Foam Concrete Market Size, Share & Industry Analysis, By Density (Low Density, Medium Density, and High Density), By Application (Void Filling & Geotechnical Applications, Roof Insulation & Floor Screeds, Trench Reinstatement, Road Sub-Base & Infrastructure, and Blocks, Panels & Precast Elements), By End-Use Industry (Residential, Commercial, Industrial, and Infrastructure) and Regional Forecast, 2026-2034

Foam Concrete Market Size and Future Outlook

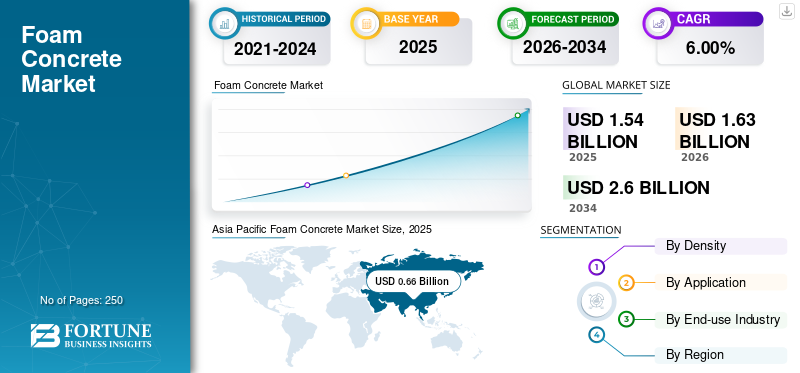

The global foam concrete market size was valued at USD 1.54 billion in 2025. The market is projected to grow from USD 1.63 billion in 2026 to USD 2.60 billion by 2034, exhibiting a CAGR of 6.00% during the forecast period. Asia Pacific dominated the foam concrete market with a market share of 42.85% in 2025.

Foam concrete, also referred to as foamed concrete or cellular foam concrete, is a lightweight cement-based material produced by introducing stable pre-formed foam into a cementitious slurry. The entrained air bubbles create a uniform cellular structure, resulting in significantly reduced density compared to conventional concrete, while maintaining flowability, self-leveling characteristics, and controlled compressive strength.

Foam concrete is gaining traction as a functional construction material that addresses weight, constructability, and performance challenges, particularly in infrastructure and urban construction projects, where speed, stability, and efficiency are increasingly critical.

Many key industry players, including EUROCEMENT, LafargeHolicim, VOTORANTIM Group, and CEMEX operating in the market, are focusing on developing innovative products to meet the rising demand for lightweight construction materials.

Download Free sample to learn more about this report.

FOAM CONCRETE MARKET TRENDS

Shift Toward Low-Density and Application-Specific Formulations is the Latest Market Trend

The foam concrete market is witnessing a clear shift toward low-density, application-specific formulations, as end users increasingly prioritize functional performance over generalized material specifications. Traditionally, foamed concrete was supplied within a limited range of standard densities; however, the growing diversity in infrastructure and building applications has created demand for tailored density-strength combinations.

Low-density formulations are particularly favored in void filling, geotechnical stabilization, trench reinstatement, and lightweight backfilling applications, where the primary objective is load reduction rather than structural strength. By optimizing density levels, contractors can minimize settlement risks, reduce stress on underlying soils, and improve long-term ground stability. At the same time, application-specific mix designs allow precise control over flowability, setting time, and compressive strength, ensuring compatibility with project-specific construction constraints.

Manufacturers and solution providers are responding by developing customized foaming agents and mix designs that can be adjusted on-site to meet exact project requirements. This shift is further supported by the increased use of mobile foaming units and ready-mix integration systems, enabling real-time density adjustment and quality control.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand For Lightweight Construction Solutions to Boost Market Growth

The growing demand for lightweight construction solutions is a key driver of the foam concrete market, as builders and infrastructure developers increasingly seek materials that reduce structural load without compromising constructability. Foam concrete offers a significant weight advantage over conventional concrete, enabling designers to lower dead loads on foundations, slabs, bridge decks, and substructures, particularly in high-rise buildings and infrastructure projects built on weak or variable soil conditions.

In dense urban environments, where space constraints horizontal expansion, lightweight materials such as foam concrete support retrofitting, vertical expansion, and structural rehabilitation without requiring extensive structural reinforcement upgrades. This makes foam concrete especially attractive for floor screeds, roof insulation layers, bridge approaches, and backfilling applications. By reducing overall structural weight, projects can achieve savings in reinforcement and foundation design, improving overall project economics.

Infrastructure development further reinforces this trend, as lightweight solutions help mitigate settlement risks in road sub-bases, tunnels, and utility corridors. Additionally, reduced material weight simplifies transportation, pumping, and placement, enabling faster construction cycles and lower labor requirements. As urbanization intensifies and construction increasingly emphasizes performance-driven design, cost-efficient design, demand for lightweight materials continues to rise, positioning foam concrete as a practical solution to both engineering and economic challenges across residential, commercial, and infrastructure projects.

MARKET RESTRAINTS

Limited Awareness, Standardization, And Specification Acceptance to Hamper Market Growth

One of the significant restraints in the foam concrete market is the limited level of awareness, standardization, and formal specification acceptance, particularly in emerging and developing regions. Unlike conventional concrete, which is governed by well-established codes and standards, foam concrete is often treated as a project-specific or specialty material. This creates uncertainty among engineers, consultants, and contractors regarding its long-term performance and appropriate use cases.

In many markets, the absence of uniform design guidelines and standardized testing protocols makes it difficult for specifiers to confidently evaluate foam concrete with traditional alternatives. As a results, conservative material selection practices often favor conventional solutions despite the potential advantages of foam concrete in weight reduction and constructability. Furthermore, limited exposure and training among contractors can create concerns around mix consistency, density control, and quality assurance, especially for on-site production.

These challenges are compounded in public infrastructure projects, where procurement frameworks and approval processes typically prioritize with established regulatory backing and long-performance records. As a result, adoption can be slowed by lengthy approval cycles and the need for extensive project-level validation. Until broader code recognition, industry education, and standardized specifications are implemented, this restraint will continue limiting market penetration despite growing demand for lightweight construction & building solutions.

MARKET OPPORTUNITIES

Expanding Infrastructure Rehabilitation And Urban Redevelopment Projects May Create Lucrative Growth Opportunities

The accelerating pace of infrastructure rehabilitation and urban redevelopment presents a significant growth opportunity for the market. Across both developed and emerging economies, aging infrastructure such as roads, bridges, tunnels, underground utilities, and transit systems requires repair, reinforcement, or replacement, often under conditions where minimizing disruption and construction time is critical. Foam concrete is particularly well suited to these environments due to its self-leveling properties, rapid placement capability, and reduced load impact on extsting structures.

In urban redevelopment projects, space constraints and existing structural limitations frequently restrict the use of heavy backfill materials. Foam concrete enables lightweight void filling, trench reinstatement, and ground stabilization without overstressing surrounding structures or utilities. This makes it an attractive solution for sinkhole remediation, abandoned pipe filling, and foundation retrofitting in dense city centers.

Additionally, governments are increasingly prioritizing faster project delivery and lifecycle cost efficiency in infrastructure spending. Foam Concrete supports these objectives by reducing excavation requirements, lowering labor intensity, and minimizing the need for mechanical compaction. As public and private investment in infrastructure rehabilitation continues to rise, particularly in North America, Europe, and Asia Pacific, the material is well positioned to evolve from a niche solution into a preferred material in urban infrastructure and redevelopment projects, creating a sustained long-term growth opportunity.

MARKET CHALLENGES

Ensuring Consistent Quality and Performance Across Project Sites Pose A Critical Challenge To Market Growth

A major challenge facing the market is maintaining consistent quality and performance across different project sites. Unlike conventional concrete, which is often produced in controlled batching environments, the product is frequently mixed and foamed on site, making final performance highly sensitive to foam stability, mix proportions, water quality, and operator expertise. Even minor variations in these parameters can result in deviations in density,comprehensive strength, and flowability.

This variability creates challenges for contractors and specifiers, particularly in large infrastructure projects where uniform performance over long distances or large volumes is essential. Inconsistent outcomes can increase the risk of settlement, uneven curing, or performance shortfalls, leading to rework or conservative overdesign.

Additionally, effective quality assurance often relies on specialized equipment and trained personnel, which may not be readily available across all regions. In markets with limited technical expertise or fragmented contractor ecosystems, scaling foam concrete solutions can be difficult. Addressing this challenge requires standardized procedures, improved workforce training, and greater use of engineered, system-based solutions. Without these measures, market penetration may remain uneven despite strong underlying demand drivers.

Segmentation Analysis

By Density

Low Density Segment Dominated due to its Widespread Use in Non-Structural And Geotechnical Applications

Based on density, the market is segmented into low density, medium density, and high density.

The low segment accounted for the largest market share in 2025 due to its widespread use in non-structural and geotechnical applications where weight reduction and ease of placement are critical performance requirements.

Low density is extensively used in void filling, trench reinstatement, ground stabilization, and lightweight backfilling, as it significantly reduces dead load on underlying soils and existing structures. Its high flowability and self-leveling characteristics allow it to fill complex or confined spaces without mechanical compaction, making it particularly suitable for urban infrastructure and rehabilitation projects

The medium density segment is anticipated to grow at the CAGR of 5.84% over the forecast period. The segment is commonly used in floor screeds, roof insulation layers, and non-load-bearing building components, where moderate compressive strength is required alongside improved thermal and acoustic performance. Its ability to provide uniform leveling and insulation in a single application makes it particularly attractive in residential and commercial construction, supporting faster installation and reduced labor requirements.

By Application

Void Filling & Geotechnical Applications Led the Market Due To High Demand

Based on application, the market is segmented into void filling & geotechnical applications, roof insulation & floor screeds, trench reinstatement, road sub-base & infrastructure, and blocks, panels & precast elements.

The void filling & geotechnical applications segment accounted for the dominant market share in 2025, driven by its extensive use in infrastructure construction, ground stabilization, and urban redevelopment projects where load reduction and flowability are critical.

Void filling and geotechnical applications represent the core use case for foam concrete, as the material’s self-leveling behavior, pumpability, and low density make it highly effective for filling underground cavities, abandoned utilities, sinkholes, and weak soil zones. In comparison to conventional backfill materials, the project exerts significantly lower lateral and vertical pressures, reducing the risk of settlement and damage to adjacent structures.

Trench reinstatement represents a key application segment within the market, driven by the need for fast, efficient, and durable restoration of excavated utility trenches. This application is widely used in water, sewage, gas, electricity, and telecom infrastructure projects, particularly in dense urban areas where minimizing surface disruption is critical. The segmeny is exoected to grow with a CAGR of 5.8%.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Residential Segment To Lead Market Due To its Widespread Use In Housing Construction

Based on end-use, the market is segmented into residential, commercial, industrial, and infrastructure.

Residential segment accounted for the dominant market share in 2025, driven by its widespread use in housing construction and residential renovation projects where materials that are lightweight and have thermal insulation properties are increasingly prioritized.

In residential applications, the product is commonly used for floor screeds, roof insulation layers, void filling, and leveling applications, particularly in multi-storey housing and affordable housing developments. Its low density and self-leveling characteristics help reduce dead load on building structures, making it well suited for vertical construction and retrofitting projects.

The infrastructure segment is a key growth contributor, driven by demand from roads, bridges, tunnels, and utility networks. Foam Concrete is increasingly used in void filling, trench reinstatement, road sub-bases, and geotechnical stabilization, where speed of placement and settlement control are critical. Rising investment in infrastructure rehabilitation and urban utility upDensitys continues to strengthen this segment’s importance within the overall market. The segment is expected to grow with a CAGR of 6.4%.

Foam Concrete Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Foam Concrete Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific reached USD 0.66 billion in 2025 and secure its position as the largest region in the market driven by rapid urbanization, large-scale residential construction, and expanding infrastructure investment. The product is widely used in housing projects, transportation infrastructure, and geotechnical applications, particularly in China and India. Cost efficiency, speed of construction, and load-reduction benefits are key adoption drivers, making the region a central growth engine for the global market.

Japan Foam Concrete Market

The Japan market in 2026 is estimated at around USD 0.07 billion, accounting for roughly 4.2% of global revenues. The market is characterized by mature, application-specific adoption, driven primarily by infrastructure maintenance, urban redevelopment, and seismic-resilient construction practices rather than new greenfield construction.

China Foam Concrete Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.29 billion, representing roughly 17.9% of global sales. China represents the largest market within the region, driven by the country’s extensive construction scale, rapid urbanization, and continuous infrastructure development. The product is widely used across residential construction, transportation infrastructure, and geotechnical applications, where lightweight materials are required to manage load and improve construction efficiency.

India Foam Concrete Market

The India market in 2026 is estimated at around USD 0.16 billion, accounting for roughly 10.06% of global revenues. The India market is in a high-growth, early-to-mid adoption phase, driven by rapid urbanization, large-scale housing programs, and expanding infrastructure investment. The product is increasingly used in residential construction, infrastructure backfilling, and geotechnical applications, where lightweight materials and faster execution are critical.

To know how our report can help streamline your business, Speak to Analyst

North America

North America held a significant share in 2025, valued at around USD 0.31 billion. The region is characterized by strong demand from infrastructure rehabilitation and trench reinstatement applications. Aging utility networks, road rehabilitation programs, and urban redevelopment projects in the U.S. and Canada have increased the use of the product for void filling and lightweight backfilling. The region benefits from higher awareness and established use of flowable fill technologies, supporting consistent adoption. Growth is steady, driven by replacement and maintenance activity than by new construction.

U.S. Foam Concrete Market

The U.S. market is expected to reach around USD 0.28 billion by 2026. The U.S. accounts for the dominant share of the market driven by its large-scale infrastructure network, high frequency of utility rehabilitation projects, and well-established construction practices. The country has a significant concentration of aging roads, bridges, and underground utility systems, which has increased demand for the product in void filling, trench reinstatement, and geotechnical stabilization applications.

Europe

Europe is projected to grow at 5.55% over the coming years and reach a valuation of USD 0.38 billion by 2026. The regions represents a mature and regulation-driven market, supported by rising demand for energy efficient buildings and infrastructure rehabilitation. Demand is largely driven by floor screeds, roof insulation, trench reinstatement, and utility corridor upDensitys, particularly in Western Europe. Strict building codes and sustainability regulations have encouraged the adoption of lightweight and thermally efficient materials, supporting steady market growth. However, market expansion is relatively moderate due to high penetration levels and conservative specification practices.

U.K. Foam Concrete Market

The U.K. market is estimated to reach around USD 0.06 billion by 2026, representing roughly 3.8% of global revenues.

Germany Foam Concrete Market

Germany’s market is projected to reach approximately USD 0.08 billion in 2026, equivalent to around 5.0% of global sales.

Latin America and Middle East & Africa

The Latin America market is an emerging and gradually developing market, driven by urbanization, housing demand, and transportation infrastructure investment. The product is primarily used in residential floor screeds, void filling, and road-related applications, where lightweight materials help address soil variability and construction efficiency challenges. Countries such as Brazil and Mexico account for the majority of regional demand due to their larger construction markets and ongoing public infrastructure programs. The Latin America market is set to reach a valuation of USD 0.13 billion by 2026.

The Middle East & Africa Foam Concrete market is largely project-driven, supported by large-scale infrastructure and real estate developments, especially in the Gulf Cooperation Council (GCC) countries. Foam Concrete is widely applied in ground stabilization, void filling, and road sub-base applications, where challenging soil conditions and high temperatures favor lightweight construction solutions. The Middle East & Africa reached USD 0.09 billion in 2025.

GCC Market

The GCC market is projected to reach around USD 0.06 billion in 2026, representing roughly 3.49% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus On Innovations By Key Players To Propel Market Progress

The market is moderately fragmented and service-driven, with competition shaped by a mix of global construction materials companies, specialty foamed concrete solution providers, and large engineering & construction contractors. Unlike conventional concrete markets, value creation in the product depends on execution capacibilities, application experties, and project-specific enginerring solutions. EUROCEMENT, LafargeHolicim, VOTORANTIM Group, and CEMEX are the largest players in the market.

Other notable players in the global market include Bouygues, Bechtel Corporation, Shanghai Construction Group, Luca Industries International, Boral Concrete, Grupo ACS, CNBM and Vinci S.A.

LIST OF KEY FOAM CONCRETE COMPANIES PROFILED

- Holcim Group (Switzerland)

- Heidelberg Materials (Germany)

- CEMEX S.A.B. de C.V. (Mexico)

- Luca Industries International (Germany)

- China National Building Material Group (CNBM) (China)

- Cematrix (Canada)

- Geofill LLC (U.S.)

- Cellucrete Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

October 2024: London Concrete announce the U.K. launch of two groundbreaking products from its innovative Airium range: Airium Roadfill and Airium Voidfill. These advanced foam concrete solutions are set to redefine efficiency, reliability, and environmental responsibility in the construction industry, offering unmatched benefits to contractors, infrastructure teams, and environmental engineers.

REPORT COVERAGE

The global market analysis includes a comprehensive study of the market size & forecast across all market segments covered in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments, and their prevalence by key regions. The global market research report also provides a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.00% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Density, Application, End-Use Industry, and Region |

| By Density |

|

| By Application |

|

| By End-use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.54 billion in 2025 and is projected to reach USD 2.60 billion by 2034

In 2025, the market value in the Asia Pacific stood at USD 0.66 billion.

The market is expected to grow at a CAGR of 6.00% over the forecast period (2026-2034).

By density, the low density led the market.

The rising demand for lightweight construction solutions are the key drivers of the market.

EUROCEMENT, LafargeHolicim, VOTORANTIM Group, and CEMEX are the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us