Heat Meter Market Size, Share & Industry Analysis, By Type (Ultrasonic, Mechanical, and Electromagnetic), By Technology (Wired and Wireless), By Application (Residential, Commercial, Industrial, and Others), Regional Forecast, 2026-2034

Heat Meter Market Size and Future Outlook

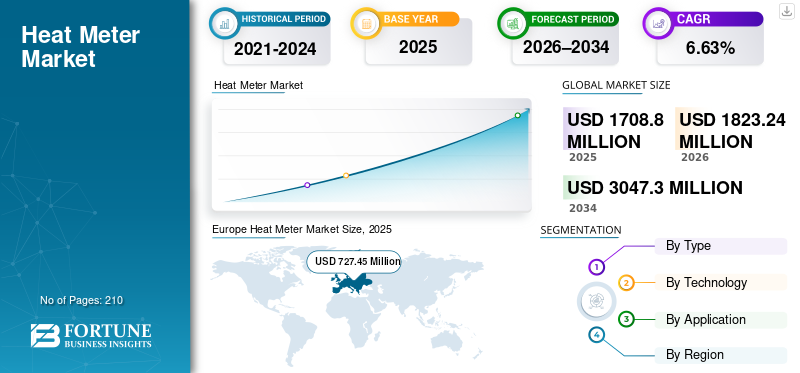

The global heat meter market size was valued at USD 1,708.80 million in 2025. The market is projected to grow from USD 1,823.24 million in 2026 to USD 3,047.30 million by 2034, exhibiting a CAGR of 6.63% during the forecast period. Europe dominated the heat meter market with a market share of 42.57% in 2025.

The increasing focus on energy efficiency and the rising need for accurate energy consumption measurement largely drive the growth of the global heat meter market. Governments are implementing stricter regulations to reduce energy waste and promote sustainability, making heat meters essential in both residential and commercial sectors. With the ongoing trend toward smart cities, the adoption of IoT-enabled heat meters is on the rise, providing real-time data for better energy management. As urbanization increases, district heating systems, which rely on efficient heat distribution, are becoming more common, driving the adoption of heat meters. Heat meters measure thermal energy consumption by accurately monitoring flow rate and temperature differences in heating systems.

- For instance, in July 2019, Kamstrup’s MULTICAL® 603 heat meter was documented in the official product literature with a data sheet revision, indicating that this version of the meter (with specifications and features current at that time) was available. This revision date is visible on the product data documentation associated with the MULTICAL® 603 heat meter. The MULTICAL® 603 is designed as an ultrasonic, smart heat (and cooling) meter providing accurate thermal energy measurement across district heating and other thermal systems. It supports programmable data logging, long battery life, and a range of communication options suitable for modern metering requirements.

Kamstrup, Zenner International GmbH & Co. KG, Siemens AG, ITRONX, and others are the key players operating in the heat meter industry. Kamstrup is a Danish metering solutions company that develops and supplies intelligent ultrasonic heat meters and related technologies to accurately measure and optimise thermal energy consumption for utilities and buildings worldwide.

Download Free sample to learn more about this report.

Heat Meter Market Takeaways

- 2025 Market Size: USD 1,708.80 million

- 2026 Market Size: USD 1,823.24 million

- 2034 Forecast Market Size: USD 3,047.30 million

- CAGR: 6.63% from 2026–203

- Europe dominated the heat meter market with a 42.57% share in 2025.

- The mechanical segment is projected to grow at a 6.53% CAGR during the forecast period.

- The wireless segment is expected to register the highest growth with a 7.16% CAGR during the forecast period.

North America

North America generated USD 251.44 million in 2025 and is projected to reach USD 266.38 million in 2026.

Europe

Europe led the global market with a valuation of USD 727.45 million in 2025 and is projected to record the highest regional CAGR of 6.91% during the forecast period.

Asia Pacific

Asia Pacific was the second-largest regional market in 2025, reaching USD 500.69 million, supported by strong demand across China, India, and Japan.

U.S.

The heat meter market was valued at USD 182.34 million in 2025, accounting for approximately 10.67% of the global market.

Japan

The heat meter market was valued at USD 62.29 million in 2025, representing approximately 3.65% of global revenue.

Read More

HEAT METER MARKET TRENDS

Shift Towards Smart, IoT-enabled meters and Integration with Energy Management Systems are the Key Market Trends

The heat meter market is evolving rapidly as global priorities shift toward energy efficiency, sustainability, and digital infrastructure. One key trend is the adoption of smart heat meters equipped with advanced sensors and communication technologies, such as IoT and wireless connectivity, enabling real‑time monitoring and remote data collection. This shift allows utilities and building managers to optimize energy usage, detect anomalies earlier, and reduce operational costs. Static heat meters use ultrasonic or electronic measurement without moving parts, ensuring high accuracy and long-term reliability.

Another significant trend is integration with smart grids and building automation systems, where heat meters feed critical consumption data into larger energy management platforms to support demand response and load balancing. Urbanization and growth in district heating and cooling networks, particularly in densely populated regions, are creating new demand for accurate and reliable heat metering solutions. There is also an increased focus on energy transparency and consumer awareness, with end‑users demanding precise billing and insights into their heating usage patterns.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Strong Emphasis on Energy Efficiency and Cost Savings to Drive Market Growth

The heat meter market is being driven by a strong global emphasis on energy efficiency and cost savings across residential, commercial, and industrial sectors. As energy prices rise and end‑users seek better control over consumption, the ability of heat meters to provide precise measurement and billing transparency has become increasingly important.

Governments and regulatory bodies are also incentivizing energy conservation and emissions reduction, prompting utility providers and building owners to adopt advanced heat metering technologies to comply with efficiency standards and greenhouse gas targets. Another significant driver is the expansion of district heating and cooling systems in urban and suburban regions, where centralized thermal networks require accurate measurement to allocate costs fairly and manage load effectively.

MARKET RESTRAINTS

Lack of Standardization and High Initial Installation Cost May Stifle Market Growth

One key restraint is the high initial installation cost of advanced heat metering systems, particularly in older buildings or areas lacking existing infrastructure. These upfront costs can be a significant barrier for small-scale property owners and utilities, limiting their ability to implement modern metering solutions.

Additionally, retrofitting existing systems to accommodate advanced digital or ultrasonic meters in older buildings and networks adds further costs and operational challenges. Another restraint is the lack of standardized regulations across different regions, making it difficult for manufacturers to design universally compatible solutions.

MARKET OPPORTUNITIES

Growing Adoption of Smart Cities and Digital Infrastructure to Drive the Market Opportunity

The heat meter market presents several growth opportunities, especially as demand for energy-efficient solutions continues to rise. One significant opportunity lies in the growing adoption of smart cities and digital infrastructure. As urban areas modernize, the integration of heat meters into smart grids and building automation systems can provide enhanced energy management, real-time monitoring, and better demand response. This creates opportunities for innovation in meter designs and the incorporation of advanced technologies such as Internet of Things (IoT) sensors and cloud-based data analytics.

Furthermore, the expansion of district heating networks in developing regions provides a substantial market opportunity, as these areas look to improve energy distribution efficiency and lower costs. The push towards renewable energy sources such as biomass, geothermal, and solar thermal energy also offers opportunities for heat meters designed to support these sustainable heating methods.

MARKET CHALLENGES

Limited Availability of Skilled Labor Presents Significant Challenges for Market Growth

The limited availability of skilled labor is a significant challenge for the heat meter market, particularly in the installation, maintenance, and integration of advanced metering systems. As technology in heat metering continues to evolve, there is a growing need for professionals with specialized knowledge in areas such as IoT, innovative grid systems, and advanced data analytics. However, many regions face a shortage of technicians and engineers who are adequately trained to handle the complexities of modern heat meters, including those with digital and ultrasonic features.

Segmentation Analysis

By Type

Ultrasonic is a Dominant Segment Owing to Higher Accuracy and Reliability

On the basis of type, the market is classified into ultrasonic, mechanical, and electromagnetic.

In 2025, the ultrasonic dominated the market share. Ultrasonic heat meters dominate the market due to their superior accuracy, reliability, and long-term performance. Unlike traditional mechanical meters, ultrasonic meters’ measure heat consumption by analyzing the flow of liquid using sound waves, which eliminates moving parts and reduces maintenance needs. This results in more precise readings and a longer lifespan.

The mechanical segment is experiencing the highest growth and is expected to grow at a CAGR of 6.53% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Wired is a Dominant Segment Owing to Stable, Reliable Data Transmission & Connectivity

On the basis of technology, the market is classified into wired and wireless.

In 2025, the wired segment dominated the global market. Wired technology dominates the heat meter market due to its reliability and stable data transmission. Wired meters are also less prone to security risks compared to wireless systems, which can be vulnerable to hacking or data breaches. Additionally, the cost-effectiveness of wired infrastructure, especially in regions where existing wired networks are already in place, contributes to its continued dominance in many markets. Wired connections provide stable, secure, and uninterrupted data transmission for heat metering systems.

The wireless segment is expected to grow at a CAGR of 7.16% during the forecast period.

By Application

Residential Dominated the Market Due to Growing Energy Efficiency Regulations and Smart Home Integration

On the basis of application, the market is classified into residential, commercial, industrial, and others.

In 2025, the residential segment held the largest market share. Heat meters allow homeowners to monitor better and manage energy use, leading to cost savings and more sustainable practices. Additionally, the integration of smart home technology has amplified demand for heat meters in residential applications, enabling features like real-time monitoring, remote control, and automation.

The commercial segment is expected to grow at a CAGR of 6.50% during the forecast period.

Heat Meter Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

Europe Heat Meter Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the third-highest share in 2025, valued at USD 251.44 million, and is expected to lead the market share in 2026 with USD 266.38 million.

North America’s heat meter popularity is fueled by rising energy costs and stronger energy‑efficiency mandates, prompting utilities and building owners to adopt precise thermal measurement for better consumption control and cost allocation. For example, residential heating expenses in the U.S. have seen notable upward pressure, making accurate metering tools more valuable for homeowners and property managers alike.

U.S. Heat Meter Market

Based on North America’s substantial contribution and the U.S. dominance within the region, the U.S. market was valued at USD 182.34 million in 2025, accounting for roughly 10.67% of the global market size.

Europe

Europe is projected to record a growth rate of 6.91% in the coming years, which is the highest among all regions, and was valued at USD 727.45 million in 2025. In Europe, the strong regulatory environment surrounding energy efficiency and consumption transparency is a significant factor driving heat meter demand. EU directives require heat meters in multi‑apartment and district heating systems to ensure accurate, fair billing based on actual usage rather than estimates, and mandate that all newly installed meters be remotely readable by 2026.

Germany Heat Meter Market

The German market in 2025 was valued at USD 189.69 million and is estimated to hit USD 205.11 million in 2026, representing roughly 11.10% of the global revenues.

Asia Pacific

Asia Pacific market reached USD 500.69 million in 2025 and secure the position of the second-largest region in the market. In the region, India and China market were valued at USD 49.53 million and USD 234.68 million, respectively, in 2025.

The popularity of the Asia Pacific heat meters’ market is driven by rapid urbanization and the expansion of district heating networks in cities like Beijing, Tokyo, and New Delhi. As urban populations grow, there is an increasing demand for efficient energy distribution systems, where accurate heat measurement is critical for fair billing and load management. The region’s focus on energy efficiency and sustainability also plays a significant role, with governments implementing stricter regulations to curb energy waste and reduce carbon footprints. For example, China has made significant strides in adopting district heating systems in northern regions, further boosting the demand for advanced heat meters.

Japan Heat Meter Market

The Japan market was valued at USD 62.29 million in 2025, accounting for roughly 3.65% of global revenues.

The demand is driven by urbanization, energy efficiency regulations, and the integration of innovative technologies in district heating systems.

China Heat Meter Market

China’s market value was accounted for USD 17.59 million in 2025, representing roughly 8.83% of the global market.

India Heat Meter Market

The India market reached a valuation of USD 234.68 million in 2025, accounting for roughly 13.73% of global revenues.

Latin America

Latin America is expected to witness moderate growth in this market space during the forecast period. The Latin America market reached a valuation of USD 103.38 million in 2025.

In Latin America, the demand for heat meters is growing due to the region's increasing focus on improving energy infrastructure and reducing energy losses. Countries like Brazil are expanding their district heating networks in urban areas, leading to greater adoption of heat metering solutions to ensure accurate billing and optimize energy use.

Brazil Heat Meter Market

Brazil's market value reached at USD 46.75 million in 2025, representing roughly 2.74% of the global market.

Middle East & Africa

The Middle East & Africa are expected to witness significant growth in this market space during the forecast period. The Middle East & Africa market was valued at USD 125.84 million in 2025.

In the Middle East & Africa, heat meter adoption is supported by expanding urban infrastructure, rising district cooling and heating projects, and growing emphasis on energy efficiency in new developments.

GCC Heat Meter Market

The GCC market was valued at USD 60.34 million in 2025, representing roughly 3.53% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Vendors are Actively Expanding Their Market Share Via Partnerships, Business Expansion, And Technological Advancements

The global heat meter market holds a consolidated market structure, constituting prominent players such as Kamstrup, Zenner International GmbH & Co. KG, Siemens AG, and others. Companies operating in the heat meter industry are adopting targeted growth strategies focused on strengthening their product portfolio, technical capability, expanding manufacturing presence, and other areas.

- For instance, in November 2024, Kamstrup announced that LoRa communication modules can now be ordered as built-in, factory-mounted options in its MULTICAL 403, 603, and 803 thermal energy meters. The company highlighted LoRaWAN as an open protocol that supports interoperability with third-party systems. It emphasized that the meters provide time-stamped data suitable for billing and valuable analytics for smart-city and residential deployments that require frequent, reliable reads.

Other key players in the global market include Kamstrup, Zenner International GmbH & Co. KG,

Siemens AG, and others. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY HEAT METER COMPANIES PROFILED

- Kamstrup (Denmark)

- Zenner International GmbH & Co. KG (Germany)

- Siemens AG (Germany)

- ITRON (U.S.)

- Danfoss (Denmark)

- Diehl Stiftung & Co. KG (Germany)

- Apator S.A. (Poland)

- BMETERS Srl (Italy)

- Trend Control Systems Ltd. (U.K.)

- Premier Control Technologies Ltd. (U.K.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: ZENNER reported its Enlit Europe 2025 showcase, focusing on the B.One ecosystem that links meters, platforms, and software into a single digital infrastructure approach. The company positioned LoRaWAN as a key enabler because a single network can support multiple utility applications, helping accelerate connected metering rollouts (including heat metering) where interoperability and scalable device fleets matter for citywide deployments.

- July 2025: in a SHARKY Series brochure dated 2025-07, Diehl highlights deployments and scale: one case notes 2,500 SHARKY 775 units ordered initially and “over 30,000” installed over time at Izmir Jeotermal, enabling automated meter reading and monthly billing. The brochure also stresses modular communications and compliance alignment with the EU Energy Efficiency Directive (EED) expectations for modern metering.

- December 2024: Siemens’ UH50 ultrasonic heat/cooling energy meter documentation (dated 2024-12-20) specifies performance and compliance points such as MID accuracy class 2 and a flow measuring range of 1:100 (EN 1434) with a total range up to 1: 1,000. It also notes multiple communication module options and suitability for district heating and multi-dwelling buildings—key requirements when utilities push remote reading and reliable low-flow accuracy.

- February 2024: Danfoss issued a SonoMeter 40 datasheet dated 2024.02, describing ultrasonic compact energy meters intended for billing and AMR. It lists concrete specs such as nominal flows from qp 0.6 to 60 m³/h, optional dynamic ranges up to 1:250 (class 2), and battery lifetime at least 15+1 years. These quantified performance claims support adoption in projects where extended battery life and wide turndown reduce total lifecycle cost.

- March 2023: BMETERS announced its General Catalogue 2023 (dated 14.03.23), explicitly including Thermal Energy Metering in the product navigation and making the new catalog available for download. While a catalog release is not a single-product launch, it signals an updated commercial lineup and documentation set—often used by distributors, EPCs, and utilities to shortlist heat meters and compatible remote-reading options for upcoming tenders.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.63% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Type, Technology, Application, and Region |

| By Type |

|

| By Technology |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1,708.80 million in 2025 and is projected to reach USD 3,047.30 million by 2034.

In 2025, the market value stood at USD 727.45 million.

The market is expected to exhibit a CAGR of 6.63% during the forecast period of 2026-2034.

The ultrasonic segment led the market by type.

Rising energy efficiency regulations, demand for accurate billing, expansion of district heating networks, and adoption of innovative metering technologies are driving the market.

Kamstrup, Zenner International GmbH & Co. KG, Siemens AG, and others are prominent players in the market.

Europe dominated the market in 2025.

Stricter energy regulations, growth of district heating systems, rising energy costs, and increasing use of smart, digitally connected meters are expected to favor heat meter adoption.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us