Hydroquinone Market Size, Share & Industry Analysis, By Grade (Industrial Grade, High Purity Grade, and Others), By End Use (Plastics, Rubber & Tire, Chemical, Photography & Imaging, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

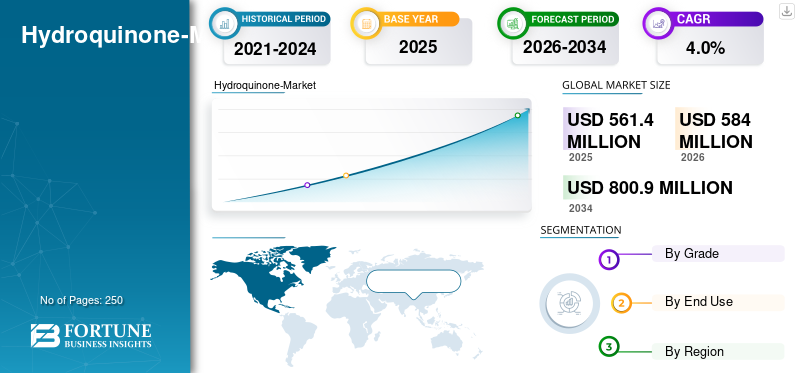

The global hydroquinone market size was valued at USD 561.4 million in 2025. The market is projected to grow from USD 584.0 million in 2026 to USD 800.9 million by 2034, exhibiting a CAGR of 4.0% during the forecast period. Asia Pacific dominated the global hydroquinone market with a market share of 50.94% in 2025.

Hydroquinone (HQ) is an essential aromatic organic compound belonging to the dihydroxybenzene family, valued for its strong reducing properties, high purity potential, and effectiveness as a polymerization inhibitor, antioxidant, and chemical intermediate. With excellent reactivity, stability, and compatibility across monomers, elastomers, and specialty chemicals, hydroquinone plays a critical role in stabilizing acrylates, methacrylates, styrene, and vinyl monomers production. Its antioxidant behavior makes it a key additive in rubber & tire manufacturing, where it helps prevent premature crosslinking and improves processing stability. The growing production of high-performance plastics, sustained expansion of rubber & tire manufacturing in Asia, and strong demand for chemical intermediates are expected to support market growth over the forecast period.

The industry is shaped by a mix of multinational and regional producers, including Solvay, Eastman Chemical Company, Camlin Fine Sciences, Global Calcium, Jiangsu Sanjili Chemical, and other Asian and European specialty chemical suppliers. Continuous investments in production technologies, capacity debottlenecking, process optimization, and the introduction of ISCC-PLUS certified mass-balance are strengthening their competitive positioning.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Consistent Demand as a Polymerization Inhibitor and Antioxidant to Aid Market Growth

HQ remains a critical additive in global polymer, resin, and elastomer manufacturing due to its exceptional performance as a polymerization inhibitor and antioxidant. Its ability to stabilize polymers during production, transportation, and storage prevents premature polymerization, reduces processing losses, and improves operational safety. In rubber & tire applications, it acts as an effective antioxidant and anti-scorching agent, maintaining compound stability during mixing and curing. The sustained expansion of plastics, elastomers, adhesives, and synthetic rubber industries, particularly in Asia, continues to reinforce their indispensable role in modern chemical processing. Rising monomer throughput, growth in downstream applications such as automotive components and packaging, and increasing demand for stabilizer efficiency are further supporting product consumption. Therefore, the rising production of polymers and elastomers, along with the consistent demand for the product as a polymerization inhibitor and antioxidant to aid the global hydroquinone market growth.

MARKET RESTRAINTS

Regulatory Restrictions and Volatility in Phenol-Based Feedstock Costs to Restrain Market Growth

Several long-term regulatory and economic factors pose challenges to market expansion. Strict regulations and partial bans in cosmetic applications across North America, Europe, and other jurisdictions have significantly reduced demand for high-purity cosmetic-grade material. These restrictions stem from safety concerns related to prolonged dermal exposure, prompting manufacturers to reformulate personal care products or shift toward alternative depigmenting agents. At the same time, its production is highly sensitive to fluctuations in phenol and benzene prices, which form the backbone of the product’s manufacturing routes. Volatility in these feedstocks, driven by global energy markets, refinery economics, and crude oil fluctuations, directly influences production margins and price stability. Additionally, rising environmental compliance costs and tightening emissions standards increase operational overhead for producers. These combined regulatory and cost-side pressures are expected to restrain market growth over the medium term.

MARKET OPPORTUNITIES

Expansion of High-Purity and Pharmaceutical-Grade to Create Lucrative Avenues in the Market

The growing demand for high-purity and pharmaceutical-grade HQ presents a significant opportunity for market participants. It is a key intermediate in the synthesis of p-aminophenol (PAP), a critical raw material for paracetamol (acetaminophen) production. With global pharmaceutical consumption rising, especially in Asia, demand for high-purity is expected to grow. Additionally, HQ’s high-grade variants play an increasingly important role in fine chemicals, electronics, advanced imaging, and specialty intermediates where purity, consistency, and trace-metal control are essential. Manufacturers are expanding purification capabilities, adopting advanced crystallization and filtration technologies, and optimizing reaction pathways to meet tighter specifications. Regulatory-driven shifts in cosmetic and dermatology markets also open opportunities for compliant, ultra-high-purity production. As industries prioritize high-performance materials and pharmaceutical reliability, investments in specialty-grade product capacity will create lucrative growth avenues for producers worldwide.

HYDROQUINONE MARKET TRENDS

Shift Toward ISCC-PLUS Certified Mass-Balance and Low-Carbon HQ Grades to Shape Market Dynamics

A notable trend reshaping the market is the emergence of ISCC-PLUS certified, mass-balance, and low-carbon grades. Driven by growing sustainability mandates, corporate decarbonization targets, and customer expectations for environmentally responsible raw materials, producers are increasingly exploring renewable-feedstock pathways and lower-emission production models. Products such as certified HQ and Monomethyl Ether of Hydroquinone (MEHQ) offerings highlight the shift toward integrating biomass- or bio-naphtha-derived inputs into established production chains via mass-balance certification. These advancements enable downstream users in plastics, coatings, adhesives, and specialty chemicals to lower Scope 3 emissions without changing product performance or processing behavior. As global supply chains prioritize verifiable sustainability attributes, adoption of low-carbon and certified grades is expected to accelerate. This trend enhances brand differentiation and supports long-term compliance with emerging environmental regulations, positioning certified products as an increasingly strategic product category.

Download Free sample to learn more about this report.

Segmentation Analysis

By Grade

Industrial Grade Segment Led the Market due to its Crucial Role as a Polymerization Inhibitor

Based on grade, the market is classified into industrial grade, high purity grade, and others.

The industrial grade segment dominated the global hydroquinone market share in 2025, driven by its essential role as a polymerization inhibitor and antioxidant across plastics, resins, and elastomer production. It is a stabilizer that helps maintain the quality of polymers such as HDPE and PET during storage and processing by preventing unwanted reactions caused by air and light. It can also be used in the production of specialized polymers, such as those containing PVC for photosensitive applications. In rubber & tire applications, industrial-grade HQ enhances compound stability, reduces oxidative degradation, and supports consistent curing behavior. As a result, demand for hydroquinone remains closely linked to global polymer throughput and elastomer output.

High-purity product grades are produced through advanced purification, crystallization, and filtration processes to meet stringent specifications required in pharmaceuticals, electronics, advanced imaging, and specialty chemical synthesis. It serves as a key intermediate in the production of p-aminophenol (PAP), which is used to manufacture paracetamol (acetaminophen), and supports the formulation of dyes, agrochemicals, and fine chemicals. Its low impurity profile and high stability are essential for applications demanding precision and controlled reactivity.

The “Others” grade category comprises niche and specialty product variants used in applications requiring unique purity levels, customized particle sizes, or specific functional characteristics. This includes photographic-grade HQ for developer solutions, demand from the cosmetics industry, and dermatology-grade HQ in regions where usage remains permitted, electronic-grade materials for high-performance components, and laboratory or reagent-grade products for research and analytical applications. Although the overall volume share is smaller compared to industrial and high-purity grades, these specialty segments often command higher prices due to tighter specifications and limited producers.

By End Use

Plastics Segment Led the Market Due to Its Ability to Prevent Premature Reaction During Storage And Thermal Processing

Based on end use, the market is segmented into plastics, rubber & tire, chemical, photography & imaging, and others.

To know how our report can help streamline your business, Speak to Analyst

Plastics remained the largest end-use segment in 2025, driven by their essential function in ensuring monomer stability and maintaining uniform polymerization behavior. It is widely incorporated into acrylics, methacrylates, vinyls, and specialty resin systems to prevent premature reaction during storage and thermal processing. This safeguards equipment integrity and enhances manufacturing efficiency, particularly in high-throughput plants. With the growing adoption of lightweight materials in automotive, electronics, and packaging, consistent stabilizer performance has become increasingly critical. Its reliability, compatibility with diverse resin chemistries, and effectiveness at low dosages sustain its importance as resin output expands globally.

The chemical industry relies on the chemical compound as a versatile intermediate and reducing agent across multiple downstream value chains. A key application is the synthesis of p-aminophenol (PAP), used in paracetamol production, where consistent reactivity and purity are crucial. It also enables the production of dyes, agrochemical intermediates, polymer additives, and specialty molecules, supporting a wide range of industrial formulations. As emerging economies expand their chemical output and invest in value-added intermediates, the chemical segment continues to represent a robust and strategically significant consumption channel.

The “Others” category encompasses diverse applications that require specific performance characteristics or tailored purity profiles. These include electronic chemicals, where the product supports fine-pattern development and controlled redox reactions; laboratory and analytical uses that depend on reagent-grade material; and cosmetic or dermatological formulations in regions where its use remains permissible. These application areas often offer higher margins due to stricter specification requirements, contributing to a stable and differentiated demand base within the global market.

Hydroquinone Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

The Asia Pacific held the largest market share in 2025, valued at USD 286.0 million, and is expected to lead the regional share in 2026. Asia Pacific is the fastest-growing regional market, driven by rapid expansion in plastics, resins, elastomers, dyes, and pharmaceutical intermediates. China dominates production and consumption, benefiting from large monomer capacities and extensive chemical integration. India is emerging as a major consumer due to rising paracetamol output, dye intermediates production, and increasing use of polymer stabilizers. Japan and South Korea sustain demand through high-purity electronic and imaging applications. Growing automotive manufacturing, expanding tire production, and rising investment in chemical value chains will further reinforce the regional demand. Region’s dynamic industrial landscape and competitive manufacturing costs position it as the global growth engine.

In 2025, the China market is estimated to reach USD 143.6 million. China is the world’s largest plastic and chemical producer in the world. It also dominates the global rubber and tire production, natural generating massive demand for the product. China is progressively upgrading its quality to supply higher-purity grades, which will shape the country’s market dynamics during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

Europe’s market is shaped by its advanced chemical manufacturing ecosystem, stringent regulatory environment, and strong focus on specialty-grade materials. Demand is distributed across fine chemicals, high-performance polymers, coatings, and pharmaceutical intermediates, where consistent purity and regulatory compliance are essential. While cosmetic applications are heavily restricted, industrial usage remains steady, supported by robust automotive, packaging, and specialty formulation sectors. The region’s mature industrial base limits high growth rates, however, the emphasis on quality, traceability, and environmental compliance reinforces long-term consumption.

North America represents a mature market with steady growth anchored by well-established plastics, coatings, and elastomer industries. The region’s large monomer and resin production base drives recurring demand for polymerization inhibitors, while the tire and automotive components sectors support consistent antioxidant usage. Pharmaceutical-grade consumption remains stable due to strong API manufacturing and steady paracetamol demand. Regulatory scrutiny on cosmetic applications limits growth in personal care, however, industrial consumption remains resilient. Overall, growth remains moderate but is supported by diversified downstream industries. The U.S. market will show steady growth during the forecast period, driven by its moderate demand as a polymerization inhibitor in plastics and as a key ingredient in cosmetics.

The Latin America and Middle East & Africa regions would witness a moderate growth in this market over the forecast period. Demand in Latin America is supported by regional plastics manufacturing, tire and rubber production, and a steadily growing coatings industry. Brazil leads consumption, driven by its large packaging, automotive, and chemical sectors, while Mexico’s industrial base maintains solid demand for polymer and elastomer stabilizers. Chemical intermediates and specialty formulations represent additional growth channels, particularly in agrochemical and dye production.

The Middle East & Africa region is shaped by expanding petrochemical activity, increasing polymer output, and rising demand for stabilizers in downstream plastics and rubber processing. GCC countries remain primary consumers due to their large monomer, resin, and coatings industries. South Africa contributes through tire manufacturing, industrial chemicals, and coatings applications. While overall volumes are smaller compared to other regions, growing petrochemical integration and industrial expansion in key economies are expected to create steady demand during the forecast period.

COMPETITIVE LANDSCAPE

Key Industry Players:

Incremental Capacity Debottlenecking and Low Carbon Grades are identified as New Growth Levers in the Market

The global hydroquinone market is moderately consolidated, anchored by a group of established multinational and regional suppliers. Major players such as Solvay, Eastman Chemical, Camlin Fine Sciences, and Jiangsu Sanjili producers dominate the industrial-grade supply used in polymerization inhibitors and rubber antioxidants. Beneath this tier, a diverse cluster of high-purity and pharmaceutical-oriented manufacturers includes Merck KGaA, Glentham Life Sciences, and others. Competition increasingly centers on purity, consistency, cost efficiency, reliability of monomer-stabilizer performance, and sustainability credentials. Overall, the market is characterized by incremental capacity debottlenecking, technology upgrades, compliance-driven purification improvements, and rising interest in low-carbon and certified mass-balance grades.

LIST OF KEY HYDROQUINONE COMPANIES PROFILED:

- Solvay S.A. (Belgium)

- Eastman Chemical Company (U.S.)

- Camlin Fine Sciences Ltd. (India)

- Global Calcium Pvt. Ltd. (India)

- Jiangsu Sanjili Chemical Co., Ltd. (China)

- Spectrum Chemical Mfg. Corp. (U.S.)

- FUJIFILM Wako Pure Chemical Corporation (Japan)

- Thermo Fisher Scientific (U.S.)

- Merck KGaA (Germany)

- Glentham Life Sciences (UK)

KEY INDUSTRY DEVELOPMENTS:

- September 2020: Camlin Fine Sciences (CFS) established a commercial production at its Diphenol manufacturing facility in Dahej, i.e., spread across approximately 15 acres of space, and is set to manufacture Hydroquinone and Catechol. The plant has a cumulative capacity of 10 kilotons for both Hydroquinone and Catechol.

- April 2019: Solvay expanded its hydroquinone production capacity by 20% at its plant in Saint-Fons, France. The expansion would address the increasing demand for diphenol inhibitors used as additives by the monomer industry.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.0% from 2026-2034 |

| Unit | Value (USD Million), Volume (Kiloton) |

| Segmentation | By Grade, End Use, and Region |

| By Grade |

|

| By End Use |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 561.4 million in 2025 and is projected to reach USD 800.9 million by 2034.

In 2025, the market value stood at USD 286.0 million

The market is expected to exhibit a CAGR of 4.0% during the forecast period (2026-2034).

The industrial grade segment led the market by grade.

The key factors driving the market are the increasing use of hydroquinone as a key ingredient across various production stages and processes of plastic and rubber.

Solvay, Eastman Chemical Company, Camlin Fine Sciences Ltd., Jiangsu Sanjili Chemical Co., Ltd., and Merck KGaA are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

Growing emphasis on sustainable and high purity grades of HQ will favor the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us