Cinema Camera Market Size, Share & Industry Analysis, By Sensor Type (CMOS, Full Frame, Dual Pixel, Super 35mm, and CCD (Charged-Coupled Device)), By Lens Type (PL Mount and EF Mount), By Video Resolution (4K/8K Resolution and Full HD Resolution (1080)), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

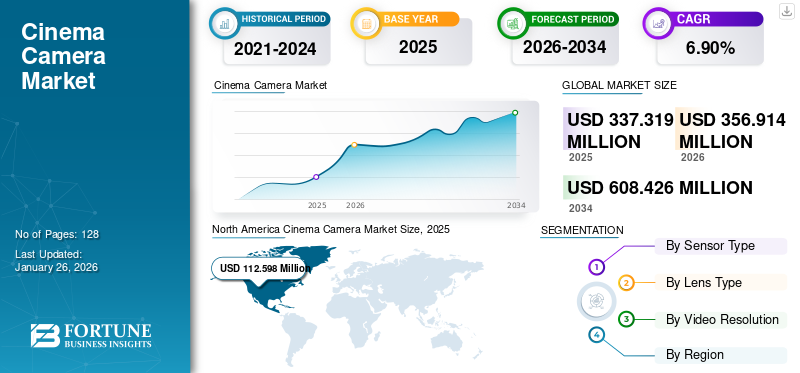

The global cinema camera market size was valued at USD 337.32 million in 2025 and is projected to grow from USD 356.91 million in 2026 to USD 608.43 million by 2034, exhibiting a CAGR of 6.90% during the forecast period. North America dominated the global market with a share of 33.40% in 2025.

A cinema camera is a professional-grade camera explicitly designed to capture high-quality video footage in filmmaking and television production. These cameras typically offer features such as interchangeable lenses, large sensors for improved image quality, high dynamic range, and various recording formats to meet the demands of cinematic production. In the research scope, we have considered solutions offered by companies such as ARRI AG, Canon Inc., Panasonic, Sony Group Corporation, Blackmagic Design, and Red Digital Cinema.

The market is being boosted by advancements in digital technology, which enhance image quality and flexibility in post-production. Additionally, the rising demand for high-quality content from the entertainment and advertising industries further drives the market growth. According to Insider Intelligence, in 2025, more than 70% of OTT users binge-watch content. Therefore, these factors are accelerating the market share.

The COVID-19 pandemic significantly impacted market growth, leading to film production disruptions, project delays, and reduced demand for cinema equipment. Lockdowns and social distancing measures resulted in the cancellation or delay of film shoots and the closure of theatres, dampening the need for new camera purchases.

Download Free sample to learn more about this report.

Cinema Camera Market Takeaways

- 2025 Market Size: USD 337.32 million

- 2026 Market Size: USD 356.91 million

- 2034 Forecast Market Size: USD 608.43 million

- CAGR: 6.90% from 2026–2034

- North America dominated the cinema camera market with a 33.40% share in 2025.

- The Super 35mm sensors segment is projected to account for 30.05% of the market in 2026.

- The PL mount segment is projected to hold 79.99% of the market in 2026 and is expected to register the highest CAGR.

North America

The market was valued at USD 112.6 million in 2025 and is projected to reach USD 118.72 million in 2026, supported by the presence of leading film studios and advanced production technologies.

Europe

The regional market reached USD 99.91 million in 2025 and is expected to grow to USD 104.45 million in 2026, driven by strong filmmaking and broadcasting activities.

Asia Pacific

The market accounted for USD 98.78 million in 2025 and is projected to reach USD 106.78 million in 2026, fueled by the rapid expansion of the film industry in China, India, and South Korea.

U.S.

The cinema camera market is projected to reach USD 96.76 million by 2026, driven by continued investments in professional film and television production.

Japan

The cinema camera market is projected to reach USD 38.322 million by 2026, supported by the country's advanced imaging technology industry and strong demand for professional camera equipment.

Read More

IMPACT OF GENERATIVE AI

Integration of Generative AI with Cinema Camera by Enhancing Capabilities to Fuel Market Growth

Generative AI offers much more to transformation through efficiencies and adaptability across scalability in industries with cinema cameras. Generative AI creates by enabling a user to think more about high-level design and innovation, creativity that is lost in the details of operations. Moreover, AI enables new forms of visual storytelling, such as generating hard-to-shoot or impossible scenes, abstract visuals, and stylized effects that might not be feasible with conventional cameras alone. Filmmakers can experiment with different visual styles and camera angles virtually before committing to physical setups, potentially reducing the number of takes and physical resources required. In a 2025 survey of AI filmmakers, 100% reported using AI-generated video in their projects, up from 87.5% in 2023 and 95.5% in 2024.

IMPACT OF RECIPROCAL TARIFFS

The recent reciprocal tariffs imposed by the U.S. government are significantly impacting the market. Electronics and technology, specifically professional cinema cameras, are subject to these tariffs, which are supposed to prompt domestic manufacturing but have resulted in immediate cost increases for filmmakers and production companies. According to an industry analyst, estimated price hikes for popular cameras range from USD 100 to over USD 1,000 per unit, depending on brand and origin.

Cinema Camera Market Trends

High-End Cameras Reaching 8K Resolution and Beyond 120fps to Enhance Footage and Slow-Motion Capture

The pursuit of higher resolutions, such as 8K in the cinema camera space, is driven by the desire to capture incredibly detailed and lifelike images. With over 33 megapixels of resolution, 8K cameras can record at a level exceeding the resolving power of the human eye. This allows filmmakers to capture the smallest nuances of texture, clarity of detail in landscapes/scenery, and finer features of actors' faces and expressions. As digital projectors and displays continue increasing in resolution, 8K acquisition future-proofs content to be exhibited on premium large-format screens.

In parallel, attaining higher selected frame rates beyond the standard 24fps is a priority to enable better slow-motion capture. Frame rates, such as 120fps and above, allow filming at 5x or higher speed than usual. When slowed down to 24fps, this produces incredibly smooth, crisp, slow-motion effects.

- In December 2023, B&H unveiled the DJI Ronin 4D-8K 4-Axis Cinema Camera 8K Combo along with the Zenmuse X9-8K Gimbal Camera, presenting various choices for videographers to enhance their current setup for capturing 8K images.

The challenge for manufacturers is packing this level of performance into a reasonably portable and affordable camera system, especially for making cinemas. Unprecedented sensor resolutions, processing power, and data throughput are needed. This drives innovations in hardware/chipsets, efficient codecs, such as ProRes RAW, and storage/memory technologies that allow sustained high-speed recording.

- In April 2024, Proton Camera released the smallest broadcast-quality cinema camera, the PROTON CAM, at NAB 2024. This tiny camera weighed 24g and measured 28x28mm, targeting niche broadcast applications and industrial applications with its 12-bit output.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Rise of Streaming Platforms and Growing Popularity of On-Demand Video Content Increased Demand for High-Quality Digital Cinematography

The proliferation of streaming platforms, such as Netflix, Amazon Prime Video, Hulu, and Disney+, has revolutionized how we consume video content. Gone are the days when viewers had to wait for scheduled broadcast times or rely solely on traditional cable/satellite TV services. The on-demand nature of streaming has empowered audiences to watch anything, anytime, on the device of their choice. This shift in consumption patterns has created an insatiable demand for fresh, high-quality content from these platforms to keep their viewers engaged and subscribed.

- In April 2024, Netflix shifted its focus toward lower-budget filmmaking projects, moving away from high-budget action films. This change allowed filmmakers to showcase their work on the platform, diverging from previous high-cost productions and high-profile content.

Streaming giants have invested heavily in producing original movies, series, and documentaries with the highest production values to meet this demand. Cinematic-quality visuals have become a key differentiator in a crowded market, where stunning imagery can captivate audiences and set a piece of content apart. This has directly translated into a growing market for professional-grade cameras capable of capturing footage with exceptional detail, dynamic range, color accuracy, and overall image quality that can bring stories to life on the screen.

Market Restraints

Rapid Technological Obsolescence to Hinder Market Expansion

The fast pace of technological advancements in camera hardware leads to frequent product updates and new model releases. Filmmakers and production houses might hold back on investing in costly equipment just owing to the fear that it would become outdated early, and they would have to bear the cost of further upgrades. Such uncertainty delays the decision to purchase and hence reduces the demand. All these factors hamper the cinema camera market growth.

Market Opportunities

Increasing Popularity of Implementing Robotics Generates Numerous Opportunities in Market

Robotics, the integration of science, technology, and engineering that substitutes human behavior, is emerging as a new advancement in different industries. Industrial robots have been developed widely in different sectors all over the world. Their popularity is growing daily with improved output, profitability, and appropriateness.

- In April 2024, Ross Video launched new products at the NAB 2024, including a weather graphics system and a roving robotic camera pedestal. It also acquired Bannister Lake, adding an HTML5 graphics solution to its offerings.

SEGMENTATION ANALYSIS

By Sensor Type

Super 35mm Segment Led Market Due to Its Various Benefits

By sensor type, the market is segmented into CMOS, full frame, dual pixel, super 35mm, and CCD (charged-coupled device).

Super 35mm sensors segment is projected to lead the market with a 30.05% in 2026 as they struck an optimal balance between image quality, depth of field, and compatibility with a wide range of lenses. This sensor size is a standard in the industry, providing filmmakers with a versatile and familiar format that meets both artistic and technical requirements for professional filmmaking.

CMOS sensors are expected to grow at the highest CAGR in the market due to their advantages in power efficiency, faster readout speeds, and superior image quality with lower noise levels. These features make CMOS sensors increasingly popular for high-resolution and high-frame-rate video capture, meeting the evolving demands of modern cinematography.

To know how our report can help streamline your business, Speak to Analyst

By Lens Type

Growing Preference for Optical Performance and Flexibility Fosters PL Mount Segment Growth

Based on lens type, the market is classified into EF mount and PL mount.

The PL mount segment is projected to lead the market with a 79.99% in 2026 and is expected to grow at the highest CAGR in the market, as it is widely recognized for its robust build quality, versatility, and compatibility with professional cameras. The PL mount's ability to support a wide range of high-quality lenses from various manufacturers makes it the preferred choice for filmmakers seeking superior optical performance and flexibility in their productions.

EF mount lenses are expected to grow at a lesser CAGR and hold a lesser share in the market as they are primarily designed for DSLR and mirrorless cameras, not for high-end cameras. Consequently, they offer less versatility and fewer professional-grade options than PL mount lenses, making them less appealing for professional filmmakers seeking superior optical performance and durability.

By Video Resolution

Rise in High-end Productions Boosted Full HD Resolution (1080) Segment Growth

By video resolution, the market is divided into 4K/8K resolution and full HD resolution (1080).

In terms of share, in 2026, the full HD resolution (1080) segment is projected to lead the market with a 65.67% as it provided a good balance of image quality, file size, and cost-effectiveness. It is widely adopted for various types of productions, including television, online content, and independent films, making it a versatile and accessible option for many filmmakers.

The 4K/8K resolution segment is projected to experience the most rapid growth, boasting the highest CAGR during the forecast period. These cameras present high-resolution pictures that are right for movie releases, business projects, and high-level streaming services such as Netflix, with 4K giving four times the clarity of Full HD and 8K giving even more detail.

CINEMA CAMERA MARKET REGIONAL OUTLOOK

By region, the market consists of North America, Asia Pacific, South America, Europe, and the Middle East & Africa.

North America

North America Cinema Camera Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America The region is home to major Hollywood studios and numerous independent filmmakers, ensuring a continuous need for cutting-edge cinema technology. Additionally, substantial financial resources and technological innovation in North America support the adoption and development of high-quality cameras. Furthermore, leading camera manufacturers and a robust distribution network also contribute to this dominance. As per a report by the Motion Picture Association, the U.S. alone has a 33% share of the global box office revenue. The U.S. market is projected to reach USD 96.76 billion by 2026. In 2025, North America held 33.40% of the global market share, reaching a valuation of USD 112.6 million, and is projected to grow to USD 118.72 million in 2026.

The market in the U.S. is prospering as a result of the existence of big film studios and production houses, coupled with a rising demand for quality video content. Moreover, compact and lightweight cameras are becoming increasingly popular in the region, choices favored by independent filmmakers and content creators.

Europe

Europe holds the second-highest share in the market, owing to its rich and diverse film industry, with numerous film festivals and a strong tradition of independent filmmaking. The presence of renowned film schools and production companies fosters a continuous demand for high-quality cinema equipment. The region's emphasis on high production values further drives the market for upgraded camera technology. The UK market is projected to reach USD 24.525 billion by 2026, and the Germany market is projected to reach USD 22.514 billion by 2026. The market in Europe reached USD 99.91 million in 2025, representing 29.60% of total market revenue, and is projected to reach USD 104.45 million in 2026.

Asia Pacific

Asia Pacific contributed approximately USD 98.78 million to the global market in 2025, accounting for 29.30% share, and is expected to reach USD 106.78 million in 2026, due to the rapid expansion of the film industry in countries such as China, India, and South Korea. Increasing disposable incomes and a growing middle class drive demand for high-quality content, leading to cinema infrastructure and equipment investments. Moreover, the rise of streaming platforms and digital content creation in the region further fuels the demand for advanced cinema cameras. Additionally, government initiatives and incentives to promote local film industries contribute to the market's growth in the region. The Japan market is projected to reach USD 38.322 billion by 2026, the China market is projected to reach USD 24.89 billion by 2026, and the India market is projected to reach USD 13.853 billion by 2026.

South America

South America is expected to grow at an average growth rate due to economic challenges, regional variations in the film industry, limited infrastructure, and cultural preferences. Factors such as political instability, currency fluctuations, and income inequality impact the purchasing power of filmmakers and production companies, limiting their ability to invest in high-end camera equipment.

Middle East & Africa

The Middle East & Africa region is expected to experience an average growth rate in the market due to economic conditions, cultural dynamics, regional instability, and infrastructure development. While some countries in the region, such as UAE and Saudi Arabia, have thriving film industries and a growing demand for cameras, others face economic challenges that may limit growth opportunities. The Middle East & Africa region captured 2.20% of the global market in 2025, generating USD 7.54 million in revenue, and is projected to reach USD 7.77 million in 2026.

Latin America

In 2025, Latin America generated USD 18.49 million, contributing 5.50% to global market revenue, and is projected to grow to USD 19.19 million in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Market Players to Use Mergers and Acquisitions, Partnership, and Product Development Strategies to Expand Business Reach

Major players frequently launch new products to enhance their market positioning by leveraging the latest technological advancements, addressing diverse consumer needs, and staying ahead of competitors. They prioritize portfolio enhancement and strategic collaborations, acquisitions, and partnerships to strengthen their product offerings. Such strategic product launches help companies maintain and grow their market share in a rapidly evolving industry.

Major Players in the Cinema Camera Market

To know how our report can help streamline your business, Speak to Analyst

Key players focus on product portfolio expansion and technological updates, acquisitions and partnerships, and research & development activities to proliferate product demand.

List of Key Cinema Camera Companies Studied

- Sony Group Corporation (Japan)

- Canon Inc. (Japan)

- Nikon Corporation (Japan)

- Panasonic Holdings Corporation (Japan)

- FUJIFILM Holdings Corporation (Japan)

- Hitachi Ltd. (Japan)

- JVCKENWOOD Corporation (Japan)

- Eastman Kodak Company (U.S.)

- Blackmagic Design Pty. Ltd. (Australia)

- ARRI AG (Germany)

- RED Digital Cinema, LLC (U.S.)

- Silicon Imaging, Inc. (U.S.)

- Sigma Corporation (Japan)

- Ikegami (Japan)

- Sharp Corporation (Japan)

- GoPro Inc. (U.S.)

- DJI (China)

- Leica Camera AG (Germany)

- Phase One (Denmark)

- Hasselblad (Sweden)

…and more.

KEY INDUSTRY DEVELOPMENTS

- January 2025: Blackmagic Design unveiled the Blackmagic URSA Cine 12K LF Body, a camera variant that retains the full quality and features of the URSA Cine 12K while omitting several accessories. This body-only option is ideal for seasoned cinematographers and rental facilities with the necessary accessories to set up their cameras.

- September 2024: Canon unveiled the EOS C80 cinema camera, a fresh addition to the Cinema EOS System of visual production tools. It boasts improved mobility due to its compact and lightweight design, a 6K full-frame sensor, and a comprehensive array of interfaces.

- May 2024: Canon launched the EOS R1, a mirrorless camera for the EOS R SYSTEM with an RF mount. This camera, aimed at professionals, combined advanced durability, performance, and reliability, featuring an image processor, DIGIC Accelerator, the existing DIGIC X processor, and a new CMOS sensory.

- May 2024: Kodak welcomed Rizuke Asia as its new Channel Partner for Malaysia, appointing it as an Authorized Reseller of Kodak's full range of printing plates, offset CTP systems, software solutions, and services for the publishing, commercial, newspaper, and packaging printing industries across the country.

- April 2024: Canon partnered with U.S. Customs and Border Protection (CBP) to combat counterfeit products entering the U.S. This partnership aimed to enhance CBP's trade enforcement operations against pirated and counterfeit goods, protecting America's economy, workers, businesses, and consumers.

INVESTMENT ANALYSIS AND OPPORTUNITIES

Developing new cinema camera technology is capital-intensive, requiring significant upfront R&D investment. Returns come from equipment sales, leasing, and technology licenses. Investing money in top camera makers or tech firms with a strong R&D pipeline and strong market potential can make lucrative investment opportunities.

REPORT COVERAGE

The report provides a detailed market analysis and focuses on key aspects, such as leading companies, sensor types, lens types, and video resolution. Besides, it offers insights into the market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.90% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Sensor Type

By Lens Type

By Video Resolution

By Region

|

|

Frequently Asked Questions

The market is projected to reach a valuation of USD 608.43 million by 2034.

In 2025, the market was valued at USD 337.32 million.

The market is projected to record a CAGR of 6.90% during the forecast period.

By sensor type, the Super 35mm segment led the market in 2025.

The rise of streaming platforms and the growing popularity of on-demand video content increased the demand for high-quality digital cinematography.

Sony Group Corporation, Canon Inc., Nikon Corporation, Panasonic Holdings Corporation, FUJIFILM Holdings Corporation, Hitachi Ltd., JVCKENWOOD Corporation, Eastman Kodak Company, Blackmagic Design Pty Ltd, ARRI AG, RED Digital Cinema, LLC, and Silicon Imaging, Inc. are the top players in the market.

North America dominated the global market with a share of 33.40% in 2025.

By video resolution, the 4K/8K resolution segment is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 128

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us