Fuel Delivery System Market Size, Share & Industry Analysis, By Component Type (Fuel Injection Components, Fuel Supply & Pressurization Components, Fuel Storage & Transfer Components and Fuel Filtration & Control Components), By Vehicle Type (Two Wheeler, Passenger Cars and Commercial Vehicles), By Distribution Channel (OEM and Aftermarket), By Fuel Type (Petrol/Diesel and Gas), By Injection Technology (Conventional Fuel Injection Systems, Port Fuel Injection Systems (MPFI) and Direct Injection Systems) and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

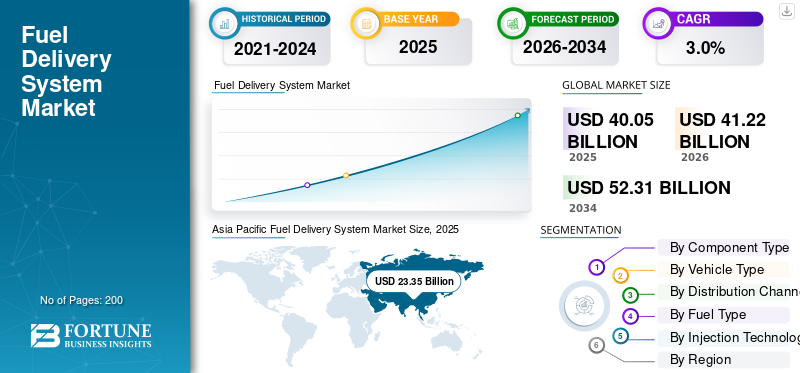

Fuel Delivery System Market Size and Future Outlook

The global fuel delivery system market size was valued at USD 40.05 billion in 2025. The market is projected to grow from USD 41.22 billion in 2026 to USD 52.31 billion by 2034, exhibiting a CAGR of 3.0% during the forecast period. Asia Pacific dominated the fuel delivery system market with a market share of 58.3% in 2025.

Fuel delivery system is a vehicle subsystem that stores, regulates and delivers fuel from the tank to the engine at controlled pressure and quantity to ensure efficient combustion, performance and compliance with emission standards. Key market drivers include sustained global production of internal combustion and hybrid vehicles, rising two-wheeler demand in emerging economies, increasing adoption of high-pressure fuel injection technologies, stricter emissions regulations, growth in alternative fuel vehicles and expanding aftermarket demand driven by an aging global vehicle parc.

Major players such as Robert Bosch GmbH, Denso Corporation, Continental AG, BorgWarner Inc., Hitachi Astemo Ltd., Marelli Holdings Co., Ltd., TI Fluid Systems plc., and Mahle GmbH focus on high-pressure injection systems, lightweight fuel-delivery components, compatibility with alternative fuels, and cost-optimized solutions, while balancing investments between conventional fuel systems and the gradual shift toward electrification.

Download Free sample to learn more about this report.

Fuel Delivery System Market Key Takeaways

- 2025 Market Size: USD 40.05 billion

- 2026 Market Size: USD 41.22 billion

- 2034 Forecast Market Size: USD 52.31 billion

- CAGR: 3.0% from 2026–2034

- Asia Pacific dominated the market with a 58.3% share in 2025.

- Fuel Injection Components segment dominated the market.

- OEM segment held the largest market share.

North America

Witnessing steady growth, supported by a large vehicle parc and rising hybrid adoption.

Asia Pacific

Dominated with a 58.3% share in 2025, driven by strong vehicle production and aftermarket demand.

Europe

Growing steadily, driven by hybrid vehicles and advanced fuel system technologies.

U.S.

The U.S. market was valued at USD 4.21 billion in 2025.

Japan

The Japan market is projected to reach USD 2.79 billion in 2026.

Read More

FUEL DELIVERY SYSTEM MARKET TRENDS

Aftermarket Portfolio Expansion Accelerates Product Demand

Demand for workshop-driven replacement is increasing as vehicle parc ages and fuel systems become more precision-dependent. High-pressure pumps, fuel injectors, rails and filtration components are increasingly replaced as performance expectations tighten and service intervals extend. Suppliers are broadening their original-equipment-quality product lines and bundling digital support to help independent workshops diagnose and fit fuel-delivery parts correctly, improving first-time-fix rates. This trend lifts aftermarket value per vehicle even when new-vehicle growth fluctuates, and it supports steady demand for filters, pumps and injection hardware across petrol/diesel and gas applications.

- In September 2024, Continental announced a major expansion of its aftermarket portfolio, explicitly including high-pressure fuel pumps.

MARKET DYNAMICS

MARKET DRIVER

Stricter Emissions Compliance Raises Fuel System Content Per Vehicle

Tighter emissions limits push OEMs to adopt more precise, higher-pressure fuel metering and cleaner combustion control. This increases demand across injection components, supply/pressurization modules, and filtration/control elements to manage particulate formation, transient operation, and durability over more extended compliance periods. As standards tighten, OEM calibration windows narrow, raising the importance of stable fuel pressure, improved atomization, and cleaner fuel delivery, especially for direct injection and advanced diesel systems. This driver is strongest in regions with aggressive regulatory cycles, and also elevates aftermarket upgrades as vehicles are maintained to meet inspection regimes. These factors collectively drives fuel delivery system market growht.

- In April 2024, the EU adopted Regulation (EU) 2024/1257 (Euro 7), reinforcing emissions-related type-approval requirements.

MARKET RESTRAINTS

Rising BEV Penetration Caps Long-Term OEM Install Growth

As battery-electric vehicles do not use conventional fuel delivery systems, gradually accelerating BEV adoption reduces the addressable share of new-vehicle installations for tanks, fuel lines, pumps, and injectors. While hybrids and plug-in hybrids still require complete fuel-delivery hardware, the shift toward BEVs increasingly limits unit growth in passenger cars, especially in markets with strong policy support and improving total cost of ownership. It does not eliminate demand, but lowers the ceiling for OEM-driven expansion and increases reliance on aftermarket and non-BEV powertrains.

- In July 2025, the IEA reported that electric car sales exceeded 17 million in 2024, accounting for more than 20%.

MARKET OPPORTUNITIES

Hydrogen ICE and Alternative Fuels Create New Injection-System White Space

Alternative fuels open growth opportunities where fuel-delivery systems evolve rather than disappear. For instance, hydrogen internal combustion engines require specialized injectors, controls, and high-integrity supply architectures; gas powertrains need dedicated pressure regulation and delivery hardware. These pathways are particularly relevant for heavy-duty and high-utilization applications where energy density, refueling real time and robust duty-cycle performance matter. For suppliers, the opportunity is to reuse proven ICE manufacturing platforms while developing fuel-specific injection and control modules, creating incremental revenue without relying solely on gasoline/diesel volumes.

- In May 2024, Bosch highlighted its work on specialized low-pressure direct-injection systems and injectors for hydrogen engines at ACT Expo.

MARKET CHALLENGES

Fuel-System Reliability and Quality Risks, Pressures Costs and Reputation

Fuel delivery systems operate under heat, vibration, and very high pressures, making durability and contamination sensitivity critical. Premature pump or injector failures can cause drivability issues, stalls, or safety risks, triggering recalls, warranty spikes and reputational damage. As injection pressures rise and components become more tightly toleranced, quality assurance and supplier process control become more challenging, especially in globalized supply chains and cost-down programs. This challenge also raises compliance exposure as failures can affect emissions performance and on-road conformity, increasing OEM scrutiny and validation burdens.

- In April 2024, Stellantis opened an investigation into low-pressure fuel pump failure that could lead to engine stalls, as documented in an NHTSA recall report chronology.

Download Free sample to learn more about this report.

Segmentation Analysis

By Component Type

Advanced Fuel Metering Enhances Fuel Injection Components Demand

Based on component type, the market is segmented into fuel injection components, fuel supply & pressurization components, fuel storage & transfer components, and fuel filtration & control components.

Fuel injection components dominate the market due to their critical role in fuel atomization, combustion efficiency and emissions control. The increasing adoption of electronically controlled, high-pressure injection systems in passenger cars and commercial vehicles significantly increases per-vehicle content value. Stricter emission norms and engine downsizing further reinforce demand, making injectors and rails indispensable across petrol, diesel, and alternative fuel vehicles.

The fuel filtration & control components segment is projected to grow at a 5.1% CAGR over the forecast period.

By Vehicle Type

High Passenger Vehicle Production Sustains Passenger Car Segment Leadership

Based on vehicle type, the market is segmented into two wheeler, passenger cars, and commercial vehicles.

Passenger cars dominate the fuel delivery system market due to their large global production base and higher adoption of advanced fuel injection technologies such as MPFI and GDI. Emission regulations, fuel efficiency targets and hybridization trends continue to increase fuel system complexity and value per passenger vehicle. Replacement demand from a large installed base of vehicles further strengthens this segment’s dominance across both OEM and aftermarket channels.

The commercial vehicles segment is projected to grow at a CAGR of 3.2% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Distribution Channel

High OEM Fitment Rates Anchor Original Equipment Channel Demand

Based on the distribution channel, the market is segmented into OEM and aftermarket.

The OEM segment held highest fuel delivery system market share due to direct integration of fuel delivery systems during vehicle manufacturing and long-term supply contracts between automakers and Tier-1 suppliers. OEM demand is closely tied to global vehicle production volumes and regulatory compliance requirements that mandate precise, durable fuel-delivery architectures. Increasing system integration and platform standardization further support OEM dominance across vehicle categories and fuel types.

The aftermarket segment is projected to grow at a CAGR of 3.2% over the forecast period.

By Fuel Type

Persistent ICE and Hybrid Volumes Drive Petrol and Diesel Fuel System Demand

Based on fuel type, the market is segmented into petrol/diesel and gas.

Petrol/diesel segment dominates and is also the fastest-growing segment, supported by continued global reliance on internal combustion and hybrid powertrains. While electrification advances, petrol and diesel engines remain prevalent in two-wheelers, passenger cars, and commercial vehicles, especially in emerging markets. Technological upgrades such as direct injection and improved filtration increase system value, sustaining growth across OEM and aftermarket channels. The segment is projected to grow at a CAGR of 3.2% over the forecast period

The gas segment, including CNG and LPG vehicles, is witnessing steady growth driven by lower fuel costs, emission reduction initiatives and rising adoption in public transport and commercial fleets, particularly in Asia Pacific and Latin America, supporting specialized fuel storage and pressure regulation component demand.

By Injection Technology

Port Fuel Injection Maintains Volume Leadership Amid Technology Transition

Based on injection technology, the market is segmented into conventional fuel injection systems, Port Fuel Injection Systems (MPFI), and direct injection systems.

MPFI dominates due to its cost-effectiveness, reliability, and widespread adoption across two-wheelers and passenger cars. It offers a balanced solution between emission compliance and affordability, particularly in cost-sensitive markets transitioning away from carburetors.

The direct injection systems segment is projected to grow at a CAGR of 6.8% over the forecast period, driven by tightening emission norms and demand for higher fuel efficiency and engine performance.

FUEL DELIVERY SYSTEM MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Fuel Delivery System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is the largest and fastest-growing regional market supported by high production of two-wheelers, passenger cars, and commercial vehicles. The region benefits from sustained demand for petrol and diesel powered vehicles, slower electrification in several emerging economies, and rising aftermarket replacement needs. The increasing adoption of fuel injection systems to meet tightening emission norms, combined with strong growth in India and ASEAN markets, continues to drive system volumes and component complexity across OEM and aftermarket channels.

China Fuel Delivery System Market

China remains the largest single-country market with a 57.5% share within Asia Pacific in 2025, in the Asia Pacific, due to its massive vehicle parc and continued production of ICE and hybrid vehicles. While EV adoption is high, fuel delivery systems remain critical for hybrids, commercial vehicles, and the aftermarket, supporting stable demand for advanced injection and filtration components.

Japan Fuel Delivery System Market

Japan’s market is supported by high hybrid vehicle penetration, which still relies on sophisticated fuel injection and pressurization systems. High technology standards, stringent emission compliance, and a large installed base of passenger vehicles drive consistent OEM demand and steady aftermarket replacement volumes. Japan market would be valued at USD 2.79 billion in 2026.

India Fuel Delivery System Market

India is a high-growth market with a 4.6% CAGR, driven by two-wheeler dominance, expanding passenger car ownership, and slow EV penetration. Government-mandated emission upgrades have accelerated the shift to fuel injection systems, significantly increasing demand for pumps, injectors and filtration components across OEM and aftermarket channels.

North America

North America demonstrates steady growth driven by a large existing vehicle parc, continued reliance on petrol-powered passenger cars, and increasing hybrid adoption. While EV penetration is rising, demand for fuel delivery remains strong in light trucks, SUVs and commercial vehicles. High aftermarket spending, longer vehicle lifecycles, and demand for performance-oriented fuel systems help offset slower OEM volume growth and sustain regional market expansion.

U.S. Fuel Delivery System Market

The U.S. market is anchored by strong production of SUVs, pickup trucks, and commercial vehicles, all of which require high-capacity fuel-delivery systems. Hybrid growth and a large aging vehicle fleet support robust aftermarket demand for fuel pumps, injectors, and filtration components despite accelerating EV adoption. The U.S. market was valued at USD 4.21 billion in 2025.

Europe

Europe’s market is growing more slowly due to faster electric vehicle adoption and stringent emissions policies. However, demand persists for advanced fuel systems in hybrid vehicles, commercial fleets and the aftermarket. Increased system complexity, driven by emissions compliance and durability requirements, helps maintain market value even as ICE vehicle volumes gradually decline.

U.K. Fuel Delivery System Market

The U.K. market is supported by hybrid vehicle sales and a sizeable aftermarket as vehicles remain on the road longer. Emission regulations increase fuel system complexity, sustaining demand for precision injection and filtration components despite a steady rise in battery electric vehicle adoption. U.K. market is estimated at USD 1.51 billion in 2026.

Germany Fuel Delivery System Market

Germany remains a key European market valued at USD 1.85 billion in 2025, due to strong OEM manufacturing, export-oriented vehicle production, and advanced powertrain technologies. High adoption of premium passenger cars and hybrids drives demand for high-pressure fuel injection systems, while a large vehicle parc supports steady aftermarket replacement activity.

Rest of the World

The Rest of the World region, including Latin America and the Middle East & Africa, shows resilient growth supported by low electric vehicle penetration, expanding commercial vehicle fleets, and long vehicle lifecycles. Fuel delivery system demand is driven by diesel and gas-powered vehicles, infrastructure development and strong aftermarket replacement, making this region one of the most stable contributors to global market growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Advanced Injection Technologies, Emission Compliance and Global Manufacturing Footprints Shape Market Competitiveness

Advancements in high-pressure fuel injection, optimized emission control, and close collaboration between OEMs and Tier-1 suppliers shape the global market trends. Leading players such as Robert Bosch GmbH, Denso Corporation, Continental AG, BorgWarner Inc., Hitachi Astemo Ltd., Marelli Holdings Co., Ltd., TI Fluid Systems plc., and Mahle GmbH compete through precision injectors, efficient fuel pumps, lightweight fuel tanks and integrated filtration solutions compatible with petrol, diesel and gaseous fuels. Companies enhance competitiveness by investing in next-generation direct-injection systems, expanding manufacturing capacity in Asia Pacific, and aligning product portfolios with hybrid and alternative-fuel powertrains. Strategic partnerships with automakers, localization of production, and cost optimization through modular fuel system architectures remain critical. Suppliers are also strengthening aftermarket offerings and digital diagnostics capabilities to capture lifecycle value, while balancing continued ICE demand with gradual electrification and evolving regulatory requirements worldwide.

LIST OF KEY FUEL DELIVERY SYSTEM COMPANIES PROFILED

- Robert Bosch GmbH (Germany)

- Denso Corporation (Japan)

- Continental AG (Germany)

- BorgWarner Inc. (U.S.)

- Hitachi Astemo Ltd. (Japan)

- Marelli Holdings Co., Ltd. (Japan)

- TI Fluid Systems plc (U.K.)

- Mahle GmbH (Germany)

- Aisin Corporation (Japan)

- Stanadyne LLC (U.S.)

- Cummins Fuel Systems (U.S.)

- Rheinmetall Automotive AG (Germany)

- Keihin Corporation (Japan)

- Parker Hannifin Corporation (U.S.)

- Woodward, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Stanadyne released its new GX Series gasoline direct injection performance fuel pumps, featuring higher flow and high-pressure capability for race and street use. The launch illustrates ongoing product activity around GDI fuel delivery components, where pump performance, pressure capability, and durability are central while also signaling supplier focus on value-rich, high-pressure fuel system subsegments as powertrain mixes evolve.

- July 2025: Cummins launched a new common-rail fuel system for off-highway applications, highlighting higher rail pressures (up to 2,200 bar, with protection up to 2,600 bar) and high-capacity pump flow. The launch underscores continued innovation in fuel injection hardware and controls to improve fuel economy, durability, and emissions outcomes in demanding industrial, construction, and mining duty cycles.

- May 2025: Bosch highlighted the development of hydrogen injectors for commercial and off-road engines, including specialized low-pressure direct injection concepts designed to resist hydrogen embrittlement and operate without external lubrication. This reinforces the fuel-delivery-systems opportunity beyond petrol/diesel shifting R&D toward hydrogen-capable injectors and injection architectures while leveraging combustion-engine manufacturing ecosystems and OEM pilot programs.

- April 2025: ABC Technologies completed its acquisition of TI Fluid Systems. They created TI Automotive by combining the global footprints and fluid-system portfolios of both companies, including fuel tanks and fuel-delivery architectures, as well as thermal and other fluid solutions. The transaction strengthens scale, customer proximity, and vertical integration, key competitive levers for supplying OEM fuel storage, transfer, and line assemblies across ICE and hybrid platforms.

- December 2024: S&S Diesel Motorsport announced the launch of its Ordnance 650 high-pressure fuel pump, engineered for higher output at extreme RPMs for performance and specialty applications. While niche, such launches highlight continued innovation in high-pressure fuel supply hardware, reflecting broader trends toward higher pressures, flow stability, and reliability that also influence mainstream high-performance GDI/diesel segments.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 3.0% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component Type, By Vehicle Type, By Distribution Channel, By Fuel Type, By Injection Technology, and By Region. |

| By Component Type |

|

| By Vehicle Type |

|

| By Distribution Channel |

|

| By Fuel Type |

|

| By Injection Technology |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 40.05 billion in 2025 and is projected to reach USD 52.31 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 23.35 billion.

The market is expected to grow at a CAGR of 3.0% during the forecast period of 2026-2034.

The petrol/ diesel segment led the market in the fuel type segment.

Stricter emissions compliance is driving the market, raising fuel-system content per vehicle.

Key players in the market include Robert Bosch GmbH, Denso Corporation, Continental AG, BorgWarner Inc., Hitachi Astemo Ltd., Marelli Holdings Co., Ltd., TI Fluid Systems plc., and Mahle GmbH.

Asia Pacific accounted for the largest share in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us