Cardiac Mapping Market Size, Share & Industry Analysis By Type (Contact Cardiac Mapping Systems and Non-contact Cardiac Mapping Systems), By Indication (Atrial Fibrillation (AF), Atrial Flutter, Atrioventricular Nodal Reentrant Tachycardia (AVNRT), Atrioventricular Reentrant Tachycardia (AVRT), Ventricular Tachycardia (VT), Premature Ventricular Contractions (PVCs) and Others), By End User (Hospitals & ASCs, Electrophysiology (EP) Labs, Specialty Clinics, Academic & Research Institutes and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

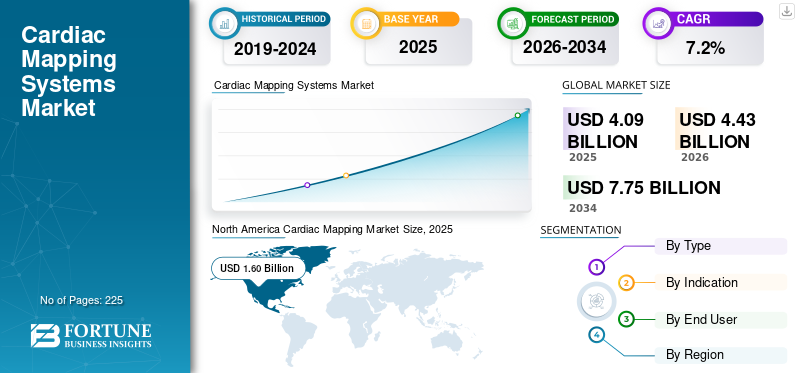

The global cardiac mapping market size was valued at USD 4.09 billion in 2025 and is projected to grow from USD 4.43 billion in 2026 to USD 7.75 billion by 2034, exhibiting a CAGR of 7.2% during the forecast period. North America dominated the global cardiac mapping market with a market share of 39.12% in 2025.

Cardiac mapping is a process that utilizes specialized equipment to record and analyze the electrical activity of the heart, thereby creating a three-dimensional map of its electrical pathways. This process, also known as electroanatomic mapping, enables doctors to identify the source of a heart arrhythmia and guide treatments such as catheter ablation. The growing patient pool and technological advancements in these systems are further boosting the adoption of cardiac mapping procedures, which enable treatment of patients suffering from high-risk diseases among the patient population.

- For instance, according to the 2024 statistics published by Journal of Cardiac Failure (JCF), approximately 6.7 million Americans over 20 years of age have heart failure in the U.S.

This, coupled with a growing focus on research and development initiatives among key players such as Johnson & Johnson, Abbott, Boston Scientific Corporation, Medtronic, and others, is expected to support the market growth.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Growing Prevalence of Cardiac Arrhythmias to Boost Market Growth

The cardiac mapping market growth is primarily driven by rising burden of cardiac arrhythmias, especially atrial fibrillation (AF), which now affects more than 37 million people worldwide and continues to grow due to aging populations and lifestyle risk factors. As AF and complex ventricular arrhythmias become more prevalent, hospitals and EP laboratories increasingly rely on high-precision 3D mapping systems to guide ablation with superior accuracy and safety. Another major driver is the rapid adoption of catheter ablation procedures, which have experienced steady growth over the past decade. For example, catheter ablation volumes in the U.S. increased significantly, supported by updated guidelines recommending catheter ablation as a first-line therapy for selected AF patients.

Furthermore, technological advancements, including high-density mapping catheters, impedance and ultrasound-based non-contact systems, and AI-enabled signal interpretation, have greatly enhanced clinician confidence in mapping technologies. These innovations reduce procedure time, improve outcomes, and support the management of complex arrhythmias, fueling global demand. Emerging markets, particularly in the Asia Pacific region and the Middle East, are also investing in advanced cardiac electrophysiology infrastructure, thereby expanding the accessible patient pool. Collectively, these factors continue to strengthen the adoption of mapping systems as a core component of modern arrhythmia care.

Market Restraints

High Cost Associated with Devices to Limit Market Growth

Despite strong momentum, the cardiac mapping market faces major restraints that can slow adoption, particularly in cost-sensitive healthcare environments. The high capital investment required for 3D mapping systems, often exceeding USD 300,000 to USD 500,000 per installation, remains a barrier for smaller hospitals and underfunded health systems. Additionally, the recurring cost of mapping catheters and disposables significantly increases procedural expenses, making reimbursement variability a key concern. In many countries, reimbursement for complex EP procedures is either limited or inconsistent, creating financial pressure on hospitals to justify technology upgrades. Clinical workflow complexity also limits adoption, advanced mapping requires well-trained electrophysiologists, and the global shortage of EP specialists slows expansion in emerging markets.

Furthermore, the learning curve associated with integrating high-density or non-contact mapping systems can lengthen procedure times during early adoption, creating hesitation among healthcare providers. Regulatory hurdles add layers of delay, particularly in regions with evolving medical device frameworks. For instance, newer mapping platforms that leverage AI or software-driven automation face additional requirements for cybersecurity, data governance, and clinical validation. These combined factors, high cost, training demands, reimbursement uncertainty, and regulatory scrutiny, form substantial market restraints that companies must navigate to expand adoption globally.

Market Opportunities

Increasing Awareness Related to Cardiac Mapping in Emerging Regions to Create Market Opportunities

Significant opportunities are emerging with cardiac mapping technologies moving toward greater precision, automation and clinical integration. One of the most promising areas is the expansion of electrophysiology programs in emerging markets such as China, India, Brazil, and the Gulf countries. These regions are witnessing accelerated investments in cardiology infrastructure, and the penetration rates of mapping systems remain significantly lower than those in North America and Europe, offering a large untapped potential. Another opportunity lies in the increasing use of mapping for non-AF indications such as ventricular tachycardia (VT) and PVC-induced cardiomyopathy. As healthcare systems detect more ventricular arrhythmias, with VT ablations increasing globally, the need for sophisticated substrate mapping has grown swiftly.

Moreover, technological convergence is unlocking new possibilities. AI-powered mapping algorithms, the automation of activation mapping, and integration with real-time MRI or CT imaging have the potential to reduce procedure time and enhance precision dramatically. Several leading manufacturers recently introduced high-density catheters and AI-enabled platforms, demonstrating strong clinical performance and expanding physician acceptance. Additionally, as remote monitoring and digital electrophysiology platforms become more prevalent, mapping systems can progressively collect, analyze, and integrate arrhythmia data across the care continuum. With a growing emphasis on precision medicine and personalized therapy, the cardiac mapping market is well-positioned to capitalize on these high-growth opportunities.

Market Challenges

Procedural Complexity Associated with Advanced Mapping to Hinder the Market Growth

The cardiac mapping market faces several persistent and emerging challenges that may limit its full growth potential. A major challenge is high procedural complexity associated with advanced mapping, which requires well-trained electrophysiologists and experienced laboratory staff. Many regions, particularly in Latin America, Africa, and parts of Southeast Asia, continue to face significant shortages of EP-trained clinicians, which hinders the adoption of mapping despite growing arrhythmia burdens. Data interpretation remains another challenge, even with high-density and AI-augmented platforms, electrophysiologists are required to navigate vast volumes of electrograms, and misinterpretation can affect ablation outcomes. System interoperability also poses hurdles, as mapping platforms often integrate poorly with imaging systems, EP recorders, or ablation generators from competing vendors.

Cybersecurity, data privacy, and software regulation concerns further complicate the adoption of cloud-connected or AI-enabled platforms. Cost pressure is another major issue, as healthcare systems tighten their budgets, hospitals may delay capital purchases or opt for refurbished systems, which limits its growth. Lastly, the prevalence of arrhythmias is rising faster than the capacity of EP labs, creating a bottleneck where demand for mapping outpaces procedural throughput. This mismatch is particularly evident with VT cases, where long procedure times strain resources. Addressing these challenges will require coordinated improvements in workforce training, system integration, regulatory clarity, and cost optimization.

Cardiac Mapping Market Trends

Technological Advancements in these Products has Emerged as a Market Trend

The cardiac mapping landscape is undergoing rapid transformation, with several notable trends shaping its future trajectory. One major trend is the widespread adoption of high-density mapping catheters, which can capture thousands of data points in seconds, enabling clearer visualization of complex arrhythmias. Platforms integrating high-resolution anatomical reconstruction with automated signal annotation are becoming standard in leading EP centers.

Another prominent trend is the rise of non-contact and ultra-rapid mapping systems, which can generate full-chamber maps in a single heartbeat. This advancement is particularly valuable for unstable ventricular arrhythmias. AI-assisted mapping is also gaining momentum, with manufacturers embedding machine-learning algorithms to improve arrhythmia classification, pattern recognition, and map accuracy. Regulatory approvals over the past few years reflect this shift as multiple AI-enhanced mapping tools have entered the U.S. and European markets, pushing the industry toward automation-first workflows.

Additionally, hybrid cardiac procedures combining imaging modalities, such as fluoroscopy-free workflows supported by 3D mapping, CT overlays, and intracardiac ultrasound, are gaining traction as hospitals strive to minimize radiation exposure. Finally, geographic trends indicate a rapid expansion of EP labs in Asia Pacific and Middle East, where increased investments and training programs are accelerating the adoption of these technologies. Together, these developments underscore a transition toward faster, smarter, and more integrated mapping systems worldwide.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Increasing Number of Product Launches to Drive Contract Cardiac Mapping Systems Segment Dominance

Based on the type, the market is classified into contact cardiac mapping systems and non-contact cardiac mapping systems.

To know how our report can help streamline your business, Speak to Analyst

The contact cardiac mapping systems segment held the largest market share in 2025. The growth is due to increasing number of patient admissions for the treatment of heart abnormalities, resulting in a rising demand for advanced cardiac mapping systems globally. This, coupled with the increasing focus of prominent companies toward receiving approvals for cardiac mapping systems, is further expected to support the segmental growth.

The non-contact cardiac mapping systems segment is expected to grow at a CAGR of 11.4% over the forecast period.

By Indication

Increasing Prevalence of Atrial Fibrillation Leads to Dominance of Segment

Based on indication, the market is bifurcated into atrial fibrillation (AF), atrial flutter, atrioventricular nodal reentrant tachycardia (AVNRT), atrioventricular reentrant tachycardia (AVRT), ventricular tachycardia (VT), premature ventricular contractions (PVCs), and others.

The atrial fibrillation (AF) segment dominated the market in 2025. In 2026, the segment is anticipated to dominate with a 55.8% share. This dominant share is attributed to the increasing prevalence of atrial fibrillation (AF), resulting in a growing number of diagnostic procedures among the patient population, thereby supporting segmental growth in the market.

- According to the Centers for Disease Control and Prevention, it is estimated that 12.1 million people in the U.S. will have AFib by 2050.

The premature ventricular contractions (PVCs) segment is expected to grow at a CAGR of 13.7% in the market during the forecast period.

By End-user

Increasing Number of Hospitals & ASCs Led to Segment’s Dominance

Based on end user, the market is bifurcated into hospitals & ASCs, electrophysiology (EP) labs, specialty clinics, academic & research institutes and others.

The hospitals and ASCs segment dominated the market in 2025. The growing prevalence of heart abnormalities, increasing patient admissions, rising number of hospitals and ambulatory surgical centers, and others are some of vital factors supporting growth of segment in the market. Furthermore, the segment is set to hold a 53.0% share in 2026.

- For instance, according to 2024 statistics published by the Ministry of Health, Labour and Welfare of Japan (MHLW), it was reported that there are about 8,122 hospitals in Japan.

In addition, specialty clinics’ end users are projected to grow at a CAGR of 8.7% during the study period.

Cardiac Mapping Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Cardiac Mapping Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America dominated the cardiac mapping market in 2025, valued at USD 1.60 billion, and also is expected to secure leading share in 2026 with USD 1.71 billion. The dominance of this region is due to distinct factors, including the growing prevalence of heart abnormalities, the increasing number of cardiac mapping procedures in the region, and established cardiac centers, among others. In 2025, the U.S. market is estimated to reach USD 1.55 billion.

- For example, according to data provided by Elsevier B.V. in August 2024, the overall prevalence of CAD among U.S. adults increased from 4.6% in 2019 to 4.9% in 2022.

Europe and Asia Pacific

Europe and Asia Pacific are expected to witness significant growth over the forecast period. During the study period, the Europe region is projected to record a growth rate of 6.4% and reach the valuation of USD 1.15 billion in 2026. This is due to growing adoption of advanced cardiac mapping systems and the rising number of diagnostic procedural volumes in the region. Moreover, the increasing prevalence of heart defects, as well as improvement of healthcare infrastructure in countries such as China, South Korea, Japan, and India, are some other contributing factors to market growth. Backed by these factors, countries such as the U.K. are expected to record the valuation of USD 0.17 billion, Germany to record USD 0.23 billion, and France to record USD 0.14 billion in 2026. After Europe, the market in the Asia Pacific is estimated to reach USD 1.17 billion in 2026 and secure the position of the third-largest region in the market. In the region, India is estimated to reach USD 0.14 billion while China is estimated to reach USD 0.37 billion in 2026.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth over the forecast period. The Latin America market in 2026 is expected to reach a valuation of USD 0.21 billion. The increasing adoption of advanced technologies, growing access to specialized cardiac care, and other factors are expected to boost product adoption in these regions. In the Middle East & Africa, GCC is set to attain the value of USD 0.10 billion in 2026.

Competitive Landscape

Key Industry Players

Growing New Product Approvals Among Key Companies Leads to Their Market Dominance

A strong geographical presence, along with a significant focus on R&D activities to develop and introduce novel products, is one of the major factors contributing to the dominance of these companies in the market. Johnson & Johnson, Abbott, Boston Scientific Corporation, and Medtronic are prominent companies in the market in 2025. Furthermore, the increasing emphasis of key players on obtaining new product approvals to enhance their brand presence is expected to support the global cardiac mapping market share.

- For instance, in October 2024, Boston Scientific announced FDA approval of the FARAWAVE NAV ablation catheter and 510(k) clearance for FARAVIEW software, both tightly integrated with the new OPAL HDx Mapping System to provide visualization and mapping support for its FARAPULSE pulsed field ablation system.

Other key players, including EnChannel Medical Ltd., MicroPort Scientific Corporation, Biotronik, and others, are also growing in the market, primarily due to their increasing focus on R&D activities to launch novel products and expand their product portfolios in the market.

List of Key Cardiac Mapping Companies Profiled

- Johnson & Johnson (U.S.)

- Abbott (U.S.)

- Boston Scientific Corporation (U.S.)

- Medtronic (Ireland)

- EnChannel Medical Ltd. (U.S.)

- MicroPort Scientific Corporation (China)

- Biotronik (Germany)

- Stereotaxis, Inc. (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Siemens Healthineers AG (Germany)

KEY INDUSTRY DEVELOPMENTS

- July 2024 - Spanish start-up Corify Care obtained the CE Mark under the EU MDR for ACORYS. This non-invasive cardiac mapping system utilizes 128 body-surface sensors and torso modeling to generate electroanatomical maps in under 10 minutes.

- February 2024 - MicroPort EverPace received CE MDR certification for its latest generation Columbus 3D EP Navigation System, a 3D mapping/navigation platform combining magnetic and impedance positioning for tachyarrhythmia treatment.

- August 2022 - FDA cleared Johnson & Johnson’s CARTO 3 with Advanced Focus Mapping (AFM), K221112, adding advanced algorithms for focal arrhythmia localization and improved mapping performance.

- November 2021 – Abbott’s EnSite X EP System obtained FDA 510(k) clearance (K213364), enabling U.S. commercialization as a programmable diagnostic computer for 3D catheter navigation and mapping.

- October 2021 - The FDA cleared Johnson & Johnson’s CARTO 3 EP Navigation System V7.2 (K213264), an incremental upgrade that enhances electroanatomical mapping workflows and system capabilities.

REPORT COVERAGE

The market report provides a detailed global cardiac mapping market analysis and focuses on key aspects such as leading companies, type, indication, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.2% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, Indication, End User, and Region |

|

By Type |

· Contact Cardiac Mapping Systems · Non-contact Cardiac Mapping Systems |

|

By Indication |

· Atrial Fibrillation (AF) · Atrial Flutter · Atrioventricular Nodal Reentrant Tachycardia (AVNRT) · Atrioventricular Reentrant Tachycardia (AVRT) · Ventricular Tachycardia (VT) · Premature Ventricular Contractions (PVCs) · Others |

|

By End User |

· Hospitals and ASCs · Electrophysiology (EP) Labs · Specialty Clinics · Academic & Research Institutes · Others |

|

By Region |

· North America (By Type, By Indication, By End User, and by Country) o U.S. (By Type) o Canada (By Type) · Europe (By Type, By Indication, By End User, and by Country/Sub-region) o U.K. (By Type) o Germany (By Type) o France (By Type) o Italy (By Type) o Spain (By Type) o Scandinavia (By Type) o Rest of Europe (By Type) · Asia Pacific (By Type, By Indication, By End User, and by Country/Sub-region) o China (By Type) o Japan (By Type) o India (By Type) o Australia (By Type) o Southeast Asia (By Type) o Rest of Asia Pacific (By Type) · Latin America (By Type, By Indication, By End User, and by Country/Sub-region) o Brazil (By Type) o Mexico (By Type) o Rest of Latin America (By Type) · Middle East & Africa (By Type, By Indication, By End User, and by Country/Sub-region) o GCC (By Type) o South Africa (By Type) o Rest of the Middle East & Africa (By Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 4.09 billion in 2025 and is projected to reach USD 7.75 billion by 2032.

In 2025, the North America regional market value stood at USD 1.60 billion.

Growing at a CAGR of 7.2%, the market will exhibit steady growth over the forecast period (2026-2034).

By type, the contact cardiac mapping systems segment is the leading segment in this market.

The growing prevalence of cardiac arrhythmias is a key factor driving the market's growth.

Johnson & Johnson, Abbott, Boston Scientific Corporation, and Medtronic are the major players in the global market.

North America dominated the market share in 2025.

The growing prevalence of heart abnormalities and increasing number of diagnostic procedures are some of the major factors anticipated to fuel the adoption of these products worldwide.

- 2021-2034

- 2025

- 2019-2024

- 225

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us