Freight Brokerage Market Size, Share & Industry Analysis, By Mode of Transportation (Road Freight Brokerage, Rail Freight Brokerage, Ocean & Inland Waterway Freight Brokerage, and Air Freight Brokerage), By Brokerage Service Type (Spot Freight Brokerage, Contract Freight Brokerage, Intermodal/Multimodal Brokerage, and Managed Transportation Services), By Shipper Size (Large Enterprises, Mid-Sized Businesses, and Small & Medium Enterprises (SMEs)), By Industry Vertical (Retail & E-commerce, Manufacturing, Healthcare & Pharmaceuticals, Automotive, and Others) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

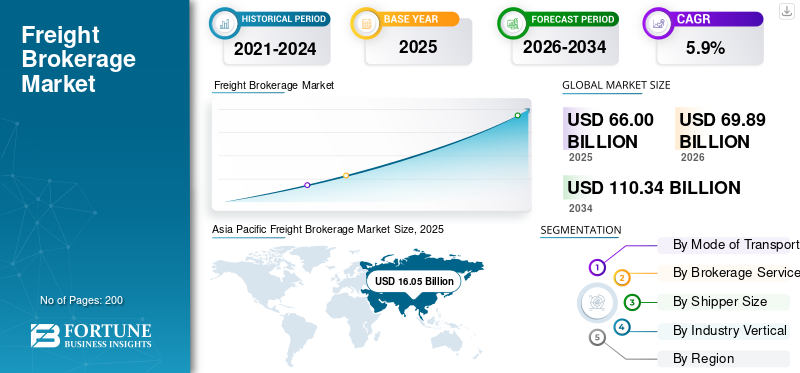

The global freight brokerage market size was valued at USD 66.00 billion in 2025. The market is projected to grow from USD 69.89 billion in 2026 to USD 110.34 billion by 2034, exhibiting a CAGR of 5.9% during the forecast period. Asia Pacific dominated the global market with a market share of 24.31% in 2025.

The global market encompasses the ecosystem of non-asset-based logistics intermediaries that facilitate the movement of goods by connecting shippers with transportation carriers across various modes, including road, rail, air, ocean, and intermodal. Freight brokers play a critical role in supply chain operations by managing carrier sourcing, rate negotiation, shipment coordination, documentation, and real-time tracking, without owning transportation assets. The market is driven by growing trade flows, increasing supply chain complexity, demand for flexible logistics operations solutions, and the rapid adoption of digital freight-matching and transportation management technologies.

Key player in the global market focuses on evaluating the competitive positioning of established logistics brokers and emerging digital-first players based on their service portfolios, modal coverage, geographic presence, customer bases, technology capabilities, and strategic initiatives. Leading players, including C.H. Robinson Worldwide, Inc., XPO, Inc., Uber Freight, Total Quality Logistics, and J.B. Hunt Transport Services, Inc., differentiate themselves through scale, carrier network strength, pricing efficiency, advanced analytics, and integrated digital platforms offering end-to-end shipment visibility.

Download Free sample to learn more about this report.

Freight Brokerage Market KEY TAKEAWAYS

- 2025 Market Size: USD 66.00 billion

- 2026 Market Size: USD 69.89 billion

- 2034 Forecast Market Size: USD 110.34 billion

- CAGR: 5.90% from 2026–2034

- Asia Pacific dominated the global market with a market share of 24.31% in 2025.

- The rail freight brokerage segment is poised to grow at a CAGR of 7.6%.

- The contract freight brokerage segment is poised to grow at a CAGR of 6.7%

North American

North America accounted for USD 23.50 billion in 2025 and maintained its leading position due to a well-established logistics network and strong e-commerce activity.

Europe

Europe held a significant share of the global freight brokerage market in 2025, supported by extensive cross-border trade and advanced transportation infrastructure.

Asia Pacific

Asia Pacific is expected to witness the fastest growth, driven by expanding manufacturing activities, increasing international trade, and rapid digitalization of logistics services.

U.S.

The U.S. freight brokerage market is projected to reach USD 24.95 billion by 2026, supported by rising freight volumes and growing adoption of digital brokerage platforms.

Japan

The Japan freight brokerage market is expected to grow steadily owing to increasing demand for efficient supply chain management and logistics optimization solutions.

Read More

FREIGHT BROKERAGE MARKET TRENDS

Increasing Shift Toward Digital and AI-Enabled Freight Brokerage Platforms is Shaping Market Trends

The global market is witnessing a pronounced shift toward digital and artificial intelligence-enabled freight brokerage platform, driven by the need for enhanced operational efficiency, cost-effectiveness, and real-time decision making. Traditionally, freight brokerage has relied on manual processes and fragmented communication between shippers and carriers, leading to inefficiencies and limited visibility. However, the integration of advanced digital solutions such as machine learning algorithms for rate forecasting, automated carrier matching, and AI-driven optimization engines is driving the market. These platforms enable dynamic pricing, predictive capacity management, and enhanced risk mitigation, supporting faster turnaround times and improved service reliability. Consequently, technology-focused freight brokers are expanding their digital capabilities through investments, partnerships with tech providers, and in-house development, accelerating the overall modernization of the market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Adoption of Digital Freight Brokerage Platforms and TMS Solutions Drives Market Growth

The rapid adoption of digital freight brokerage platforms and transportation management system (TMS) solutions is a key driver of the global market, as shippers and carriers increasingly seek technology-enabled logistics coordination. Digital platforms enable real-time freight matching, automated rate benchmarking, and end-to-end shipment visibility, significantly reducing manual processes and turnaround times. TMS solutions further support route optimization, performance monitoring, and data-driven decision-making, allowing freight brokers to enhance service reliability and scalability. As supply chains become more dynamic and time-sensitive, the shift toward digital brokerage and integrated logistics technologies continues to strengthen freight brokerage market growth during the forecast period.

- For instance, in 2025, major automotive OEMs such as Toyota and Volkswagen are expected to increasingly leverage digital freight brokerage and TMS-enabled logistics solutions to enhance supply chain resilience and visibility for inbound components and outbound vehicle shipments. These OEMs partnered with digital freight platforms, such as Uber Freight, to leverage dynamic capacity, data-driven carrier selection, and real-time shipment tracking, thereby supporting just-in-time (JIT) manufacturing schedules and reducing premium freight costs across North American and European operations.

MARKET RESTRAINTS

High Volatility in Freight Rates and Fuel Prices Is Limiting Market Growth

High volatility in freight rates and fuel prices is a key factor restraining the growth of the global market. Frequent fluctuations in fuel costs directly impact transportation pricing, making it challenging for freight brokers to maintain stable margins and offer predictable rates to shippers. Sudden changes in freight demand, carrier capacity constraints, and geopolitical or economic disruptions further intensify rate instability across regions. This volatility increases financial risk for brokers operating on thin margins, particularly in spot-market transactions. Moreover, uncertainty in pricing reduces long term contract visibility and limits profitability, thereby restraining market growth despite increasing demand for brokerage services.

MARKET OPPORTUNITIES

Expansion of E-commerce and Omnichannel Retail Logistics is Creating Market Opportunities

The expansion of e-commerce and omnichannel retail logistics is creating significant growth opportunities for the global market, as retailers increasingly integrate online, offline, and hybrid sales channels. This shift has resulted in higher shipment volumes, smaller and more frequent order sizes, and fragmented delivery patterns across regional and last-mile networks. Managing inventory replenishment, reverse logistics solutions, and time-sensitive deliveries across multiple channels has significantly increased transportation complexity. Freight brokers play a crucial role in addressing these challenges by providing flexible carrier sourcing, optimized routing solutions, and real-time shipment tracking to ensure timely and cost-effective deliveries. Furthermore, the growing focus on same-day and next-day delivery models has intensified the need for dynamic freight coordination. As e-commerce penetration continues to rise globally, shippers are increasingly relying on freight brokerage services to enhance supply chain agility, scalability, and operational efficiency, thereby supporting sustained market growth.

MARKET CHALLENGES

Complex Regulatory and Compliance Requirements Across Regions are Challenging Market Growth

Complex regulatory and compliance requirements across regions pose a significant challenge to the growth of the global market. Freight brokers operating across domestic and international trade lanes must comply with varying transportation laws, licensing requirements, customs regulations, safety standards, and documentation norms, which differ widely by country and region. Frequent regulatory updates related to carrier compliance, cross-border trade policies, and environmental standards further increase operational complexity and compliance costs. These challenges are particularly burdensome for small and mid-sized freight brokers, who often have limited regulatory expertise and resources. As a result, navigating fragmented regulatory frameworks can slow market entry, limit scalability, and increase operational risks, thereby restraining overall market efficiency and growth.

Segmentation Analysis

By Mode of Transportation

Road Freight Brokerage Segment Dominates Due to Flexibility and Strong Domestic Freight Demand

Based on the mode of transportation, the market is segmented into road freight brokerage, rail freight brokerage, ocean & inland waterway freight brokerage, and air freight brokerage.

The road freight brokerage segment is anticipated to account for the largest share of the global market. The dominance of this segment is primarily attributed to the extensive use of road transportation for domestic and short-to-medium-haul freight movement, particularly across the manufacturing, retail, and e-commerce industries. Road freight offers higher flexibility, faster transit times, door-to-door connectivity, and easier integration with last-mile delivery networks compared to other transport modes. The rising demand for time-sensitive deliveries, coupled with the growth of e-commerce and omnichannel retail logistics, has further strengthened reliance on road freight brokerage services. Additionally, the fragmented nature of the trucking industry increases the need for brokers to efficiently match shippers with available carriers, supporting sustained segmental growth.

The rail freight brokerage segment is poised to grow at a CAGR of 7.6%, showcasing the fastest growth over the analysis period.

By Brokerage Service Type

Contract Freight Brokerage Segment to Lead Due to Growing Demand for Rate Stability and Long-Term Capacity Assurance

Based on brokerage service type, the market is segmented into spot freight brokerage, contract freight brokerage, intermodal/multimodal brokerage, and managed transportation services.

The contract freight brokerage segment is expected to hold the largest share of the global market. The dominance of this segment is primarily driven by the growing need for rate stability, capacity assurance, and long-term logistics planning among shippers, particularly large enterprises and high-volume industries such as retail, manufacturing, and the automotive sector. Contract freight brokerage enables shippers to secure consistent carrier capacity at pre-negotiated rates, reducing exposure to spot-market volatility and fuel price fluctuations. Additionally, long-term contracts support better demand forecasting, operational efficiency, and service reliability for both shippers and brokers. As supply chains become more structured and cost-focused, the preference for contract-based brokerage arrangements continues to strengthen, reinforcing the segment’s leading market position.

The contract freight brokerage segment is poised to grow at a CAGR of 6.7%, showcasing the fastest growth over the analysis period.

To know how our report can help streamline your business, Speak to Analyst

By Shipper Size

Large Enterprises Segment Dominates Due to High Shipment Volumes and Advanced Logistics Requirements

Based on shipper size, the market is segmented into large enterprises, mid-sized businesses, and small and medium enterprises (SMEs).

The large enterprises segment is anticipated to dominate the global market. This dominance is primarily attributed to the high shipment volumes, complex supply chain networks, and multimodal transportation requirements associated with large enterprises operating across domestic and international markets. These organizations require scalable, reliable, and technology-enabled freight brokerage solutions to manage frequent shipments, cross-border logistics, and long-term carrier relationships.

Large enterprises also have a higher adoption rate of contract freight brokerage, managed transportation services, and advanced digital platforms, enabling better cost control, visibility, and risk management. Furthermore, their ability to engage in long-term strategic partnerships with freight brokers strengthens service continuity and operational efficiency, reinforcing the segment’s leading freight brokerage market share.

The large enterprises segment is poised to grow at a CAGR of 6.5%, showcasing the fastest growth over the analysis period.

By Industry Vertical

Manufacturing Segment to Hold the Largest Share Due to High-Volume and Complex Supply Chain Requirements

Based on industry vertical, the market is segmented into retail & e-commerce, manufacturing, healthcare & pharmaceuticals, automotive, and others.

The manufacturing segment is expected to account for the dominant share of the global market. This dominance is primarily driven by the high frequency of raw material sourcing, intra-facility transfers, and finished goods distribution across domestic and international supply chains. Manufacturing companies rely heavily on freight brokerage services to manage their complex and high-volume transportation requirements across various modes, including road, rail, ocean, and intermodal. The need for just-in-time production, inventory optimization, and cost-efficient logistics further strengthens demand for reliable brokerage solutions. Additionally, manufacturers are increasingly opting for long-term contract brokerage and managed transportation services to ensure capacity availability, rate stability, and end-to-end shipment visibility. As global manufacturing activities continue to expand and diversify, the reliance on freight brokers to enhance supply chain efficiency and resilience is expected to reinforce the segment’s leading market position.

The retail & e-commerce segment is poised to grow at a CAGR of 7.2%, showcasing the fastest growth over the analysis period.

Freight Brokerage Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Freight Brokerage Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the global market, driven by rapid industrialization, expanding manufacturing hubs, and rising intra-regional trade. Countries such as China, India, and those in Southeast Asia are experiencing strong growth in domestic freight movement and cross-border exports. The rapid expansion of e-commerce and omnichannel retail has significantly increased demand for flexible and scalable freight brokerage services. While the market remains fragmented, increasing investment in digital freight platforms, logistics infrastructure, and cross-border connectivity is driving the adoption of brokerage services across the region.

China Freight Brokerage Market

In China, the market in 2025 is estimated to be around USD 7.22 billion, representing approximately 10.9% of global freight brokerage revenues.

North America

North America is expected to hold a significant share of the global market, driven by a highly developed logistics infrastructure, strong domestic freight demand, and early adoption of digital brokerage platforms. The presence of a large and fragmented trucking industry increases reliance on freight brokers for efficient carrier matching and capacity management. Growth in e-commerce, cross-border trade within the USMCA region, and the adoption of contract freight brokerage among large enterprises further support market expansion. Additionally, advanced use of transportation management systems, data analytics, and AI-enabled platforms positions the region as a mature yet innovation-driven freight brokerage market.

U.S. Freight Brokerage Market

In the U.S., the market in 2025 is estimated to be around USD 21.08 billion, representing approximately 31.9% of global freight brokerage revenues.

Europe

Europe boasts a well-established market, underpinned by extensive cross-border trade, robust manufacturing activity, and a complex regulatory framework. The region’s dependence on multimodal transportation, which combines road, rail, and inland waterways, creates a consistent demand for brokerage services that can manage regulatory compliance and facilitate cross-border coordination. Increasing sustainability initiatives and emissions regulations are also influencing freight planning, encouraging shippers to optimize routes and modes through brokers. Growth in e-commerce, particularly in Western and Central Europe, along with the rising adoption of digital brokerage, continues to strengthen the region’s market outlook.

U.K. Freight Brokerage Market

The U.K. market in 2025 is estimated at around USD 3.75 billion, representing approximately 5.7% of global freight brokerage revenues.

Rest of the World

The Rest of the World, comprising Latin America, the Middle East, and Africa, is expected to register steady growth during the study period. The expansion of trade corridors, infrastructure development, and rising industrial and mining activities are key drivers of growth. In these regions, freight brokers play a crucial role in mitigating transportation inefficiencies, navigating regulatory complexities, and expanding limited carrier networks. The growing adoption of outsourced logistics services by enterprises, along with the gradual digitalization of freight operations, is improving market penetration. Although challenges such as infrastructure gaps persist, long-term trade and economic development continue to support market growth.

COMPETITIVE LANDSCAPE

Major Players are Focusing on Upgrading their Digital Platforms to Boost their Market Share

The global market exhibits a moderately consolidated competitive structure, characterized by the presence of large multinational logistics brokers alongside emerging digital-first platforms. Prominent players, including C.H. Robinson Worldwide, Inc., XPO, Inc., Uber Freight, Total Quality Logistics, and J.B. Hunt Transport Services, Inc., hold a significant market share due to their extensive carrier networks, diversified service portfolios, and strong geographic presence. These companies are actively focusing on enhancing their digital platforms, utilizing AI-enabled freight matching, and implementing data-driven pricing models to improve operational efficiency and customer experience. Strategic initiatives, including technology investments, partnerships, and acquisitions, are key approaches adopted to strengthen competitive positioning.

- For instance, in May 2025, Uber Freight announced enhancements to its digital freight platform by integrating advanced AI-driven pricing and carrier-matching capabilities to improve shipment visibility and reduce booking cycle times for shippers.

Other notable players operating in the global market include Echo Global Logistics, Inc., RXO, Inc., Kuehne + Nagel International AG, and DB Schenker. These companies are expected to focus on platform innovation, expanding contract freight services, and strategic collaborations to enhance their market presence and capitalize on emerging growth opportunities during the forecast period.

LIST OF KEY FREIGHT BROKERAGE MARKET COMPANIES PROFILED

- H. Robinson Worldwide, Inc. (U.S.)

- Total Quality Logistics (TQL) (U.S.)

- XPO, Inc. (U.S.)

- Echo Global Logistics, Inc. (U.S.)

- Worldwide Express, LLC (U.S.)

- RXO, Inc. (U.S.)

- Landstar System Holdings, Inc. (U.S.)

- Hub Group, Inc. (U.S.)

- GlobalTranz Enterprises, LLC (U.S.)

- Allen Lund Company (U.S.)

- Transplace (U.S.)

- Werner Logistics (U.S.)

- BNSF Logistics (U.S.)

- Kuehne + Nagel International AG (Switzerland)

- KLN Logistics Group Limited (China)

KEY INDUSTRY DEVELOPMENTS

- November 2025- C.H. Robinson announced that the company had been named to the 2026 FreightTech 25, an award that recognizes the most innovative companies transforming transportation and logistics through technology.

- November 2025- Freight Technologies launched Zayren, a cutting-edge platform powered by artificial intelligence and machine learning, designed to revolutionize pricing predictions and carrier matching for freight shipments across Mexico and the U.S. This innovative platform also features an AI agent that assists users in efficiently identifying available carriers for specific routes, thereby streamlining and expediting the freight procurement process. The introduction of Zayren aims to enhance operational efficiency in over-the-road freight transportation by automating and accelerating the process of matching shipments with suitable carriers.

- November 2025- Uber Freight expanded its commercial partnership with Better Trucks, a leading last-mile delivery platform, enabling Uber Freight to leverage Better Trucks’ technology and network to significantly enhance its last-mile delivery capabilities and extend coverage to approximately 68% of the U.S. population. This strategic collaboration also includes a targeted investment to integrate sortation and routing technologies, resulting in more efficient end-to-end logistics.

- June 2025- Echo announced that its subsidiary, Roadtex, a national provider of temperature-controlled shipping and supply chain management services, had opened up two new facilities. The company explained that the new facilities were selected for their strategic locations, enabling Roadtex to provide top-of-the-line service in logistics-friendly areas. Additionally, it noted that these facilities feature a 50,000-square-foot expansion, state-of-the-art temperature-controlled technology, and tools that are food-grade and FDA-certified.

- May 2025- Uber Freight launched the industry’s first scaled AI logistics network, powered by a proprietary logistics-specific large language model (LLM). This AI-enabled network, integrated into its transportation management system (TMS), supports real-time decision-making and optimized execution across the freight lifecycle.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.9% from 2025-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Mode of Transportation, By Brokerage Service Type, By Shipper Size, By Industry Vertical, and By Region |

|

By Mode of Transportation |

· Road Freight Brokerage · Rail Freight Brokerage · Ocean & Inland Waterway Freight Brokerage · Air Freight Brokerage |

|

By Brokerage Service Type |

· Spot Freight Brokerage · Contract Freight Brokerage · Intermodal / Multimodal Brokerage · Managed Transportation Services |

|

By Shipper Size |

· Large Enterprises · Mid-Sized Businesses · Small & Medium Enterprises (SMEs) |

|

By Industry Vertical |

· Retail & E-commerce · Manufacturing · Healthcare & Pharmaceuticals · Automotive · Others |

|

By Geography |

· North America (By Mode of Transportation, By Brokerage Service Type, By Shipper Size, By Industry Vertical, and by Country) o U.S. (By Mode of Transportation) o Canada (By Mode of Transportation) o Mexico (By Mode of Transportation) · Europe (By Mode of Transportation, By Brokerage Service Type, By Shipper Size, By Industry Vertical, and by Country) o Germany (By Mode of Transportation) o U.K. (By Mode of Transportation) o France (By Mode of Transportation) o Rest of Europe (By Mode of Transportation) · Asia Pacific (By Mode of Transportation, By Brokerage Service Type, By Shipper Size, By Industry Vertical, and by Country) o China (By Mode of Transportation) o Japan (By Mode of Transportation) o India (By Mode of Transportation) o Rest of Asia Pacific (By Mode of Transportation) · Rest of the World (By Mode of Transportation, By Brokerage Service Type, By Shipper Size, By Industry Vertical, and by Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 66.00 billion in 2025 and is projected to reach USD 110.34 billion by 2034.

In 2025, the market value stood at USD 16.05 billion.

The market is expected to exhibit a CAGR of 5.9% during the forecast period (2026-2034).

The road freight brokerage segment led the market by mode of transportation.

Rapid adoption of digital freight brokerage platforms and TMS solutions is the key factor driving market growth.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us