Precision Agriculture Market Size, Share & Industry Analysis, By Product Type (Hardware [Sensors, Drones/UAVs, GPS receivers, and Others], Software [Farm management platforms, Data analytics tools, and Others], and Services [Consulting services, System integration, Data analytics & advisory, and Others]), By Application (Yield Monitoring, Crop Scouting, Field Mapping, Irrigation Management, Fertilizer Management, and Others), By Technology (Guidance Systems, Remote Sensing, Variable-Rate Technology, and Others), By Farm Size (Large, Medium, and Small), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

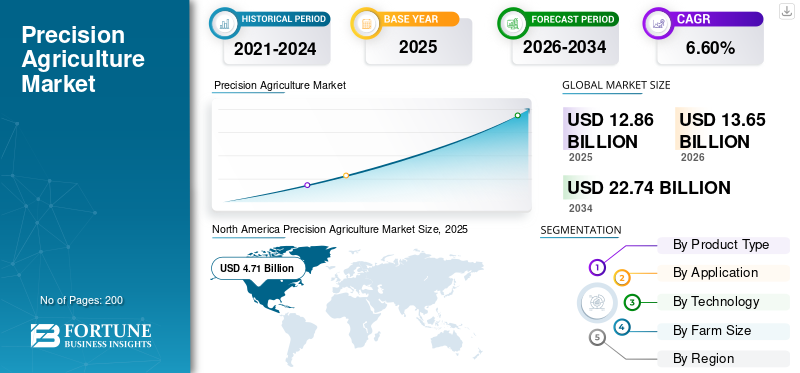

Precision Agriculture Market Size and Future Outlook

The global precision agriculture market size was valued at USD 12.86 billion in 2025. The market is projected to grow from USD 13.65 billion in 2026 to USD 22.74 billion by 2034, exhibiting a CAGR of 6.60% during the forecast period. North America dominated the precision agriculture market with a market share of 36.63% in 2025.

Precision agriculture refers to the use of connected hardware, sensors, drones, software platforms, data analytics, and automated field systems to improve farm productivity, reduce input waste, and optimize decision-making at the field level. The market is gaining momentum as growers increasingly prioritize yield improvement, cost control, and climate-resilient farm management. Demand is being supported by higher adoption of GPS-guided machinery, artificial intelligence, remote sensing, precision irrigation, variable-rate input application, and integrated farm data platforms.

The global market is moderately consolidated, with leading companies such as Deere & Company, Trimble Inc., AGCO Corporation, CNH Industrial N.V., and Topcon Positioning Systems, Inc. competing through product innovation, precision hardware integration, software-led farm intelligence, and automation capabilities.

Download Free sample to learn more about this report.

Precision Agriculture Market KEY TAKEWAYS

- 2025 Market Size: USD 12.86 Billion

- 2026 Market Size: USD 13.65 Billion

- 2034 Forecast Market Size: USD 22.74 Billion

- CAGR: 6.60% from 2026–2034

- North America dominated the precision agriculture market with a 36.63% share in 2025.

- The hardware segment led the market in 2025, reaching USD 4.79 billion.

- The fertilizer management segment accounted for USD 2.17 billion in 2025.

North America

North America accounted for USD 4.71 billion in 2025 and is projected to reach USD 8.20 billion by 2034.

Europe

Europe was valued at USD 3.48 billion in 2025 and is projected to reach USD 6.25 billion by 2034.

Asia Pacific

Asia Pacific generated USD 2.81 billion in 2025 and is expected to reach USD 5.54 billion by 2034.

U.S.

The precision agriculture market was valued at USD 3.68 billion in 2025.

Japan

Farm modernization and adoption of advanced precision farming technologies drive growth.

Read More

Precision Agriculture Market Trends

Rising Adoption of Data-Driven Farming Systems to Shape Industry Trends

The increasing adoption of data-driven farming is a key trend shaping the market. Farmers are progressively leveraging precision farming techniques such as IoT-enabled sensors, satellite imaging, and AI-powered analytics to monitor soil health, crop conditions, and weather patterns in real time data. These technologies enable the precise application of fertilizers, water, and pesticides, reducing wastage, and improving productivity.

The integration of cloud-based farm management platforms and automation and control systems is also gaining traction, allowing farmers to make informed decisions and enhance operational efficiency. The trend is particularly strong in developed markets, while emerging economies are witnessing the adoption of precision farming due to government support and rising awareness.

- As per the World Bank, digital agriculture solutions, including data analytics and farm management platforms, can reduce input costs (fertilizers, water, and pesticides) by 15–25%, improving overall farm profitability.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Rising Need for Input Optimization and Resource Efficiency to Support Market Growth

The need to produce more with tighter margins is a major driver for precision agriculture market growth. Growers are under pressure to improve yields while controlling fertilizer, seed, water, fuel, and labor costs. Precision technologies directly address this need by allowing site-specific farm management rather than uniform field treatment. Adoption data already shows that these technologies are moving into mainstream commercial farming.

- According to the United States Department of Agriculture - Economic Research Service, in 2023, guidance autosteering systems were used by 52% of midsize farms and 70% of large-scale crop-producing farms in the U.S., while 68% of large-scale crop-producing farms used yield monitors, yield maps, and soil maps. This confirms that precision tools are increasingly embedded in operating practices rather than remaining niche technologies.

Market Restraints

High Upfront Costs, Interoperability Issues, and Uneven Farm Readiness to Limit Market Expansion

Despite favorable long-term economics, adoption still faces barriers in many markets. Precision agriculture systems often require significant upfront investment in connected equipment, sensors, subscriptions, software integration, and operator training. Small and medium growers, particularly in fragmented agricultural systems, may struggle to justify full-scale deployment unless payback is visible within a short cycle.

- FAO’s State of Food and Agriculture 2022, based on 27 case studies, notes that while digital agricultural automation can improve productivity and resilience, inclusive adoption remains constrained by affordability, access, skills, and structural barriers for small-scale producers.

These constraints are particularly visible where farm sizes are small, connectivity is inconsistent, and access to financing or technical service support is limited.

Market Opportunities

Precision Irrigation, Remote Sensing, and Analytics-Led Decision Platforms to Create New Growth Avenues

A major opportunity for the industry lies in precision irrigation and crop intelligence systems. As water, labor, and input costs rise, technologies that help growers apply the right amount of water and crop inputs at the right time are likely to attract stronger investment. The Food and Agriculture Organization and UN-linked water datasets continue to show agriculture as the world’s largest water-using sector, while the United States Department of Agriculture analysis indicates that global crop calorie production would need to rise by about 47% by 2050 under a medium population growth scenario to feed 9.75 billion people. This strengthens the case for technologies that improve field productivity without proportionate increases in land, water, and chemical use.

SEGMENTATION ANALYSIS

By Product Type

Hardware Segment Dominated Market Due to Its Foundational Role in On-Farm Precision Deployment

Based on product type, the market is segmented into hardware, software, and services.

The hardware segment dominated the global precision agriculture market share in 2025, reaching USD 4.79 billion, as field deployment still begins with physical systems such as guidance components, controllers, monitors, receivers, drones, and connected machinery attachments. Hardware remains the first point of investment for many growers as it delivers visible operational benefits in steering, mapping, application control, and monitoring. Within the broader hardware base, sensors and drones are gaining traction as farms move toward more responsive field management.

The software segment is projected to record the fastest CAGR of 8.19% during 2026–2034, driven by growing demand for unified dashboards, prescription engines, field data-driven decisions, and agronomic analytics.

To know how our report can help streamline your business, Speak to Analyst

By Application

Fertilizer Management Segment Dominated Market Due to High Input Costs and Need for Precise Nutrient Application

Based on application, the market is segmented into yield monitoring, crop scouting, field mapping, irrigation management, fertilizer management, pest & disease management, planting & seeding optimization, harvest management, and livestock monitoring.

The fertilizer management segment led the market in 2025, valued at USD 2.17 billion, reflecting the high economic importance of nutrient-use efficiency in commercial agriculture. Rising fertilizer prices, environmental compliance concerns, and the need to improve per-acre returns are driving demand for variable-rate application systems and prescription-led nutrient management. Yield monitoring, crop scouting, and field mapping also account for a substantial share as they form the information layer required for precision decision-making.

The irrigation management segment is expected to witness the fastest CAGR of 8.28% during the forecast period, supported by increasing water stress, the need for efficient irrigation scheduling, and stronger adoption of moisture-linked control systems.

By Technology

Guidance Systems Segment Dominated Market Due to Broad Commercial Use Across Large and Mid-Sized Farms

Based on technology, the market is segmented into guidance systems, remote sensing, variable-rate technology, yield monitoring systems, soil monitoring & mapping, farm management software, and weather tracking & forecasting.

The guidance systems segment held the leading market position in 2025, reaching USD 3.28 billion, as autosteer, assisted steering, and machine guidance technologies are among the most established and commercially scalable precision farming tools. These systems help reduce overlap, improve pass accuracy, lower fuel use, and support precise planting and spraying operations, making them highly attractive in row-crop and broad-acre farming. They also act as an entry point for wider precision adoption as they connect directly with field operations and existing machinery fleets.

The remote sensing segment is projected to grow at the fastest CAGR of 8.83% during the forecast period, supported by the expansion of satellite imagery, drone-based scouting, multispectral analysis, and real-time crop stress detection.

By Farm Size

Large Farm Segment Dominated Market Due to Higher Capital Availability and Faster Technology Payback

Based on farm size, the market is segmented into large, medium, and small.

The large segment dominated the market in 2025, accounting for USD 6.92 billion, as large-scale operations are more likely to invest in integrated precision agriculture systems and capture measurable savings from optimized input application, labor efficiency, and equipment productivity. These farms typically have stronger purchasing power, better access to dealer support, and greater incentive to adopt technologies that improve operating scale. Medium farms are also becoming an important demand base, particularly where retrofit solutions and subscription-based software models reduce initial investment pressure.

The small segment is projected to grow at the fastest CAGR of 8.08% during the forecast period, largely due to lower-cost digital tools, drone services, mobile-based monitoring, and shared-access models are gradually improving affordability.

Precision Agriculture Market Regional Outlook

Regionally, the market is studied across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Precision Agriculture Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the global market and was valued at USD 4.71 billion in 2025 and is projected to reach USD 8.20 billion by 2034, growing at a CAGR of 6.42% during 2026–2034. The growth is driven by its highly commercialized farming systems, large average farm sizes, strong machinery replacement cycle, and mature adoption of GPS guidance, autosteering, remote sensing, and prescription-based application technologies.

U.S. Precision Agriculture Market

The U.S. dominates the North American market, valued at approximately USD 3.68 billion in 2025. Growth is supported by widespread use of guidance systems, strong demand for variable-rate technologies, and increasing investment in autonomy, analytics, and connected field operations across corn, soybean, wheat, and specialty crop farms.

Canada Precision Agriculture Market

Canada was valued at approximately USD 0.70 billion in 2025, with an expected CAGR of around 7.50% during the projected period. Adoption is rising across broad-acre farming regions as producers increasingly deploy auto-guidance, section control, imagery-led crop scouting, and data-driven nutrient management to improve operating efficiency in large field environments.

Europe

Europe was valued at USD 3.48 billion in 2025, and is projected to reach USD 6.25 billion by 2034, registering a CAGR of 6.76% during 2026–2034. Regional growth is supported by a strong focus on sustainable agricultural practices, emissions reduction, and resource-efficient farming practices.

Germany Precision Agriculture Market

Germany is one of the leading European markets, valued at approximately USD 0.81 billion in 2025, and is expected to grow at a CAGR of around 5.83% during the forecast period. The country’s advanced farm machinery base, strong agritech ecosystem, and increasing focus on nutrient efficiency and digital compliance continue to support adoption.

U.K. Precision Agriculture Market

The U.K. market was valued at approximately USD 0.42 billion in 2025, with a projected CAGR of around 7.05% during the forecast period. Demand is being driven by farm digitization, variable-rate input management, precision mapping, and the use of data-led decision systems in cereals, oilseeds, and mixed farming operations.

Asia Pacific

Asia Pacific was valued at USD 2.81 billion in 2025 and is projected to reach USD 5.54 billion by 2034, growing at the fastest CAGR of 7.87% during 2026–2034. The region is emerging as the fastest-growing market due to increasing mechanization, rising food demand, pressure on water and land resources, and stronger government interest in farm modernization. Growth is especially visible in China, India, Japan, and Australia, although the adoption mix varies by farm structure and crop profile.

China Precision Agriculture Market

China dominates the Asia Pacific market, valued at approximately USD 0.94 billion in 2025, and is expected to grow at a CAGR of around 7.59% during the forecast period. Growth is supported by the rapid adoption of agricultural drones, smart machinery, digital farm platforms, and precision input application across large-scale crop zones and commercial agriculture projects.

South America and Middle East & Africa

South America was valued at USD 1.20 billion in 2025 and is projected to reach USD 1.81 billion by 2034, registering a CAGR of 4.68% during 2026–2034. Growth in the region is led by commercial row-crop farming, large plantation structures, and the need to improve yield stability and input efficiency across export-oriented agricultural systems. Brazil and Argentina remain the core markets due to their scale in soybean, corn, sugarcane, and other mechanized crop production.

The Middle East & Africa market was valued at USD 0.66 billion in 2025 and is projected to reach USD 0.95 billion by 2034, expanding at a CAGR of 4.25% during the forecast period. Growth here is being supported by water management needs, controlled irrigation systems, protected cultivation, and selective adoption of farm monitoring technologies.

Brazil Precision Agriculture Market

Brazil dominates the South American market, valued at approximately USD 0.75 billion in 2025, and is expected to grow at a CAGR of around 4.75% during the forecast period. Demand is supported by large-scale mechanized farming, rising use of variable-rate application, and broader deployment of connected systems in soybean, corn, cotton, and sugarcane operations.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Integrated Platforms, Automation, Mixed-Fleet Compatibility, and Resource Efficiency

Leading participants are focusing on expanding connected equipment ecosystems, enhancing software interoperability, and developing analytics-led solutions that help growers improve productivity while reducing input waste. Market competition is increasingly shaped by the ability to provide end-to-end solutions across guidance, sensing, remote monitoring, application control, autonomy, and farm data management. Deere, Trimble, AGCO, CNH, Topcon, Hexagon, DJI Agriculture, and Valmont are all active in precision agriculture through platforms spanning equipment, software, precision irrigation, drones, or automation solutions. Official company materials show continued emphasis on precision farming, mixed-fleet compatibility, autonomy, and connected agronomic workflows.

Key Players in the Precision Agriculture Market

|

Rank |

Company Name |

|

1 |

Deere & Company |

|

2 |

Trimble Inc. |

|

3 |

AGCO Corporation |

|

4 |

CNH Industrial N.V. |

|

5 |

Topcon Positioning Systems, Inc. |

List of Key Precision Agriculture Companies Profiled in Report

- Deere & Company (U.S.)

- Trimble Inc. (U.S.)

- AGCO Corporation (U.S.)

- CNH Industrial N.V. (U.K.)

- Topcon Positioning Systems, Inc. (U.S.)

- Hexagon AB (Sweden)

- TeeJet Technologies (U.S.)

- DJI Agriculture (China)

- Kubota Corporation (Japan)

- Ag Leader Technology (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: John Deere and Bayer expanded their partnership through a new wireless data‑link between Bayer’s FieldView platform and Deere’s Operations Center, effectively tightening the “hardware + software” precision‑ag ecosystem around the U.S. growers and fueling a broader valuation debate around Deere’s tech‑driven model.

- February 2025: Yamaha Motor expanded into precision agriculture by launching Yamaha Agriculture, Inc., a new U.S.–based subsidiary focused on autonomous equipment and AI‑powered digital solutions for specialty‑crop growers. The move formalizes and scales Yamaha’s decades‑long work in agricultural automation, especially around unmanned helicopters and robotic field operations.

- February 2025: Daedong, a leading South Korean agricultural machinery company, launched Korea's first commercial precision agriculture service. This AI-powered solution targets rice farmers initially, following four years of field demonstrations that reduced fertilizer use by 7% and boosted rice yields by 6.9%.

- February 2025: BASF launched a new precision‑farming tool called Xarvio Field Manager for Fruits & Veggies, a digital crop‑optimization platform tailored specifically for fresh‑produce growers such as table and wine grape producers. The system uses field‑level data and scientific models to provide growers with tailored advice on when, where, and how much to apply crop‑protection and nutrient inputs, aiming to improve efficiency, yield, and sustainability.

- September 2024: Netafim, Orbia's precision agriculture business, launched GrowSphere as an innovative all-in-one operating system for digital farming, focusing on precision irrigation and fertigation. This system integrates hydraulic, operational, and agronomic capabilities to automate farming processes and reduce manual fieldwork.

REPORT COVERAGE

The global precision agriculture market report analyzes the market in depth and highlights crucial aspects such as global market trends, market dynamics, supply chains, prominent companies, and investment in research and development. Besides this, the report also provides insights into the global market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.60% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Application

|

|

|

By Technology

|

|

|

By Farm Size

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was valued at USD 12.86 billion in 2025 and is anticipated to reach USD 22.74 billion by 2034.

At a CAGR of 6.60%, the global market will exhibit steady growth over the forecast period.

By application, the fertilizer management segment led the market.

North America held the largest market share in 2025.

Rising need for input optimization and resource efficiency to support market growth.

Deere & Company, Trimble Inc., AGCO Corporation, CNH Industrial N.V., and Topcon Positioning Systems, Inc. are the leading players in the market.

Rising adoption of data-driven farming systems is shaping industry trends.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us