HVAC Sensors Market Size, Share & Industry Analysis, By Sensor Type (Temperature Sensors, Humidity Sensors, Pressure Sensors, Smoke & Gas Sensors, and Others), By Application (Residential HVAC Systems, Commercial HVAC Systems, and Industrial HVAC Systems), By Installation Type (Duct-Mounted Sensors, Wall-Mounted Sensors, and Outdoor Sensors), By Technology (Wired Sensors and Wireless Sensors (Wi-Fi, Bluetooth Low Energy (BLE), NB-IoT, LoRaWAN, and Zigbee)), By End-Use Industry (Building Automation, Data Centers, Automotive, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

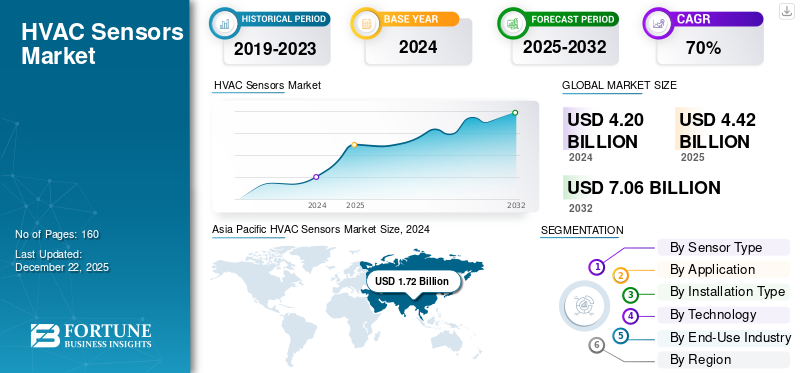

The global HVAC sensors market size was valued at USD 4.42 billion in 2025. The market is projected to grow from USD 4.67 billion in 2026 to USD 7.94 billion by 2034, exhibiting a CAGR of 6.85% during the forecast period. The Asia Pacific dominated the global market, accounting for a 40.95% share in 2025.

HVAC stands for Heating, Ventilation, and Air Conditioning. The industry often uses sensors to maintain thermal comfort. These HVAC sensors monitor and regulate various functions, including air temperature, pressure, and quality in commercial, industrial, and residential HVAC systems.

The rapid expansion of industrialization and urban development across the globe is a key factor propelling the market's growth. Additionally, the increase in building of diverse commercial and residential properties globally creates a strong need for HVAC sensors utilized in heating and cooling systems, ventilation control, humidity regulation, and air purification, further propelling the market growth. For example, in 2023, the IEA reported that the value of the global building construction industry rose by 5% from the previous year, exceeding USD 6.3 trillion. These elements aid in the expansion of market share.

The COVID-19 pandemic boosted the demand for HVAC sensors focused on air quality and safety while contributing to increased costs and supply chain challenges. The pandemic accelerated the adoption of advanced sensor technologies in HVAC systems to improve ventilation, monitor air quality, and ensure safety with new refrigerants.

Download Free sample to learn more about this report.

IMPACT OF GENERATIVE AI

Integration of Generative AI with HVAC Sensors by Enhancing Capabilities to Fuel Market Growth

By frequently analyzing the data from sensors and modifying system outputs accordingly, generative AI enhances energy efficiency. For instance, it reduces heating or cooling levels when fewer people are around, resulting in a smaller environmental impact and significant cost savings. Furthermore, gen AI enables detailed testing and calibration of HVAC sensors.

IMPACT OF RECIPROCAL TARIFFS

The effect of reciprocal tariffs has brought considerable difficulties and changes in strategies within the HVAC sensors sector, mainly for manufacturers and integrators dependent on global supply chains. Additionally, system integrators focus on reducing risks by managing inventory effectively and increasing the number of suppliers.

MARKET DYNAMICS

HVAC Sensors Market Trends

Increased Integration of IoT with HVAC Sensors to Emerge as a Key Market Trend

HVAC sensors are transformed by IoT devices, offering connectivity and communication flows. These IoT-enabled sensors enable remote monitoring and control, onsite immediate insight, and diagnostic capabilities. IoT allows predictive maintenance to sense issues building up before they are magnified, thus making the system operational.

Market Drivers

Rising Popularity of Smart Homes to Aid Market Growth

A smart home uses internet-connected devices to track and manage homes by maintaining different aspects such as heating, air conditioning, and lighting. The benefits of a smart home include energy efficiency, better aesthetics, and easy user operation. Smart home technology enhances both reliability and precision. The total energy use, carbon dioxide emissions, and operational expenses of residential, commercial, and industrial buildings are directly influenced by the quality of the HVAC setup and its incorporation into the sensor network. According to the U.S. Department of Energy, smart home technology can lead to over a 60% reduction in energy consumption in residential homes and around 59% in commercial properties. Consequently, the rising popularity of smart homes is fostering the HVAC sensors market growth.

Market Restraints

Technical and Packaging Issues to Hinder Market Expansion

Making small, tough, and cheap sensors for HVAC uses, particularly MEMS-based differential pressure sensors, faces issues in packaging, material selection, and environmental protection. These technical issues can slow the market growth by increasing development costs and making the sensors less reliable.

Market Opportunities

Increasing Demand for BEMS for Building Operations to Create Lucrative Market Opportunities

HVAC sensors are essential for building operations despite their high costs. According to the Australian Department of Climate Change, Energy, the Environment, and Water, an average HVAC system accounts for approximately 40% of a building's total energy use and 70% of its baseline energy consumption. Building Energy Management Systems (BEMS), which are automated systems powered by computers, monitor and manage all energy-related systems within the buildings, including mechanical and electrical components. Energy management protects businesses from unnecessary energy expenses by facilitating accurate and automated control over energy systems and supply.

SEGMENTATION ANALYSIS

By Sensor Type

Rapid Adoption of IoT and Industry 4.0 Boosted Temperature Sensors Segment Growth

Based on sensor type, the market is segmented into temperature sensors, humidity sensors, pressure sensors, smoke & gas sensors, occupancy & motion sensors, and others.

The temperature sensors segment dominated the market share 32.98% in 2026 due to the increasing adoption of IoT, Industry 4.0, wearable technologies, and smart home devices, which require precise temperature monitoring and control.

The smoke & gas sensors segment is anticipated to experience the highest compound annual growth rate (CAGR) during the forecast period. The segment growth is due to increased indoor air quality and safety awareness, with advanced multi-gas and particulate sensors becoming more common in smart home and industrial applications.

By Application

Increasing Demand for Energy Efficiency Fueled Demand for Residential HVAC Systems

Based on application, the market is segmented into residential HVAC systems, commercial HVAC systems, and industrial HVAC systems.

The residential HVAC systems segment registered the highest revenue in 2026,with a share of 50.60% driven by the growing demand for energy efficiency, smart home adoption, and indoor air quality concerns.

The commercial HVAC systems segment is anticipated to register the highest CAGR during the forecast period. This growth is driven by increasing construction and retrofit activities, especially in emerging markets where urbanization and government housing initiatives boost demand for HVAC components.

By Installation Type

Rising Need to Save Energy in Buildings Boosted Demand for Duct-mounted Sensors

Based on installation type, the market is segmented into duct-mounted sensors, wall-mounted sensors, and outdoor sensors.

The duct-mounted sensors segment held the largest market share in 2026 due to rising energy costs and the push for energy-efficient buildings. Duct-mounted sensors enable precise airflow, temperature, humidity, and air quality monitoring, thus optimizing HVAC sensor performance and reducing energy consumption.

The outdoor sensors segment is anticipated to register the highest CAGR during the forecast period. The integration of IoT and smart building technologies is increasing the adoption of outdoor sensors in the market.

By Technology

Wired Segment Dominated Market Owing to Its Exceptional Capabilities

Based on technology, the market is categorized into wired sensors and wireless sensors.

The wired segment dominated the market in 2024, as it fulfills industrial demand and reliability requirements. This segment remains essential for sensors' stability, integration, and industrial-grade performance. These sensors minimize signal interference and power variability mainly for industrial, automation, data centers, etc. Also, it provides enhanced security as compared to wireless.

The wireless segment is expected to record the highest CAGR during the forecast period due to the rising need to retrofit existing systems with minimal disruption. Moreover, wireless sensors reduce downtime in industrial HVAC units.

By End-Use Industry

Building Automation Segment Dominated Market Due to Its Improved Benefits

Based on end-use industry, the market is categorized into building automation, data centers, automotive, healthcare, food & beverage, and others.

The building automation segment held the largest HVAC sensors market share in 2024. HVAC sensors are used in building automation and produce data to control a building's heating, cooling, ventilation, and air quality systems. When integrated into building automation systems, these sensors lead to improved occupant comfort, reduced energy consumption, and enhanced reliability of building systems.

The healthcare segment is expected to register the highest CAGR during the forecast period. It emphasizes the need for environmental control to ensure patient safety, investor/operator efficiency, and compliance with medical standards. These sensors help maintain sterile environments, improving patient outcomes within healthcare facilities.

To know how our report can help streamline your business, Speak to Analyst

HVAC SENSORS MARKET REGIONAL OUTLOOK

Based on geography, the market is divided into Europe, South America, North America, Asia Pacific, and the Middle East & Africa.

Asia Pacific

Asia Pacific HVAC Sensors Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region captured 40.95% of the global market in 2025, generating USD 1.81 billion in revenue, and is projected to reach USD 1.91 billion in 2026, driven by ongoing construction projects in Japan, India, and China, along with growing consumer spending on high-end products. Increasing disposable income and low ownership rates in Asia are likely to support the market expansion. The residential sector has captured a substantial market share due to heightened demand from India and China.The Japan market is projected to reach USD 0.43 billion by 2026, the China market is projected to reach USD 0.67 billion by 2026, and the India market is projected to reach USD 0.26 billion by 2026.

Download Free sample to learn more about this report.

China's urbanization has led to increased demand for HVAC sensor installations. This fuels the construction activity and the need for advanced HVAC solutions, including smart sensors and controls integrated with IoT and AI technologies for energy efficiency and indoor air quality management.

To know how our report can help streamline your business, Speak to Analyst

South America

The South American market is experiencing steady growth due to recent shifts in the local economy and enhanced government funding for research initiatives.

Europe

In 2025, the Europe market stood at USD 0.94 billion, representing 21.24% of global demand, and is projected to grow to USD 1 billion in 2026. Europe is estimated to grow at the highest rate during the forecast period. The rapid uptake of HVAC sensors in different environments and the automotive industry is driving market expansion in the region. Additionally, the creation of innovative sensors by firms to enhance the performance of HVAC systems contributes to market growth.The UK market is projected to reach USD 0.21 billion by 2026, while the Germany market is projected to reach USD 0.2 billion by 2026.

Middle East & Africa

In 2025, Middle East & Africa generated USD 0.19 billion, contributing 4.36% to global market revenue, and is projected to grow to USD 0.2 billion in 2026. The Middle East & Africa region has a smaller market presence. Expanding construction and infrastructure projects have created a positive impact, while economic diversification could be challenging.

North America

North America contributed approximately USD 1.34 billion to the global market in 2025, accounting for 30.36% share, and is expected to reach USD 1.42 billion in 2026. The North American market is witnessing substantial growth opportunities driven by urbanization, technological innovation, energy efficiency mandates, and increasing demand for smart, connected HVAC systems in new and retrofit applications. The U.S. market is experiencing strong growth due to the rising adoption of energy-efficient HVAC systems, driven by regulatory mandates and consumer demand for lower energy costs.The U.S. market is projected to reach USD 1.07 billion by 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Adopt Merger & Acquisition, Partnership, and Product Development Strategies to Expand their Business Reach

Companies operating in the HVAC market provide advanced HVAC sensors to improve the system performance and energy efficiency. They focus on signing acquisition agreements with small and local firms to increase their business operations. Moreover, partnerships, mergers & acquisitions, and key investment strategies will boost the demand for this technology.

List of Key HVAC Sensor Companies Profiled

- Honeywell International Inc. (U.S.)

- Johnson Controls International plc (Ireland)

- Siemens AG (Germany)

- Schneider Electric SE (France)

- Emerson Electric Co. (U.S.)

- Sensirion AG (Switzerland)

- Amphenol Corporation (U.S.)

- TE Connectivity Ltd. (Switzerland)

- Belimo Holding AG (Switzerland)

- Danfoss A/S (Denmark)

- Rotronic AG (Switzerland)

- Testo SE & Co. KGaA (Germany)

- Soloon Actuators (China)

- Microchip Technology Inc. (U.S.)

- Trane Technologies (Ireland)

- Mitsubishi Electric Corporation (Japan)

- Variohm Eurosensor Ltd (England)

- CHINO Corporation (Japan)

- Asahi Denso (Japan)

- Kawaso Electric Industrial Co., Ltd (Japan)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Sensirion extended its manufacturing facility in Hungary. The newly built section provides approximately 7,000 square meters of area for logistics and manufacturing. This expansion increases the ability to produce sensor modules aligned with Sensirion's expansion goals.

- August 2024: Senseair, a subsidiary of Asahi Kasei Microdevices (AKM) based in Sweden, created "Sunlight R290," a gas sensor known for its high accuracy in measurements and wide operating range, while reducing heat output, packaging requirements, and energy consumption.

- July 2024: The Bosch Group acquired the global HVAC solutions division for residential and light commercial properties from Johnsons Controls. Additionally, Bosch plans to fully purchase the Johnson Controls-Hitachi Air Conditioning (JCH) joint venture, which encompasses Hitachi's 40 percent share.

- September 2023: Belimo, manufacturer of field devices for the energy-efficient management of HVAC systems, launched its RetroFIT+ program aimed at helping customers optimize building efficiency as a step toward a greener future.

- May 2023: Johnson Controls expanded its portfolio of tools for residential and commercial contractors by introducing the new Johnson Controls Ducted Systems (DS) Solutions App. This free app provides contractors quick access to commercial and residential equipment details to help make installation, troubleshooting, and maintenance tasks easier.

INVESTMENT ANALYSIS AND OPPORTUNITIES

This market offers promising investment opportunities driven by technological advancements and increasing automation across various sectors. Key players invest heavily in R&D to develop smart, IoT-enabled sensors that provide real-time data analytics, predictive maintenance, and enhanced energy efficiency. This could provide strategic advantages in the field.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects, such as leading companies, products/types, and the leading end-use industry of the product. Besides, it offers insights into the market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.85% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Sensor Type

By Application

By Installation Type

By Technology

By End-Use Industry

By Region

|

|

Companies Profiled in the Report |

Honeywell International Inc. (U.S.) Johnson Controls International plc (Ireland) Siemens AG (Germany) Schneider Electric SE (France) Emerson Electric Co. (U.S.) Sensirion AG (Switzerland) Amphenol Corporation (U.S.) TE Connectivity Ltd. (Switzerland) Belimo Holding AG (Switzerland) Danfoss A/S (Denmark) |

Frequently Asked Questions

The market is projected to reach a valuation of USD 7.94 billion by 2034.

In 2025, the market was valued at USD 4.42 billion.

The market is projected to record a CAGR of 6.85% during the forecast period.

By sensor type, the temperature sensors segment led the market in 2025.

The rising popularity of smart homes is aiding market growth.

Honeywell International Inc., Johnson Controls International plc, Siemens AG, Schneider Electric SE, Emerson Electric Co., Sensirion AG, Amphenol Corporation, TE Connectivity Ltd., Belimo Holding AG, and Danfoss A/S are the top players in the market.

Asia Pacific held the highest market share in 2025.

By end-use industry, the healthcare segment is expected to record the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us