Genitourinary Drugs Market Size, Share & Industry Analysis By Drug Class (Androgen Receptor Pathway Inhibitors, GnRH Agonists/GnRH Antagonists, and Others), By Disease Indication (Prostate Cancer, Benign Prostatic Hyperplasia (BPH), Erectile Dysfunction, and Others), By Age Group (Pediatric, Adult, and others), By Type (Branded and Generics), By Route of Administration (Oral, Vaginal, Injectable/Parenteral, Topical/Transdermal, and Others), By Gender (Male and Female), By Distribution Channel (Hospital Pharmacies, Drug Stores & Retail Pharmacies, and Others), and Regional Forecast, 2026-2034

Genitourinary Drugs Market Size and Future Outlook

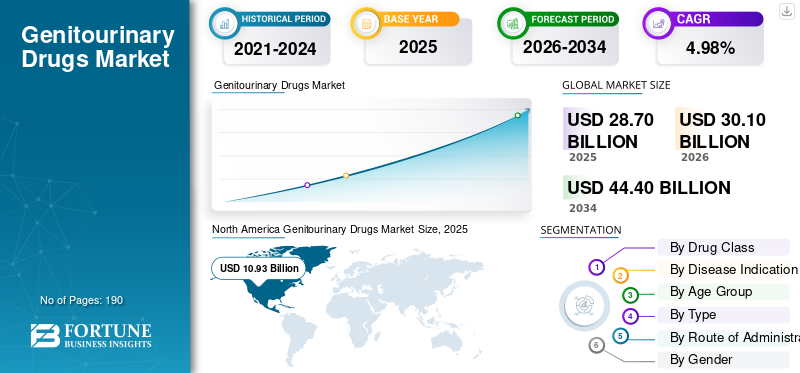

The global genitourinary drugs market size was valued at USD 28.70 billion in 2025. The market is projected to grow from USD 30.10 billion in 2026 to USD 44.40 billion by 2034, exhibiting a CAGR of 4.98% during the forecast period. North America dominated the genitourinary drugs market with a market share of 38.08% in 2025.

The global market includes medicines used to treat disorders affecting the urinary tract and reproductive system, such as overactive bladder, benign prostatic hyperplasia, urinary incontinence, erectile dysfunction, urinary tract infections, and genitourinary cancers, among others. The market is witnessing growth amid rising burdens from these conditions, an aging population, changing lifestyle patterns, and improved disease diagnosis across major countries. Furthermore, pharmaceutical companies are introducing more targeted therapies, combination regimens, and specialty treatments, as well as regulatory approvals for innovative medicines, which are expanding treatment options and improving patient outcomes.

- For instance, in September 2025, Johnson & Johnson received the U.S. FDA approval for INLEXZO (gemcitabine intravesical system) for certain patients with BCG-unresponsive high-risk non-muscle-invasive bladder cancer. The offering is designed to deliver cancer medication locally and continuously into the bladder. Such developments strengthen innovation in bladder cancer treatment and show how the market is shifting toward more targeted and differentiated genitourinary therapies.

Furthermore, major players, such as Astellas Pharma Inc., Pfizer Inc., Merck & Co., Inc., and Johnson & Johnson, are engaging in strategic partnerships to strengthen their market positions.

Download Free sample to learn more about this report.

Genitourinary Drugs Market Key Takeaways

- 2025 Market Size: USD 28.70 billion

- 2026 Market Size: USD 30.10 billion

- 2034 Forecast Market Size: USD 44.40 billion

- CAGR: 4.98% from 2026–2034

- North America dominated the genitourinary drugs market with a 38.08% share in 2025.

- The beta-3 adrenergic agonists segment is projected to grow at a CAGR of 7.18% during the forecast period.

- The bladder/urothelial cancer segment is expected to grow at a CAGR of 6.49% during the forecast period.

North America

North America maintained its leading position with a market value of USD 10.93 billion in 2025.

Asia Pacific

Asia Pacific is estimated to reach a market value of USD 7.49 billion in 2026.

Europe

Europe is projected to reach a market value of USD 8.25 billion in 2026.

U.S.

The U.S. market is estimated to reach USD 10.60 billion in 2026.

Japan

The Japan market is estimated to reach USD 1.51 billion in 2026.

Read More

GENITOURINARY DRUGS MARKET TRENDS

Expansion of Specialty Drugs for Urologic Oncology Treatment is a Prominent Trend

A prominent global trend in the market is the shift toward specialty drugs in urologic oncology, such as bladder, prostate, and kidney cancers. These cancer types often require more targeted, disease-specific treatment than traditional therapies can provide. As more patients are diagnosed at different stages of disease, the product demand is increasing for therapies that can improve survival, delay progression, and offer better outcomes in difficult-to-treat settings. Furthermore, pharmaceutical companies are investing more in antibody-drug conjugates, immunotherapy combinations, and localized drug-delivery platforms for urologic cancers. As a result, specialty drugs are becoming an important market trend, expanding treatment options and changing the standard of care in genitourinary oncology.

- For instance, in March 2026, Johnson & Johnson announced results for Erda-iDRS, an investigational intravesical drug-releasing system with erdafitinib for certain patients with non-muscle-invasive bladder cancer. The product is stated to have the potential to become the first targeted treatment for early-stage bladder cancer, underscoring the market's shift toward more specialized and differentiated urologic oncology therapies.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Prevalence of Urinary and Reproductive System Disorders to Drive Market Growth

One of the key factors driving the global genitourinary drugs market growth is increasing urinary and reproductive system disorders affecting a larger patient pool, especially in the adult and elderly populations. As the number of patients with benign prostatic hyperplasia, lower urinary tract symptoms, bladder disorders, and related genitourinary conditions increases, the need for long-term drug therapy also rises. This increases the demand for both routine symptom-management drugs and advanced therapies for more severe or progressive disease. As a result, pharmaceutical companies are expanding their portfolios, focusing on regulatory approval in this area, and healthcare providers are using more drug-based treatment options to manage the growing disease burden.

- For instance, in June 2025, Bayer AG received approval from the U.S. FDA for NUBEQA (darolutamide) for patients with metastatic hormone-sensitive prostate cancer, with or without chemotherapy. The development expanded treatment access in a large and growing prostate cancer patient population, showing how rising disease burden is creating stronger demand for advanced genitourinary therapies.

MARKET RESTRAINTS

Side Effects and Poor Tolerability of Genitourinary Drugs to Limit Long-Term Treatment Adoption

One of the key factors restricting the global market growth is the risk of side effects, which reduces patient comfort and long-term adherence. When patients experience dry mouth, constipation, cognitive burden, dizziness, sexual side effects, or other tolerability issues, they are more likely to delay treatment, switch drugs, or stop therapy altogether. This lowers real-world treatment persistence and limits the full commercial potential of marketed therapies, especially in conditions that need long-duration drug use. As a result, poor tolerability remains an important barrier to market growth, as it affects both prescription continuity and patient confidence in the therapy.

- For instance, in September 2023, NIH published a review titled ‘Patient and Clinician Challenges with Anticholinergic Step Therapy in the Treatment of Overactive Bladder: A Narrative Review’ that reported anticholinergic therapies are limited by poor tolerability and anticholinergic-related side effects. An overactive bladder is one of the major treatment areas within genitourinary care and lower adherence directly reduces therapy duration and revenue capture for drug manufacturers.

MARKET OPPORTUNITIES

Development of Novel Drug-Delivery Systems to Create New Growth Opportunities

The market is experiencing strong growth opportunities in novel drug-delivery systems as traditional genitourinary treatments often face limitations such as repeated procedures, short drug exposure times, or poor patient convenience. When companies develop sustained-release, localized, or intravesical delivery platforms, they can improve the duration of drug exposure at the disease site and reduce the need for more invasive treatment approaches. This creates an opportunity for better patient compliance, broader physician adoption, and stronger product differentiation in high-value urology and bladder cancer segments. As a result, novel drug-delivery technologies are opening new commercial opportunities by improving both treatment effectiveness and patient experience.

- For instance, in June 2025, UroGen Pharma Ltd. reported new data on UGN-102, an investigational intravesical mitomycin formulation for recurrent low-grade intermediate-risk non-muscle-invasive bladder cancer. The product uses its proprietary RTGel sustained-release hydrogel technology to allow longer exposure of bladder tissue to the drug and support treatment by non-surgical means. Such development showcases how innovative drug-delivery systems can create a new treatment pathway in genitourinary care.

MARKET CHALLENGES

Pricing and Reimbursement Barriers to Slow Wider Adoption of Advanced Genitourinary Therapies

The market faces a major challenge as many advanced genitourinary drugs, especially in bladder and prostate cancer, are expensive and require strong reimbursement support before they can reach a wider patient pool. When treatment costs are high, payers become more selective, health technology assessment reviews take longer, and access can vary sharply across countries or even regions. This slows the commercial uptake as doctors may have fewer funding options and patients may not receive timely access even when the clinical need is high. As a result, pricing and reimbursement pressure remain an important market challenge, particularly for novel oncology therapies that are clinically valuable but financially difficult for health systems to absorb at scale.

- For instance, in September 2025, a published article reported that Ireland’s HSE did not fund Lu-PSMA-617 for prostate cancer, and described the case as showing the tension between access and affordability for new cancer treatments. Such instances highlight that even promising genitourinary therapies can face delayed uptake when reimbursement systems are not aligned with pricing expectations.

Segmentation Analysis

By Drug Class

Large Outpatient Treatment Base to Propel PDE5 Inhibitors Segment Growth

Based on drug class, the market is categorized into androgen receptor pathway inhibitors, GnRH agonists/GnRH antagonists, PDE5 inhibitors, alpha blockers, antimuscarinics/anticholinergics, beta-3 adrenergic agonists, and others.

Among these, the PDE5 inhibitors segment accounted for the largest share in 2025. Erectile dysfunction remains one of the most visible and frequently treated genitourinary conditions, and this drug class has been widely accepted due to its strong efficacy, convenience, and familiarity among prescribers and patients for such an indication. These therapies are also supported by established brands, multiple formulations, and broad use in adult male patients, which keeps prescription demand high. Furthermore, PDE5 inhibitors benefit from a large outpatient treatment base, which supports repeat use and a strong retail-market presence. As a result, the segment continued to dominate.

- For instance, in January 2025, Opella announced that the U.S. FDA lifted the clinical hold on its planned actual use trial to support the switch of Cialis (tadalafil) from prescription to over-the-counter use. Such continued commercial confidence in one of the best-known PDE5 inhibitor brands highlights how the class is moving toward broader consumer access and stronger mainstream adoption.

The beta-3 adrenergic agonists segment is expected to grow at a CAGR of 7.18% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

Increasing Prevalence of Benign Prostatic Hyperplasia (BPH) in Males to Drive the Dominance of the Segment

Based on disease indication, the market is segmented into prostate cancer, benign prostatic hyperplasia (BPH), erectile dysfunction, overactive bladder (OAB), urinary tract infections (UTIs), bladder/urothelial cancer, and others.

Among these, the benign prostatic hyperplasia (BPH) segment accounted for the largest share in 2025. It affects a very large male patient population, especially in middle-aged and older adults, and it often requires long-term symptom management. Patients commonly need ongoing treatment for urinary frequency, a weak stream, urgency, and related lower urinary tract symptoms, creating steady prescription demand over time. These factors encourage key players to invest in new product launches and research and development.

- For instance, in December 2024, Sumitomo Pharma America announced the U.S. FDA approval of GEMTESA (vibegron) for men with overactive bladder symptoms receiving pharmacological therapy for BPH.

The bladder/urothelial cancer segment is projected to grow at a CAGR of 6.49% during the forecast period.

By Age Group

Greater Patient Pool in the Adults Segment to Boost Segmental Growth

Based on age group, the market is segmented into pediatric, adult, and geriatric.

In 2025, the adults segment accounted for the largest genitourinary drugs market share as most genitourinary disorders, including erectile dysfunction, BPH, bladder dysfunction, and prostate-related diseases, are mainly diagnosed and treated in adult populations. The adult segment also offers the broadest treatment options across both chronic urology conditions and oncology-related genitourinary therapies. As a result, the adult segment dominated the market as it represents the broadest and most commercially active patient base in the market and it has seen innovative product launches.

- For instance, in June 2025, Bayer AG announced that the U.S. FDA approved NUBEQA (darolutamide) for adult patients with metastatic castration-sensitive prostate cancer. Such leading genitourinary therapies are designed for adult patient populations, especially in prostate cancer, which continues to drive the global product demand.

The geriatric segment is projected to grow at a CAGR of 5.78% during the forecast period.

By Type

Novel Mechanisms Offered by Branded Therapies to Elevate their Demand and Propel Segment Growth

Based on type, the market is segmented into branded and generics.

In 2025, the branded drugs segment accounted for the largest share. The genitourinary market includes many specialty, oncology, and differentiated therapies that still command premium pricing and stronger physician preference. In areas such as bladder cancer and advanced prostate cancer, branded products often lead as they offer novel mechanisms, label expansion opportunities, and stronger clinical differentiation. These therapies also benefit from company-led commercialization, patient-support programs, and greater promotional visibility. As a result, branded products continued to dominate given that much of the market’s value remains concentrated in innovative, high-priced therapies rather than in volume-driven generics.

- For instance, in September 2025, Johnson & Johnson announced the U.S. FDA approval of INLEXZO (gemcitabine intravesical system) for certain patients with bladder cancer. These developments showcase how branded innovation continues to capture value in the market through differentiated products that generics do not easily replicate.

The generics segment is projected to grow at a CAGR of 4.36% during the forecast period.

By Route of Administration

Ease of Administration of Oral Therapies to Support the Segment’s Dominance

Based on the route of administration, the market is segmented into oral, vaginal, injectable/parenteral, topical/transdermal, and others.

The oral segment accounted for the highest share in 2025 as they are easier to prescribe, simpler for patients to use, and more suitable for long-term outpatient management than injectable or procedure-based therapies. Many high-volume genitourinary conditions are treated with oral medicines, which supports wider physician acceptance and better patient convenience. Oral therapies also reduce hospital dependence and fit well into chronic treatment settings, helping them reach a broader patient base. Underscoring these advantages, key companies are developing oral therapies for genitourinary disorders.

- For instance, in March 2024, Sumitomo Pharma announced the availability of ORGOVYX (relugolix) in Canada and identified it as the first and only oral androgen deprivation therapy treatment for men with advanced prostate cancer.

The others segment is projected to grow at a CAGR of 7.42% over the analysis period.

By Gender

High Volume of Genitourinary Conditions to Boost Male Segmental Growth

Based on gender, the market is segmented into male and female.

In 2025, the male segment accounted for the largest share as several of the highest-value and highest-volume genitourinary conditions are male-specific, especially erectile dysfunction, BPH, and prostate cancer. These diseases create sustained treatment demand across both chronic symptom-management drugs and advanced oncology therapies. In addition, male-focused genitourinary conditions are strongly linked to aging, which further expands the treated population as demographics shift upward. As a result, the male segment dominated as it captures the largest concentration of commercially important indications within the market.

- For instance, in May 2025, Astellas collaborated with Pfizer to announce long-term overall survival data for XTANDI in metastatic hormone-sensitive prostate cancer. The companies noted that more than one million patients have been treated with XTANDI globally.

The female segment is projected to grow at a CAGR of 5.41% during the forecast period.

By Distribution Channel

Consumer Familiarity of Drug Stores and Retail Pharmacies to Drive Segmental Dominance

Based on distribution channel, the market is segmented into hospital pharmacies, drug stores & retail pharmacies, online pharmacies, and specialty pharmacies.

The drug stores & retail pharmacies segment accounted for the largest share given that many leading genitourinary therapies are prescribed and refilled in outpatient settings rather than being administered only in hospitals. Conditions such as erectile dysfunction, BPH, and overactive bladder usually require convenient access, repeat dispensing, and neighborhood availability, all of which support retail-channel dominance. Retail pharmacies also benefit from consumer familiarity, physician prescribing patterns, and the growing shift toward self-managed or long-term chronic therapy. As a result, this channel dominated as it is the most practical and accessible route for a large share of routine genitourinary prescriptions.

- For instance, in September 2025, Boots announced the launch of its own-brand Sildenafil Orodispersible Film 50mg, which it described as the U.K.’s first rapidly dissolving oral film for the treatment of erectile dysfunction. Such instances show how retail pharmacy chains are dispensing genitourinary therapies and actively broadening consumer access and product availability within this market.

The online pharmacies segment is projected to grow at a CAGR of 7.53% over the analysis period.

Genitourinary Drugs Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Genitourinary Drugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 with a value of USD 9.83 billion and maintained its leading position in 2025, reaching a valuation of USD 10.93 billion. The market is growing in North America as the region has a high diagnosis rate for prostate cancer, BPH, overactive bladder, and erectile dysfunction, which keeps the treatment demand strong. Furthermore, robust access to branded drugs, specialty therapies, and advanced oncology treatments supports higher prescription value, driving product innovation and broad reimbursement coverage.

U.S. Genitourinary Drugs Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated to touch around USD 10.60 billion in 2026, accounting for roughly 35.23% of the global market.

Europe

Europe is projected to grow at a CAGR of 4.59% over the forecast period, the second-highest among all regions, and reach a valuation of USD 8.25 billion in 2026. The market is growing in Europe given that the region has a large aging population, which increases the burden of chronic genitourinary disorders and urologic cancers.

U.K. Genitourinary Drugs Market

The U.K. market is estimated to reach around USD 1.64 billion in 2026, representing roughly 5.46% of the global market.

Germany Genitourinary Drugs Market

The Germany market is projected to reach approximately USD 1.89 billion in 2026, equivalent to around 6.29% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 7.49 billion in 2026 and secure the position of the third-largest region in the market. The market is growing in the Asia Pacific as the patient pool is large and diagnosis rates are improving as healthcare access expands across major countries.

Japan Genitourinary Drugs Market

The Japan market is estimated to touch around USD 1.51 billion in 2026, accounting for approximately 5.03% of the global market.

China Genitourinary Drugs Market

The China market is projected to be one of the largest worldwide, with 2026 revenues estimated to reach around USD 2.64 billion, representing approximately 8.76% of global sales.

India Genitourinary Drugs Market

The India market is estimated to reach around USD 1.11 billion in 2026, accounting for roughly 3.68% of global revenue.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The market in Latin America is estimated to reach a valuation of USD 1.66 billion. The market in Latin America is growing due to increased awareness of chronic urology conditions and genitourinary cancers improves, leading to higher diagnosis and treatment rates. In the Middle East & Africa, the GCC is set to reach USD 0.56 billion in 2026.

South Africa Genitourinary Drugs Market

The South Africa market is projected to reach approximately USD 0.26 billion in 2026, accounting for roughly 0.86% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Emphasis of Key Players toward Regulatory Approvals to Propel Market Progress

The global genitourinary drugs market is semi-consolidated, with companies such as Astellas Pharma Inc., Pfizer Inc., Merck & Co., Inc., Johnson & Johnson, Bayer AG, and AstraZeneca PLC accounting for a significant share. These companies hold strong positions due to their established presence in major therapeutic areas, including prostate cancer, bladder cancer, overactive bladder, and other chronic urology conditions, and a wide commercial reach across key healthcare markets. Ongoing strategic partnerships, product launches, label expansions, and regulatory approvals are further helping these companies strengthen their market presence and improve their share in the sector.

- For instance, in September 2025, Johnson & Johnson received the U.S. FDA approval for INLEXZO (gemcitabine intravesical system), indicated for certain patients with BCG-unresponsive high-risk non-muscle-invasive bladder cancer. The development introduced a differentiated branded therapy. It also supports the value share of branded products in the market.

Other notable participants in the global market include Sumitomo Pharma Co., Ltd., Organon & Co., and Ferring Pharmaceuticals. These companies are expected to focus on strategic collaborations, regional licensing agreements, expansion of their women’s health portfolio, bladder cancer innovation, and new product launches to strengthen their market positions during the forecast period. The rest of the market remains fragmented among other multinational companies, regional manufacturers, and generic suppliers serving high-volume chronic genitourinary therapy segments.

LIST OF KEY GENITOURINARY DRUGS COMPANIES PROFILED

- Astellas Pharma Inc. (Japan)

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Bayer AG (Germany)

- AstraZeneca PLC (U.K.)

- Sumitomo Pharma Co., Ltd. (Japan)

- Organon & Co. (U.S.)

- Ferring Pharmaceuticals (Switzerland)

- Endo, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: UroGen Pharma Ltd. reported that the commercial launch of ZUSDURI for adults with recurrent low-grade, intermediate-risk non-muscle-invasive bladder cancer is on track.

- February 2026: Organon collaborated with Sebela Pharmaceuticals for exclusive rights to MIUDELLA, a hormone-free copper intrauterine device (IUD) contraceptive.

- November 2025: Pfizer Inc. received approval from the U.S. FDA for PADCEV (enfortumab vedotin-ejfv), a Nectin-4 directed antibody-drug conjugate (ADC), in combination with Keytruda QLEX (pembrolizumab and berahyaluronidase alfa-pmph) or the PD-1 inhibitor Keytruda (pembrolizumab), as neoadjuvant treatment. The drug can then be continued after cystectomy (surgery) as adjuvant treatment for adult patients with MIBC (muscle-invasive bladder cancer) who are not eligible for cisplatin-containing chemotherapy.

- June 2025: Knight Therapeutics Inc. collaborated with Sumitomo Pharma America Inc. to commercialize MYFEMBREE (relugolix/estradiol/norethindrone acetate), ORGOVYX (relugolix), and vibegron in Canada.

- March 2025: GSK plc secured U.S. FDA approval for Blujepa (gepotidacin) for the treatment of pediatric patients (≥12 years, ≥40 kg) and female adults (≥40 kg) with uncomplicated urinary tract infections (uUTIs) caused due to susceptible microorganisms.

REPORT COVERAGE

The report provides a comprehensive analysis of the global genitourinary drugs market. It covers detailed market analysis across drug class, disease indication, age group, type, route of administration, gender, and distribution channel. It examines the demand for therapies used in benign prostatic hyperplasia, erectile dysfunction, overactive bladder, urinary tract infections, bladder and prostate cancers, and other genitourinary disorders, while also assessing the role of PDE5 inhibitors, androgen receptor pathway inhibitors, alpha blockers, antimuscarinics, beta-3 adrenergic agonists, and other drug classes in current treatment practice. The study further provides regional insights across key geographies, competitive landscape analysis, company profiling, recent developments, and evaluation of the major factors driving, restraining, and shaping future opportunities in the market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.98% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Drug Class, Disease Indication, Age Group, Type, Route of Administration, Gender, Distribution Channel, and Region |

| By Drug Class |

|

| By Disease Indication |

|

| By Age Group |

|

| By Type |

|

| By Route of Administration |

|

| By Gender |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 28.70 billion in 2025 and is projected to reach USD 44.40 billion by 2034.

In 2025, the market value stood at USD 10.93 billion.

The market is expected to grow at a CAGR of 4.98% over the forecast period of 2026-2034.

By drug class, the PDE5 inhibitors segment led the market in 2025.

The high prevalence of urinary and reproductive system disorders is a key factor fueling market growth.

Astellas Pharma Inc., Pfizer Inc., Merck & Co., Inc., Johnson & Johnson, and Bayer AG are the major players in the global market.

North America dominated the market in 2025 in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us