Grid Connected PV Systems Market Size, Share & Industry Analysis, By Component (Solar Modules, Power Conditioning Unit, Grid Connection Equipment, Inverters, and Others), By Technology (Crystalline Silicon, Thin-Film, and Others), By End User (Residential, Commercial, Utility, and Industrial), Regional Forecast, 2026-2034

Grid Connected PV Systems Market Size and Future Outlook

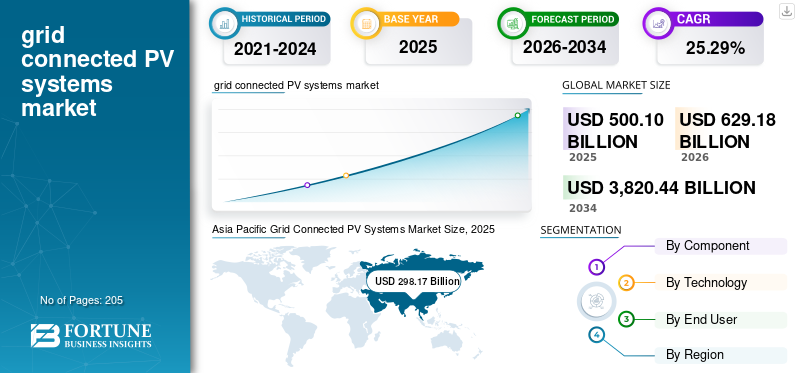

The global grid connected PV systems market size was valued at USD 500.10 billion in 2025. The market is projected to grow from USD 629.18 billion in 2026 to USD 3,820.44 billion by 2034, exhibiting a CAGR of 25.29% during the forecast period. Asia Pacific dominated the grid connected pv systems market with a market share of 59.62% in 2025.

Grid-connected PV systems are solar power systems that are directly connected to the utility grid, enabling the supply of generated solar energy to both on-site consumption and the wider power network. Grid connected photovoltaic PV systems are witnessing strong growth due to rapid capacity additions and favorable policy frameworks across major economies. The integration of solar into national grids is becoming central to energy transition strategies, driving the market share.

According to the International Energy Agency, in January 2025, global solar PV capacity additions exceeded ~550 GW in 2024, marking the highest annual increase on record. Additionally, the IRENA Renewable Capacity Statistics 2024 reported that solar PV accounted for over 70% of total renewable capacity additions in 2023. Government initiatives such as the EU’s REPowerEU plan and India’s 500 GW non-fossil capacity target by 2030 (MNRE) are further accelerating deployment. Declining costs also play a key role, with IRENA 2023 noting that utility-scale solar LCOE has fallen by ~89% between 2010 and 2022, making grid-connected PV one of the most cost-competitive power sources globally.

- For instance, in June 2024, China commissioned one of the world’s largest grid-connected solar projects, the Midong Solar Park (3.5 GW) in Xinjiang, significantly boosting its renewable capacity. According to the National Energy Administration (NEA), China added over 216 GW of solar PV capacity in 2023, the highest globally. Such large-scale grid-connected installations highlight the growing role of utility-scale solar in meeting electricity demand and supporting national decarbonization targets.

Some of the leading companies operating in the industry include Trina Solar, JinkoSolar Holding Co., Ltd., Canadian Solar Inc., First Solar, Inc., and others. Trina Solar Co., Ltd. is a leading global provider of solar photovoltaic (PV) products and smart energy solutions, headquartered in China. The company specializes in the manufacturing of high-efficiency solar modules, as well as integrated solutions including trackers and energy storage systems.

Download Free sample to learn more about this report.

GRID CONNECTED PV SYSTEMS MARKET TRENDS

Expansion of Grid Infrastructure and Smart Grid Integration are the Key Market Trends

The expansion of grid infrastructure and deployment of smart grid technologies are playing a critical role in enabling higher penetration of grid-connected PV systems. As solar generation is variable, modern grids require enhanced flexibility, digitalization, and real-time management capabilities. According to the IEA, June 2024, global investment in electricity grids to support renewable integration reached over USD 310 billion in 2023, reflecting a significant increase.

Additionally, the IEA (Electricity Grids and Secure Energy Transitions, 2023 highlights that more than 80 million km of grid infrastructure will need to be added or upgraded by 2040 to meet climate targets. Smart grid technologies, including Advanced Metering Infrastructure (AMI), automated substations, and grid analytics, enable efficient load balancing and integration of distributed solar systems. Countries such as the U.S. and China are rapidly deploying digital grid solutions to accommodate rising solar capacity. These developments reduce curtailment risks, improve grid reliability, and facilitate seamless integration of large-scale and distributed PV systems into national electricity networks.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growth of Energy Storage Integration with Solar PV Projects to Drive the Market Growth

The growing integration of energy storage systems with solar PV projects is significantly driving the adoption of grid-connected PV systems by enhancing reliability and grid stability. As solar power generation is intermittent, Battery Energy Storage Systems (BESS) enable the storage of excess electricity generated during peak sunlight hours for use during periods of low or no generation. According to the IEA Renewables 2024 Report, global battery storage capacity additions are expected to increase sharply, supporting higher shares of solar PV in electricity generation.

In addition, the IEA World Energy Outlook 2023 highlights that energy storage capacity must expand nearly six fold by 2030 to meet clean energy transition goals. The integration of storage with solar projects allows utilities and grid operators to manage peak demand, reduce reliance on fossil fuel-based backup power, and improve overall system flexibility. This hybrid model is increasingly being adopted in utility-scale solar projects as well as commercial and industrial applications, thereby accelerating the growth of grid-connected PV systems globally.

MARKET RESTRAINTS

Grid Integration Challenges and Curtailment Risks to Hamper the Market Demand

The rapid expansion of grid connected PV systems is constrained by limitations in existing grid infrastructure and integration challenges. As solar generation is variable and often concentrated during peak daylight hours, many regions face issues related to grid stability, transmission bottlenecks, and power curtailment.

According to the IEA Renewables 2024 report, several countries with high solar penetration, including China and parts of Europe, have experienced increasing curtailment due to insufficient grid flexibility and storage capacity. Additionally, delays in transmission infrastructure development hinder the evacuation of power from large-scale solar projects.

MARKET OPPORTUNITIES

Rising Adoption of Solar PV in Emerging Markets and Decentralized Energy Systems is Creating Growth Opportunities

The expansion of grid-connected PV systems presents significant opportunities in emerging markets and decentralized energy systems. Many developing regions in Asia, Africa, and Latin America are experiencing rapid growth in electricity demand, generating a strong need for scalable and cost-effective power generation solutions. Governments in these regions are increasingly investing in grid expansion and renewable energy integration, enabling wider deployment of solar PV systems.

According to the IEA Electricity 2024 report, developing economies are expected to account for over 85% of global electricity demand throughout 2026. Additionally, the rise of decentralized energy systems, including distributed rooftop solar and mini-grid integration with national grids, is creating new avenues for the product adoption. International funding from organizations such as the World Bank and IFC is further supporting solar projects in underserved regions.

MARKET CHALLENGES

Supply Chain Constraints and Raw Material Dependency to Challenge Market Growth

The growth of the market faces challenges due to supply chain constraints and dependence on key raw materials. The solar industry relies heavily on materials such as polysilicon, silver, and critical components like wafers and cells, with a significant portion of production concentrated in a few countries. Disruptions in raw material supply, trade restrictions, or geopolitical tensions can lead to price volatility and project delays. Additionally, fluctuations in polysilicon prices have historically impacted module costs and project economics.

According to the IEA Solar PV Global Supply Chains Report, July 2022, China accounts for over 80% of global solar manufacturing capacity across key stages, creating supply concentration risks.

Segmentation Analysis

By Component

Solar Modules Lead as They are the Primary Energy-Converting Components

Based on component, the market is classified into solar modules, power conditioning unit, grid connection equipment, inverters, and others.

In 2025, solar modules dominate the grid connected PV systems market share as they are the primary components responsible for converting sunlight into electricity, making them the most essential and largest cost contributor in the system. According to IRENA Renewable Power Generation Costs, 2023, modules account for a significant share of total system costs despite substantial price declines over the past decade. The dominance is further reinforced by continuous advancements in module efficiency, large-scale manufacturing (especially in China), and increasing deployment across both utility-scale and rooftop installations.

The inverters segment is set to experience the highest growth of 28.14% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Crystalline Silicon, with its High Efficiency and Reliability is the Governing Technology

According to technology, the market is classified into crystalline silicon, thin-film, and others.

In 2025, Crystalline silicon (c-Si) dominates the market due to its high efficiency, reliability, and well-established manufacturing ecosystem. It offers superior performance compared to other technologies, with higher conversion efficiencies and longer operational lifespans, making it the preferred choice for both utility-scale and rooftop installations.

The thin-film segment is expected to grow at a CAGR of 27.23% from 2026 to 2034.

By End User

Utility Is The Dominant End User With Their Large-Scale Cost-Efficient Power Generation

On the basis of end user, the market is classified into residential, commercial, utility, and industrial.

In 2025, the utility segment dominated due to their ability to generate electricity at significantly lower costs through economies of scale. Large solar farms benefit from bulk procurement of components, optimized land use, and higher operational efficiency, resulting in Lower Levelized Cost of Electricity (LCOE). These projects are typically developed by independent power producers and utilities, ensuring stable revenue streams.

The residential segment is expected to grow at a CAGR of 25.17% over the forecast period.

Grid Connected PV Systems Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

Asia Pacific Grid Connected PV Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the third-highest share in 2025, valued at USD 60.80 billion, and also expected to take a significant share in 2026 with USD 75.49 billion.

Grid-connected solar PV systems in North America are experiencing steady growth, driven primarily by large-scale deployments in the U.S. and increasing adoption in Canada. According to the U.S. Energy Information Administration, the U.S. installed over 30 GW of new solar capacity in 2023, bringing total installed capacity to approximately 180 GW. Additionally, the Inflation Reduction Act (2022) continues to support long-term solar expansion through tax incentives. As of early 2026, in Canada, solar capacity has reached ~5–6 GW, with growth concentrated in provinces such as Ontario and Alberta.

U.S. Grid Connected PV Systems Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was approximated at around USD 54.12 billion in 2025, accounting for roughly 10.82% of the global market size.

Europe

Europe is projected to record a growth rate of 25.59% in the coming years, which is the second-highest among all regions, and reached a valuation of USD 84.31 billion by 2025. Grid-connected solar PV systems in Europe are witnessing strong growth, supported by policy frameworks and energy security concerns. According to SolarPower Europe 2024, the region installed approximately 56 GW of new solar capacity in 2023, bringing total installed capacity to over 260 GW. Countries such as Germany, Spain, and the Netherlands are leading installations, with significant contributions from both utility-scale and rooftop systems.

Germany Grid Connected PV Systems Market

The Germany market in 2025 reached around USD 23.71 billion 2025 and is estimated at around USD 29.91 billion in 2026, representing roughly 4.74% of the global market revenues. Germany is one of the leading markets in Europe, with installed capacity exceeding 80 GW in 2024, according to IEA reports. Strong policy support, high rooftop adoption, and increasing utility-scale projects continue to drive steady demand in the country.

Asia Pacific

Asia Pacific touched USD 298.17 billion in 2025 and secured the largest share of the market. In the region, India and China are both estimated to reach USD 38.35 billion and USD 146.83 billion, respectively, in 2025.

According to IEA, the Asia Pacific leads global grid-connected PV deployment, contributing over 60% of total global solar electricity generation in 2023. Also, the region is home to the world’s largest solar manufacturing base, accounting for over 85% of global module production capacity

Japan Grid Connected PV Systems Market

The Japan market in 2025 reached around USD 26.95 billion, accounting for roughly 5.39% of global market revenues.

Japan is a mature and technologically advanced market, characterized by strong rooftop adoption and stable policy support. The country has one of the highest solar capacities per unit of land due to space constraints and urban deployment.

China Grid Connected PV Systems Market

China’s market is projected to be significant, with 2025 revenues touching USD 146.83 billion, representing roughly 29.36% of the global market.

India Grid Connected PV Systems Market

The India market in 2025 was around USD 38.35 billion, accounting for roughly 7.67% of global revenues.

Latin America

Latin America is expected to witness moderate growth in this market space during the forecast period. The Latin America market reached a valuation of USD 36.21 billion in 2025.

It is emerging as a high-growth region, driven by strong solar irradiation and increasing private-sector investment in countries such as Chile and Colombia.

Brazil Grid Connected PV Systems Market

Brazil's market was around USD 20.39 billion in 2025, representing roughly 4.08% of the global market.

Middle East & Africa

The Middle East & Africa are expected to witness significant growth in this market space during the forecast period and also recorded a valuation of USD 20.61 billion in 2025.

The region is witnessing increasing adoption of grid-connected PV systems, supported by large-scale solar tenders and rising energy demand across key economies. The region is also attracting significant international financing, with countries like Egypt and Morocco expanding their solar capacity through multi-gigawatt projects and public-private partnerships.

GCC Grid Connected PV Systems Market

The GCC market touched around USD 9.85 billion in 2025, representing roughly 1.97% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Are Expanding Their Market Share Via Partnerships, Business Expansion, and Technological Advancements

The global grid connected PV systems market holds a consolidated market structure, constituting prominent players such as Trina Solar, JinkoSolar Holding Co., Ltd., Canadian Solar Inc., First Solar, Inc., and others. Companies operating in the market are adopting targeted growth strategies focused on strengthening their product portfolio, technical capability, expanding manufacturing presence, and other areas.

- For instance, in May 2024, First Solar, Inc. announced the commissioning of its largest U.S.-based manufacturing facility in Alabama, adding 3.5 GW of annual module production capacity to support utility-scale grid-connected PV projects. The expansion aligns with growing demand for domestically produced solar modules under U.S. clean energy policies.

Other key players in the global market include Hanwha Q CELLS Co., Ltd., SMA Solar Technology AG, ABB Ltd., and others. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY GRID CONNECTED PV SYSTEMS COMPANIES PROFILED

- Trina Solar (China)

- JinkoSolar Holding Co., Ltd. (China)

- Canadian Solar Inc. (Canada)

- First Solar, Inc. (U.S.)

- Hanwha Q CELLS Co., Ltd. (South Korea)

- SMA Solar Technology AG (Germany)

- ABB Ltd. (Switzerland)

- Schneider Electric SE (France)

- Huawei Technologies Co., Ltd. (China)

- SolarEdge Technologies, Inc. (U.S.)

- LG Electronics Inc. (South Korea)

- JA Solar Technology Co., Ltd. (China)

- Delta Electronics, Inc. (Taiwan)

- SunPower Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2024: Trina Solar supplied high-efficiency modules for a large-scale grid-connected solar project in Saudi Arabia, contributing to the country’s renewable expansion under Vision 2030. The project utilizes Trina’s advanced n-type TOPCon modules, designed for high output in desert conditions. This deployment highlights Trina Solar’s growing presence in utility-scale solar installations across the Middle East, where demand for grid-connected PV systems is rapidly increasing.

- August 2024: First Solar signed an agreement to supply modules for a multi-gigawatt utility-scale solar project pipeline in the U.S. The projects will use First Solar’s thin-film CdTe modules, known for strong performance in high-temperature environments. These installations support grid-connected solar expansion under the Inflation Reduction Act, highlighting First Solar’s leadership in supplying modules for large utility-scale PV systems.

- July 2024: JinkoSolar announced the delivery of its Tiger Neo modules for multiple utility-scale grid-connected PV projects in Brazil. The projects are part of Brazil’s expanding solar portfolio, driven by increasing demand for renewable power. JinkoSolar’s high-efficiency modules are being used to improve energy yield and system performance, reinforcing its strong position in Latin America’s fast-growing grid-connected solar market.

- June 2024: Canadian Solar secured a contract to supply modules and develop a grid-connected solar project in Spain through its subsidiary, Recurrent Energy. The project forms part of Europe’s accelerating solar deployment under clean energy targets.

- January 2024: First Solar began module deliveries for a large-scale solar project portfolio in India totaling over 1 GW. The projects are part of India’s push toward expanding grid-connected renewable capacity. First Solar’s thin-film technology is being deployed to improve performance under high-temperature conditions, reinforcing its role in supporting utility-scale solar expansion in emerging markets.

REPORT COVERAGE

The global grid connected PV systems market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and the market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 25.29% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Technology, End User, and Region |

| By Component |

|

| By Technology |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 500.10 billion in 2025 and is projected to reach USD 3,820.44 billion by 2034.

In 2025, the market value stood at USD 298.17 billion.

The market is expected to exhibit a CAGR of 25.29% during the forecast period.

The solar modules segment led the market by component.

Rising renewable energy targets, declining solar costs, grid infrastructure expansion, and increasing electricity demand are the key factors driving the market.

Trina Solar, JinkoSolar Holding Co., Ltd., Canadian Solar Inc., and First Solar, Inc. are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

Supportive government policies, expansion of grid networks, increasing corporate clean energy procurement, and integration with energy storage are expected to favor systems’ adoption.

- 2021-2034

- 2025

- 2021-2024

- 205

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us