Fire Stopping Materials Market Size, Share & Industry Analysis, By Product Type (Sealants, Blocks & Boards, Collars & Cast-in Devices, Mortars, Putty & Putty Pads, and Others), By End Use (Commercial, Residential, and Industrial & Utility Facilities), and Regional Forecast, 2026-2034

Fire Stopping Materials Market Size and Future Outlook

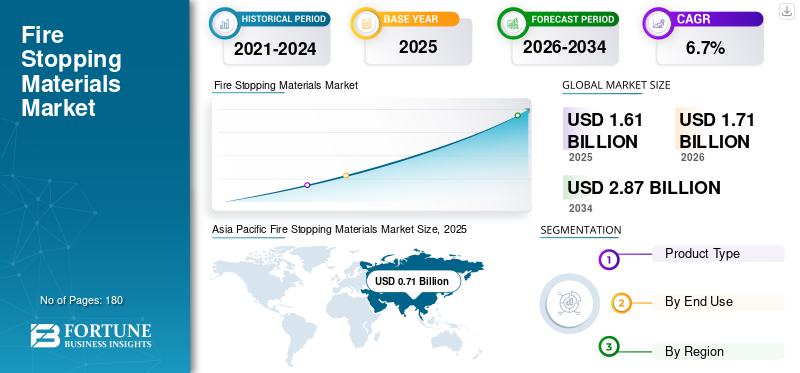

The global fire-stopping materials market size was valued at USD 1.61 billion in 2025. The market is projected to grow from USD 1.71 billion in 2026 to USD 2.87 billion by 2034, exhibiting a CAGR of 6.7% during the forecast period. Asia Pacific dominated the fire-stopping materials market with a market share of 44.09% in 2025.

Fire stopping materials are specialized passive fire protection solutions designed to seal gaps & joints, penetrations, and service openings in fire-rated walls and floors to prevent the spread of flames, smoke, and toxic gases during a fire event. They play a critical role in maintaining the integrity of compartmentation systems, ensuring occupant safety, limiting property damage, and supporting regulatory compliance. These materials are extensively used across residential and commercial buildings, industrial plants, data centers, healthcare facilities, transportation infrastructure, and energy projects, particularly where complex mechanical, electrical, and plumbing (MEP) systems create multiple wall and floor penetrations. The market is driven by tightening fire safety regulations, rising awareness of life-safety standards, rapid urban development, and increased investment in high-value assets such as hospitals, airports, metro systems, and commercial complexes. Renovation and retrofit activities in aging buildings further support steady demand for fire stopping systems.

The global fire stopping materials industry is characterized by manufacturers with strong technical expertise in fire testing, certification protocols, and materials science innovation. Key players such as Hilti Group, 3M, Sika AG, Fischer, and Promat maintain competitive positions through comprehensive product portfolios including sealants, intumescent coatings, firestop collars, wraps, and mortars. These players benefit from close collaboration with architects, contractors, and code authorities, offering engineered systems, on-site technical support, and advanced fire stopping solutions tailored to address complex building environments.

Download Free sample to learn more about this report.

Fire Stopping Materials Market MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.61 billion

- 2026 Market Size: USD 1.71 billion

- 2034 Forecast Market Size: USD 2.87 billion

- CAGR: 6.7% from 2026–2034

- Asia Pacific dominated the fire-stopping materials market with a 44.09% share in 2025.

- Residential segment led vessel type demand with a 29.0% share in 2026.

- Sealants segment led the product type market due to wide application across building penetrations.

North American

North America recorded USD 0.39 billion in 2025, supported by strong regulatory compliance and renovation activity.

Europe

Europe reached USD 0.34 billion in 2025 and is set to rise at a CAGR of 5.8% over the forecast period.

Asia Pacific

Asia Pacific reached USD 0.76 billion in 2026, driven by rapid urbanization and strict fire safety enforcement.

U.S.

Market is estimated at USD 0.34 billion in 2026, driven by NFPA and IBC fire safety compliance.

Japan

Growth supported by high-rise construction safety standards and advanced building codes.

Read More

FIRE STOPPING MATERIALS MARKET TRENDS

Growing Adoption of Certified, System-Based Passive Fire Protection Solutions to Favor Product Demand

Building owners and contractors are increasingly shifting toward fully tested and certified fire-stopping systems rather than standalone sealants or site-specific solutions. System-based firestop assemblies, including sealants, collars, wraps, boards, and intumescent coatings, ensure compliance with stringent fire-resistance ratings and third-party certification standards. As modern buildings incorporate dense MEP networks, data cabling, and modular construction techniques, the complexity of service penetrations increases, which demands engineered firestop solutions. The trend aligns with broader construction industry priorities focused on life safety, liability reduction, insurance compliance, and long-term asset protection. Such norms are strictly followed, particularly in high-rise buildings, healthcare facilities, airports, and other settings. Hence, the growing adoption of certified, system-based passive fire protection solutions is favoring product demand.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Fire Safety Regulations and Expanding Urban Infrastructure Sustain Demand

The rapid expansion of high-rise residential, commercial, and mixed-use infrastructure across urban centers is significantly increasing the need for compartmentalized fire protection systems. As buildings grow taller and more complex in design, the density of electrical, plumbing, HVAC, and data penetrations across floors increases substantially, creating higher fire-propagation risks if not properly sealed. At the same time, regulatory bodies globally are tightening fire safety codes following high-profile fire incidents, mandating the use of certified firestop systems for penetrations and joints. Authorities are also increasing inspection frequency and enforcement of compliance, compelling contractors and developers to adopt tested, third-party-approved fire-stopping materials. Together, vertical construction trends and stricter code enforcement are structurally elevating demand for advanced intumescent sealants, firestop wraps, boards, and barrier systems across both new developments and refurbishment projects. The aforementioned factors are set to drive the global fire stopping materials market growth during the forecast period.

- According to the U.S. Infrastructure Investment and Jobs Act (IIJA), approximately USD 1.2 trillion has been allocated toward infrastructure modernization, indirectly supporting demand for compliant fire protection materials across transportation hubs, utilities, and public buildings.

MARKET RESTRAINTS

High Compliance Costs and Installation Complexity Limit Penetration in Price-Sensitive Projects

Certified fire stop products typically involve third-party fire testing, comprehensive documentation, trained applicators, and mandatory inspection procedures, all of which significantly increase installation and lifecycle compliance costs compared to non-certified or improvised sealing methods. High installation and inspection costs can discourage adoption, particularly in cost-sensitive residential and small-scale commercial projects, where contractors often prioritize immediate budgetary considerations over long-term risk mitigation. Additionally, a lack of skilled installers in several emerging markets leads to inconsistent application quality, raising the risk of non-compliance and potential liability exposure for developers and contractors. This challenge is further compounded by variability in regional fire code enforcement, as inconsistent inspection rigor and regulatory oversight create uneven demand patterns and slower penetration of advanced, premium fire stopping systems in developing economies.

MARKET OPPORTUNITIES

Increasing Data Center Construction Requiring Advanced Compartmentalization, Creating Opportunities in Market

The rapid expansion of hyperscale and edge data centers is creating new opportunities for advanced fire-stopping materials, as these facilities require highly engineered compartmentalization to protect mission-critical infrastructure. Data centers contain dense cable trays, power distribution units, cooling systems, and server racks that create numerous wall and floor penetrations, increasing fire spread risks if not properly sealed. Unlike conventional buildings, downtime in data centers can result in substantial financial losses. As a result, there is an increase in demand for high-performance, low-smoke, and halogen-free firestop systems that maintain integrity without damaging sensitive electronic equipment. As global investments in cloud computing, AI infrastructure, and digital storage accelerate, the need for reliable, certified fire compartmentation solutions in both new builds and retrofits is expected to expand steadily.

- The Government of India is actively positioning the country as a global data center hub by targeting up to USD 200 billion in total investments to build world-class data center infrastructure, including supportive tax holidays and policy measures to attract capital from global cloud and AI players.

Segmentation Analysis

By Product Type

Sealants Led Market Owing to Extensive Application across Penetration and Joint Systems

Based on product type, the market is segmented into sealants, blocks & boards, collars & cast-in devices, mortars, putty & putty pads, and others.

The sealants segment accounted for the largest global fire stopping materials market share in 2025, driven by its widespread application in sealing linear joints, cable penetrations, pipe openings, and curtain wall gaps across commercial, residential, and industrial buildings. Firestop sealants offer flexibility, ease of application, and compatibility with diverse substrates, making them a preferred solution in both new construction and retrofit projects. The segment’s growth is supported by increasing code compliance requirements and rising installation across high-density building services.

Blocks & boards represent the fastest-growing product segment, expanding at a CAGR of 7.0% during the forecast period. The segment’s growth is driven by rising adoption in large commercial facilities, data centers, and industrial plants where re-penetrable and modular firestop systems are required to accommodate frequent cable modifications. Their clean installation profile, reusability, and suitability for high-traffic service openings make them increasingly attractive in mission-critical infrastructure projects.

Collars & cast-in devices are primarily used to seal plastic pipe penetrations that require intumescent expansion during fire exposure. Increasing installation of PVC and combustible piping systems in residential and commercial buildings supports steady demand. Cast-in devices are gaining particular traction in high-rise and large commercial developments, as they allow pre-installation during slab casting, improving installation efficiency and ensuring inspection compliance. Such exceptional parameters are set to drive the segment’s growth at a CAGR of 6.2% over the forecast period.

By End Use

To know how our report can help streamline your business, Speak to Analyst

Commercial Segment Led Market Owing to High Code Enforcement and Complex Building Designs

By end use, the market is segmented into residential, commercial, and industrial & utility facilities.

The commercial segment held the dominant share in 2025 due to the high density of MEP installations and strict life-safety regulations in office complexes, hospitals, airports, hotels, educational institutions, retail centers, and data centers. High enforcement of fire codes, third-party inspections, and liability considerations make fire stopping systems mandatory across commercial developments. Growth in vertical construction and mixed-use buildings further sustains segment expansion.

The residential segment is expected to grow at a CAGR of 6.2% during 2026–2034 due to rapid urbanization, expansion of multi-family housing projects, and increasing enforcement of fire safety standards in mid- and high-rise buildings. The rising installation of electrical systems, plumbing networks, and vertical service shafts in apartment complexes requires certified firestop solutions to maintain compartment integrity. While adoption remains slightly moderated in low-rise and cost-sensitive housing markets, compliance requirements in urban high-density developments continue to sustain steady demand.

The industrial & utility facilities segment is set to rise at a CAGR of 6.9% during 2026–2034, driven by increasing investments in energy infrastructure, manufacturing facilities, transportation hubs, and critical utility installations. Industrial environments require robust fire-compartmentation systems to protect high-value equipment, maintain operational continuity, and comply with stringent safety standards. Expansion of power plants, oil & gas facilities, data centers, and public infrastructure projects, particularly across the Asia Pacific and the Middle East, continues to drive demand for durable, heavy-duty fire-stopping materials.

Fire Stopping Materials Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Fire Stopping Materials Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the global market in 2025, reaching USD 0.71 billion, and is expected to maintain its leadership in 2026 with USD 0.76 billion. The region’s dominance is driven by rapid urbanization, high-rise residential development, expansion of commercial infrastructure, and increasing enforcement of fire safety regulations across China, India, and Southeast Asia. Growing installation of complex MEP systems in dense urban structures continues to accelerate demand for certified firestop sealants, collars, boards, and mortars to maintain compartment integrity and regulatory compliance.

China Fire Stopping Materials Market

China is expected to reach USD 0.40 billion in 2026, representing around 24% of global demand, supported by large-scale urban housing projects, metro rail expansion, healthcare infrastructure, and tightening fire code enforcement standards.

India Fire Stopping Materials Market

India is expected to reach USD 0.11 billion in 2026, driven by expansion in high-rise residential construction, growth in commercial real estate, and government-led infrastructure initiatives emphasizing improved building safety compliance.

North America

The market in North America reached USD 0.39 billion in 2025, supported by stable residential demand, strong commercial renovation activity, and infrastructure rehabilitation programs. The U.S. remains the dominant regional market due to strict fire protection codes, high inspection standards, and widespread adoption of certified passive fire protection systems. Ongoing upgrades to aging transportation networks, public infrastructure, healthcare facilities, and data centers are driving demand for compliant fire-stopping materials.

U.S. Fire Stopping Materials Market

The U.S. market is expected to reach USD 0.34 billion in 2026, accounting for roughly 20% of global revenues. Growth is supported by stringent building codes (IBC and NFPA standards), retrofit projects, and expansion of mission-critical infrastructure such as data centers and healthcare facilities.

Europe

Europe reached USD 0.34 billion in 2025 and is set to rise at a CAGR of 5.8% over the forecast period. Commercial construction activity, infrastructure upgrades, and strict fire safety regulations across the European Union support demand. Increasing focus on certified, system-based fire protection solutions and enhanced inspection protocols is driving the adoption of advanced firestop materials. Sustainability considerations and energy-efficient building renovations further contribute to steady market expansion.

Germany Fire Stopping Materials Market

Germany is expected to reach USD 0.08 billion in 2026, representing around 5% of global demand, supported by industrial construction, infrastructure modernization, and strong enforcement of fire safety standards in commercial and public buildings.

U.K. Fire Stopping Materials Market

The U.K. market in 2026 is expected to reach USD 0.06 billion, accounting for roughly ~3% of global revenues. Heightened regulatory scrutiny following building safety reforms and increasing demand for compliant compartmentation systems in residential and mixed-use high-rise projects are driving growth.

Latin America

Latin America reached USD 0.08 billion in 2025, supported by residential and commercial construction growth. Expanding urban infrastructure and the gradual strengthening of fire safety awareness are contributing to the rising adoption of certified fire-stopping materials. Government-backed transportation and public infrastructure projects, particularly in Brazil, are creating steady demand for passive fire protection systems.

Brazil Fire Stopping Materials Market

The Brazil market in 2026 is expected to reach USD 0.04 billion, accounting for roughly ~2% of global revenues. Demand is supported by infrastructure investments in transportation, airports, sanitation, and public housing programs, where improved building safety standards are increasingly incorporated into project specifications.

Middle East & Africa

The Middle East & Africa market reached USD 0.10 billion in 2025, driven by large-scale infrastructure development and rapid urban expansion, particularly in Gulf countries. Growth in high-rise towers, airports, commercial complexes, and mega urban projects requires advanced passive fire protection systems to meet international safety standards. Saudi Arabia’s Vision 2030 initiatives and major construction developments in the UAE are significant demand drivers, particularly for high-performance firestop systems used in complex building environments.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation, Capacity Expansion, and Compliance-Driven Solutions Shape Competitive Intensity

The fire stopping materials market is shaped by manufacturers that combine product innovation, regional capacity expansion, and certification-led system development to strengthen their competitive positioning. Leading players such as Hilti Group, 3M, Sika AG, Fischer, and Promat are focusing on advanced intumescent technologies, re-penetrable systems for data centers, sustainable low-VOC formulations, and expansion of fire-rated board production to address rising regulatory and infrastructure-driven demand. Strategic acquisitions and portfolio enhancements are further enabling companies to broaden their technical capabilities and geographic reach. Firms that integrate certified product systems with engineering advisory support and regional manufacturing scale continue to gain an advantage as global fire safety enforcement tightens and project complexity increases.

LIST OF KEY FIRE STOPPING MATERIAL COMPANIES PROFILED

- 3M (U.S.)

- Fischer (Germany)

- Flamro (Germany)

- Hilti (Liechtenstein)

- KuhnOdice (France)

- Promat (Belgium)

- Pyroplex (U.K.)

- RectorSeal (U.S.)

- SIKA (Switzerland)

- Stanvac Chemicals India Ltd. (India)

KEY INDUSTRY DEVELOPMENTS

- October 2025: 3M introduced enhanced fire barrier solutions, including upgraded 3M™ Fire Barrier Electrical Box Inserts and Tuck-In Wrap Strips featuring advanced intumescent Hyper-GS technology. The improvements strengthen fire resistance performance while simplifying installation in both new construction and retrofit applications.

- September 2025: Hilti launched a new firestopping solution called Firestop Flexible Seal, aimed at sealing medium to large openings quickly and efficiently on construction sites. This addition expands Hilti’s firestop portfolio with a product that is faster to install and offers versatility across construction types, representing a meaningful enhancement for passive fire protection systems.

- August 2025: Tremco expanded its TREMstop® firestopping product line with new solutions, including TREMstop® Acrylic Spray and SuperStrip Intumescent Wrap Strips, broadening its offering for penetration seals and joint fire protection systems across commercial and infrastructure projects.

- December 2024: Saint-Gobain, through its construction solutions business, continued expanding its fire protection systems portfolio, including high-performance firestop sealants and boards designed to improve compartmentation performance in commercial and high-rise buildings amid tightening fire codes globally.

- May 2024: Sika strengthened its passive fire protection portfolio through continued expansion of its Sikacryl® and SikaSeal® firestop systems, enhancing certified solutions for service penetrations and linear joints to comply with increasingly stringent global fire safety regulations.

REPORT COVERAGE

The global fire stopping materials market analysis provides an in-depth study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The fire stopping materials market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.7% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, End Use, and Region |

| Product Type |

|

| By End Use |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 1.61 billion in 2025 and is projected to reach USD 2.87 billion by 2034.

In 2025, the market value in Asia Pacific stood at USD 0.71 billion.

Recording a CAGR of 6.7%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The commercial end use segment led the market in 2025.

High-rise infrastructure and stringent building safety regulations are expected to drive market growth.

Hilti Group, 3M, Sika AG, Fischer, and Promat are some of the prominent players in the market.

Asia Pacific held the highest market share in 2025.

The growing adoption of certified, system-based passive fire protection solutions is expected to drive product demand.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us