Hypersonic Weapons Market Size, Share & Industry Analysis, By Weapon Type (Hypersonic Glide Vehicles (HGVs), Hypersonic Cruise/Maneuvering Missiles, and Air-launched Ballistic/ Quasi-hypersonic Systems), By Launch Platform (Air-launched, Land-launched, and Sea-Launched), By Range (Short-range/tactical (<1,000 km), Medium-range (1,000–3,000 km), Intermediate-range (3,000–5,500 km), and Strategic/long-range (>5,500 km)), By Component (Propulsion, Guidance/Navigation/Control, Airframe, Thermal protection, Payload, Seeker, and Others), By End User, and Regional Forecast, 2026-2034

Hypersonic Weapons Market Size and Future Outlook

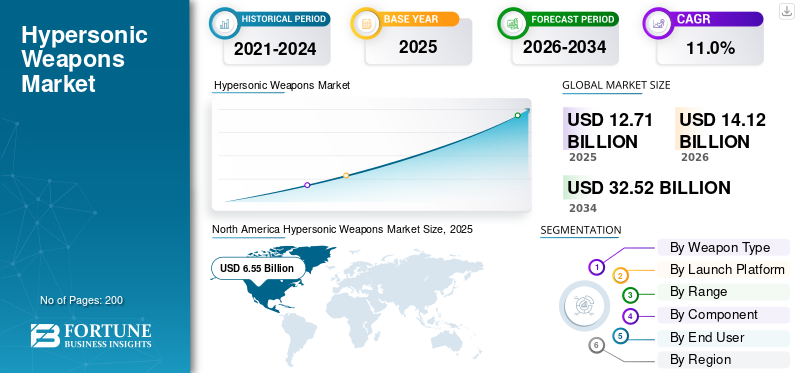

The hypersonic weapons market size was valued at USD 12.71 billion in 2025. The market is projected to grow from USD 14.12 billion in 2026 to USD 32.52 billion by 2034, exhibiting a CAGR of 11.0% during the forecast period. North America dominated the hypersonic weapons market with a market share of 51.53% in 2025.

Hypersonic weapons are systems capable of traveling at speeds of Mach 5 or higher. This speed makes them harder to spot and shoot down compared to regular missiles. The market is expanding due to rising arms races, increased investment in hypersonic technology, ongoing improvements in propulsion and guidance systems, and efforts by the U.S. and other countries to create and launch these systems.

Key players in the market include Lockheed Martin, RTX, Northrop Grumman, and Boeing, along with support from the Department of Defense and the Defense Advanced Research Projects Agency (DARPA). These organizations are speeding up the development and deployment of hypersonic programs through new tests, improvements in missile technology, and advancements in hypersonic glide vehicles, propulsion systems, and missile defenses.

Download Free sample to learn more about this report.

HYPERSONIC WEAPONS MARKET TRENDS

Rising Government Funding to Fuel Industry Expansion

The trend in the hypersonic weapons market is the shift from pure research and development to programs focused on deployment. Governments are now funding more, not just to work on the concept, but instead they are advancing hypersonic weapon development into actual testing, platform integration, and early field use. This change is increasing demand across missile technology, propulsion systems, guidance systems, and the overall supply chain. It also highlights the importance of companies that can develop and deploy systems on a large scale, rather than only designing.

For instance, in May 2025, the U.S. Navy announced a successful end-to-end flight test of its Conventional Prompt Strike capability. They reported that the launch used the cold-gas method planned for future sea-based platform deployment.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Strategic Deterrence and Long-Range Precision Strike is Driving Market Growth

The major drivers in the market are the growing need for faster and more survivable strike systems. Major defense programs are now focused on weapons that can travel faster than Mach 5, and have high precision, long range, and the ability to get past missile defenses. This is pushing the U.S. and its industry partners to invest more in hypersonic weapons technology, improve guidance and propulsion systems, and speed up the development and deployment of hypersonic platforms.

For instance, in May 2025, the U.S. Navy announced its successful end-to-end flight test of Conventional Prompt Strike. This test marked another step toward sea-based fielding. The Navy stated that the speed, range, and survivability of hypersonic weapons are vital for integrated deterrence.

MARKET RESTRAINTS

Complexity Associated with Developing the Product to Hinder Market Growth

A major challenge in the hypersonic weapons market growth is the complexity of these systems and getting them ready for use in the field. Hypersonic programs are developing rapidly; however, they are dealing with cost issues, failed tests, and schedule risks. For instance, in July 2024, the GAO (GAO-24-106792) stated that the DOD's hypersonic efforts do not fully follow best practices in product development. It also pointed out that high costs and failed tests are still a worry for some programs.

MARKET OPPORTUNITIES

Scaling Manufacturing Capacity and the Supply Chain Creates a Significant Market Opportunity

One of the main opportunities in the market is the shift from limited prototyping to scalable production. As more programs focus on developing and deploying operational systems, demand is increasing for fully finished weapons and faster manufacturing of aeroshells, propulsion systems, guidance systems, and other important parts. As a result, the next growth phase would benefit companies that can shorten production cycles, improve throughput, and strengthen the supply chain for hypersonic weapon development. This opportunity is major, as the market is moving from pure innovation to industrial-scale execution.

MARKET CHALLENGES

Extreme Thermal Stress is a Big Challenge for Market Growth

Hypersonic weapons systems must withstand extreme heat while maintaining stable flight and accurate guidance. The GAO has highlighted that the high-temperature environment surrounding these systems creates complex physical and chemical conditions not encountered in other weapon programs. This makes specialized materials, guidance systems, and dedicated testing infrastructure important. As a result, it is difficult to develop and deploy hypersonic systems on a large scale.

Impact of the Russia-Ukraine War

The Russia-Ukraine war has shifted hypersonic systems from a future battlefield concept to an urgent defense priority. Russia’s use of advanced missile attacks has prompted governments to take a closer look at long-range strike options, quicker response abilities, and better missile defenses. As a result, the conflict has increased interest in funding hypersonic weapons technology, counter-hypersonic systems, guidance systems, and the supporting supply chain required for creating and using them.

In February 2025, NATO approved its Integrated Air and Missile Defence Policy, noting that Russia is developing, fielding, and employing advanced air and missile capabilities, including hypersonic missiles. This serves as a clear policy signal that the war is changing procurement focuses and accelerating both hypersonic weapon development and investment in missile defense systems across NATO markets.

Segmentation Analysis

By Weapon Type

Hypersonic Glide Vehicles (HGVs) Segment Dominated the Market due to Long-Range Strike Capabilities

In terms of weapon type, the market is categorized into Hypersonic Glide Vehicles (HGVs), Hypersonic Cruise/Maneuvering Missiles, and Air-launched ballistic/quasi-hypersonic systems.

The Hypersonic Glide Vehicles (HGVs) segment held the largest hypersonic weapons market share in 2025, as they are part of the prominent and well-funded military programs. These systems offer long-range strike capabilities along with maneuverability. This combination makes them harder to track and intercept compared to traditional missile paths. In the U.S., HGV-based systems are advancing in both land and sea programs, fueling the segment growth during the forecast period.

For instance, in May 2025, the U.S. Navy announced a successful end-to-end flight test of its Conventional Prompt Strike capability. They stated that the program is progressing toward sea-based deployment using the common “All Up Round” that is being developed with the Army.

The hypersonic cruise/maneuvering missiles segment is expected to grow at a CAGR of 13.7% over the forecast period.

By Launch Platform

Land-launched Segment Led due to its Ability to Provide a Clear Route for Short-Term Development and Deployment of Hypersonic Capabilities

On the basis of launch platform, the market is classified into air-launched, land-launched, and sea-launched.

Faster transition from testing to deployment makes land-launched hypersonic weapons the dominant segment in 2025. Compared to sea- and air-launched systems, ground-based launchers are simpler to set up in dedicated batteries, place closer to operational zones, and integrate into long-range strike strategies. As a result, land-launched platforms provide a clear route for short-term development and deployment of hypersonic capabilities, especially for hypersonic glide vehicles.

Air-launched is expected to show the fastest growth, registering a CAGR of 11.8% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Range

Medium-range (1,000 to 3,000 km) Segment Lead the Market due to its Ability to Better Align With Real Military Planning than other Range Options

Based on range, the market is segmented into short-range/tactical (<1,000 km), medium-range (1,000–3,000 km), intermediate-range (3,000–5,500 km), and strategic/long-range (>5,500 km).

Medium-range (1,000–3,000 km) holds the largest hypersonic weapons market share as they are better aligned with real military planning than other range options. These systems offer sufficient regional range while providing superior mobility, forward-positioning capabilities, and rapid deployment compared to long-range options. This range aligns with the deterrence strategies of major powers in contested environments, addressing the requirement for rapid response and high survivability, resulting in segment dominance.

Strategic/long-range (>5,500 km) is the fastest-growing segment and is expected to grow at a CAGR of 12.1% across the forecast period.

By Component

Propulsion Segment Dominated the Market due to its Crucial Role In Weapons Velocity

Based on component, the market is segmented into propulsion, guidance/navigation/control, airframe, thermal protection, payload, seeker, and others.

The propulsion segment held the largest share of the hypersonic weapon market in 2025, attributed to its crucial role in weapons velocity, endurance, thermal durability, and overall weapon performance. The booster, rocket motor, scramjet, or other propulsion design affects weapon acceleration, range, and maneuverability under extreme heat. The U.S. Government Accountability Office (GAO) has noted that hypersonic weapons require specialized components to maintain high-speed flight, and these choices impact capability, cost, and manufacturability. In June 2024, DARPA pointed out that propulsion is one of the toughest technical challenges across the full speed range needed for hypersonic flight.

For instance, in January 2023, DARPA announced the final successful flight of the HAWC program. During this flight, the Lockheed Martin vehicle used an Aerojet Rocketdyne scramjet and met all primary objectives. DARPA stated that the program has produced two viable hypersonic air-breathing missile designs for future development.

Seeker is the fastest-growing segment in the market and is expected to grow at a CAGR of 12.9% during the forecast period.

By End User

Air Force Segment Dominates the Market due to Strong Program Support

Based on end user, the market is segmented into Army/land forces, Navy, Air Force, and strategic forces/joint command.

The air force segment held the largest share of the market in 2025 as air-launched systems provide a mix of speed, reach, and operational flexibility. The systems can be integrated into existing bomber and fighter fleets, enabling militaries to launch from safer distances while still hitting important targets quickly. This segment also benefits from strong program support, especially in the U.S., where hypersonic cruise missile development is driven by Air Force and DARPA projects. As a result, the air domain is one of the most important areas for hypersonic weapon development.

The strategic forces/joint command segment is expected to show the fastest market growth, registering a CAGR of 12.0% over the forecast period.

Hypersonic Weapons Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Hypersonic Weapons Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America led the development and deployment of hypersonic weapons in 2025. The region holds the largest share of the market as the U.S. is at the forefront of major hypersonic weapon development. The region benefits from large Department of Defense budgets, strong support from the Defense Advanced Research Projects Agency (DARPA), and a wide industrial base spanning guidance systems, propulsion systems, launch platforms, and the overall supply chain. This focus gives the region a significant advantage in hypersonic capabilities.

U.S. Hypersonic Weapons Market

Based on the strong contribution of North America to the market and the dominance of the U.S. within the region, the U.S. market stood at around USD 6.51 billion in 2025, growing at a CAGR of 7.5%.

Europe

Europe holds the third-largest share of the market. The region's growth is shaped more by sovereignty-driven strike programs rather than large-volume procurement. The U.K. has advanced its Team Hypersonics effort with a significant propulsion test campaign and a framework valued at up to approximately USD 1.5 billion. Meanwhile, the Franco-British program, now called STRATUS, has moved into the development phase. Across Europe, the focus remains on building domestic capabilities, forming selective partnerships, and gradually strengthening the industrial base.

France Hypersonic Weapons Market

France market reached approximately USD 0.25 billion in 2025, equivalent to around 11.09% of Europe's revenues.

Germany Hypersonic Weapons Market

The German market stood at around USD 0.10 billion in 2025, representing roughly 4.62% of Europe's revenues.

Asia Pacific

Asia Pacific is the second-largest market and is anticipated to be the third-fastest growing region during the forecast period, registering a CAGR of 13.1%. The region is strategically important after North America, as it combines existing military capabilities with rapid local development. The U.S. Department of Defense noted that China has deployed the DF-17 hypersonic weapons technology and continues to expand its inventory. Meanwhile, Japan's FY2026 defense budget allocates investments in hypersonic weapons technology for HVGP, hypersonic missile procurement, and manufacturing expansion. India is also progressing in this space, as the DRDO reported a 1,000-second ground test of an active-cooled scramjet combustor in April 2025.

China Hypersonic Weapons Market

China’s market is projected to be one of the largest in the Asia Pacific, with 2025 revenues standing at around USD 1.77 billion, representing roughly 54.87% of the global sales.

Japan Hypersonic Weapons Market

The Japanese market in 2025 stood at around USD 0.47 billion, accounting for roughly 14.53% of global revenues.

Rest of the World

The rest of the World (Middle East & Africa and Latin America) holds a comparatively smaller market share but is expected to grow at a CAGR of 15.3% during the study period. In the Middle East, activity is focused and limited. Iran has announced progress in hypersonic technology with the unveiling of the Fattah-2, while Israel is more focused on strengthening its layered air and missile defense capabilities rather than deploying hypersonic weapons offensively. In contrast, Latin America shows relatively limited publicly disclosed activity in hypersonic weapons offensively.

Latin America Hypersonic Weapons Market

The market in Latin America reached around USD 0.03 billion, accounting for roughly 4.29% of Rest of the World revenues, in 2025.

Middle East & Africa Hypersonic Weapons Market

The Middle East & Africa market stood at around USD 0.63 billion in 2025 and is expected to reach USD 2.10 billion in 2034, representing roughly 95.71% of Rest of the World revenues in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Expanding Operational Capabilities to Gain Competitive Edge

The hypersonic weapons market is relatively concentrated, with the U.S. leading through a few major defense firms. Lockheed Martin, RTX/Raytheon, and Northrop Grumman are the most prominent players due to their involvement in key programs. Lockheed Martin is closely tied to the Army’s Long-Range Hypersonic Weapon effort. Raytheon is in charge of the Air Force’s HACM program, and Northrop Grumman plays a crucial role in propulsion and missile components. This positions these companies strongly across guidance systems, propulsion systems, integration, and the broader supply chain required for developing and deploying hypersonic systems.

Competition is shifting beyond simple prototype development toward manufacturability, affordability, and deployment readiness. DARPA’s HAWC program was designed to demonstrate speed and to validate cost-effective flight concepts, manage heat, and maintain sustained air-breathing propulsion. Current industry efforts are focused on improving manufacturing and expanding operational capabilities. Boeing, while not as central as Lockheed Martin or Raytheon at present, remains relevant due to its prior involvement in SCIFiRE design and platforms such as the F-15EX. Overall, the market prioritizes companies capable of bridging the gap between laboratory validation and operational deployment aligned with U.S. Department of Defense priorities.

LIST OF KEY HYPERSONIC WEAPONS COMPANIES PROFILED

- Northrop Grumman Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- RTX (Raytheon Technologies) (U.S.)

- Boeing Defense, Space & Security (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- BAE Systems plc. (U.K.)

- Rolls-Royce Holdings plc. (U.K.)

- ArianeGroup (France)

- Israel Aerospace Industries (IAI) (Israel)

- BrahMos Aerospace (India)

KEY INDUSTRY DEVELOPMENTS

- February 2026: The UK Ministry of Defence awarded an approx USD 16.09 million contract to Amentum UK, with support from Ebeni and Synthetik. This contract aimed to advance hypersonic missile system design through flight testing and prototype development, indicating that European procurement is now moving deeper into applied program execution.

- May 2025: The U.S. Navy’s Strategic Systems Programs completed a successful end-to-end flight test of a conventional hypersonic missile. This test used the Navy’s cold-gas launch method for Conventional Prompt Strike. It brought the program closer to sea-based deployment and provided another boost to the market.

- November 2024: The U.K., U.S., and Australia signed the Hypersonic Flight Test and Experimentation (HyFliTE) Project Arrangement under AUKUS. This major collaboration aimed to speed up the development, testing, and evaluation of hypersonic vehicles and supporting technologies across the partner industrial bases.

- January 2023: DARPA announced the final successful flight of the HAWC program, which used the Lockheed Martin vehicle with an Aerojet Rocketdyne scramjet. This provided further evidence that different design paths were progressing toward follow-on programs.

- September 2022: The U.S. Air Force awarded Raytheon Missiles & Defense a USD 985.35 million contract to develop and demonstrate prototypes of the Hypersonic Attack Cruise Missile (HACM). This reinforced the commercial and strategic value of air-launched hypersonic weapons.

- September 2021: DARPA and the U.S. Air Force conducted a successful HAWC free-flight test of a missile built by Raytheon Technologies that used a Northrop Grumman scramjet. This test marked an important milestone for air-breathing hypersonic cruise missile technology.

- June 2021: The U.S. Air Force awarded three 15-month SCIFiRE contracts to Boeing, Lockheed Martin, and Raytheon Technologies. These contracts aimed to complete preliminary designs for a hypersonic cruise missile and provided an early competitive push for air-launched hypersonic concepts.

REPORT COVERAGE

The global hypersonic weapons market analysis provides an in-depth study of market size, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and trends that are expected to drive the market during the forecast period. It offers information on the technological advances, new product launches, key industry developments, and details on strategic partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key market players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.0% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Weapon Type

|

|

By Launch Platform

|

|

|

By Range

|

|

|

By Component

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 14.12 billion in 2026 and is projected to reach USD 32.52 billion by 2034.

In 2025, the market value stood at USD 6.55 billion.

The market is expected to exhibit a CAGR of 11.0% during the forecast period.

By weapon type, the Hypersonic Glide Vehicles (HGVs) segment led the market.

Rising demand for strategic deterrence and long-range precision strike is driving market growth.

Key players in the market include Northrop Grumman, Lockheed Martin, RTX, L3Harris, and BAE Systems.

North America dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us