Fertilizers Market Size, Share & Industry Analysis, By Type (Chemical Fertilizers [NPK Fertilizers, Micronutrients, Secondary Macronutrients] and Bio-fertilizers [Nitrogen Fixing, Phosphate Solubilizers and Others]), By Form (Dry and Liquid), By Mode of Application (Foliar, Fertigation, Soil Treatment, and Seed Treatment), By Crop Type (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

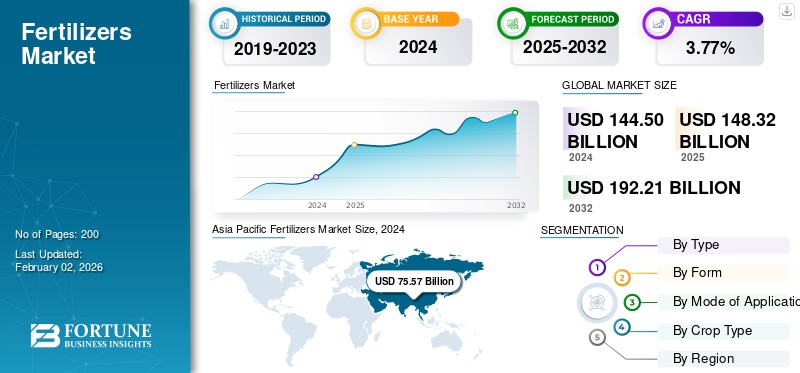

KEY MARKET INSIGHTS

The global fertilizers market size was valued at USD 148.32 billion in 2025. The market is projected to grow from USD 152.66 billion in 2026 to USD 204.67 billion by 2034, exhibiting a CAGR of 3.73% during the forecast period. Asia Pacific dominated the global fertilizers market with a share of 52.32% in 2025.

Fertilizers are natural or synthetic materials that supply essential nutrients to plants to enhance productivity and soil fertility. They play a critical role in modern agriculture, supporting food security amid the increasing global pressure of population growth and shrinking arable land. The market encompasses both chemical and bio-based fertilizers, with nitrogen, phosphorus, and potassium (NPK) formulations dominating agricultural use. Fertilizer imports in the global market have increased due to rising demand for crop productivity in developing regions. In recent years, technological advancements, precision farming, and the adoption of sustainable agricultural practices have fueled the evolution of the global fertilizer industry. Increasing demand for sustainable agricultural practices is expected to stabilize global fertilizer prices in the long term within the global market.

In addition, the industry's key players such as Nutrien Ltd., Yara International ASA, The Mosaic Company, CF Industries Holdings, Inc., and ICL Group Ltd dominate the global market.

Download Free sample to learn more about this report.

Fertilizers Market KEY TAKEAWAYS

- 2025 Market Size: USD 148.32 billion

- 2026 Market Size: USD 152.66 billion

- 2034 Forecast Market Size: USD 204.67 billion

- CAGR: 3.73% from 2026–2034

- Asia Pacific dominated the fertilizers market with a 52.32% share in 2025.

- The chemical fertilizers segment is projected to dominate the market with a 97.95% share in 2026.

- The dry segment is projected to dominate the market with a 76.41% share in 2026.

Asia Pacific

Valued at USD 77.60 billion in 2025, driven by extensive fertilizer use, government subsidies, and rising food production.

Europe

Valued at USD 21.51 billion in 2025, driven by sustainable nutrient management and bio-based fertilizer innovations.

North America

Valued at USD 25.82 billion in 2025, supported by precision farming and large-scale cultivation of nutrient-intensive crops.

U.S.

Projected to reach USD 34.53 billion by 2026, supported by strong demand from large-scale crop cultivation.

Japan

Projected to reach USD 11.89 billion by 2026, driven by increasing adoption of advanced fertilizer solutions.

Read More

MARKET DYNAMICS

Market Drivers

Agricultural Intensification and Rising Food Demand to Drive Market Growth

Agricultural intensification practices that increase output per unit of agricultural land require the use of fertilizers to maintain soil fertility and support continuous crop production. Moreover, the rapid global population growth projected to surpass 9.7 billion by 2050, according to the FAO, continues to exert immense pressure on global food systems. To meet rising food demand, farmers are increasingly adopting intensive cultivation practices requiring large volumes of fertilizers to sustain soil productivity. Fertilizers provide essential nutrients such as nitrogen, phosphorus, and potassium that are critical to achieving higher crop yields, essential for global trade and food security.

- According to the International Fertilizer Association Statistics, in 2023, global fertilizer consumption was an estimated 194 million tons (Mt) of nutrients, a 3% recovery from declines in the two preceding years.

Market Restraints

Environmental Regulations and Soil Degradation Challenges to Impede Market Growth

Environmental regulations and soil degradation are significant challenges impeding the global fertilizers market growth. Governments globally are increasingly implementing stricter regulations to reduce environmental damage caused by fertilizer overuse, such as soil and water pollution and greenhouse gas emissions.

- For instance, the European Union's Farm to Fork Strategy aims to reduce fertilizer use by 20% by 2030 to combat nutrient runoff and soil degradation, mandating producers to develop more sustainable fertilizer alternatives.

This regulatory pressure restricts the volume and type of fertilizers used, thereby slowing market growth in regions with stringent policies.

Moreover, soil degradation due to excessive chemical fertilizer usage has led to declining soil health, reduced biodiversity, and increased vulnerability to erosion, further complicating fertilizer application and effectiveness.

Market Opportunities

Increasing Adoption of Precision and Smart Farming Technologies to Unlock New Growth Opportunities

The growing adoption of precision agriculture and digital farming solutions is a major catalyst driving global fertilizers market demand. These technologies help farmers optimize fertilizer use, improve nutrient efficiency, and reduce wastage. Advanced systems using GPS mapping, IoT sensors, and AI-based nutrient management platforms enable site-specific fertilizer application, improving yields while minimizing environmental impact.

- The Food and Agriculture Organization estimates that precision farming can reduce fertilizer consumption by up to 20% while maintaining the same or higher productivity levels.

This efficiency and cost benefit are motivating large-scale adoption, supporting steady fertilizer demand in modernized farms worldwide.

Fertilizers Market Trends

Expansion of Green Ammonia Production and Low-Carbon Fertilizer Production to Shape Industry

Sustainability-focused innovation is reshaping the fertilizer landscape. Growing global commitments to carbon neutrality are driving investment in green ammonia, which is ammonia produced using renewable hydrogen and nitrogen from the air. This shift supports the development of low-emission fertilizers that reduce the carbon footprint of agriculture. Major fertilizer producers such as Yara International, CF Industries, and Nutrien have already launched pilot projects for green ammonia-based fertilizers. This transition aligns with government sustainability initiatives and bolsters long-term fertilizer market growth.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

High Efficiency and Widespread Use to Lead the Chemical Segment’s High Market Proportion

The global market by type is segmented into chemical fertilizers and bio-fertilizers.

The Chemical Fertilizers segment dominated the market, accounting for 97.95% market share in 2026. The chemical fertilizers segment dominated the market with a value of USD 141.97 billion in 2024, projected to reach USD 185.88 billion by 2032, growing at a CAGR of 3.56%. The segment is further segmented into NPK fertilizers, micronutrients, and secondary macronutrients. The segment’s dominance is attributed to high efficiency, immediate nutrient availability, and widespread use in large-scale agriculture. NPK fertilizers account for the largest share within this segment.

The bio-fertilizers segment is expected to grow significantly in the forecast period with a CAGR of 12.31% in 2025.

By Form

Ease of Storage and Large-Scale Operations to Fuel Dry Segment Market Leadership

On the basis of form, the market is segmented into dry and liquid.

The Dry segment is projected to dominate the market with a share of 76.41% in 2026, valued at USD 110.93 billion in 2024, projected to reach USD 144.77 billion by 2032 at a CAGR of 3.52%, driven by ease of storage, blending flexibility, and cost-effectiveness. Dry fertilizers are suitable for large-scale operations, have higher nutrient concentration, and facilitate precision agriculture practices.

The liquid segment is anticipated to grow at the fastest CAGR of 4.56% during the global fertilizers market forecast period.

By Mode of Application

High Compatibility and Widespread Acceptance Fuels Soil Treatment Segment Market Leadership

On the basis of mode of application, the market is segmented into foliar, fertigation, soil treatment, and seed treatment.

The soil treatment segment dominates the global fertilizer market share of 71.51% in 2026, with a market size valued at approximately USD 104.11 billion in 2024. Soil treatment is the primary method used for major crops and is expected to grow at a CAGR of about 3.38%. The dominant share of soil treatment reflects its widespread acceptance due to its effectiveness for large-scale agriculture and compatibility with various crops.

The fertigation segment, valued at USD 20.69 billion in 2024, is forecasted to record the highest CAGR of 5.11%, boosted by the adoption of drip and sprinkler irrigation.

To know how our report can help streamline your business, Speak to Analyst

By Crop Type

Large Cultivation Areas and High Demand for Staple Foods to Lead Grains & Cereals Segment’s Market Leadership

Based on the crop type, the market is segmented into grains and cereals, pulses and oilseeds, fruits and vegetables, and others.

In 2026, the grains & cereals segment is projected to lead the market with a 43.12% share. The grains & cereals segment led the market with USD 62.85 billion in 2024, growing at a 3.32% CAGR. This growth is primarily supported by the large cultivation areas of key crops such as rice, wheat, and maize. Large-scale production in these staple crops meets significant global caloric needs and food demand. The segment's expansion is also driven by advancements in seed technology and farming practices, which improve yields and crop resistance.

The fruits and vegetables segment is expected to grow significantly in the forecast period at a CAGR of 4.83% from 2025 to 2032.

Fertilizers Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

Asia Pacific Fertilizers Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

In 2025, the North America market stood at USD 25.82 Billion, representing 17.41% of global demand, and is projected to grow to USD 26.43 Billion in 2026. Growth is supported by advanced precision farming, adoption of controlled-release fertilizers, and large-scale corn and soybean cultivation in the U.S.

The U.S. accounts for the largest share of fertilizer demand in North America, driven by its extensive cultivation of corn, soybeans, wheat, and cotton, all of which are nutrient-intensive crops. The U.S. market is estimated at USD 34.53 billion by 2026.

Europe

The Europe region captured 14.50% of the global market in 2025, generating USD 21.51 Billion in revenue, and is projected to reach USD 22.11 Billion in 2026. The region’s growth is supported by sustainable nutrient management practices and innovations in bio-based fertilizers under the EU’s Green Deal. The U.K. market is estimated at USD 6.54 billion by 2026, while the Germany market is estimated at USD 8.90 billion by 2026.

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 77.6 Billion in 2025, accounting for a 52.32% share, and is expected to reach USD 79.9 Billion in 2026. The region’s dominance stems from the extensive use of fertilizers in China, India, and Southeast Asia for rice, maize, and horticultural crops. Government subsidy programs and rising food production are key growth factors.

The Japan market is estimated at USD 11.89 billion by 2026, while the China market is estimated at USD 11.17 billion by 2026. The India market is estimated at USD 10.47 billion by 2026.

South America

South America was valued at USD 16.55 billion in 2024 and is forecasted to grow at the highest CAGR of 4.61%, driven by expanding soybean and corn acreage in Brazil and Argentina. Export-oriented agribusiness and the adoption of modern fertilizers are key drivers.

Middle East & Africa

The Middle East & Africa market accounted for USD 6.27 billion in 2025, representing 4.23% of the global industry, and is expected to reach USD 6.46 billion in 2026, fueled by growing agricultural modernization, water-efficient fertilizer solutions, and government initiatives for food security.

South America accounted for USD 17.12 billion in 2025, representing 11.54% of the global market share, and is projected to reach USD 17.75 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

R&D and Sustainable Fertilizer Innovations to Strengthen Market Competitiveness

The global market is moderately consolidated, with major players investing heavily in R&D for efficient and eco-friendly formulations. Companies are emphasizing precision agriculture, micronutrient fortification, and bio-based fertilizer development to sustain competitiveness.

Key Players in the Fertilizers Market

|

Rank |

Company Name |

|

1 |

Nutrien Ltd. |

|

2 |

Yara International ASA |

|

3 |

The Mosaic Company |

|

4 |

CF Industries Holdings, Inc. |

|

5 |

ICL Group Ltd. |

List of Key Fertilizer Companies Profiled

- Nutrien Ltd. (Canada)

- Yara International ASA (Norway)

- The Mosaic Company (U.S.)

- CF Industries Holdings, Inc. (U.S.)

- ICL Group Ltd. (Israel)

- EuroChem Group AG (Switzerland)

- OCI N.V. (Netherlands)

- Haifa Chemicals Ltd. (Israel)

- Coromandel International Ltd. (India)

- OCP Group (Morocco)

KEY INDUSTRY DEVELOPMENTS

- November 2025: OCP Group, a Moroccan state-owned company, launched NP 5-42, a new binary fertilizer product containing 5% nitrogen and 42% phosphate (P2O5) as part of its phosphate portfolio expansion, particularly under its triple superphosphate (TSP) initiative. This product is a compound NP fertilizer with ammonia as the nitrogen source, designed to complement TSP, which traditionally contains 46% P2O5 but no nitrogen. Phosphatic fertilizers are an important part of the global market as they help crops grow better and increase yields.

- September 2025: Refex Renewables Infrastructure diversified into the fertilizer manufacturing and trading business, and launched its organic manure products under the brand name "Biodhanic." This new business segment was approved by shareholders through amendments to the company's Memorandum of Association.

- July 2025: Kan Biosys, an Indian agri-biotech company, launched two new product lines in 2025 to promote sustainable farming in India. These include ROFA (Real Optimized Fertilizer Application), a range of 12 imported, fully water-soluble specialty fertilizers developed in collaboration with French company De Sangosse, designed for precision nutrient delivery across diverse agro-climatic conditions and foliar application.

- December 2024: Fertilizer major IFFCO developed a new nano NPK fertilizer in granular form and is seeking government approval to launch it in the retail market. The product will be produced at IFFCO's Kandla unit.

- June 2023: ICL launched a new line of advanced water-soluble micronutrient and N-P-K fertilizers in North America, under their Nova brand. The flagship products include Nova FINISH, Nova PULSE, Nova ELEVATE, and Nova FLOW, which are designed for foliar and fertigation applications.

REPORT COVERAGE

The global fertilizers industry report analyzes the market in depth and highlights crucial aspects such as global market trends, market dynamics, supply chain, prominent companies, investment in research and development, and end-use. Besides this, the report also provides insights into the global fertilizers market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.73% from 2026 – 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type · Chemical Fertilizers o NPK Fertilizers o Micronutrients o Secondary Macronutrients · Bio-fertilizers o Nitrogen Fixing o Phosphate Solubilizers o Others |

|

By Form · Dry

|

|

|

By Mode of Application · Foliar · Fertigation · Soil Treatment · Seed Treatment |

|

|

By Crop Type · Grains and Cereals · Pulses and Oilseeds · Fruits and Vegetables · Others |

|

|

By Region · North America (By Type, Form, Mode of Application, By Crop Type, and Country) • U.S. (By Type) • Canada (By Type) • Mexico (By Type) · Europe (By Type, Form, Mode of Application, By Crop Type, and Country) • Germany (By Type) • Spain (By Type) • Italy (By Type) • France (By Type) • U.K. (By Type) • Rest of Europe (By Type) · Asia Pacific (By Type, Form, Mode of Application, By Crop Type, and Country) • China (By Type) • Japan (By Type) • India (By Type) • Australia (By Type) • Rest of Asia Pacific (By Type) · South America (By Type, Form, Mode of Application, By Crop Type, and Country) • Brazil (By Type) • Argentina (By Type) • Rest of South America (By Type) · Middle East & Africa (By Type, Form, Mode of Application, By Crop Type, and Country) • South Africa (By Type) • Israel (By Type) • Rest of the idle East & Africa (By Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 152.66 billion in 2026 and is anticipated to reach USD 204.67 billion by 2034.

At a CAGR of 3.73%, the global market will exhibit steady growth over the forecast period.

By type, the chemical segment leads the market.

Asia Pacific held the largest market share in 2025.

Agricultural intensification and rising food demand drive the market growth.

Nutrien Ltd., Yara International ASA, The Mosaic Company, CF Industries Holdings, Inc., and ICL Group Ltd are the leading companies in the market.

Expansion of green ammonia and low-carbon fertilizer production is shaping the industry.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us