Fiberglass Market Size, Share & Industry Analysis, By Glass Type (E-Glass and Specialty), By Product (Glass Wool, Yarn, Roving, Chopped Strands, and Others), By Application (Transportation, Building & Construction, Electrical & Electronics, Pipe & Tank, Consumer Goods, Wind Energy, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

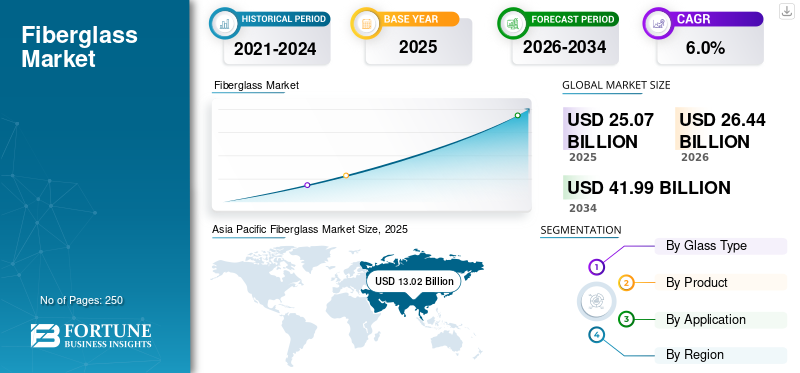

Fiberglass Market Size & Future Outlook

The global fiberglass market size was valued at USD 25.07 billion in 2025. The market is projected to grow from USD 26.44 billion in 2026 to USD 41.99 billion by 2034, exhibiting a CAGR of 6.0% during the forecast period. Asia Pacific dominated the fiberglass market with a market share of 51.93% in 2025.

Fiberglass, also known as glass fiber, is a reinforced material made from fine strands of glass combined with resin matrices to form composites. It offers high tensile strength, lightweight properties, corrosion resistance, and thermal insulation, making it well-suited to transportation, construction, energy, and industrial applications. Fiberglass is categorized by glass type, including E-glass and specialty glass variants, each serving distinct performance requirements. The material is further processed into products such as yarn, roving, glass wool, and chopped strands. The growing demand for lightweight materials in the automotive and wind energy sectors is a significant driver of market growth. Additionally, infrastructure expansion and energy-efficient building standards further drive consumption. As industries increasingly prioritize durability and performance efficiency, fiberglass continues to play a critical role in composite materials, reinforcing its strategic importance in the global materials market. The major companies operating in the market are The Fiberglass Company, Shandong Fiberglass Group Corp., and Nippon Electric Glass Co., Ltd.

Download Free sample to learn more about this report.

Fiberglass Market Trends

Rising Demand for Lightweight Composites is a Prominent Market Trend

As environmental concerns grow, many industries are demanding lightweight composites to reduce their carbon footprint. In addition, an increase in smart infrastructure construction is driving the application of this material to control overheating and maintain room temperature in buildings. Therefore, several government agencies globally are investing more in the sustainable development of energy-efficient buildings, thereby increasing demand for the product.

Additionally, numerous renovation and remodeling projects are replacing traditional building materials with fiberglass for greater structural stability and better insulation. Apart from that, significant growth in the renewable energy sector has increased demand for the product in manufacturing various electrical devices for using safe, clean energy sources, such as tidal and wind power.

The growing automotive sector, along with rising demand for fuel-efficient vehicles, is driving increased use of the product in panel assemblies, body panels, wheelhouse assemblies, front fascia, and battery boxes. It is also replacing metal-based substitutes for pipes, tanks, and subsea systems in the water treatment and oil & gas sectors. These factors will continue to drive the global fiberglass market growth in the coming years.

Market Dynamics

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Product Demand from Transportation Industry to Drive Market Growth

Glass fibers have been utilized in the transportation sector as reinforcement since mass-produced pultrusion approaches were first documented. A matrix of liquid resin was combined with continuous reinforcement fabric strands to enhance the material's structural integrity, further enabling the glass wool to be formed into high-strength structural shapes. This material offers a superior strength-to-weight ratio for the transport sector, thanks to its improved resistance to many corrosive media.

For transport applications, this material is ideal as it is lightweight, solid, rigid, offers excellent protection from external elements, can be shaped into any size & form, and has an excellent finish. It is used in the automobile and wind energy industries owing to its low weight, high strength-to-weight ratio, and excellent longevity.

Moreover, structural reinforcements and crash protection systems are now increasingly being manufactured using reinforced polymer materials. For instance, Chrysler, a vehicle brand owned by Stellantis, has been using fiberglass products to build a supporting beam for a blow-molded plastic fuel tank owing to the material’s advanced thermal properties and corrosion resistance.

Due to the need for impact-resistant and lightweight materials, the marine and automotive sectors are using fiberglass on a large scale. To reduce carbon dioxide emissions, stringent regulations have been imposed on the automotive industry. It has encouraged the sector to introduce lightweight, fuel-efficient vehicles to reduce greenhouse gas emissions. This composite material is also widely used as a substitute for aluminum and steel in the automotive industry to produce lightweight cars. This is expected to drive market growth during the forecast period.

MARKET RESTRAINTS

Emission of Harmful Substances into Environment May Obstruct Market Growth

Fiberglass processing consumes substantial energy and resources. For each kilogram of molten glass, 1 kg of carbon dioxide (CO2) is released into the environment, in addition to nitrogen oxide (NOx), sulfur dioxide (SO2), chlorine, fluoride, Volatile Organic Compounds (VOCs), and particles.

In comparison, for every ton of molten glass, 17 GJ of electricity is consumed. Some 25% of this fiber is sent to landfills at the end of its life, amounting to around 250,000 tons/year in Europe. This results in a significant emission of harmful substances into the environment and a decrease in landfill space. Due to its characteristics, Glass Fiber Reinforced Polymer (GFRP) is widely accepted. It is neither fusible nor soluble due to the polymeric portion's thermoset nature, thereby preventing direct remelting or remolding. These fabrics typically contain a significant quantity of inorganic fillers in addition to glass and polymeric matrix, so they are difficult to recycle. GFRPs are typically sent to landfills or incinerators, where they have a detrimental environmental impact.

Thus, for the sustainable growth of the industry, the development of proper recycling technologies for glass wool and other composite materials is becoming crucial.

MARKET OPPORTUNITIES

Growing Demand for Lightweight Solutions in Numerous Industries to Create Lucrative Opportunities

Fiberglass has garnered significant attention in recent years due to its unique properties and versatile applications across various industries. This composite material, made from fine glass fibers, is renowned for its lightweight nature, durability, and resistance to corrosion, making it an ideal choice for numerous applications.

As the global demand for lightweight construction materials rises, the fiberglass market is poised for substantial growth. Key sectors, such as automotive, aerospace, marine, and construction industries are increasingly recognizing the advantages of fiberglass, such as enhanced performance and fuel efficiency. In the automotive industry, for instance, manufacturers are increasingly replacing traditional metal components with fiberglass to reduce weight and improve fuel economy. The shift toward electric vehicles further amplifies this demand as lightweight materials are crucial for optimal performance.

In the aerospace sector, the need for advanced composite materials is rising as they are critical for improving aircraft efficiency and performance. Fiberglass is being increasingly used in the manufacturing of aircraft components due to strict regulations on weight reduction and fuel consumption. Similarly, the marine industry employs fiberglass in boat building, thanks to its ability to withstand harsh marine environments.

The construction industry is also experiencing a surge in the demand for fiberglass composite materials to be used in both structural and non-structural applications. With the increasing emphasis on sustainable construction practices and the development of energy-efficient structures, fiberglass products are becoming a preferred choice. Moreover, emerging markets in Asia Pacific, particularly China and India, present lucrative opportunities due to rapid industrialization and urbanization. As infrastructure projects ramp up, the demand for fiberglass materials is set to grow.

MARKET CHALLENGES

Challenges With Innovation and Sustainability Compliance to Hinder Market Growth

The market, integral to various industries, such as automotive, construction, and aerospace, has been witnessing robust growth due to the material’s lightweight and high-strength properties. However, this sector faces several challenges that could impede its future expansion.

The primary challenge is the fluctuation in raw material prices. Fiberglass is produced from silica, resins, and other additives, and price volatility in these raw materials can significantly impact production costs. Manufacturers often find it difficult to pass these costs onto consumers without risking market share, leading to tighter profit margins.

Additionally, environmental concerns surrounding fiberglass production and disposal pose a significant hurdle. The manufacturing process is energy-intensive, contributing to greenhouse gas emissions. Furthermore, fiberglass products are not biodegradable, raising issues related to waste management and environmental sustainability. Increasing regulatory scrutiny and consumer demand for eco-friendly materials challenge the industry to innovate and develop more sustainable practices.

Fiberglass Market Segmentation Analysis

By Glass Type

E-Glass Segment to Gain Momentum Due to Its Increasing Applications in Various End-use Industries

By glass type, the market is segmented into e-glass and specialty.

The e-glass segment held the largest global fiberglass market share and is likely to maintain this position during the forecast period as well. E-glass, commonly referred to as electrical glass, is manufactured using oxides of magnesium, silicon, calcium, aluminum, and boron. It offers strong resistance to vibration and abrasion while maintaining excellent flexibility and lightweight properties. Due to these characteristics, E-glass fabric is widely used in marine, aerospace, and various industrial applications. It is considered the industry benchmark as it provides an optimal balance between cost and performance. Additionally, the growing adoption of environmentally friendly boron-free variants is expected to support segment growth during the forecast period.

The specialty segment includes S-glass, ECR-glass, D-glass, AR-glass, and other advanced variants. The segment is growing at a CAGR of 6.1% during the forecast period. These glasses are used in building & construction, renewable energy, electronics, and healthcare applications due to their improved strength, high electrical conductivity, and acid corrosion resistance. The aforementioned end-use industries are expected to drive demand during the forecast period.

By Product

Glass Wool Segment Dominated Market Owing to Rising Demand for Insulation Materials

Based on product, the market is categorized into glass wool, yarn, roving, chopped strands, and others.

In 2025, the glass wool segment held the largest market share. As a thermal and acoustic insulation material, glass wool is mainly used in indoor applications. Most commonly, it is applied under pitched roofs, on wooden floors, or on inner walls. Glass wool is deployed inside the house as once it comes into contact with a damp area, it quickly loses its insulation value.

Chopped strands are used globally as reinforcement materials in conjunction with high-performance resins, with a certain substance added to Fiber Reinforced Plastics (FRPs) and Fiber Reinforced Thermoplastics (FRTPs) for electronics and automobiles. The segment is growing at a CAGR of 6.0% during the forecast period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Building & Construction Segment to Hold Leading Market Share Owing to Rising Demand for Insulation Materials

Based on application, the market is divided into transportation, building & construction, electrical & electronics, pipe & tank, consumer goods, wind energy, and others.

The building & construction segment accounted for the largest share in terms of volume in 2025. Rising construction activities in emerging economies, along with the increasing adoption of insulation materials in residential and commercial buildings, are expected to support market growth. Furthermore, growing demand for lightweight aircraft and fuel-efficient vehicles is projected to boost product consumption. The ongoing shift from heavy metal components to lightweight composite materials across the automotive, aerospace, and marine industries is expected to drive significant growth during the forecast period.

The transportation segment growth is driven by stringent environmental regulations such as carbon emission targets in Europe and Corporate Average Fuel Economy (CAFE) standards in the U.S. These regulations have compelled OEMs to incorporate lightweight materials to reduce vehicle weight and improve fuel efficiency. The segment is growing at a CAGR of 5.3% during the forecast period.

FIBERGLASS MARKET REGIONAL OUTLOOK

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Fiberglass Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the largest share of the market in 2025. Strong growth in the construction sectors of developing countries such as China, India, Indonesia, and Thailand is expected to support continued market expansion. The increasing product use in electrical and thermal insulation applications, combined with rapid industrialization, is further strengthening regional demand. Additionally, rising government investments in infrastructure and large-scale construction projects are contributing to higher consumption of fiberglass products. These factors collectively position Asia Pacific as the leading region in the global market.

China Fiberglass Market

Based on Asia Pacific’s strong contribution and China’s large-scale manufacturing footprint, the China market was valued at USD 6.86 billion in 2025, accounting for approximately 27.4% of global revenues. Expansion is supported by large-scale industrialization, strong wind energy installations, and high production of composite materials for transportation and construction.

To know how our report can help streamline your business, Speak to Analyst

India Fiberglass Market

India’s market was valued at around USD 1.98 billion in 2025. Growth is driven by rapid infrastructure development, expanding residential construction, and rising demand for insulation materials in urban housing projects.

North America

The residential sector in North America is expected to support market growth significantly. Low interest rates on housing loans and rising wages have increased demand for residential units, leading to higher construction activity across the U.S. and Canada. After a slowdown, housing development rebounded from 2021 onward, supported by sustained infrastructure and smart city investments. In the building and construction industry, glass fiber is widely used for insulation, cladding, surface coatings, and roofing materials, further strengthening regional demand.

U.S. Fiberglass Market

The U.S. market was valued at USD 5.16 billion in 2025, representing approximately 20.6% of global revenues. Growth is fueled by infrastructure modernization programs and increasing adoption of lightweight composites in the automotive and renewable energy sectors.

Europe

In Europe, the mature consumer electronics industry benefits from advanced technological connectivity. The growing adoption of smart homes and smart workplaces is increasing demand for products such as smart televisions, refrigerators, and air conditioning systems, thereby supporting market expansion.

Germany Fiberglass Market

Germany’s market reached a valuation of about USD 1.32 billion in 2025, accounting for about 5.3% of global revenues. Demand is driven by advanced automotive manufacturing and a rising focus on energy-efficient building insulation solutions.

U.K. Fiberglass Market

The U.K. market was valued at USD 0.69 billion in 2025, accounting for roughly 2.7% of global revenues. Growth is supported by smart building initiatives and steady demand from the electrical and consumer electronics industries.

Latin America and Middle East & Africa

In the Middle East & Africa, rising construction activities and tourism-driven infrastructure development are boosting housing investments. Government initiatives such as Saudi Arabia’s white land tax and expanding wind energy projects are further supporting demand. Meanwhile, in Latin America, the growing use of corrosion-resistant glass fiber pipes and tanks in oil disposal and industrial applications is driving regional market growth.

GCC Fiberglass Market

The GCC market accounted for around USD 0.19 billion in 2025, about 0.8% of regional revenues. Expansion is driven by large-scale construction projects, tourism-related infrastructure development, and increasing investment in renewable energy installations.

Competitive Landscape

Key Industry Players

Key Players are Adopting Business Expansion Strategies to Maintain their Market Position

The global market is fragmented, with prominent players including LANXESS, Owens Corning, 3B – The Fiberglass Company, Shandong Fiberglass Group Corp., and Nippon Electric Glass Co., Ltd. Companies are actively expanding their operations and strengthening production capabilities to enhance competitiveness and reduce the threat posed by new entrants.

Market participants compete intensely at both international and regional levels, leveraging strong distribution networks, regulatory expertise, and established supplier relationships. To reinforce their market positions, leading manufacturers are entering into supply agreements, acquisitions, and strategic partnerships. These initiatives enable companies to broaden their geographic footprint, enhance product portfolios, and strengthen their presence in the global industry.

LIST OF KEY FIBERGLASS COMPANIES PROFILED IN REPORT

- LANXESS (Germany)

- Owens Corning (U.S.)

- 3B - The Fibreglass Company (Belgium)

- Shandong Fiberglass Group Corp (China)

- Nippon Electric Glass Co., Ltd (Japan)

- Taishan Fiberglass Inc.(CTG) (China)

- Chongqing Polycomp International Corp. (China)

- Johns Manville (U.S.)

- Saint-Gobain Vetrotex (France)

- China Jushi Co., Ltd. (China)

- Taiwan Glass Industry Corporation (Taiwan)

- PFG Fiber Glass Corporation (Taiwan)

- Asahi Fiber Glass Co., Ltd. (Japan)

- Knauf Insulation (U.S.)

- KCC Corporation (South Korea)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Knauf Insulation expanded its Performance+ portfolio with pipe and pipe & tank fiberglass insulation lines, described as the only formaldehyde-free fiberglass insulation available in those categories and the first to be both Asthma & Allergy Friendly® Certified and Verified Healthier Air, signalling further extension of its fiberglass platform into industrial applications.

- February 2025: Johns Manville announced plans for a new Climate Pro blown-in fiberglass insulation production line in Winder, Georgia, with construction to begin in 2026 and operations targeted for mid-2027, signalling added fiberglass-insulation capacity and stronger service reach across the East Coast and Central U.S. markets.

- February 2025: China Jushi launched construction of the second phase of its Huai’an carbon-neutral intelligent manufacturing base, featuring a 100,000-ton electronic-grade glass fiber production line and a 500MW supporting wind power facility, signalling further capacity additions in electronic-grade glass fiber and faster progress toward carbon-neutral, digitally integrated glass fiber manufacturing.

- November 2024: Johns Manville launched a new microfiberglass production line at its Wertheim, Germany, site for Evalith microfiberglass nonwovens used in indoor air filtration, creating 12 jobs and incorporating sustainability technologies such as advanced exhaust, water, and heat recovery systems, signalling capacity expansion for high-performance filtration-grade fiberglass media.

- November 2024: Johns Manville released Insul-SHIELD Black, a fiberglass insulation board with a black core, designed for theaters, music studios, and dark ride applications, signalling product-line expansion in specialty fiberglass insulation for acoustic and light-control end uses.

- September 2024: China Jushi launched product 390, described by the company as its best glass roving for wind turbine blades, made from its E9 glass formulation with a modulus above 100 GPa, signalling continued movement into higher-performance fiberglass solutions for ultra-large wind blade applications.

- September 2024: Knauf Insulation launched its Performance+ residential thermal and acoustical fiberglass insulation portfolio, with the range positioned as CERTIFIED Asthma & Allergy Friendly® and Verified Healthier Air, further premiumizing its residential fiberglass offering.

REPORT COVERAGE

The fiberglass market report provides a detailed analysis of the market and focuses on crucial aspects, such as leading companies, products, and end-use industries. Also, the report offers insights into market trends and highlights vital industry developments. In addition to the factors mentioned above, the report encompasses various factors that have contributed to the market's growth in recent years. This report includes historical data & forecasts revenue growth at global, regional, and country levels and analyzes the industry's latest dynamics and opportunities.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.0% from 2026 to 2034 |

| Unit | Value (USD Billion) and Volume (Kiloton) |

| Segmentation | By Glass Type, Product, Application, and Region |

| By Glass Type |

|

| By Product |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 25.07 billion in 2025 and is projected to reach USD 41.99 billion by 2034.

In 2025, the Asia Pacific’s market size stood at USD 13.02 billion.

Recording a CAGR of 6.0%, the market will exhibit steady growth during the forecast period of 2026-2034.

In terms of application, the building & construction segment is the leading market segment.

The growing product penetration in the automotive industry will aid the market growth.

LANXESS, Owens Corning, 3B - The Fiberglass Company, Shandong Fiberglass Group Corp, and Nippon Electric Glass Co., Ltd. are the major players in the global market.

Asia Pacific held the largest market share in 2025.

The product’s superior properties and rising demand from the automotive industry are expected to foster its adoption.

- 2021-2034

- 2025

- 2021-2024

- 250

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us