indian government finalized the Letter of Request (LoR) for a massive USD 39 billion program to acquire 114 Rafale jets.

- May 2026: Dassault Aviation and Tata Advanced Systems Limited (TASL) finalized Production Transfer Agreements to manufacture Rafale fuselage sections in India, with production starting in 2028.

- April 2025: India signed a USD 1 billion agreement with the U.S. for 113 GE engines to power its domestic Tejas Mk1A fighter jets.

- March 2025: The U.S. Department of Air Force awarded Boeing the engineering and manufacturing development contract for the next-generation NGAD platform (designated as the F-47).

REPORT COVERAGE

The market research report offers a detailed analysis of emerging trends and rapidly adopted technologies in the industry across key regions. The report outlines key factors driving market growth and discusses challenges for expansion, delivering a detailed picture of the fighter jet industry landscape. The study also highlights recent advancements to support stakeholders in making well-informed decisions.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Platform Class, By Propulsion, By Type, By Take-off and Landing, and Region |

| By Platform Class |

|

| By Propulsion |

|

| By Type |

|

| By Take-off and Landing |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 78.64 billion in 2025 and is projected to reach USD 126.52 billion by 2034.

In 2025, the North America market value stood at USD 31.84 billion.

The market is expected to exhibit a CAGR of 5.5% during the forecast period of 2026-2034.

By platform class, the medium fighter segment led the market in 2025.

The rising geopolitical tensions and defense modernization mandates are key factors fueling the market growth.

Lockheed Martin Corporation (U.S.), The Boeing Company (U.S.), Dassault Aviation SA (France), Saab AB (Sweden), BAE Systems plc (U.K.), and Hindustan Aeronautics Limited (HAL) (India) are major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us