Fuel Additives Market Size, Share & Industry Analysis, By Type (Deposit Control, Cetane Improvers, Lubricity Improvers, Cold Flow Improvers, Stability Improvers, Octane Improvers, and Corrosion Inhibitors), By Application (Gasoline, Diesel, and Aviation Fuel), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

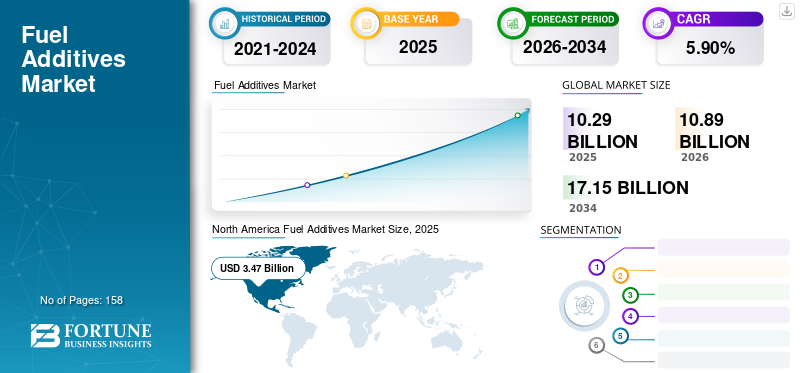

The global fuel additives market size was USD 10.29 billion in 2025 and is projected to grow from USD 10.89 billion in 2026 to USD 17.15 billion by 2034, exhibiting a CAGR of 5.90% during the forecast period. North America dominated the fuel additives market with a market share of 33.80% in 2025. Moreover, the fuel additives in the U.S. is projected to grow significantly, reaching an estimated value of USD 3.73 billion by 2032, driven by its efficacy to reduce and remove harmful deposits restoring fuel economy and power loss.

Due to the rising demand for advanced and improved goods from the car and other end-use sectors, the worldwide market is expected to rise significantly. Stringent restrictions implemented by government businesses are another major factor that is predicted to boost the global market. Furthermore, favorable government regulations and increased awareness about carbon emission reduction will benefit the market.

The automobile industry has seen a decline in demand because of the shutdown of operating activities, during the pandemic. The European vehicle manufacturers and corporations had to reduce their operational output to deal with the falling demand. Renault, for example, halted production at 12 plants in France, affecting over 18,000 workers. The demand for gasoline greatly reduced because of the strict rules and code of conduct enforced by governments to prevent the spread of infection. Due to the strict lockdown and curfew, demand for fuel and its additives decreased.

In the coming years, the middle class and young people will contribute even more to the additives demand. During the COVID-19 epidemic, there was a minor impact on the supply of types for the gasoline additive business. The pandemic and the ensuing lockdown wreaked havoc on the fuel additive industry's whole production and supply chain. However, with the declining impact of the pandemic, fuel use increased in the automotive industry. This resulted in the stabilized additives market.

Download Free sample to learn more about this report.

Global Fuel Additives Market Key Takeaways

Market Size & Forecast:

- 2025 Market Size: USD 10.29 billion

- 2026 Market Size: USD 10.89 billion

- 2034 Forecast Market Size: USD 17.15 billion

- CAGR: 5.90% from 2025–2034

Market Share:

- North America dominated the fuel additives market with a 33.80% share in 2025, driven by rising demand from transportation and power generation sectors and strong regulatory frameworks promoting clean fuel technologies.

- By type, cetane improvers are expected to remain dominant due to their crucial role in enhancing diesel ignition quality and efficiency across key end-use industries.

Key Country Highlights:

- United States: The U.S. fuel additives market is projected to reach USD 3.73 billion by 2032, supported by their effectiveness in restoring engine power, reducing emissions, and complying with Clean Air Act mandates.

- Europe: Growth is driven by stringent emission norms, a strong automotive manufacturing base, and regulatory support from entities such as the Additive Technical Committee (ATC).

- China & India: Rapid industrialization, urbanization, and growing vehicle fleets in China and India are fueling demand for high-performance fuel additives, especially lubricity improvers and deposit control agents.

- Brazil & Mexico: These countries lead the Latin American market, supported by expanding manufacturing sectors and increasing mining activities driving demand for industrial fuels.

- UAE & Qatar: With the resurgence of tourism and major global events such as Expo 2021 and the FIFA World Cup 2022, fuel demand surged, positively impacting the regional additives market.

Fuel Additives Market Trends

Increasing Research and Usage of Ultra-Low Sulfur Diesel to Create New Opportunities

Ultra Low Sulfur Diesel (ULSD) was developed as a response to a number of regulatory activities aimed at reducing diesel fuel emissions. The Clean Air Act was amended in 1990, requiring stringent emission reductions of hydrocarbons, nitrogen oxides, carbon monoxide, particulate matter and other air-polluting emissions. The envisioned effect of lowering sulfur content in diesel has led to numerous positives that can be observed from the huge reductions in harmful emissions. Unfortunately, to achieve reduced sulfur levels, the fuel must first be processed. This processing has led to some less-than-desirable side effects due to the changes it makes to the fuel’s chemistry and reduces the lubricity, thus creating demand for lubricity-improving fuel additives.

Sulfur at an Extremely Low Level Sulfur-free diesel is diesel with a low sulfur content. This is an example of how sophisticated low-emission technologies can potentially reduce harmful gas emissions from diesel combustion. The European government enacted regulations that required the reduction of diesel sulfur content and the implementation of current ULSD criteria. However, in order to retain its performance, the ULSD requires lubricity improvers. One of the trends that is predicted to boost the growth rate of this market is the rising demand for low-sulfur fuel.

Fuel Additives Market Growth Factors

Favorable Regulatory Scenario to Propel Fuel Additives Market Growth

Due to the increased demand for fuel from various industries, the market for fuel additives is likely to rise rapidly. The industry of fuel additives is one that requires a lot of research and development. To address the demand from companies that convert hydrocarbon n fuels to heat energy for diverse applications such as transportation, electricity production, and others, a wide range of products has been produced. According to ATC data, 95 percent of on-road retail fuel is treated with performance additives, accounting for about half of the volume, with the rest going to refineries and other terminals. This assures that the output meets the European government's criteria. Additionally, market expansion will be fueled by increased research and development in the Ultra-Low Sulfur Diesel business.

The market development will be aided by stricter emissions control from autos and refineries. One of the factors promoting growth and development in the product portfolio of fuel additives is growing concerns about air pollution caused by incomplete and complete combustion of hydrocarbons. The Clean Air Act, for example, specifies the use of detergents and deposit control additives to reduce carbon monoxide emissions. Furthermore, a diverse assortment of goods for various types of fuels improves the fuel's performance. Fuel-related difficulties in engines and machinery including fuel efficiency are common, but they can be solved with the application of additives. They are commonly found in refineries, distribution systems, and even storage tanks for various transportation systems and vehicles.

Degrading Quality of Crude Oil to Drive Market

Petroleum oils are quickly photo-oxidized and biodegraded because of the presence of marine microorganisms that utilize it as a carbon source. This occurs mostly at the oil-water interface, producing a wide range of compounds that decrease the quality of the petroleum oil produced. Both of these factors work together to speed up the oxidation process under specific conditions. Fuel additives remove carbonaceous deposits on the walls of combustion chambers. Furthermore, one of the factors diminishing the quality of crude oils is the ongoing mining of crude oil reservoirs to obtain petroleum oil and natural gas. Increasing demand for these additives to preserve quality and meet government standards will drive the market forward.

RESTRAINING FACTORS

Rise in Demand for Alternative Fuels May Hamper Demand

Over the last few years, various forms of clean energy sources have been produced. Concerns about carbon emissions and air pollution have increased the need for sustainable energy sources dramatically. One of the most recent technologies produced for sustainable living is the use of batteries in vehicles and automobiles. Organizations, enterprises, and governments that provide transportation prefer Electric Vehicles (EVs) to practice sustainability and support the use of clean and green energy sources.

Fuel Additives Market Segmentation Analysis

By Type Analysis

Cetane Improvers Segment to Generate High Revenue Due to High Demand from Key End-Use Industries

Based on type, the market is segmented into deposit control, cetane improvers, lubricity improver, cold-flow improver, stability improver, octane improver, and corrosion inhibitors. Cetane number is the parameter used to indicate the ignition properties of a fuel relative to the standard cetane number. Cetane improvers are highly employed in diesel fuel. Its exothermic decomposition lead to fuel reactions which results in the start of combustion at lower temperature.

- Cetane improvers segment is expected to lead the market, contributing 38.75% globally in 2026.

Octane improvers is the major segment. Higher octane number of a fuel indicates higher performance. Increasing demand for octane improvers from refineries due to its cost-effectiveness in order to meet the octane number specifications shall boost its demand. Deposit control additive and stability improvers are in demand attributed to the decreasing quality of crude oil and petroleum oils.

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

Gasoline Segment to Hold a Significant Share Due to Growth in the Automotive Sector

The market is segmented into gasoline, diesel, and aviation fuel in terms of application. The gasoline segment constituted the primary market share in 2023. The growing demand for gasoline fuel supported by the increasing automotive production, is one of the prime reasons driving the market. Besides increasing demand for aviation fuel for commercial application owing to the increasing tourism is expected to drive the market's growth.

The gasoline segment is anticipated to witness a market share of 48.39% in 2026.

REGIONAL INSIGHTS

North America Fuel Additives Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The North America market was valued at USD 3.47 billion in 2025, capturing 33.80% of global revenue, and is estimated to reach USD 3.69 billion in 2026, and is expected to do so during the projected period. Increasing petroleum exploration operations and increasing demand for fuel from a variety of end-user industries, such as transportation and power production, could propel market expansion. The rapidly increasing aerospace and defense sector, as well as numerous U.S. government projects, will fuel regional prosperity. The U.S. market is projected to reach USD 2.55 billion by 2026.

Europe

In 2025, Europe held 29.60% of the global market, reaching a valuation of USD 3.04 billion, and is projected to grow to USD 3.2 billion in 2026. In terms of volume, Europe is likely to rise significantly. The market is likely to be driven by the well-established automotive manufacturing sector and rising demand for passenger automobiles. Furthermore, the presence of organizations such as the Additive Technical Committee (ATC), which supports the expansion of the additive industry, will have an impact on growth. The UK market is projected to reach USD 0.62 billion by 2026, while the German market is projected to reach USD 0.95 billion by 2026.

Asia Pacific

The market in the Asia Pacific reached USD 2.1 billion in 2025, representing 20.40% of total market revenue, and is projected to reach USD 2.26 billion in 2026. In terms of development and industrialization, the Asia Pacific is one of the most prosperous regions. Due to rising demand from countries such as China and India, the fuel additive sector is expected to be a significant driver for the market. Increased efforts by automakers such as Tata, Bajaj, Ashok Leyland, and others to build better automobiles would fuel demand. The Japan market is projected to reach USD 0.44 billion by 2026, the China market is projected to reach USD 0.68 billion by 2026, and the India market is projected to reach USD 0.27 billion by 2026.

To know how our report can help streamline your business, Speak to Analyst

Rest of The World

Brazil, Mexico, Argentina, Columbia and Chile are the major growth countries for the market due to their robust manufacturing sector. Increasing mining activities in Brazil and other Latin American regions are driving the demand for fuels, further supporting the market growth.

In 2025, the Middle East & Africa market stood at USD 0.59 billion, representing 5.70% of global demand, and is projected to grow to USD 0.61 billion in 2026.

Population growth and growing tourism due to the hosting of mega-events are key growth factors for the fuel industry. Increasing tourism and transportation will positively impact market growth. The UAE and Qatar are expected to be lucrative countries for the fuel additive industry as they move on with initiatives to support tourism ahead of the Expo 2021 and FIFA World Cup 2022.

Latin America maintained a strong presence in the global market, reaching USD 1.09 billion in 2025, accounting for 10.60% share, and is expected to reach USD 1.14 billion in 2026.

List of Key Companies in the Fuel Additives Market

Key Companies to Adopt Strategies and Widen their Market Presence

The global market is consolidated in nature, with a few key players governing a major market share. BASF SE, Evonik Industries, Lubrizol Corporation, TotalEnergies, and Dow Inc. are some of the market's key players.

Key manufacturers mainly operate based on the product's pricing strategy. To gain a competitive edge and enhance their market share, several key players are engaged in several strategic partnerships to encourage brand and sales. For instance, in South Korea, BASF SA launched a new diesel additive, which is available through Coupang, an e-commerce company.

LIST OF KEY COMPANIES PROFILED:

- BASF SA (Germany)

- Dow Inc. (U.S.)

- Lubrizol Corporation (U.S.)

- Evonik Industries AG (Germany)

- TotalEnergies (France)

- Clariant (Switzerland)

- Chemtura (U.S.)

- Dorf Ketal Chemicals (India)

- Innospec Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- October 2023 – The Lubrizol Corporation announced a new distribution contract with a leading global distribution partner, IMCD Group, and formulator of ingredients and specialty chemicals as part of its obligation to serve the growing fuel additives and lubricant market in Bangladesh.

- August 2022 – BASF, one of the leading producers of fuel additives, started production of fuel performance additives at its Pudong site in Shanghai, China. The new plant was constructed as a response to the growing regional demand for fuel performance additives and to bring better flexibility and supply security to clients in Asia.

- December 2021 – BASF launched a new multipurpose diesel additive under the brand name KEROPUR-D in South Korea. It is a high performance multipurpose diesel additive that removes deposits from the engine and prevent formation of new deposits.

- November 2021 – Evonik announced the setup of the new oil additive performance test lab in Asia Pacific. This new state-of-art house laboratory facility and testing services for additives and aims to serve customer in Asian region.

- January 2021 - To boost the overall value to consumers and demonstrate their commitment to the ethanol yield business, BASF Enzymes LLC and Innospec Fuel Specialties LLC have entered into a distribution agreement. BASF will distribute DCI-11 Plus ClearTrak – a concentrated corrosion inhibitor – to ethanol producers in the U.S. as part of this agreement.

REPORT COVERAGE

The global fuel additives market research report offers an in-depth analysis of the market and discusses on key aspects including major companies, and products. In addition, the report provides insights on market trends and evaluates key industry developments. In addition to this, the report encompasses various factors that have contributed to the market's growth in recent years.

This report includes historical data & forecasts revenue growth at global, regional, and country levels, and analyzes the industry's latest market dynamics and opportunities.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) and Volume (Kiloton) |

|

Growth Rate |

CAGR of 5.90% from 2026 to 2034 |

|

Segmentation |

By Type

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global fuel additives market size was USD 10.29 billion in 2025 and is projected to reach USD 17.15 billion by 2034, growing at a CAGR of 5.9% during the forecast period.

The fuel additives market is primarily driven by stringent emission regulations, rising demand for cleaner fuels, and increased usage of Ultra-Low Sulfur Diesel (ULSD). The growing automotive and aviation sectors are also key contributors.

Growing at a CAGR of 5.90%, the market will exhibit steady growth during the forecast period (2026-2034).

North America holds the largest market share in the fuel additives industry, accounting for over 33.5% in 2023, driven by high fuel consumption, strict environmental standards, and growing demand from transport and defense sectors.

Key fuel additive types include cetane improvers, deposit control additives, octane improvers, lubricity improvers, cold flow improvers, corrosion inhibitors, and stability improvers, each enhancing fuel performance in specific ways.

While the rise of EVs may gradually reduce demand for gasoline and diesel additives, fuel additives remain essential for sectors like aviation, heavy-duty transport, and power generation, which continue to rely on liquid fuels.

ULSD helps reduce harmful emissions, but it lacks natural lubricity. This creates high demand for lubricity-improving additives to maintain engine efficiency and comply with environmental standards like the Clean Air Act.

The gasoline segment led the market in 2025 due to rising passenger vehicle usage and increasing automotive production, particularly in emerging economies like India and China.

Major players in the global fuel additives market include BASF SE, Lubrizol Corporation, Evonik Industries, Dow Inc., TotalEnergies, and Clariant, all focused on expanding their product portfolios and regional presence through strategic partnerships and R&D.

- 2021-2034

- 2025

- 2021-2024

- 158

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us