Gas Turbine Market Size, Share & Industry Analysis, By Capacity (1-2 MW, 2-5 MW, 5-7.5 MW, 7.5-10 MW, 10-15 MW, 15-20 MW, 20-30 MW, 30-40 MW, 40-100 MW, 100-150 MW, 150-300 MW, and 300+ MW) By Technology (Heavy Duty, Light Industrial, and Aeroderivative), By Cycle (Simple Cycle and Combined Cycle), By Sector (Power Utilities, Oil & Gas, Manufacturing, Aviation, Data Centers, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

Gas Turbine Market Size and Future Outlook

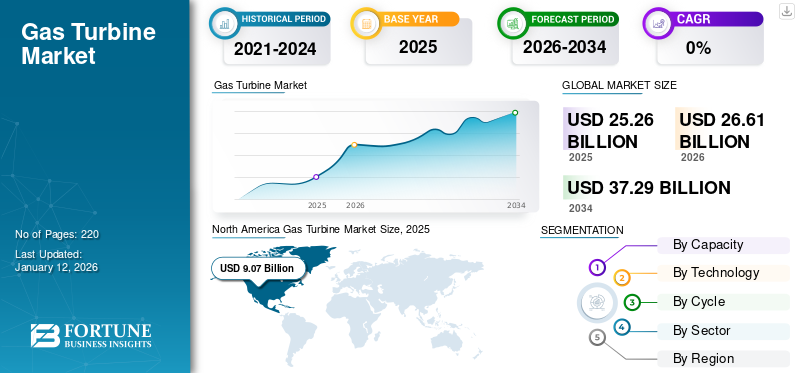

The global gas turbine market size was valued at USD 23.27 billion in 2025. The market is projected to grow from USD 24.70 billion in 2026 to USD 43.50 billion by 2034, exhibiting a CAGR of 7.33% during the forecast period. North America dominated the gas turbine market with a market share of 30.17% in 2025.

Moreover, the North American market is driven by rapid coal-to-gas power generation shifts, aging infrastructure replacement, and the need for fast-ramping, flexible capacity to support renewable energy integration. Abundant, low-cost shale gas supplies and favorable policies, such as the Inflation Reduction Act (IRA), further boost demand.

A gas turbine is a type of continuous, internal combustion engine. It consists of a combustor, an upstream rotating gas compressor, and a downstream turbine on the same shaft as the compressor. There is one more component called turbo fans, which is mainly used to increase efficiency and convert power into either electric or mechanical form. These turbines are very effective and are replacing traditional gas- or oil-fired power plants with combined-cycle power plants that primarily run on natural gas, using such turbines.

- For instance, in December 2025, Mitsubishi Power and Mitsubishi Electric completed functional testing of their next-generation gas turbine control system for thermal power plants. It integrates advanced control and high-speed data processing to deliver stable output, rapid load adjustments to support renewables, and compatibility with diverse fuels, including hydrogen.

GE Vernova holds a premier position in the global market, powering approximately 25% of the world's electricity. Its HA-class technology is the industry's fastest-growing, with over 200 units ordered, and the company expects to sell out production capacity through 2030 due to high demand from data centers and utility-scale projects. The global market is highly consolidated, with the major manufacturers such as GE Vernova, Siemens Energy, Mitsubishi Power, and Solar Turbines controlling the vast majority of the market.

Download Free sample to learn more about this report.

GAS TURBINE MARKET TRENDS

Manufacturers Focusing on Technological Advancements to Drive Market Growth

Manufacturers are focusing on innovations such as advanced cooling technologies, improved materials, and optimized combustion systems, leading to the development of higher efficiency gas turbines. This translates to lower fuel consumption and operating costs, making them more competitive.

Combined Cycle Power Plants (CCPPs) featuring both gas and steam turbines are continually improving, achieving ultra-high efficiency levels exceeding 60%. Developments in lean pre-mixing and dry low-NOx (DLN) combustors are minimizing nitrogen oxide (NOx) emissions. Research on hydrogen-fueled turbines of gas holds immense potential for near-zero emissions power generation, aligning with stricter environmental regulations. Carbon Capture and Storage (CCS) technologies are being explored to capture and store CO2 emissions from such turbines, further reducing their environmental impact.

- In June 2025, GE Vernova and IHI will launch a large-scale combustion test facility at IHI’s Aioi Works in Japan to develop combustors enabling 100% ammonia firing in F-class gas-turbines by 2030. Full-scale prototype tests begin in summer 2025, advancing carbon-free power with no net CO2 emissions.

Advancements in materials and diagnostics are enhancing the reliability and durability of gas turbines, leading to longer operating lifespans and reduced downtime. New designs and control systems are making such turbines more flexible, allowing them to adapt to the fluctuating electricity demand and integrate with renewable energy sources.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Electricity Demand Across the World Augmented Market Growth

Electricity demand is rapidly increasing worldwide due to urbanization and infrastructure development. Industrialization is also growing across developing countries. In many countries, various smart building and smart city projects have been initiated, further increasing electricity demand. To meet electricity demand, the public and private sectors are increasing power plant capacity by installing new plants or expanding existing ones.

- According to the International Energy Agency, Global power demand surged in 2024 due to the expansion of electrification, marking the new Age of Electricity. The 2025-2027 forecast shows that all additional demand is met by low-emissions technologies such as renewables and nuclear, sustaining clean energy growth amid rising demand.

Such projects primarily involve installing gas-driven turbines, as they are efficient and less harmful. Governments have also implemented stringent emission norms, provoking companies to adopt gas-based turbines on a large scale. Thus, this factor is expected to drive gas turbine market growth in the coming years.

MARKET RESTRAINTS

Volatility in Natural Gas Prices to Hamper Market Growth

Natural gas prices are affected by disruptions in supply. Geopolitical tensions are a disruptive factor that creates uncertainty about the availability or demand for gas. This can cause higher gas price volatility. The cost of gas in the U.S. has fallen drastically due to shale gas exploitation, but elsewhere in the world, the price remains relatively high. Most countries in the Middle East account for a significant share of the region's natural gas reserves. It is a highly unstable region due to political and cultural issues. significantly. Thus, the costs of gas also dropped, which negatively impacted market growth.

MARKET OPPORTUNITIES

Technological Advancements in Semiconductors to Offer Growth Opportunities

Technological advancements in semiconductors are a major driver of growth opportunities in the solid-state devices market. These advancements, particularly in wide-bandgap semiconductors such as silicon carbide (SiC) and gallium nitride (GaN), offer several key benefits that significantly enhance the performance, efficiency, and cost-effectiveness of solid-state devices. SiC and GaN semiconductors can handle higher power densities in smaller form factors. This enables the design of more compact and lightweight solid-state devices. The ability to deliver more power in a smaller size is crucial for applications such as EVs, 5G infrastructure, and consumer electronics.

MARKET CHALLENGES

Rapid Expansion of Renewable Energy Sources May Create Challenges for Market Growth

The market faces several structural and market-driven challenges. One major challenge is the rapid expansion of renewable energy sources such as solar and wind, which are reducing the reliance on conventional thermal power generation and limiting new gas turbine installations in some regions. Closely linked to this is the global decarbonization push, with stricter emissions regulations and net-zero commitments pressuring utilities and industries to transition to low-carbon alternatives.

Another key challenge is the high capital and maintenance costs associated with such turbine systems, particularly for advanced combined-cycle plants, which can deter investments in price-sensitive markets. Market growth is also affected by volatility in natural gas prices and supply chain disruptions, which impact project economics and operational planning. Additionally, long-term project development timelines and complex permitting processes slow deployment.

Segmentation Analysis

By Technology

Technology Segment Held Largest Market Share Due to High Adaptability

Based on technology, the market is segmented into heavy duty, light industrial, and aeroderivative.

The aeroderivative segment is expected to lead the market in 2026, with a 42.80% market share prized for their agility, quick startup times, and adaptability across power generation and industrial uses.

Meanwhile, the light industrial segment surged ahead as the one of the fastest growing area with CAGR of 7.46%, fueled by rising demand for efficient, compact solutions in manufacturing, oil and gas operations, and distributed energy systems globally.

By Capacity

150-300 MW Segment Held Largest Market Share Due to High Demand from Power Industry

Based on capacity, the market is segmented into 1-2 MW, 2-5 MW, 5-7.5 MW, 7.5-10 MW, 10-15 MW, 15-20 MW, 20-30 MW, 30-40 MW, 40-100 MW, 100-150 MW, 150-300 MW, and 300+ MW.

The 150-300 MW segment dominates the market in 2026, with a 19.84% market share. These capacity turbines are primarily used in the power generation industry, as the industry has been shifting to reduce harmful gas emissions in response to environmental safety concerns.

The small-capacity industrial turbine segments of 1-2 MW, 2-5 MW, 5-7.5 MW, 7.5-10 MW, 10-15 MW, and 15-20 MW are leading due to the ready availability of gas. The small-capacity gas-driven turbines with capacities of 1-2 MW are expected to grow at a significant rate, with a CAGR of 9.79%. These turbines are very useful as they are modular and can operate on two fuels. Such CHP and cogeneration plants are widely installed in residential, commercial, and industrial segments worldwide.

By Cycle

Combined Cycle Segment Holds Significant Market Share Due to High Demand from Power Plants

Based on the cycle, the market is segmented into simple-cycle and combined-cycle.

The combined cycle segment holds a 70.01% market share in 2026. The growth is mainly attributed to effective waste heat utilization, proximity to the environment, and operational efficiency. The demand for gas turbines is increasing in power plants. The combined-cycle plants are built in phases: first, simple-cycle plants are constructed, and then they are gradually converted to combined-cycle.

The simple cycle segment is mostly to grow at a CAGR of 6.71% in this market during the forecast period. Simple-cycle plants are cost-effective compared to combined-cycle gas turbine plants, and they are easy to construct and maintain.

By Sector

To know how our report can help streamline your business, Speak to Analyst

Power Utility Sector is to hold Highest Market Share Due to Rise in Coal Turbine Replacement Activities

Based on sector, the market is segmented into power utilities, oil & gas, manufacturing, aviation, data centers, and others.

The power utility segment is anticipated to dominate the global market in 2026, with a 46.94% market share. The growing focus on replacing conventional steam and coal-fired turbines with gas-fired turbines in various power-generating stations is intensifying. These turbines provide higher efficiency in power generation than traditional power plants.

The oil & gas segment is expected to grow significantly, with a CAGR of 6.40% over the forecast period. Demand and consumption of oil & gas are rapidly increasing worldwide. Exploration and production activities are increasing significantly worldwide. Natural gas is used primarily as a fuel in this turbine.

Gas Turbine Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Gas Turbine Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America market value reached USD 7.02 billion by 2025, securing its position as the largest market. The urgent need for grid modernization primarily drives the market, the replacement of aging 1960s/70s infrastructure, and the necessity for fast-ramping, flexible capacity to support increasing renewable energy integration. Surging electricity demand from data centers, AI, and industrial growth, combined with low-cost natural gas, accelerates this demand.

U.S. Gas Turbine Market

Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market was valued at around USD 5.91 billion in 2025, accounting for roughly 25.66% of the global market. Low natural gas prices, tightening environmental regulations, and the requirement for efficient, quick-start, small-to-mid-sized peaking plants are also fueling rapid adoption.

Asia Pacific

Asia Pacific held the second largest share in 2025, at USD 5.58 billion, and also led in 2026, with USD 6.02 billion.

The market is primarily driven by surging electricity demand, rapid urbanization, and a strategic shift from coal to cleaner, natural gas-fired power plants. Key factors include significant infrastructure investments in China and India, the need for flexible, high-efficiency power solutions, and environmental regulations pushing for lower carbon emissions.

China Gas Turbine Market

The China market in 2025 is estimated to be around USD 1.28 Billion, accounting for roughly 5.52% of the global market revenues, driven by rapid industrialization, large-scale urbanization, and strict government mandates to reduce coal dependency, leading to increased adoption of natural gas-based, high-efficiency, reliable power generation. Key demand drivers include expanding infrastructure, rising energy demand, and increased domestic natural gas production.

India Gas Turbine Market

India’s market is projected to be one of the largest worldwide, with 2025 revenues estimated at around USD 0.20 billion, representing approximately 2.68% of the global market.

Europe

Europe is projected to grow at 6.40% over the coming years, the second-highest among all regions, and reached a valuation of USD 5.40 billion in 2025, driven by the need for grid flexibility to balance intermittent renewable energy, the replacement of aging power infrastructure, and decarbonization efforts.

Germany Gas Turbine Market

The German market size in 2025 was valued to be around USD 0.56 billion. It is projected to reach USD 0.60 billion by 2026, representing approximately 2.41% of the global revenues.

Latin America

Latin America is projected to grow at 4.57% over the coming years and reached a valuation of USD 1.35 billion in 2025, driven by rising industrialization (especially in Brazil and Argentina), the urgent need to upgrade aging power infrastructure, and the shift toward cleaner, natural gas-fired generation over coal.

Brazil Gas Turbine Market

The German market in 2025 was recorded to be around USD 0.92 billion. It is projected to reach USD 0.97 billion by 2026, representing approximately 1.16% of the global revenues.

Middle East & Africa

The Middle East & Africa is projected to grow at 5.28% over the coming years and reached a valuation of USD 4.21 billion in 2025. Key drivers include massive infrastructure development, the integration of high-efficiency, hydrogen-ready, and Combined-Cycle Gas Turbines (CCGT), alongside demand for desalination plants in the region.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Participants Are Concentrating On New Contracts to Boost Market Share

The market is highly uneven, with several large-scale players worldwide. These include a group of major companies having a wider geographical presence. Several companies are pursuing organic and inorganic growth strategies to solidify their market positions worldwide. The companies are focusing on new contracts to increase their gas turbine market share. In January 2026, Mitsubishi Power secured a major contract to supply hydrogen-ready M701JAC gas-turbines for Qatar's Facility E IWPP near Doha, adding 2.4 GW of power and 495,000 tons/day desalinated water, 20% of national grid capacity. The 2028 project supports Qatar's National Vision 2030 decarbonization efforts, with long-term service to ensure reliability. Such developments are expected to fuel market growth over the forecast period.

LIST OF KEY GAS TURBINE COMPANIES PROFILED

- GE (U.S.)

- Siemens (Germany)

- Mitsubishi Power (Japan)

- Ansaldo Energia (Italy)

- Solar Turbines (U.S.)

- Kawasaki Heavy Industries, Ltd. (Japan)

- Doosan Heavy Industries & Construction (South Korea)

- Bharat Heavy Electrical Limited (India)

- OPRA Turbines (Netherlands)

- Rolls-Royce (U.K.)

- Vericor Power Systems LLC (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Russia launched its first domestically produced high-capacity GTD-110M gas turbine at Udarnaya power station. Built by Rostec, it's lighter and more compact than foreign models such as Siemens/GE, boosting plant capacity to 560 MW amid sanctions that curb imports.

- July 2025: GE Vernova and Crusoe announced a major deal for 29 LM2500XPRESS aeroderivative gas turbine packages to power Crusoe's AI data centers, providing nearly 1GW of flexible electricity. The units, equipped with SCR emissions tech, offer rapid deployment, high reliability, and 90% lower NOx emissions than traditional engines. This builds on prior orders from December 2024 and June 2025.

- March 2023: GE’s latest high-efficiency turbine of gas will cover less natural gas, which will be implemented in the 435-megawatt Tallawarra power station in Sydney, Australia.

- January 2023: Mitsubishi Power accepts an order for H-25 Gas Turbine for Taiwan’s Chang Chun petrochemical project; additionally, conversion of the cogeneration system at the Miaoli Factory in Miaoli City to a High Power-Efficient Gas-Fired System to Decrease CO2 Emissions.

- January 2022: GE Digital’s Autonomous Tuning Speed up the Energy Transition with Machine Learning and Artificial Intelligence, which will reduce harmful emissions and fuel consumption for gas turbines. Additionally, this will cost lower machinery and operational flexibility.

REPORT COVERAGE

The global gas turbine market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and industry trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market report also encompasses a detailed competitive landscape with information on the market share and profiles of key market players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.33% from 2026-2034 |

| Unit | Value (USD Billion), Volume (MW) |

| Segmentation | By Capacity, Technology, Cycle, Sector, and Region |

| By Capacity |

|

| By Technology |

|

| By Cycle |

|

| By Sector |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 23.27 billion in 2025 and is projected to reach USD 43.50 billion by 2034.

In 2025, the market value stood at USD 5.58 billion.

The market is expected to exhibit a CAGR of 7.33% during the forecast period.

The power utilities led the sector segment.

The rising electricity demand across the world augmented growth in the market.

GE, Siemens, Mitsubishi Power, Ansaldo Energia, Solar Turbines, Siemens, Mitsubishi Power, Ansaldo Energia, and Solar Turbines are some of the prominent players.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us