Hispanic Foods Market Size, Share & Industry Analysis, By Consumer Type (Hispanic Households and Mainstream Non-Hispanic), By Format (Ambient/Shelf-Stable, Refrigerated, and Frozen), By Product Type (Core Staple Foods, Sauces & Condiments, Prepared & Ready-to-Eat, Snacks, and Others), By Distribution Channel (Supermarkets & Hypermarkets, Mass Merchandisers, Online/D2C, and Others), and Regional Forecast, 2026-2034

(Offer valid till 30th Jun 2026)

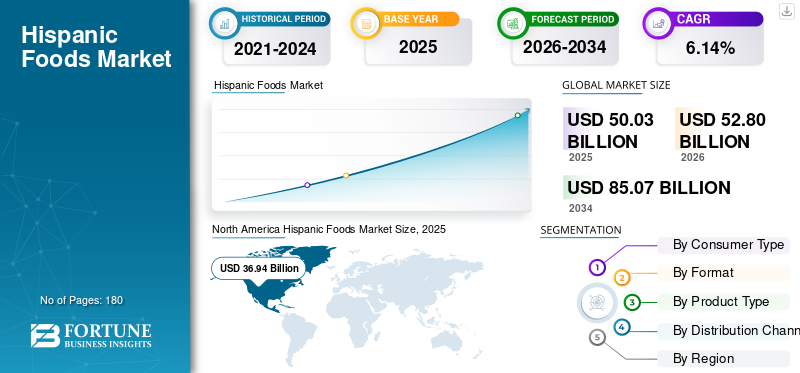

Hispanic Foods Market Size and Future Outlook

The global hispanic foods market size was valued at USD 50.03 billion in 2025. The market is projected to grow from USD 52.80 billion in 2026 to USD 85.07 billion by 2034, exhibiting a CAGR of 6.14% during the forecast period. North America dominated the hispanic foods market with a market share of 73.83% in 2025.

Hispanic foods are packaged and prepared products based on Latin American cooking traditions, especially Mexican and Tex-Mex cuisine. Examples include tortillas, salsas, beans, seasoning mixes, frozen burritos, and related staple products. These products are marketed based on their Hispanic flavors and cooking styles. The market is growing quickly as Hispanic populations increase in major economies, increasing consumer interest in bold and diverse global flavors, and rising demand for convenient meal solutions. In emerging markets, the expansion of modern retail channels is also transforming traditional, informal eating habits into packaged product sales. Additionally, the introduction of premium product lines, clean-label formulations, and plant-based options is helping manufacturers attract new consumer segments in North America and other markets beyond traditional ethnic segments present in South America and Mexico.

Companies such as Grupo Bimbo, Hormel Foods Corporation, and B&G Foods are some of the key players operating in this market. Product Line expansion is the key strategy adopted by companies, which is boosting product sales and supporting market growth.

Download Free sample to learn more about this report.

HISPANIC FOODS MARKET TRENDS

Increasing Popularity of Private-Label Brands to Boost Market Expansion

The global market for the Hispanic food industry is changing rapidly as these products become more mainstream and available in a wider range of formats. Private-label brands are gaining traction, especially in Europe, increasing price competition and improving accessibility for a broader consumer base. More companies are offering clean-label, plant-based versions of Hispanic foods, a trend especially strong in North America. Additionally, cross-cultural fusion products are emerging as a key trend, blending Hispanic flavors with Asian and Mediterranean profiles to drive consumer experimentation and expand usage occasions.

MARKET DYNAMICS

MARKET DRIVERS

Rising Hispanic Population to Fuel Industry Expansion

Growth in the global Hispanic packaged foods market is mainly driven by population growth and increased consumption of Hispanic cuisine. In North America, the growing Hispanic population, younger age groups, and higher food spending are driving steady demand for staples and sauces. At the same time, adoption among non-Hispanic consumers is increasing, with Mexican and Tex-Mex flavors becoming part of everyday meal choices. As a result, these products are not limited to ethnic aisles and are now widely available across mainstream retail channels. Moreover, frozen and convenient food options are becoming more popular as it is convenient option for consumers who have limited time to cook food at home.

MARKET RESTRAINTS

Increasing Import Dependence to Hinder Market Growth

A key challenge for the global Hispanic packaged foods market is that most products fall into just a few categories and are not widely available across regions. In addition, limited local manufacturing capacity in regions such as Europe, Asia, and the Middle East & Africa is increasing reliance on imports. This dependence increases supply chain risks and complicates regulations, slowing growth even when demand is high.

MARKET OPPORTUNITIES

Growing Popularity of Mexican and Tex-Mex Flavors to Present Key Growth Opportunities

A significant opportunity for the Hispanic foods market lies in expanding beyond North America through premiumization and localized product adaptation. Mexican and Tex-Mex flavors are becoming more popular in Europe, Asia Pacific, and the Middle East, creating opportunities for products that blend authentic flavors with local culinary preferences. Offering more frozen meals, plant-based Hispanic proteins, and clean-label tortillas can help attract customers willing to pay a premium for quality and health-oriented options.

As modern retail grows in South America and Mexico, there is an opportunity to turn informal food purchases into branded packaged products. Working with local food manufacturers can lower import needs, make pricing more competitive, and help Hispanic foods reach more customers in new markets.

Download Free sample to learn more about this report.

Segmentation Analysis

By Consumer Type

Hispanic Households Segment Led due to Population Growth

The market is segmented by consumer type into hispanic households and mainstream non-hispanic.

The hispanic households segment held the largest Hispanic foods market share in 2025. Hispanic households are the main consumers in the retail Hispanic packaged foods market, as these foods are a regular part of their diets, and they purchase across a wide range of product categories.

Products such as tortillas, cooking sauces, beans, and traditional dairy items are everyday meal-preparation staples, not just occasional purchases. More Hispanic households buy these products, often across different types, leading to higher total spending. Cultural traditions passed down through generations keep demand steady, while population growth in key markets such as the U.S. continues to support overall sales. Due to these habits, Hispanic households are the main source of value for this product category.

Mainstream non-Hispanic consumers hold the second-largest share of the market and are expected to grow at a CAGR of 6.49% during the forecast period. Hispanic flavors have become part of everyday meals, especially in North America and some areas of Europe. This trend has helped these flavors reach more households beyond just Hispanic communities.

By Format

Ambient/ shelf-stable Segment Led the Market, Driven by Longer Shelf Life

Based on format, the market is segmented into ambient/shelf-stable, refrigerated, and frozen.

Ambient/ shelf-stable held the largest market share in 2025. Ambient and shelf-stable products lead the retail Hispanic packaged foods market as they are the main choice in key categories such as tortillas, dry beans, rice, sauces, seasoning mixes, and snacks. These products last longer, are easier to distribute, and can reach more areas, especially where stores depend on imports. Shelf-stable products suit shoppers who prefer to stock up and look for value, making them popular in both established and growing markets. Retailers give these products a lot of space in central store aisles, which helps shoppers notice them and buy them again, supporting the overall value of the category.

Frozen foods make up the second-largest share of the market and are expected to grow at a CAGR of 5.95% during the forecast period. This growth is largely driven by demand for easy meal options such as burritos, enchiladas, and ready-to-heat Tex-Mex dishes. Frozen foods also allow companies to create new products, such as bundled meals and portion-controlled options, which can be sold at higher prices than basic staples. However, Hispanic frozen foods are still growing, supported by the expansion of modern retail formats and increasing consumer preference for convenience.

By Product Type

Core Staples Foods segment Dominated as they are the Foundation of Daily Meals

By product type, the market is segmented into core staple foods, sauces & condiments, prepared & ready-to-eat, snacks, and others.

The core staple foods segment led the global market in 2025. Core staple foods are the top-selling products in the retail Hispanic packaged foods market as they are the foundation of daily meals. Products such as tortillas, rice, and packaged beans are often purchased by many people, especially in Hispanic households, as part of their regular shopping. Across regions, in many areas, even where Hispanic food is just becoming popular, tortillas and similar staples are usually the first products people try in this category.

The sauces & condiments segment accounted for the second-largest market share in 2025 and is expected to register a CAGR of 6.14% during the forecast period. Salsa, enchilada sauces, and seasoning mixes are easy to add to regular meals, which helps people from different backgrounds start using them quickly. In new markets, sauces usually become popular before staple foods. In established markets, they help brands offer higher-end products and drive innovation.

To know how our report can help streamline your business, Speak to Analyst

By Distribution Channel

Supermarkets & Hypermarkets Segment Led owing to their Wide Selection

The market is segmented by distribution channel into supermarkets & hypermarkets, mass merchandisers, online/D2C, and other.

The supermarkets & hypermarkets segment led the global market in 2025. Supermarkets and hypermarkets are the main way Hispanic packaged foods reach customers. Their wide selection, large number of shoppers, and big share of grocery spending make them the top choice for retailers. These stores offer plenty of shelf space for staples, sauces, snacks, frozen meals, and specialty items. This helps shoppers witness all their options and makes it easier for stores to promote different products together.

The mass merchandisers segment accounted for the second-largest market share in 2025 and is expected to register a CAGR of 6.30% during the forecast period. Their success is driven by low pricing, selling in bulk, and being located in busy suburban areas. Large-format retailers use their scale to maintain competitive prices on items such as tortillas, sauces, and snack multipacks, attracting shoppers who are looking for good value.

Hispanic Foods Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

North America Hispanic Foods Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market was valued at USD 2.23 billion in 2025. The region is a developing and diverse market, where Hispanic packaged foods are still a small but growing segment. Most of the demand comes from Japan, Australia, China, and South Korea, where supermarkets and city retail centers are the main places these products are sold. Sauces and snacks are usually the first Hispanic foods people try. In places such as China and Singapore, online shopping is especially important as these markets rely more on imports. People are not very familiar with traditional Hispanic foods, which makes it harder for these products to become more popular. However, as more people try Western cuisine and modern retail options expand, Hispanic foods are witnessing steady growth in cities.

Singapore Hispanic Foods Market

The Singapore market in 2025 was valued at around USD 0.16 billion, accounting for roughly 0.31% of global market revenues.

China Hispanic Foods Market

China’s market in 2025 was valued at around USD 0.52 billion, representing roughly 1.03% of the global Hispanic foods market share. China is still an emerging market, and most Hispanic packaged foods are found in Tier 1 cities. Sauces and snacks are the most popular choices for new buyers; however, staples and frozen foods are consumed in limited quantities.

Japan Hispanic Foods Market

The Japanese market in 2025 reached a valuation of around USD 0.46 billion, accounting for roughly 0.92% of global market revenues.

North America

The market in North America reached a valuation of USD 36.94 billion in 2025, making it the leading region in the world. North America is the biggest market for retail Hispanic packaged foods, mainly driven by the large Hispanic population in the U.S. Core staples and sauces anchor category value, while frozen and convenience formats contribute incremental growth. Modern stores, plenty of shelf space, and private label brands help the market grow and mature. Mexico’s retail market also strengthens the region’s overall position.

U.S. Hispanic Foods Market

In 2025, the U.S. market reached USD 22.72 billion. The U.S. is the world’s largest market, due to a large Hispanic population and broad acceptance among mainstream consumers. Basic staples and sauces drive core value, while frozen foods and convenience products contribute to further growth. Most products are sold through supermarkets and large retail chains. The rise of premium products and store brands is reshaping competitive dynamics in the market.

Europe

The European market reached a valuation of USD 4.27 billion in 2025. Europe is a mid-sized market that is steadily growing. Sauces and meal kits are the main categories that introduce shoppers to Hispanic foods. Shelf-stable products are the most common, as most items are imported, and there is limited local production of fresh or refrigerated options. Although Hispanic foods are less common than in North America, growing interest in global cuisine and increased product variety in retail stores are slowly supporting sales growth across major Western European countries.

Germany Hispanic Foods Market

The market in Germany in 2025 reached around USD 0.55 billion, representing roughly 1.09% of global market revenues. Germany is the leading market owing to strong supermarket sales and the popularity of Hispanic cuisine. The market relies heavily on imports, while private label brands are becoming more common. Growth remains steady, supported by increasing adoption of global flavor.

U.K. Hispanic Foods Market

The U.K. market reached approximately USD 0.74 billion in 2025, equivalent to around 1.48% of global market sales.

South America and the Middle East & Africa

South America is expected to hold significant growth in this market over the forecast period. The South American market in 2025 recorded a value of USD 5.56 billion. In South America, the retail market is moderate in size. While Hispanic cuisine is widely consumed throughout the region, Mexican-style and Tex-Mex products fill a specific niche in grocery stores. Growth is driven by the expansion of modern retail and a slow move toward premium products; however, informal food sales and price concerns limit packaged category growth. The Middle East & Africa region reached a valuation of USD 1 billion in 2025. The market remains relatively small; however, strong demand for premium imported products makes it significant. Most sales from Gulf Cooperation Council countries, mainly the United Arab Emirates and Saudi Arabia. These markets benefit from large expatriate communities and established hypermarket networks.

UAE Hispanic Foods Market

The UAE market is set to grow at a CAGR of 4.69% during the forecast period. The UAE is the leading market owing to a strong demand from expatriates and well-developed hypermarkets. Sauces, snacks, and frozen foods are the most common products, with most items being imported. Online grocery shopping is also more popular in the UAE compared to many other places.

COMPETITIVE LANDSCAPE

Key Industry Players

New Product Launch in Innovative Packages to Meet Product Demand

The global market has two main structural segments. In North America, a few companies dominate the market, while in other regions, the market is more fragmented. Limited multinational companies control a significant share of key product categories such as tortillas, tacos, burritos, enchiladas, and other products. In Europe, Asia Pacific, and the Middle East & Africa, global brands compete with local distributors and specialty importers. The market is less concentrated and more affected by logistics challenges. Barriers to entering the market are moderate. Companies are undertaking product innovation initiatives and launching new products in innovative packages to meet the growing demand for Hispanic food products in emerging markets.

LIST OF HISPANIC FOODS COMPANIES PROFILED IN THE REPORT

- Grupo Bimbo (Mexico)

- Gruma, S.A.B. de C.V. (Mexico)

- Grupo Herdez (Mexico)

- B&G foods (U.S.)

- General Mills (U.S.)

- Campbell Soup Company (U.S.)

- Hormel Foods Corporation (U.S.)

- Goya Foods, Inc. (U.S.)

- La Costeña (Mexico)

- MegaMex Foods (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Cornitos, a top Indian brand known for its nacho crisps and snacks, introduced two new Tortilla Wrap flavors: Spinach and Multigrain. The new wraps offer both good nutrition and great taste. They are suitable for preparing quesadillas, burritos, veggie wraps, DIY tacos, and others.

- September 2025: Frozen Mexican food brand José Olé launched new Premium Taquitos, which are available in Birria Beef and Pollo Asado at retailers in the U.S. market. These product varieties contain no artificial flavors or colors.

- February 2025: Baja Foods strategically expanded its retail presence and launched a new premium brand, namely Chef Gustavo. The first product launched is Chicken & Cheese Enchiladas with Salsa Verde, which is composed of antibiotic-free shredded white meat chicken, corn tortillas, and other ingredients.

- February 2025: Ruiz Food Products, Inc., launched a new national advertising campaign to attract consumers and increase the sales of its Mexican food products.

- October 2024: Nestlé launched new frozen brands focused on Mexican and Asian cuisines, which are specifically tailored for consumers opting for ethnic Mexican meals. The products are targeted toward younger consumers who are increasingly looking for bolder flavors and more diverse food options found in global cuisine.

REPORT COVERAGE

The global Hispanic foods market forecast provides an in-depth study of market size & forecast by all the market segments included in the report. The market analysis includes details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on market insights, technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The industry also encompasses a detailed competitive landscape with information on the market segmentation, market share, and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.14% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Consumer Type, By Format, By Product Type, By Distribution Channel, and Region |

| By Consumer Type |

|

| By Format |

|

| By Product Type |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 50.03 billion in 2025 and is projected to reach USD 85.07 billion by 2034.

In 2025, North Americas market value stood at USD 36.94 billion.

The market is expected to exhibit a CAGR of 6.14% during the forecast period.

By format, the ambient/shelf-stable support segment led the global market in 2025.

The rising Hispanic population is the key factor driving the market.

Grupo Bimbo, Hormel Foods Corporation, and B&G Foods are a few of the players in the market.

North America held the largest market share in 2025.

The increasing popularity of private-label brands is the major market trend.

- 2021-2034

- 2025

- 2021-2024

- 180

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us