FPSO Market Size, Share, Growth & Industry Analysis, By Storage Capacity (Less than 1 MMBBLs, 1-2 MMBBLs, and More than 2 MMBBLs) By Water Depth (Shallow Water, Deepwater, and Ultra-Deepwater), By Construction Type (Converted and New Build), By Hull Type (Single Hull and Double Hull), By Ownership (Contractor Owned {Contractor Managed and Operator Managed} and Operator Owned {Contractor Managed and Operator Managed}), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

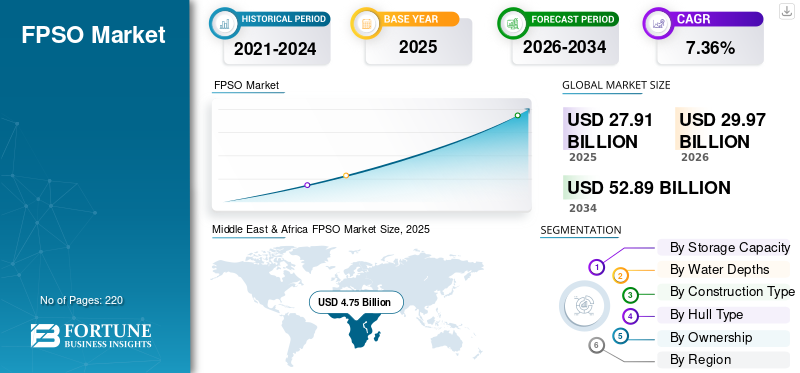

The global FPSO market size was valued at USD 27.91 billion in 2025. The market is projected to grow from USD 29.97 billion in 2026 to USD 52.89 billion by 2034, exhibiting a CAGR of 7.36% during the forecast period. The Middle East & Africa dominated the global market with a share of 36.37% in 2019.

A floating production storage and offloading (FPSO) unit is a specialized vessel used in the oil & gas industry to produce and store large volumes of hydrocarbons from offshore basins. The vessel is widely used across different water depths to store and process the crude oil produced from the wells. It is manufactured either by using an existing ship through necessary modifications or by building a new special vessel from scratch. The unit houses various types of equipment to perform tasks such as treating and separating crude oil, helping contractors manage the output efficiently and offload it, and reducing dependence on external pipeline infrastructure.

Download Free sample to learn more about this report.

FPSO MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 27.91 billion

- 2026 Market Size: USD 29.97 billion

- 2034 Forecast Market Size: USD 52.89 billion

- CAGR: 7.36% from 2026-2034

- The Middle East & Africa held the largest global market share of 36.37% in 2019.

- North America recorded a cancer cachexia market size of USD 0.80 billion in 2025.

- The progestogens segment retained the leading market position in 2026, driven by high treatment efficiency and lower cost.

North America

North America is expected to record steady growth, driven by established offshore infrastructure, ongoing production activities, and the presence of leading companies.

Europe

Europe is anticipated to experience stable market growth, driven by continued investments in offshore energy projects and technological advancements.

Asia Pacific

Asia Pacific is expected to lead market growth, supported by rising energy demand, expanding exploration activities, and offshore oil & gas developments.

U.S.

Strong offshore crude oil and natural gas production, along with continued investments in offshore infrastructure, support the U.S. market.

Japan

Japan is expected to maintain market presence through technological expertise, engineering capabilities, and the participation of leading FPSO solution providers.

Read More

LATEST TRENDS

Imposition of Long-Term Contracts Among Companies a Key Trend to Propel Growth

The global market is experiencing a large number of long-term agreements between various industry participants. These contracts involve building and operating the vessels such as front-end engineering and design (FEED), operations & maintenance, commissioning, and technology upgrading. For instance, in September 2020, SRO Solutions, a U.K. based technology company, announced the complete digitalization of a couple of floating production storage and offloading vessels owned by MODEC in Ghana.

Download Free sample to learn more about this report.

Collaborative Effort by Industry Players to Develop High Capacity Fields to Favor Industry Landscape

Different oil & gas companies are making efforts to integrate the technology offerings and produce from various assets. The partnerships are set to provide an opportunity to generate significant investments for the deployment of different platforms & equipment. For instance, in October 2020, two key hydrocarbon industry players, BP and Equinor, collectively announced to find two new oil reserves in offshore Canada. The two resources named Cambriol and Cappahayden are located at the 600 meters and 1,000 meters’ water depth, respectively.

DRIVING FACTORS

Increasing Energy Demand Globally to Aid Market Growth

Various emerging and developed countries have observed a significant increase in energy consumption over the years. The rising need for reliable fuel sources such as oil, gas, and other petrochemicals from power generation stations to operate various machinery is set to boost the floating production storage and offloading market. For instance, in September 2019, the U.S. EIA anticipated that over half of the global energy consumption increase will incur from the non-Organization for Economic Co-operation and Development (OECD) Asian nations India and China by 2050. Additionally, the report projected that the energy intake would almost double in the region, with India and China being significant contributors to the demand upsurge.

Continuous Discoveries of New Offshore Reserves with High Output Potential to Augment Growth

Different oil & gas exploration companies have demonstrated their efforts to encounter new bulk capacity reservoirs unlocking new industry potential. The enterprises have drilled various wildcat wells in different basins to substantiate their findings and quantify the production capacity of zones. For instance, in December 2020, Brazilian company Petrobras confirmed its discovery of a new oil reserve in the Buzios field in the Santos Basin located in offshore Brazil. The well is located in an ultra-deepwater depth of about 1,850 meters with an excellent quality oil reservoir.

RESTRAINING FACTORS

High Initial Constructing Cost to Hinder Market Growth

The construction of floating production, storage, and offloading vessels requires building and integrating various components & structures, leading to a significant amount of money. Additionally, certain selection & designing factors are considered for the deployment of FPSO in the oil & gas industry, including production capacity, hydrocarbon reserves, number of wells, water depth, and existing infrastructure constraining the building and operational flexibility. These factors are likely to impact the FPSO market growth.

SEGMENTATION

By Storage Capacity Analysis

To know how our report can help streamline your business, Speak to Analyst

1-2 MMBBLs Segment Anticipated to Lead

Based on storage capacity, the market is trifurcated into less than 1 MMBBLs, 1-2 MMBBLs, and more than 2 MMBBLs.

FPSO units with a storage capacity of less than 1 million barrels (MMBBLs) are projected to showcase a significant rise during the forecast period as the vessels greatly help in near-shore depths providing less complex operations.

The 1-2 MMBBLs segment is anticipated to experience considerable growth due to the awarding of new vessel contracts with large capacity and the detection of new bulk reserves.

By Water Depth Analysis

Deepwater Segment to Dominate Backed by New Reserves Discovery in Deeper Formations

Based on water depth, this industry can be primarily segregated into shallow water, deepwater, and ultra-deepwater.

Continuous discovery of deepwater reserves, coupled with the rising inclination of E&P companies to produce from deeper reservoirs, is set to propel the deepwater segment.

The shallow water segment is expected to hold a significant market share as various regions are currently focusing on producing from continental shelves and continental slopes.

By Construction Type Analysis

New Build Segment Projected to Generate Highest CAGR

Based on the construction type, the market is segmented into a converted and new build.

The new-build segment is expected to hold substantial growth due to the higher cost of construction for new vessels and a wide range of configuration options, and optimum design flexibility as per the contractor’s requirements.

The converted segment is likely to grow considerably owing to its low capital expenditure, along with short procurement cycles.

By Hull Type Analysis

Double Hull Segment Demand is Augmented by Various Design Advantages Supporting Easy Operations

Based on hull type, the market is bifurcated into a single hull and double hull.

The double hull segment is likely to witness significant growth over the forecast timeframe as the design offers a dedicated containment area and lowers the risks of oil spills.

A single type of hull imparts more design stability to the system as it balances the meta-centric height and center of gravity of the vessels optimally. This is likely to lead to segmental growth during the forecast period.

By Ownership Analysis

Operator Owned Segment to Hold Dominating Position

Based on ownership, the market can be broadly categorized into contractor-owned and operator-owned, with further partitions into subcategories centered on the management of the vessels.

Various contractors are participating across the industry to provide vessels to the field operators within a little time, propelling the contractor-owned segment size.

The presence of key operators and a long-standing presence in developing offshore reservoirs complement the operator-owned segment's growth.

REGIONAL INSIGHTS

Middle East & Africa FPSO Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The market has been analyzed across five key regions, including North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific is anticipated to be one of the leading regions in the global floating production storage and offloading market due to rapidly rising energy demand among the developing economies. Additionally, the increasing exploration & production activities in the region is expected to favor the market growth. For instance, in December 2017, China National Petroleum Corporation (CNPC) announced the discovery of new reserves in the Junggar Basin located in Xinjiang province with a total estimated reservoir capacity between 0.52 to 1.24 billion tons of recoverable crude oil.

North America has a long-standing presence in the floating production storage and offloading industry and operates one of the time-tested units in its harsh water conditions. Besides, high production targets from the regional agencies and the presence of various industry giants are expected to favor the regional growth. For instance, in November 2019, the U.S. Energy Information Administration reported that around 19% of the country’s total crude oil production in 2018 was achieved from the Federal Gulf of Mexico waters. The organization further stated that approximately 3% of the national dry gas was derived from the same fields.

The Middle East & Africa is projected to be the most prominent region globally due to increasing investments in exploring offshore assets and discovering new bulk reserves. The region stood at USD 4.75 billion in 2019. Various regional countries, including Angola, Nigeria, and Ghana, have significantly proven and unproven offshore reservoirs and exhibit an established presence in deploying FPSO units at different depths. The collaboration efforts from various players to explore these reserves is another factor augmenting the regional growth. For instance, in November 2020, a Nigerian oil & gas company First E&P announced to initiate oil production through the Abigail-Joseph floating production storage and offloading vessel located in shallow waters of the country’s offshore basin. The company chartered the vessel from Yinson in February 2019 with the seven-year agreement and an option to extend it up to 15 years.

KEY INDUSTRY PLAYERS

MODEC to Advance its Fleet Ownership and Initiate Several Contracts to Fortify its Industry Foothold

Various regional and global companies are actively participating in the industry to provide different components, equipment, services, and solutions. The companies concentrate on enhancing their offerings to deliver cost-effective operation solutions and foster production & processing capacities. MODEC, Inc. is a Japanese enterprise dealing in engineering, procurement, construction, and installation of floating production storage and offloading units. The company provides a wide range of services primarily related to the FPSO hull and mooring, along with operations & maintenance solutions, to gain various long-term agreements.

For instance, in December 2020, Modec Inc. secured a contract from Woodside to deliver the operations & maintenance contract for Sangomar floating production storage and offloading vessels in Senegal. The new deal is set to cover the installation & commissioning operations, along with O&M, for a decade with an optional extension for up to 10 additional years after the initial period.

LIST OF KEY COMPANIES PROFILED:

- Petrobras (Brazil)

- CNOOC (China)

- Total (France)

- Royal Dutch Shell (Netherlands)

- Chevron (U.S.)

- ExxonMobil (U.S.)

- BP (UK)

- Equinor (Norway)

- Woodside Energy (Australia)

- Aker Solutions (Norway)

- Dana Petroleum Limited (UK)

- Vår Energi (Norway)

- Vietsovpetro (Vietnam)

- Eni (Italy)

- Dommo Energia (Brazil)

- Keppel Offshore & Marine (Singapore)

- BW Offshore (Norway)

- Teekay (Bermuda)

- Bumi Armada Berhad (Malaysia)

- SBM Offshore (Netherlands)

- Yinson Holdings Berhad (Malaysia)

- Bluewater (Netherlands)

- MISC Berhad (Malaysia)

- Modec Inc. (Japan)

- Rubicon Offshore (Singapore)

- Saipem (Italy)

KEY INDUSTRY DEVELOPMENTS:

- December 2020 – SBM Offshore extended its prevailing contract with Shell for leasing of Espirito Santo FPSO located in Brazil. The extension will last for five years, with the new operational period from December 2023 to December 2028.

- November 2020 – Keppel Offshore & Marine secured an order worth about USD 75 million from an unknown customer to deliver conversion work for an FPSO vessel. The contract involves fabrication & integration operations for components like riser balconies, topside modules, and spread mooring support, among other services.

REPORT COVERAGE

The research and business intelligence report offer an in-depth analysis of the market. It further provides details on the adoption of the product across several regions. Information on trends, opportunities, drivers, restraints, and threats of the market can further aid stakeholders in gaining valuable insights into the market. The report offers a detailed competitive landscape by presenting information on key players and their strategies in the market.

Report Scope & Segmentation

Request for Customization to gain extensive market insights.

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Million) |

|

Segmentation |

Storage Capacity; Water Depth; Construction Type; Hull Type; Ownership; and Region |

|

By Storage Capacity |

|

|

By Water Depth |

|

|

By Construction Type |

|

|

By Hull Type |

|

|

By Ownership |

|

|

By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the FPSO market size was USD 27.91 billion in 2015 and is projected to reach USD 52.89 billion by 2034.

In 2025, the Middle East and Africa FPSO market stood at USD 4.75 billion.

Registering a CAGR of 7.36%, the FPSO market will exhibit substantial growth over the forecast period (2026-2034).

The 1-2 MMBBLs storage capacity segment is anticipated to dominate this market during the forecast period.

The growing discovery of new crude oil reserves in offshore locations, along with the increasing energy demand, is the major factor expected to drive the market growth.

Petrobras, CNOOC, BW Offshore, MODEC, and Total are key participants operating across the industry.

The Middle East & Africa dominated the market in terms of share in 2019.

The discovery of new offshore reserves, along with significant oil, attracts the required investments to deploy FPSO vessels and produce hydrocarbons from the large capacity reserves over a longer period through optimized production & processing operations.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us