Frozen Desserts Market Size, Share & Industry Analysis, By Product Type (Ice Cream, Frozen Yogurt, Frozen Custard, Gelato, Sherbet & Sorbet, and Others), By Ingredient Base (Plant-based and Dairy-Based), By Category (Sugar-Free and Conventional), By Distribution Channel (Retail and Foodservice), and Regional Forecast, 2026–2034

(Offer valid till 30th Jun 2026)

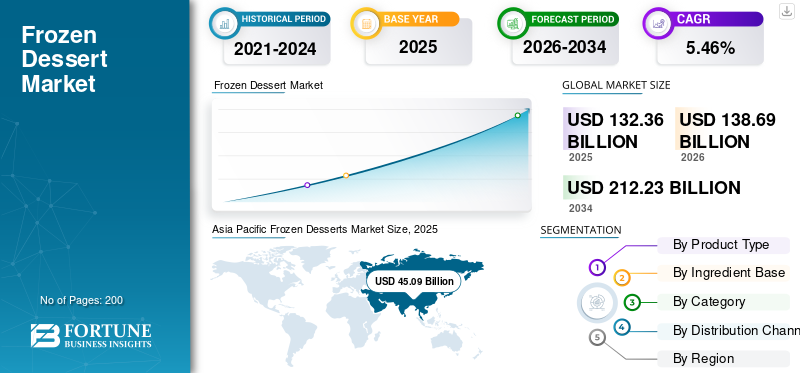

Frozen Dessert Market Overview

The global frozen desserts market size was valued at USD 132.36 billion in 2025. The market is projected to grow from USD 138.69 billion in 2026 to USD 212.23 billion by 2034, exhibiting a CAGR of 5.46% during the forecast period. Asia Pacific dominated the frozen desserts market with a market share of 34.07% in 2025.

Frozen desserts are sweet chilled products that include ice cream, frozen yogurt, sorbet, gelato, frozen custard, dairy-free frozen desserts, and other similar indulgent categories. The market is supported by rising global demand for convenient indulgence, product innovation in flavors and formats, and expanding availability across retail and foodservice channels. Consumer preferences are also shifting toward healthier and more diverse offerings, including low-sugar, functional, vegan, and lactose-free frozen dessert. At the same time, premiumization, artisanal product development, and demand for clean-label ingredients are reshaping competition across the category.

Top market players such as General Mills Inc., Nestle SA, Unilever PLC, Ferrero Group, Dairy Farmers of America, and Dunkin Brands are dominating the market with their diversified product range and geographical presence.

Download Free sample to learn more about this report.

Frozen Desserts Market Trends

Emerging Premiumization and Artisanal Products to Shape the Industry

Premiumization is becoming one of the key frozen dessert market trends as consumers increasingly seek high-quality and more distinctive frozen dessert products. Instead of buying only standard mass offerings, the growing consumer base is showing stronger interest in artisanal gelato, mochi ice cream, premium frozen yogurt, and chef-inspired frozen treats. This shift is supported by rising disposable incomes, especially in urban markets where consumers are more willing to spend on indulgent desserts with better texture, ingredients, and flavor variety. Premium products are also benefiting from stronger product storytelling, such as small-batch production, local ingredients, and clean-label positioning. In retail stores and foodservice outlets, premium frozen desserts help brands enhance value realization even with moderate volume growth. Better cold-chain management and a stronger distribution channel network are also helping premium brands reach more consumers. As a result, premium and artisanal innovation is becoming an important strategy for market expansion and long-term market growth. This trend is expected to remain strong as brands continue to launch products with unique flavors, premium inclusions, and a better eating experience.

- According to the International Dairy Food Association, in 2024, premium and regular ice cream accounted for 80% of the U.S. market, showing the strong position of premium offerings in the frozen dessert category.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Rising Functional, Low-Calorie, and Low-Sugar Products to Drive Market Growth

The demand for functional, low-calorie, and low-sugar frozen dessert products is becoming a major driver of the global market. Many health-conscious consumers now want desserts that provide indulgence while also fitting better into their daily diet goals. This has increased demand for reduced-sugar ice cream, high-protein frozen yogurt, portion-controlled desserts, and products made with alternative sweeteners. Such products are increasingly witnessed as a smarter alternative to traditional ice cream, especially among younger consumers and urban households. The market is also benefiting from growing awareness of calorie intake, sugar reduction, and balanced nutrition. This is encouraging brands to develop products with added health benefits, such as probiotics, higher protein, lower fat, and cleaner labels. As these products become more available across supermarkets, convenience stores, and online distribution channel platforms, consumer adoption is likely to improve further. Therefore, health-led innovation is supporting both product diversification and overall market growth in frozen.

- According to the International Food Information Council, reported in 2025, that 75% of Americans are actively trying to limit or avoid sugar, including 61% trying to limit and 14% trying to avoid it entirely. This strongly supports the demand for lower-sugar frozen desserts.

Market Restraints

High Sugar and Fat Contents Coupled with Intense Competition to Hamper Market Growth

A major restraint in the frozen desserts industry is that many conventional products still contain high levels of sugar, calories, and fat. This can limit purchase frequency, especially among health-conscious consumers who are becoming more selective about indulgent food choices. Although frozen dessert remains popular, regular consumption may be affected when consumers compare them with lighter snacks or healthier substitutes. This makes it difficult for some traditional brands to maintain strong growth without reformulation. At the same time, the market is highly competitive, with multinational brands, private labels, local producers, and artisanal players all competing for shelf space. This intense competition creates pricing pressure and makes differentiation harder, especially in mature retail markets. Frequent product launches, promotional discounts, and flavor innovations also increase pressure on margins. In addition, cold storage and cold supply chain requirements increase operating complexity for producers and retailers. Therefore, nutritional concerns along with rising competition continue to challenge long-term market expansion.

Market Opportunities

Rising Vegan and Lactose-free Products to Change the Industry Growth

Vegan and lactose-free products are creating a strong growth opportunity in the global market. These products are attracting consumers who avoid dairy due to digestive discomfort, lifestyle choices, or a preference for plant-based alternatives. As a result, non-dairy frozen desserts made from oats, almonds, coconuts, and soy are becoming an important alternative to traditional ice cream. This shift is helping brands broaden their consumer base and enter new premium and wellness-focused segments. The opportunity is also supported by rising awareness of lactose intolerance and the wider popularity of plant-based eating. In addition, these products fit well with the current demand for cleaner labels, sustainability, and innovative flavors. As product quality improves, vegan and lactose-free offerings are gaining greater shelf visibility across modern retail and foodservice distribution channels. This supports category diversification, market expansion, and future frozen desserts market growth. In the coming years, plant-based and lactose-free frozen dessert is expected to remain a major area of opportunity for innovation and brand differentiation.

- The National Institute of Diabetes and Digestive and Kidney Diseases states that about 68% of the world’s population has lactose malabsorption, creating a large consumer base for lactose-free frozen dessert.

SEGMENTATION ANALYSIS

By Product Type

Strong Mass-Market Acceptance and Broad Consumer Preference to Help Ice Cream Segment Hold the Highest Share

On the basis of product type, the global market is segmented into ice cream, frozen yogurt, frozen custard, gelato, sherbet & sorbet, and others.

The ice cream segment dominated the market in 2025, valued at USD 80.88 billion, driven by its strong global acceptance, wide flavor availability, an affordable mass-premium range, and deep penetration across retail and foodservice channels. Ice cream remains the most established frozen dessert format in both developed and developing markets as it appeals to a broad consumer base across age groups and income categories. Its strong presence in impulse purchases, take-home tubs, family packs, cones, sticks, and novelty formats supports consistent sales across supermarkets, convenience stores, specialty outlets, and quick-service chains. In addition, manufacturers continue to introduce premium variants, indulgent inclusions, seasonal flavors, and better-for-you formats, which help the segment maintain both volume demand and value growth. The segment also benefits from established cold-chain infrastructure, high brand visibility, and strong product innovation, all of which support its leading market share.

The gelato segment is projected to grow at the CAGR of 7.47% during 2026–2034. Gelato is gaining popularity for its dense texture, rich flavor profile, and premium positioning relative to conventional ice cream. Urban consumers and younger demographics are showing greater interest in café-style desserts, handcrafted offerings, and international dessert formats. Further, helping gelato expand beyond traditional specialty stores into modern retail and foodservice menus.

To know how our report can help streamline your business, Speak to Analyst

By Ingredient Base

Strong Consumer Familiarity and Established Dairy Processing to Help Dairy-Based Products Segment to Hold the Highest Market Share

On the basis of ingredient base, the global market is segmented into dairy-based and plant-based.

The dairy-based segment led the global frozen desserts market share in 2025 at USD 123.36 billion, supported by its long-established consumer acceptance, creamy texture, rich mouthfeel, and wide use across conventional frozen-dessert products. Dairy remains the foundation of most traditional ice cream, frozen yogurt, frozen custard, and premium indulgent dessert formats. The segment benefits from established manufacturing systems, stable formulation performance, and broad availability across global markets. In addition, dairy-based frozen dessert continues to dominate supermarket shelves and foodservice menus as they are strongly associated with indulgence, familiarity, and taste satisfaction. Product innovation in premium dairy desserts, protein-enriched offerings, and low-sugar variants is also helping the segment remain relevant among evolving consumer preferences.

The plant-based segment is expected to grow at the fastest CAGR of 8.38% during the forecast period.

By Category

Established Consumer Base and Wider Product Penetration to Help Conventional Products Segment to Hold the Highest Share of the Market

On the basis of category, the global market is segmented into conventional and sugar-free.

The conventional segment held the largest share of the market in 2025, valued at USD 121.52 billion. Due to its strong mass-market presence, broad product portfolio, and well-established consumer demand across both developed and emerging markets. Conventional frozen desserts remain widely preferred for their familiar taste, indulgent appeal, and lower price sensitivity than niche health-positioned products. The segment includes a wide range of regular ice cream, frozen yogurt, custard, gelato, and novelty items sold across both retail and foodservice channels. Its leading share is also supported by extensive brand competition, frequent flavor launches, and widespread availability across different price points. Since a large share of consumers still prioritizes taste and indulgence over strict nutritional control, conventional frozen dessert continues to account for the majority of market revenue.

The sugar-free segment is projected to grow at the fastest CAGR of 6.67% during the forecast period.

By Distribution Channel

Wide Shelf Presence and Strong Household Purchase Patterns to Help Retail Segment to Hold the Highest Share of the Market

On the basis of distribution channel, the global market is segmented into retail and foodservice.

The retail segment held the largest share of the market in 2025, valued at USD 96.16 billion, owing to the strong availability of frozen dessert products across supermarkets, hypermarkets, convenience stores, specialty stores, and online grocery platforms. Retail remains the leading distribution channel as it serves both routine household consumption and impulse purchases. Take-home packs, single-serve products, multi-packs, and family-size formats are widely distributed through organized retail networks, making frozen desserts easily accessible to consumers. The growth of modern trade, wider freezer availability, and expansion of private-label offerings have further strengthened the retail channel. In addition, seasonal promotions, product variety, and premium shelf placement enhance visibility and drive repeat purchases. These factors continue to make retail the dominant sales channel in the global market.

The foodservice segment is projected to grow at the fastest CAGR of 6.90% during the forecast period. This growth is supported by the increasing popularity of such desserts in cafés, quick-service restaurants, full-service restaurants, dessert parlors, and premium hospitality outlets.

Frozen Desserts Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Frozen Desserts Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific market reached USD 45.09 billion in 2025 and is the leading and fastest-growing region, with a 6.64% CAGR during 2026-2034. The region’s growth is supported by rising disposable incomes, rapid urbanization, and the expansion of modern retail and e-commerce channels. The region benefits from a large young consumer base that is increasingly open to new flavors, premium novelties, and international dessert formats. Growth is also supported by stronger cold-chain investment and better product availability in supermarkets, convenience stores, and digital delivery platforms. Unlike mature Western markets, Asia Pacific still offers strong white-space potential in premiumization, health-positioned frozen dessert, and plant-based alternatives. Urban consumption growth and rising spending on convenience foods continue to support category expansion across major countries.

China Frozen Desserts Market

China was valued at USD 17.30 billion in 2025. China is a leading market in Asia Pacific due to its large urban consumer base, rising premium consumption, and strong appetite for novelty-driven food products. The market in China is supported by demand for premium ice cream, innovative packaging, and visually distinctive products that appeal to younger consumers. The country also benefits from strong adoption of digital commerce, which helps premium and impulse frozen products reach urban households more efficiently. Rising urban incomes are improving consumers’ ability to trade up from basic products to premium, high-quality frozen dessert.

India Frozen Desserts Market

The Indian market size reached USD 7.49 billion in 2025. India is emerging as a high-growth market, supported by its hot climate, expanding dairy base, and rising penetration of affordable impulse products across urban and semi-urban areas. The market is strongly influenced by single-serve formats, sticks, cones, cups, and family packs that cater to price-sensitive, fast-growing mass consumption. India also benefits from a large milk production base, which supports raw material availability for dairy-based frozen dessert. In addition, the rapid growth of e-commerce and quick-commerce is improving the last-mile availability of frozen products, especially in major cities. This is helping frozen-desserts reach consumers beyond traditional kirana and modern trade outlets.

North America

North America market accounted for USD 35.60 billion in 2025 and is projected to grow at a CAGR of 5.13% during 2026–2034. North America remains a major market for frozen-based desserts, supported by strong household penetration, mature cold-chain systems, and broad product availability across supermarkets, convenience stores, club stores, and foodservice outlets. The region benefits from high consumer familiarity with ice cream and other frozen treats, along with strong demand for premium tubs, indulgent novelties, and family take-home packs. Growth is also supported by frequent product innovation in better-for-you, lactose-free, and premium formats, which helps brands expand beyond standard offerings. The region’s developed retail infrastructure and strong freezer capacity across stores support consistent product visibility and impulse purchases. Foodservice also contributes to demand through dessert parlors, quick-service chains, and restaurant menus. According to IDFA, the average American consumes roughly 19 pounds of ice cream per year, highlighting the market’s large and well-established consumer base.

U.S. Frozen Desserts Market

The U.S. market was valued at approximately USD 31.58 billion in 2025 and is expected to expand at a CAGR of 4.87% during the forecast period. The market is supported by a strong mix of retail and out-of-home demand, with manufacturers benefiting from local and regional brand strength and nationwide grocery distribution. Premiumization is especially important in the U.S., where consumers are willing to pay more for indulgent textures, high-quality inclusions, and seasonal flavors. At the same time, the market is witnessing gradual expansion in non-dairy and plant-based frozen dessert, helping brands address changing dietary preferences. The U.S. also has a highly developed manufacturing base and a large number of long-established frozen dessert producers, which support continuous innovation and new product launches. According to IDFA, premium and regular ice cream account for 80% of the market in 2024, and most U.S. manufacturers have a strong presence, reinforcing the country’s mature but innovation-driven market structure.

Europe

Europe market is expected to grow steadily over the forecast period. The market was valued at USD 27.29 billion in 2025 and is expected to expand at a CAGR of 3.83% during 2026-2034. The growth is driven by strong consumer preference for premium indulgence, artisanal formats, and diverse dessert traditions across countries. The region benefits from well-developed retail networks, strong demand for take-home desserts, and a mature café and dessert culture that supports gelato, sorbet, and premium frozen products. Product quality, texture, and ingredient authenticity are especially important in Europe, which supports value growth in premium and artisanal segments. Seasonal demand remains relevant, but year-round consumption is also supported by innovation in grocery retail and foodservice. The region further benefits from established dairy-processing capabilities and a rising interest in plant-based alternatives and reduced-sugar offerings. Eurostat reported that the EU produced 3.3 billion liters of ice cream in 2024, up 2% from 2023, reflecting the region’s large manufacturing base and stable demand.

Germany Frozen Desserts Market

The Germany market accounted for approximately USD 6.56 billion in 2025. Germany is one of Europe’s key markets, supported by its large industrial production base, strong organized retail presence, and broad consumer acceptance of take-home ice cream and impulse formats. The market benefits from efficient distribution through supermarkets and discount stores, which helps both branded and private-label frozen dessert maintains strong volume growth. Germany also shows stable demand for multipacks, tubs, and value-oriented products, while premium and flavor-led innovation continues to support higher-value sales. In addition, consumers increasingly purchase frozen dessert through modern retail formats that offer a wide assortment and year-round availability. Eurostat reported that Germany was the largest ice cream producer in the EU in 2024, with 607 million liters, while industry data indicate that per-capita consumption remained at 8.0 liters in 2024, showing the country’s strong production-consumption balance.

South America and the Middle East & Africa

South America accounted for USD 14.91 billion in 2025, growing at a CAGR of 5.21% during 2026-2034. The region holds an important position in the market, supported by its warm climate, high urban population concentration, and steady everyday demand for affordable indulgent products. The market is shaped by a mix of impulse purchases, family take-home consumption, and a strong preference for fruit-based and locally adapted flavors. Compared with more mature premium-led markets, South America is supported more by accessibility, climate-driven refreshment demand, and rising modern retail penetration in urban centers. The region’s dense urban population base helps such desserts achieve repeat purchase through supermarkets, neighborhood retail, and convenience outlets.

The Middle East & Africa market was valued at USD 9.48 billion in 2025 and is expected to expand at a CAGR of 5.58% during 2026-2034. The Middle East & Africa market is supported by hot weather, a young and expanding urban population, and improved access to modern retail formats. Demand is strongest in urban centers, where consumers have better access to supermarkets, convenience stores, malls, and foodservice outlets that offer ice cream and other frozen-desserts. The region also benefits from rising exposure to international brands, premium novelty formats, and café-led dessert consumption, particularly in higher-income city markets. However, growth differs across countries depending on purchasing power, freezer infrastructure, and cold-chain efficiency.

South Africa Frozen Desserts Market

The South Africa market was valued at approximately USD 2.76 billion in 2025 and is projected to grow at a CAGR of 5.39% from 2026 to 2034. South Africa is one of the key frozen dessert markets in Africa, supported by its relatively developed dairy industry, organized retail presence, and stronger cold-chain and supermarket infrastructure than many other African markets. The country benefits from broad consumer familiarity with dairy products and growing visibility of indulgent packaged foods in modern retail. Such desserts also benefit from convenience-driven consumption in urban areas and from foodservice activity in malls, quick-service outlets, and leisure channels. While affordability remains important, branded dairy desserts and ice cream continue to benefit from stable retail distribution.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Focused on Innovation, Portfolio Expansion, and Strategic Partnerships

The global frozen desserts market is characterized by a few dominant multinational corporations and a large number of regional and local frozen-dessert producers. Leading companies such as General Mills Inc., Nestle SA, Unilever PLC, Ferrero Group, Dairy Farmers of America, and Dunkin' Brands hold a significant share of the global market. These players are focused on product expansion, store openings, geographic expansion, and innovation. Further, it helps key players strengthen their global market share through strategic partnerships.

Key Players in the Frozen Desserts Market

|

Rank |

Company Name |

|

1 |

General Mills Inc. |

|

2 |

Nestle SA |

|

3 |

Unilever PLC |

|

4 |

Ferrero Group |

|

5 |

Dairy Farmers of America |

List of Key Frozen Desserts Companies Profiled

- General Mills Inc. (U.S.)

- Nestle SA (Switzerland)

- Unilever PLC (U.K.)

- Ferrero Group (Italy)

- Dairy Farmers of America (U.S.)

- China Mengniu Dairy Company Limited (China)

- Blue Bell Creameries (U.S.)

- Dunkin Brands (U.S.)

- GS Gelato (U.S.)

- Gelato Italia Ltd., (U.K.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Tillamook County Creamery Association, an Oregon-based dairy cooperative company, launched new ice cream bar products in various flavors, including Cookies & Cream, Mint Chocolate Chip, Tillamook Mudslide, and Vanilla

- February 2026: Amara, an Indian restaurant chain in Bengaluru, launched three premium frozen desserts with regional Indian recipes and traditional halwai collaborations. The new product contains Meetha Paan Sundae, Mangalore Gudbud dessert, and Lonavala Salted Caramel Chikki Sundae.

- July 2025: Unilever Plc, global frozen desserts manufacturer, launched a limited-edition Minecraft ice cream to target gamers under its brand Wall’s. The company partnered with Minecraft to launch an ice cream inspired by the game.

- April 2025: Iceberry, one of Europe’s fastest-growing dessert brands, opened its first flagship store in Saarbrücken, Germany. The company expanded its geographical presence to enhance its business operations.

- April 2025: Lotte Wellfood Co., Ltd., a South Korean company, launched Lotte Krunch, a disruptive 4-layered ice cream bar that fuses Korean innovation and flavors designed to thrill the senses and let consumers “Taste the 4D”.

REPORT COVERAGE

The market report analyzes the market in depth and highlights key aspects, including global market trends, supply chain, market dynamics, prominent companies, investment in research and development, and end-use. In addition, the research report provides insights into the global frozen desserts market and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.46% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Ingredient Base

|

|

|

By Category

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 132.36 billion in 2025 and is anticipated to reach USD 212.23 billion by 2034.

At a CAGR of 5.46%, the global market will grow steadily over the forecast period.

By product type, the ice cream segment led the market.

Asia Pacific held the largest market share in 2025.

The rising functional, low-calorie, and low-sugar products are driving the market growth.

General Mills Inc., Nestle SA, Unilever PLC, Ferrero Group, Dairy Farmers of America, and Dunkin' Brands are the leading companies in the market.

The emerging premiumization and artisanal products are shaping the industry.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us