High Protein Food Market Size, Share & Industry Analysis, By Product Type (Protein Bars & Bites, High-Protein Dairy Foods, Meat, Poultry & Seafood Protein Snacks, High-Protein Beverages, High-Protein Snacks, and Others), By Source (Animal-Based Protein, Plant-Based Protein, Blended Protein, and Others), By Form (Solid, Semi-Solid, and Liquid), By Distribution Channel (Supermarkets & Hypermarkets, Online Retail, Convenience Stores, Specialty Nutrition / Health Stores, and Others), By Storage Condition (Ambient / Shelf-Stable, Chilled / Refrigerated, and Frozen) and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

High Protein Food Market Size and Future Outlook

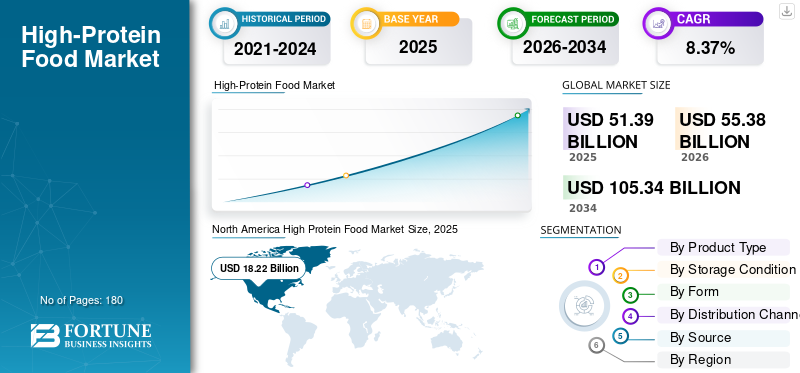

The high protein food market size was valued at USD 51.39 billion in 2025. The market is projected to grow from USD 55.38 billion in 2026 to USD 105.34 billion by 2034, exhibiting a CAGR of 8.37% during the forecast period. North America dominated the high protein food market with a market share of 35.45% in 2025.

High-protein food products are foods and drinks that have more protein than conventional products. They are typically generated from animal sources such as meat, dairy, and eggs, and also from plants such as soy, peas, and legumes. Examples of such products include protein bars, shakes, dairy products, snacks, and meals with added protein.

The market for these products is growing rapidly with increasing focus on health, fitness, and consumers concerned about managing their weight. People are also consuming food products which helps to build muscle, feel full, and support overall wellness. The market is also expanding worldwide due to growth in sports nutrition products, rising adoption of plant-based diets, and increasing popularity of convenient products.

Companies such as Nestlé S.A., Danone S.A., PepsiCo, Inc., Glanbia plc, and Abbott Laboratories and others are some of the key players operating in this market. New product launch with improved product formulation is the key strategy boosting product sales and supporting the market growth.

Download Free sample to learn more about this report.

HIGH PROTEIN FOOD MARKET TRENDS

Shift Toward Plant-Based, Clean-Label, and On-the-Go Protein Products are Emerging Market Trends

One major market trend is the rising demand for plant based protein sources, as more people are concerned about the environmental and ethical issues. Health-conscious consumers are seeking clean-label and minimally processed products. Hence, increasing number of food manufacturers are launching snacks, dairy alternatives, and drinks with added protein. Rising adoption of digital health products that track calories and protein consumed each day along with increased fitness awareness among young consumers shape their purchase behavior. New hybrid protein products that mix plant and animal sources are also becoming popular which are launched in convenient packages.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Health, Fitness, and Weight Management Awareness Accelerates Market Growth

The market is driven by increasing consumer focus on health, fitness, and active lifestyles. Rising awareness of the role of protein in muscle building, weight management, and overall wellness is significantly boosting demand. Sports nutrition sector is rapidly and expanding consumers are exercising in gyms to maintain physique or train and become athletes. These are the prime consumers for the market which is directly boosting product sales. Plant-based diets are becoming more popular, leading to launch of new protein options such as soy, pea, and lentil proteins in the market. Ready-to-eat high protein snacks and drinks are convenient and high number of consumers across all age groups are choosing them.

MARKET RESTRAINTS

High Production Costs and Taste Formulation Challenges Limits Market Expansion

The market faces challenges such as high production costs associated with protein extraction and processing, particularly for plant-based and specialty proteins. Price sensitivity in developing markets can limit the adoption of premium high-protein products. Taste, texture, and formulation issues can also impact consumer acceptance of these products, especially for plant-based proteins. Non uniform regulatory rules and labeling standards for protein claims can create confusion and hamper commercialization of the products, thus slowing down the market growth.

MARKET OPPORTUNITIES

Growing Demand for Alternative Proteins and Personalized Nutrition Creates New Market Expansion Potential

There are many opportunities to develop new protein sources, such as plant-based, insect-based, and lab-grown proteins. As more people look for personalized nutrition and functional foods, there is an opportunity for the manufacturers to create high-protein products that meet specific health needs. Emerging markets also present strong growth potential for the manufacturers due to rising disposable incomes and evolving dietary patterns in these regions. Expansion of protein-enriched snacks, beverages, and meal replacements is creating new product categories and boosting market growth. Moreover, using advanced food technology can help improve taste, texture, and absorption of these products, making them more appealing.

Segmentation Analysis

By Product Type

High Demand for Convenient, Portable, and On-the-Go Protein Snacks Driving Dominance of Protein Bars & Bites Segment

The market is segmented by product type into protein bars & bites, high-protein dairy foods, meat, poultry & seafood protein snacks, high-protein beverages, high-protein snacks, plant-based high-protein foods, high-protein bakery & cereals, high-protein ready meals & meal solutions and others.

The protein bars & bites segment is projected held the largest high protein food market share in 2025. These protein rich foods products are popular as they are convenient, easy to carry, and fit well with busy lifestyles. Fitness enthusiasts and working professionals often choose these products as quick meal replacements or snacks. Such products are available in portion sizes, last longer on shelves, and are easy to store, which makes them a good fit for retail stores. New flavors, textures, and added benefits keep these products appealing to customers.

High-protein beverage is another major segment, amounting to 9.35% CAGR during the forecast period. These products are popular among consumers who prefer ready to drink nutrition options. These drinks are convenient and are absorbed quickly, which makes them popular with athletes and consumers leading active lifestyle. However, such products incur higher costs, shorter shelf life, and storage requirements compared to bars.

By Storage Condition

Longer Shelf Life and Ease of Storage Without Cold Chain Requirements Driving Dominance of Ambient / shelf-stable Segment

Based on the storage condition the market is segmented into ambient / shelf-stable, chilled / refrigerated and frozen.

Ambient / shelf-stable derived accounted for the largest market share in 2025. This is due to their longer shelf life, ease of storage, and widespread distribution advantages. These products do not require refrigeration, making them highly suitable for mass retail, e-commerce, and global supply chains. Protein bars, powders, and shelf-stable snacks are the main products in this category and they fit well with on-the-go eating habits and impulse buying of consumers.

Chilled is another major segment, amounting to 8.58% CAGR during the forecast period. Chilled products have the second-largest market share and this category includes items such as protein yogurts, dairy drinks, and fresh snacks, which are known for their taste and freshness. However, chilled products have a shorter shelf life and higher storage and transport costs. They also rely on cold chain infrastructure, which makes them difficult to scale than ambient products.

By Form

High Consumer Preference for Convenient, Portable, and Shelf-Stable Protein Options Drives Dominance of Solid Segment

The market is segmented, by form into solid, semi-solid and liquid.

The solid segment leads in the global market in 2025. They are convenient, easy to carry, and fit current snacking and meal replacement trends. Protein bars, bites, and fortified foods do not need additional preparation, and last longer, which makes them suitable for eating on-the-go. Solid products also come in many flavors and textures, which helps boost their popularity.

Liquid is another major category that has a CAGR of 8.90% during the forecast period. Liquid forms are the second most popular option as they are easy to absorb and convenient, especially in ready-to-drink protein shakes and drinks. Athletes and people with active lifestyles often pick these for recovery after workouts.

By Source

Superior Amino Acid Profile and Higher Bioavailability Driving Dominance of Animal Based Protein Sources

The market is segmented, by source into animal-based protein, plant-based protein, blended protein and alternative / novel protein.

The animal based protein segment leads in the global market in 2025. They offer a complete amino acid profile, are easily absorbed by the body, and have earned strong consumer trust. Traditional animal based proteins from dairy, meat, eggs, and whey are commonly used in supplements, drinks, and functional foods as they are highly nutritious and help with muscle building and recovery. Strong supply chains, wide product availability, and long-standing consumer habits also help animal-based proteins segment growth. Fitness enthusiasts and athletes often pick animal-based proteins for their performance benefits.

Plant based protein segment account for the second largest market share in 2025 and are expected to register a growth rate of 8.57% CAGR during the forecast period. Consumers are choosing plant based alternatives and vegetarian diets due to rising concerns about the environment. Soy, pea, and rice proteins are becoming more popular choices.

By Distribution Channel

To know how our report can help streamline your business, Speak to Analyst

High Consumer Trust and Wide Product Availability Leads to Supermarkets & Hypermarkets Segment Dominance

The market is segmented, by distribution channel into supermarkets & hypermarkets, online retail, convenience stores, specialty nutrition / health stores and pharmacies & drug stores.

The supermarkets & hypermarkets segment led the global market in 2025. They offer a wide range of products, have strong consumer trust, and attract many shoppers. These stores allow consumers to compare different brands, check nutrition labels, and choose products that suit their specific needs. Their strong supply chains and presence in many locations also help them stay ahead in both developed and emerging markets.

Online retail segment account for the second largest market share in 2025 and are expected to register a growth rate of 9.13% CAGR during the forecast period. This is driven by convenience, wider product assortment, and growing digital adoption. However, lack of physical inspection, delivery timelines, and trust concerns in certain regions limit their dominance compared to offline retail formats.

High Protein Food Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

North America High Protein Food Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market is valued at USD 13.33 billion in 2025. The region is growing quickly, as protein rich product are gaining popularity among consumers. China, India, and Japan are major markets, and demand for both animal and plant-based proteins is rising in these countries. Growth in food processing and shifts in eating habits are speeding up the adoption of protein products. Expansion of sports activities among young population is also boosting protein rich food demand in the region.

India High Protein Food Market

The India market in 2025 was around USD 1.65 billion, accounting for roughly 3.21% of global market revenues.

China High Protein Food Market

China’s market in 2025 was around USD 3.07 billion, representing roughly 5.97% of global high protein foods market share. Consumers are looking for sports nutrition and foods with extra protein, which is helping the market grow. Retail stores and online shopping are making these products easier to find.

Japan High Protein Food Market

The Japan market in 2025 reached around USD 1.90 billion, accounting for roughly 3.70% of global market revenues.

North America

The market in North America reached USD 18.22 billion in 2025 and is the leading region in the world. This is driven by strong consumer awareness of fitness, weight management, and active lifestyles. The U.S. leads with high demand for protein bars, beverages, and supplements, supported by a well-established sports nutrition industry. The region benefits from strong retail distribution, innovation, and presence of key market players. Additionally, increasing adoption of plant-based proteins is shaping regional market growth.

U.S. High Protein Food Market

In 2025, the U.S. market reached USD 14.97 billion. The U.S. leads the regional market, supported by strong fitness culture and high consumer awareness. Demand for protein bars, beverages, and protein supplements is high, driven by weight management and sports nutrition trends. The market benefits from continuous product innovation and strong presence of global brands. Increasing demand for plant-based proteins is also shaping market dynamics.

Europe

The European market was valued at USD 15.09 billion in 2025. Europe is a well-established market that continues to grow, as more people are focusing on health and looking for clean-label, high-protein products. Germany, the U.K., and France play major roles in this market. There is also a growing demand for plant-based and sustainable protein sources in the region. Strict regulations help maintain product quality however the commercialization of such products is slowed down.

Germany High Protein Food Market

The market in Germany, in 2025 reached around USD 2.58 billion, representing roughly 5.01% of global market revenues. The growth of this market is driven by rising health awareness and demand for clean-label and sustainable products.

U.K. High Protein Food Market

U.K. market reached USD 2.11 billion in 2025, equivalent to around 4.11% of global market sales.

South America and Middle East and Africa

Over the forecast period, South America is expected to experience significant growth in this market. The South America market in 2025 recorded USD 2.07 billion. The market is seeing steady growth, and increasing number of young consumers are showing interest toward fitness and nutrition products. Brazil and Argentina are important markets, with more people looking for protein supplements and fortified foods. Middle East & Africa region reached USD 2.68 billion in 2025. This market is growing and gulf countries including the UAE and Saudi Arabia play a major role as people there have more disposable income. Improving retail infrastructure and focusing on wellness are expected to support market development.

UAE High Protein Food Market

UAE market is set to grow at a CAGR of 6.91% during the forecast period. Expansion of packaged protein snacks and supplements is supporting growth. Increasing penetration of e-commerce and growing middle-class population are expected to accelerate market adoption.

COMPETITIVE LANDSCAPE

Key Industry Players

Increasing Product Innovations are Intensifying Market Competition

The high-protein food market is very competitive and divided, with large global companies, specialized nutrition brands, and new startups all competing in different product categories. Major companies including Nestlé S.A., Danone S.A., PepsiCo, Inc., Glanbia plc, and Abbott Laboratories use their strong brands, wide distribution, and ongoing product innovation to stay ahead. These companies focus on expanding portfolios in protein bars, beverages, dairy, and plant-based products. These companies are also investing into research and development to improve taste, texture, and nutrition.

LIST OF HIGH PROTEIN FOOD COMPANIES PROFILED

- Nestlé S.A. (Switzerland)

- Danone S.A. (France)

- Glanbia plc (Ireland)

- PepsiCo, Inc. (U.S.)

- General Mills, Inc. (U.S.)

- Quest Nutrition LLC (U.S.)

- Abbott Laboratories (U.S.)

- Active Nutrition International GmbH (Switzerland)

- Grupo Bimbo (Mexico)

- Britannia Industries (India)

KEY INDUSTRY DEVELOPMENTS

- February 2026: ChunkyFit, a soft-baked protein cookie brand, launched a reformulated cookie recipe across its full product line. The new product lineup includes Classic Chocolate Chip, Cookie Monster, Cookie Butter, Funfetti, and Nutty N’ Nice, which contains a high amount of protein, 16 grams.

- January 2026: Bimbo Bakeries launched a high protein bread loaf in the market. The product is packed with 22 Grams of Protein Per Serving.

- January 2026: Zydus Wellness launched a new high-protein bar in the market named RiteBite Max Protein. The bar is made of 10 gm of protein and millets targeted towards health-conscious consumers.

- October 2024: Chobani launched high-protein-based food products such as Greek yogurt cups and drinkables in the market. The product is lactose-free with no added protein powders.

- August 2021: Danone’s Silk launched new plant-based Greek yogurt in the U.S. market. This plant-based yogurt is available in four varieties, namely Strawberry, Blueberry, Vanilla, and Lemon.

REPORT COVERAGE

The global high protein food market research provides an in-depth study of market sizes & forecast by all the market segments included in the report. The market analysis includes details on the market dynamics and market trends expected to drive the market forecast. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market report also encompasses detailed competitive landscape with information on the market segmentation, market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.37% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, By Source, By Form, By Distribution Channel, By Storage Condition and Region |

| By Product Type |

|

| By Source |

|

| By Form |

|

| By Distribution Channel |

|

| By Storage Condition |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 51.39 billion in 2025 and is projected to reach USD 105.34 billion by 2034.

In 2025, the North America market value stood at USD 18.22 billion.

The market is expected to exhibit a CAGR of 8.37% during the forecast period

By distribution channel, supermarkets & hypermarkets segment led the global market.

Rising health, fitness, and weight management awareness accelerating demand for high-protein foods.

Nestlé S.A., Danone S.A., PepsiCo, Inc., Glanbia plc, and Abbott Laboratories are a top players in the market.

North America held the largest market share.

Shift toward plant-based, clean-label, and on-the-go protein products driving market innovation.

- 2021-2034

- 2025

- 2021-2024

- 180

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us