Healthcare Simulation Market Size, Share & Industry Analysis, By Product & Service Type (Simulation Hardware {Patient & Surgical Simulators, & Others}, Simulation Software {Virtual Simulation Platforms, AR Simulation Software, & Others}, & Simulation Services), By Fidelity Level (Low, Medium, & High-Fidelity Simulation), By Application (Medical Education & Training, Nursing & Allied Health Training, Surgical Skills Training, Emergency & Trauma Care Training, & Others), By End-user (Academic & Educational Institutions, Hospitals & Healthcare Providers, & Others), & Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

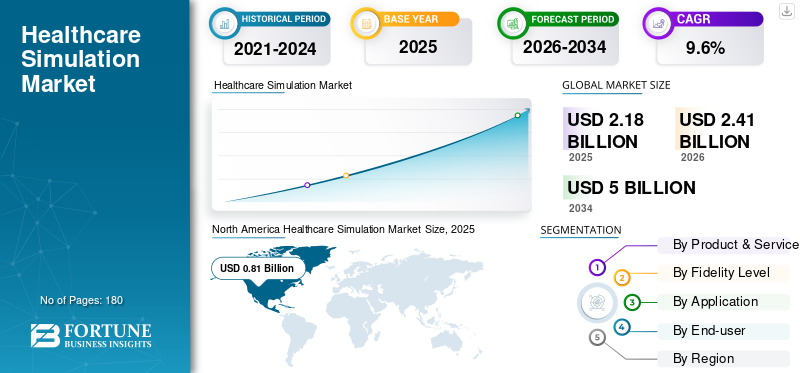

The global healthcare simulation market size was valued at USD 2.18 billion in 2025. The market is projected to grow from USD 2.41 billion in 2026 to USD 5.00 billion by 2034, exhibiting a CAGR of 9.6% during the forecast period. North America dominated the global healthcare simulation market with a market share of 37.15% in 2025.

Healthcare simulation is a training method that utilizes realistic, artificial scenarios to help medical professionals learn, practice, and assess clinical skills in a safe environment, mimicking real-life situations without exposing patients to risk. This approach ultimately improves patient safety and care quality through experiential learning.

The market is witnessing sustained growth as healthcare systems globally place greater emphasis on patient safety, competency-based education, and error reduction. Rising surgical volumes, increasing complexity of procedures, and a global shortage of skilled healthcare professionals are accelerating the adoption of simulation-based learning. According to international health agencies, millions of preventable adverse events occur annually due to clinical errors, reinforcing the need for structured simulation training.

Furthermore, Laerdal Medical, Elevate Healthcare, Surgical Science Group AB, and Gaumard Scientific held the largest market share, driven by increasing investments and strategic initiatives, such as collaborations and partnerships.

Download Free sample to learn more about this report.

HEALTHCARE SIMULATION MARKET TRENDS

Shift Toward Digital, AR, and Virtual Simulation Platforms as a Key Market Trend

A notable trend shaping the healthcare simulation market is the shift from purely hardware-based solutions toward digital, virtual, and augmented reality simulation platforms. Institutions are increasingly adopting virtual simulation software to complement physical simulators, enabling remote learning, scalability, and standardized assessment. The COVID-19 pandemic accelerated acceptance of virtual simulation, particularly for nursing and allied health training. Since then, companies have continued to invest in immersive AR-based solutions for procedural guidance and anatomy visualization.

- For instance, several vendors have launched AR-enabled surgical training modules that allow learners to practice complex procedures with real-time feedback. These technologies reduce dependency on physical lab space while improving learner engagement.

Additionally, subscription-based software models are gaining traction, providing predictable costs and frequent content updates. This digital transition is reshaping purchasing behavior and expanding access to simulation beyond traditional academic hospitals.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Focus on Patient Safety and Clinical Competency to Fuel Market Growth

Patient safety has emerged as a key driver of the healthcare simulation market, supported by growing evidence linking simulation training to a reduction in medical errors. Studies published by global patient safety organizations indicate that preventable adverse events remain among the leading causes of morbidity in hospital settings, particularly during high-risk procedures such as surgery, anesthesia, and emergency care. As a result, regulators, accreditation bodies, and healthcare institutions are increasingly mandating simulation-based training for credentialing and continuous medical education.

- For instance, surgical societies in North America and Europe now recommend simulator-based proficiency benchmarks as a prerequisite for independent practice.

Additionally, the global rise in surgical procedures driven by aging populations and the increasing prevalence of chronic diseases has increased demand for advanced procedural training. Companies such as Surgical Science and Mentice have expanded their surgical simulation portfolios to address minimally invasive and endovascular procedures. Hospitals are also investing in simulation labs to standardize team-based training, particularly for intensive care and trauma scenarios, reinforcing simulation as a core component of modern clinical education.

MARKET RESTRAINTS

High Capital Investment and Budget Constraints to Restrict Market Growth

Despite its clinical benefits, the healthcare simulation market faces adoption challenges due to high upfront capital requirements, particularly for high-fidelity simulators and advanced surgical platforms. Full-scale patient simulators, integrated simulation labs, and immersive AR/VR systems require significant investment in hardware, software licenses, infrastructure, and faculty training. This cost burden is especially restrictive for smaller hospitals, public healthcare institutions, and medical schools in cost-sensitive regions. In emerging economies, simulation procurement often competes with essential healthcare infrastructure spending, limiting large-scale deployment.

Furthermore, simulation equipment requires regular maintenance, software updates, and technical support, adding to long-term ownership costs. While vendors such as Laerdal and Elevate Healthcare offer modular and scalable solutions, budget approvals remain lengthy and fragmented in many regions. These financial barriers can slow replacement cycles and restrict adoption beyond flagship academic centers, particularly in low- and middle-income countries.

MARKET OPPORTUNITIES

Expansion of Medical Education Infrastructure in Emerging Markets to Create Significant Growth Opportunities

The rapid expansion of medical education infrastructure across the Asia Pacific, the Middle East, and Africa presents a significant growth opportunity for the healthcare simulation market. Governments in countries such as India, China, Saudi Arabia, and Indonesia are investing heavily in new medical colleges, nursing schools, and healthcare universities to address workforce shortages. For example, several Gulf Cooperation Council (GCC) countries have launched centralized simulation centers to support national training programs. Simulation is increasingly viewed as a cost-effective way to scale clinical education without overburdening hospital systems.

In parallel, private medical universities and international collaborations are incorporating simulation into standardized curricula to meet global accreditation standards. Vendors are responding by introducing region-specific, cost-optimized simulators and cloud-based virtual platforms that reduce infrastructure dependence. As healthcare education capacity expands, simulation is expected to become a foundational training tool rather than a supplementary resource, particularly in fast-growing healthcare systems.

MARKET CHALLENGES

Shortage of Trained Simulation Faculty and Standardization Gaps to Challenge Market Growth

One of the key challenges facing the healthcare simulation market is the shortage of trained simulation educators and the lack of standardized implementation frameworks. Effective simulation training requires skilled faculty who can design scenarios, operate equipment, and conduct structured debriefing sessions. However, many institutions lack adequately trained simulation professionals, limiting the clinical impact of installed systems.

Additionally, simulation practices vary widely across regions, institutions, and specialties, creating inconsistencies in training outcomes. While international organizations have published best-practice guidelines, adoption remains uneven. Smaller hospitals and newer medical schools often struggle to integrate simulation into curricula due to limited expertise and operational support. Vendors are increasingly offering training and consulting services to address this gap, but workforce constraints remain a critical bottleneck, particularly in rapidly expanding healthcare education markets.

Segmentation Analysis

By Product & Service Type

Wide Adoption of Hardware to Drive Simulation Hardware Segment Growth

Based on product & service type, the market is segmented into simulation hardware, simulation software, and simulation services. Simulation hardware is further segmented into patient simulators, surgical simulators, and others. Additionally, simulation software is further segmented into virtual simulation platforms, augmented reality (AR) simulation software, and others.

To know how our report can help streamline your business, Speak to Analyst

The simulation hardware segment accounted for the largest global healthcare simulation market share in 2025. Patient simulators and surgical simulators are widely adopted across medical schools, nursing institutions, and hospitals for teaching core clinical skills, emergency response, and procedural techniques. Hardware-based training remains essential for replicating tactile feedback, physiological responses, and real-world clinical environments.

Major institutions often prioritize capital investment in high-fidelity mannequins and surgical trainers to meet accreditation requirements. Although software adoption is increasing, hardware remains a key component in simulation labs, particularly in developed markets where replacement and upgrade cycles sustain demand.

Additionally, the simulation software segment is projected to grow at a CAGR of 12.6% during the forecast period.

By Fidelity Level

Wide Applications to Accelerate High-Fidelity Simulation Segment

By fidelity level, the market is classified into low-fidelity simulation, medium-fidelity simulation, and high-fidelity simulation.

High-fidelity simulation holds a dominant share due to its ability to closely mimic real patient physiology and complex clinical scenarios. These systems are extensively used in advanced surgical training, anesthesia, intensive care, and trauma management. High-fidelity simulators enable multidisciplinary team training and error management without patient risk, making them indispensable in tertiary care hospitals and academic centers. Moreover, the segment is projected to hold a 39.6% share in 2026.

Additionally, the medium-fidelity simulation segment is estimated to grow at a CAGR of 9.0% during the forecast period.

By Application

Increasing Medical Education & Training Globally to Drive Medical Education & Training Segment’s Growth

By application, the market is categorized into medical education & training, nursing & allied health training, surgical skills training, emergency & trauma care training, and others.

Medical education & training represent the largest application segment, driven by the growing number of medical schools and structured residency programs globally. Simulation is now integrated into undergraduate and postgraduate curricula to supplement limited clinical exposure and ensure standardized skill development. Moreover, the segment is projected to hold a 35.4% share in 2026.

Additionally, the surgical skills training segment is estimated to grow at a CAGR of 12.3% during the forecast period.

By End-user

High Number of Academic & Educational Institutions to Propel Segment Growth

On the basis of end-user, the market is classified into academic & educational institutions, hospitals & healthcare providers, and others.

In 2025, academic & educational institutions dominated the market by end-users. Academic and educational institutions dominate end-user adoption due to their central role in training future healthcare professionals. Medical universities, nursing colleges, and allied health schools are primary buyers of simulation hardware, software, and services. These institutions often receive government funding or grants for simulation infrastructure and are early adopters of new training technologies. Furthermore, the segment is set to hold 56.7% share in 2026.

In addition, the hospitals & healthcare providers segment is projected to grow at a CAGR of 11.4% during the forecast period.

Healthcare Simulation Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Healthcare Simulation Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024, at USD 0.75 billion, and is expected to reach USD 0.81 billion in 2025. North America remains a significant contributor to growth due to the deep integration of simulation into medical education, accreditation, and hospital training programs. The region boasts one of the highest concentrations of medical schools, nursing colleges, and teaching hospitals globally, all of which are increasingly mandating simulation-based training to enhance patient safety.

The U.S. alone performs tens of millions of surgical procedures annually, driving demand for advanced procedural and surgical simulators. The regulatory emphasis on competency-based training, particularly in surgery, anesthesia, and emergency care, continues to reinforce its adoption.

U.S Healthcare Simulation Market

In 2026, the U.S. market is projected to represent USD 0.78 billion, capturing 32.3% of total global revenue.

Europe

Europe is expected to achieve a 7.5% growth rate in the coming years, the second-highest globally, reaching USD 0.60 billion by 2026. The presence of structured public healthcare systems and stringent regulatory oversight of medical training drives the Europe healthcare simulation market. Many European countries have integrated simulation into national medical education frameworks, particularly for nursing, anesthesia, and surgical specialties.

U.K Healthcare Simulation Market

The U.K. market is projected to reach USD 0.08 billion by 2026, accounting for 3.8% of the global market revenue.

Germany Healthcare Simulation Market

Germany's healthcare simulation market is projected to reach about USD 0.10 billion by 2026, representing roughly 4.6% of global revenue.

Asia Pacific

In 2026, the Asia Pacific healthcare simulation market is predicted to be valued at USD 0.60 billion, ranking as the third-largest globally. The growth is driven by rapid expansion of healthcare infrastructure and medical education capacity. Countries such as China, India, and Southeast Asian nations are adding large numbers of medical and nursing schools to address physician and nurse shortages. This expansion is increasing demand for scalable training tools such as patient simulators and virtual simulation platforms. The region is also experiencing a sharp rise in surgical procedures due to urbanization, improved healthcare access, and growing chronic disease burden.

Japan Healthcare Simulation Market

Japan is projected to generate approximately USD 0.09 billion in revenue by 2026, contributing nearly 3.6% to the global market.

China Healthcare Simulation Market

China’s healthcare simulation market is forecast to reach approximately USD 0.15 billion by 2026, contributing about 6.1% to global revenues.

India Healthcare Simulation Market

India is forecast to contribute approximately USD 0.07 billion to the healthcare simulation market by 2026, corresponding to about 3.0% of global revenues.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate healthcare simulation market growth, with Latin America expected to reach around USD 0.17 billion by 2026. Growth in Latin America is supported by the gradual modernization of healthcare systems and increasing focus on professional training and patient safety. Brazil and Mexico are witnessing rising surgical volumes and growing private healthcare investment, which is driving demand for simulation-based training tools.

GCC Healthcare Simulation Market

By 2026, the GCC is expected to generate approximately USD 0.07 billion in the healthcare simulation market, accounting for nearly 2.8% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Distribution Network to Strengthen Market Position of Prominent Players

The global healthcare simulation market is moderately consolidated, with a small group of multinational players holding a significant share. At the same time, a long tail of regional and niche companies contributes to fragmentation. Market leadership is largely defined by the breadth of its product portfolio, the size of its installed base, and the strength of its long-term relationships with academic and healthcare institutions. Established players dominate the patient simulator and high-fidelity hardware segments, whereas specialized companies are gaining traction in surgical, endovascular, and digital simulation. Large vendors such as Laerdal Medical and Elevate Healthcare benefit from strong global distribution networks and recurring institutional contracts, particularly with medical schools and teaching hospitals. In parallel, Surgical Science Group has strengthened its competitive position through portfolio expansion in procedural and ultrasound simulation, consolidating its role in advanced surgical training.

Moreover, mid-sized players such as Gaumard Scientific, Mentice, and Kyoto Kagaku compete through product specialization and regional strength. At the same time, newer companies are focusing on virtual and immersive simulation platforms to differentiate themselves based on flexibility and scalability.

LIST OF KEY HEALTHCARE SIMULATION MARKET COMPANIES PROFILED

- Laerdal Medical (Norway)

- Elevate Healthcare (U.S.)

- Surgical Science Group AB (Sweden)

- Gaumard Scientific (U.S.)

- Mentice AB (Sweden)

- Kyoto Kagaku Co., Ltd. (Japan)

- Simulab Corporation (U.S.)

- Limbs & Things Ltd. (U.K.)

- VirtaMed AG (Switzerland)

- Simulaids Ltd. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Elevate Healthcare, the leader in simulation-based education, announced that it has entered into a strategic partnership with SimX, the leader in virtual reality (VR) healthcare training, to transform the landscape of medical education and training. This collaboration will bring together SimX’s innovative VR simulation platform and Elevate’s proven expertise in healthcare simulation and simulation center management.

- February 2025: Surgical Science Sweden AB has completed the purchase of Intelligent Ultrasound Group PLC.

- January 2025: InSimo and VirtaMed announced the strengthening/renewal of their partnership with a dedicated suturing module.

- May 2024: After the successful acquisition by Madison Industries in February, CAE Healthcare has announced that it has rebranded to Elevate Healthcare. The launch of Elevate Healthcare reflects the company’s renewed vision and commitment to driving innovation in healthcare education and simulation.

- February 2024: Madison Industries has acquired Montreal-based CAE Healthcare, a technology company that makes the world safer and more productive through cutting-edge medical simulation and training solutions.

REPORT COVERAGE

The global healthcare simulation market report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.6% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product & Service Type, Fidelity Level, Application, End-user, and Region |

|

By Product & Service Type |

· Simulation Hardware o Patient Simulators o Surgical Simulators o Others · Simulation Software o Virtual Simulation Platforms o Augmented Reality (AR) Simulation Software o Others · Simulation Services |

|

By Fidelity Level |

· Low-Fidelity Simulation · Medium-Fidelity Simulation · High-Fidelity Simulation |

|

By Application |

· Medical Education & Training · Nursing & Allied Health Training · Surgical Skills Training · Emergency & Trauma Care Training · Others |

|

By End-user |

· Academic & Educational Institutions · Hospitals & Healthcare Providers · Others |

|

By Region |

· North America ( By Product & Service Type, Fidelity Level, Application, End-user, and Country) o U.S. (By Product & Service Type) o Canada (By Product & Service Type) · Europe (By Product & Service Type, Fidelity Level, Application, End-user, and Country/Sub-region) o Germany (By Product & Service Type) o U.K. (By Product & Service Type) o France (By Product & Service Type) o Spain (By Product & Service Type) o Italy (By Product & Service Type) o Scandinavia (By Product & Service Type) o Rest of Europe (By Product & Service Type) · Asia Pacific (By Product & Service Type, Fidelity Level, Application, End-user, and Country/Sub-region) o China (By Product & Service Type) o Japan (By Product & Service Type) o India (By Product & Service Type) o Australia (By Product & Service Type) o Southeast Asia (By Product & Service Type) o Rest of Asia Pacific (By Product & Service Type) · Latin America (By Product & Service Type, Fidelity Level, Application, End-user, and Country/Sub-region) o Brazil (By Product & Service Type) o Mexico (By Product & Service Type) o Rest of Latin America (By Product & Service Type) · Middle East & Africa (By Product & Service Type, Fidelity Level, Application, End-user, and Country/Sub-region) o GCC (By Product & Service Type) o South Africa (By Product & Service Type) o Rest of the Middle East & Africa (By Product & Service Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.18 billion in 2025 and is projected to reach USD 5.00 billion by 2034.

In 2025, the market value stood at USD 0.81 billion.

The market is expected to exhibit a CAGR of 9.6% during the forecast period of 2026-2034.

The simulation hardware segment led the market by product & service type.

The key factors driving the market are advancements in simulation, the expansion of several applications, and others.

Laerdal Medical, Elevate Healthcare, Surgical Science Group AB, and Gaumard Scientific are some of the major players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us