Industrial CCUS Market Size, Share & Industry Analysis, By Type (Capture, Transportation, Utilization, and Storage), By Application (Oil & Gas, Power Generation, Chemical & Petrochemicals, Cement, Iron & Steel, and Others) and Regional Forecast, 2025-2032

KEY MARKET INSIGHTS

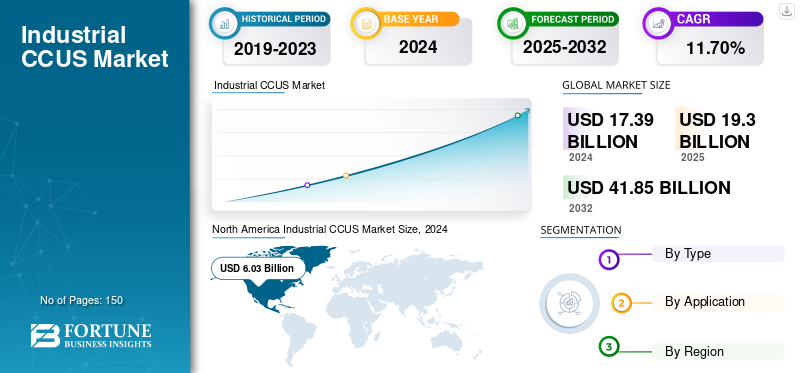

The global industrial CCUS market size was valued at USD 17.39 billion in 2024. The market is projected to grow from USD 19.3 billion in 2025 to USD 41.85 billion by 2032, exhibiting a CAGR of 11.70% during the forecast period. North America dominated the global market with a share of 34.67% in 2024.

Industrial CCUS refers to the carbon capture, utilization and storage technologies that are adopted by industries in sectors such as steel, cement, chemical and others. This helps in capturing carbon dioxide emissions and store it underground or convert it into useful end use as per the need.

The market is growing steadily due to stringent climate regulations, surging carbon prices, net zero commitments and growing demand for decarbonization across industries. There are various key players operating in the market including Aker Carbon Capture, Mitsubishi Heavy Industries, Fluor Corporation, Shell Catalysts & Technologies, Technip Energies, Honeywell UOP, Carbon Clean, Air Liquide, and Linde Engineering. These companies are adopting strategies such as investment in storage and transportation networks, partnerships, perusing government based funding and investing in technological innovations to sustain market competition.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Stringent Emission Regulations and Net-Zero Goals Drives the Market Development

Strict emission regulations with targets for global net-zero are driving industrial CCUS market growth. Governments globally are implementing stringent limits on carbon-intensive industries, thus leading to an increased tax on carbon, and emerging mandatory reporting frameworks. This has enabled companies to adopt innovative capture technologies.

Similarly, different industrial net zero commitments and countries are dynamically creating long-term demand for scalable Decarbonization solutions. This pushes giant industries in cement, chemical and steel sector to invest in huge CCUS projects that are backed by tax incentives, public funding, and different carbon credit schemes.

Market Restraints

High Capital Costs and Limited Commercial Viability Deters the Market Growth

Restricted commercial viability and higher capital costs tend to limit the market growth. Building transport pipelines, capture units and storage facilities demand a higher upfront investment with different operational expenses remaining higher due to energy-intensive procedures. Particularly for small and medium sized industries, the return on investment is uncertain, with profitability relying on favorable carbon pricing, government subsidies and consistent demand for carbon dioxide derived products.

Market Opportunities

Technological Innovation and Industrial Partnerships Offers Lucrative Growth Opportunities

Advancements in technology and wider industrial partnerships offers major growth opportunity for the market. Revolutions in electrochemical CO2, catalytic conversion, utilization and mineralization and bio-based pathways are growing range of high-value products derived from captured carbon. Such innovations are enhancing efficiency and reducing the operational costs.

Similarly, collaborations among the heavy industries, clean-tech startups, and research organizations are boosting the pilot projects, allowing for faster commercialization of emerging CCU technologies. These partnerships tend to support shared infrastructure, co-investment, and knowledge transfer.

INDUSTRIAL CCUS MARKET TRENDS

Growing Focus on Carbon Circularity Has Emerged as a Prominent Market Trend

Increasing emphasis on carbon circularity has emerged as a major trend reshaping the market, while companies are change captured CO2 via waste stream into an effective economic resource. Industries are growingly investing in advanced technologies that covert CO2 into a specialty chemical, low-carbon fuels, and highly sustainable building materials, thus reducing its reliance on raw materials.

Additionally, this is further backed by a stringent climate policy, rising commercial viability of CO2 based products and net-zero commitments. Partnerships among industrial emitters, technology developers and research institutions also augments innovations in the market.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Growing Deployment of Capture Types in Refineries Augments Segment Growth

Based on type, the market is segmented into capture, transportation, utilization, and storage.

In 2024, capture segment held the largest industrial CCUS market share and with a revenue of USD 10.9 billion. This growth is due to the presence of high-cost equipment, technologies and infrastructure that are needed to purify and separate CO2 from industrial emissions. Additionally, its growing deployment in refineries, power plants and chemical sector further boosts the segmental growth.

Additionally, utilization segment held the highest CAGR of 12.4% in 2024. This segmental growth is owing to the increasing advancements in converting captured CO2 emissions into a value added offerings including chemical, fuels, and construction materials. Moreover, the increasing investments in circular carbon technologies and supportive government policies are boosting the segmental growth.

By Application

To know how our report can help streamline your business, Speak to Analyst

Well-Established Infrastructure for Carbon Capture Drive Oil & Gas Segment Growth

The market is divided into oil & gas, power generation, chemical & petrochemicals, cement, iron & steel, and others, based on application.

Among these, the oil and gas segment dominated the market with a revenue share of USD 4.86 billion in 2024. This growth is due to a well-established infrastructure for carbon capture, extensive CO2 emissions, and wider use of captured CO2 in enhanced oil recovery (EOR) processes. Industries are also investing in CCU technologies to decarbonize manufacturing and align with the global net-zero goals.

Chemicals and petrochemicals segment held highest CAGR of 13.2% in 2024. This growth is due to surging integration of captured CO2 as a feedstock for producing polymers, fuels and special chemicals. Moreover, advancements in electrochemical conversion technologies and catalytic, coupled with growing sustainability commitments are also driving the product adoption across this industry.

INDUSTRIAL CCUS MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

North America Industrial CCUS Market Size, 2024 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The North America region is leading the market with a share of USD 6.03 billion in 2024 and USD 5.54 billion in 2023. This growth is due to established carbon capture projects, strong government support, and prominent investments by giant oil & gas as well as chemical industries. Additionally, the presence of huge CCUS projects across the U.S. and Canada augmented by supporting favorable policies including tax credits such as 45Q also strengthens the regional growth. The U.S. leads the North American market with an expected revenue share of USD 5.04 billion in 2025.

Europe

The Europe region is growing with an expected share of USD 4.02 billion in 2025. This regional growth is owing to higher carbon prices, stringent climate policies, and stronger EU funding across the region. U.K., Germany, and Italy are some of the major contributors to the market growth with an expected revenue share of USD 0.79 billion, USD 0.99 billion and USD 0.43 billion respectively by 2025.

Asia Pacific

Asia Pacific region held highest CAGR of 13.6% in 2024. The market is also expected to reach USD 6.2 billion in 2025. This growth is driven by rising CO2 emission, rapid industrialization, and growing government initiatives to boost carbon capture technologies. Additionally, growing chemical, energy and manufacturing sectors across countries such as India, China and Japan also fuels the demand for cost effective CCUS solutions. India and China are the major contributors for the market growth with an expected revenue share of USD 0.81 billion and 2.52 billion by 2025.

South America and Middle East & Africa

The markets of South America and Middle East & Africa are growing with an expected share of USD 1.05 billion and USD 1.42 billion respectively in 2025. This growth is due to growing awareness about captured carbon to recover oil, produce synthetic fuels and chemicals, and offer economic growth to the regions. GCC countries are predicted to have a market share of USD 0.65 billion by 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Growing Focus on Adopting Innovative Technologies Leads to Key Player’s Dominating Market Positions

The Industrial CCUS industry consists of different players operating in the market, including Aker Carbon Capture, Mitsubishi Heavy Industries, Fluor Corporation, Shell Catalysts & Technologies, Technip Energies, Honeywell UOP, Carbon Clean, Air Liquide, and Linde Engineering. These firms are rapidly adopting different key strategies such as mergers and collaborations, developing innovative technologies, and new product launches to strengthen their market position.

LIST OF KEY INDUSTRIAL CCUS COMPANIES PROFILED

- Aker Carbon Capture (Norway)

- Mitsubishi Heavy Industries (Japan)

- Fluor Corporation (U.S.)

- Shell Catalysts & Technologies (Netherlands)

- Technip Energies (France)

- Honeywell UOP (U.S.)

- Carbon Clean (U.K.)

- Air Liquide (France)

- Linde Engineering (Germany)

- SLB – Schlumberger (U.S.)

- Baker Hughes (U.S.)

- Worley (Australia)

KEY INDUSTRY DEVELOPMENTS

- In July 2025, Carbon Clean, a global leader in revolutionizing carbon capture solutions, announced the official opening of its new Global Innovation Centre (GIC) in Navi Mumbai, India. The GIC will be one of the world's largest dedicated carbon capture research facilities, spanning 77,121 square feet and housing two carbon capture plants alongside state-of-the-art laboratories for solvent development, analysis, and testing. It will serve as a hub for research, innovation, and technology demonstration.

- In May 2025, Mitsubishi Heavy Industries, Ltd. (MHI) has installed a new CO2 capture pilot plant at the Himeji No.2 power plant in Hyogo Prefecture owned by The Kansai Electric Power Co., Inc. (KEPCO), and today held a ceremony at the site to coincide with the start of operations. The pilot plant was established to conduct research and development for CO2 capture technologies using flue gas from gas turbines at the power plants. The plant has a capture capacity of approximately five tons per day, and through demonstration of innovative CO2 capture technologies for the next generation, will strengthen the competitiveness of the carbon dioxide capture, utilization and storage (CCUS) business.

- In March 2025, Malaysian government officially unveiled the Carbon Capture, Utilization, and Storage (CCUS) Bill 2025, establishing a legal framework for the development of the industry. The bill is expected to create a dedicated agency to oversee the carbon capture market. However, opposition from Sabah and Sarawak, East Malaysian states that refused to participate, significantly reduces the bill’s economic potential.

- In September 2024, Baker Hughes has launched a new digital solution for carbon capture, utilization, and storage (CCUS) operations. The solution, named Carbon Edge, is the first end-to-end, risk-based digital solution for CCUS operations that provides comprehensive support for regulatory reporting and operational risk management.

- In May 2023, Koch Engineered Solutions LLC (KES) has signed a Memorandum of Understanding (MOU) with Chart Industries, Inc., a leading diversified global manufacturer of highly engineered cryogenic equipment and processes for the industrial gas and other industries, positioning both companies to provide full carbon capture solutions to key customers and industries.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the Industrial CCUS market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2019-2032 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2032 |

| Growth Rate | CAGR of 11.70% from 2025-2032 |

| Historical Period | 2019-2023 |

| Unit | Value (USD billion) |

| Segmentation | By Type, Application and Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 17.39 billion in 2024 and is projected to reach USD 41.85 billion by 2032.

The market is expected to exhibit steady growth at a CAGR of 11.70% during the forecast period.

Stringent emission regulations and net-zero goals drives the market growth.

Aker Carbon Capture, Mitsubishi Heavy Industries, Fluor Corporation, Shell Catalysts & Technologies, Technip Energies, Honeywell UOP, Carbon Clean, Air Liquide, and Linde Engineering are some of the top players in the market.

The North America region held the largest market share.

Asia Pacific was valued at USD 6.03 billion in 2024.

- 2019-2032

- 2024

- 2019-2023

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us