Industrial Gas Turbine Market Size, Share & Industry Analysis, By Capacity (1-2MW, 2-5MW, 5-7.5MW, 7.5-10MW, 10-15MW, 15-20MW, 20-30MW, 30-40MW, 40-100MW, 100-150MW, 150-300MW, 300+MW), By Technology (Heavy Duty, Light Industrial, Aeroderivative), By Cycle (Simple Cycle, Combined Cycle), By Sector (Electric Power Utility, Oil & Gas, Manufacturing) and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

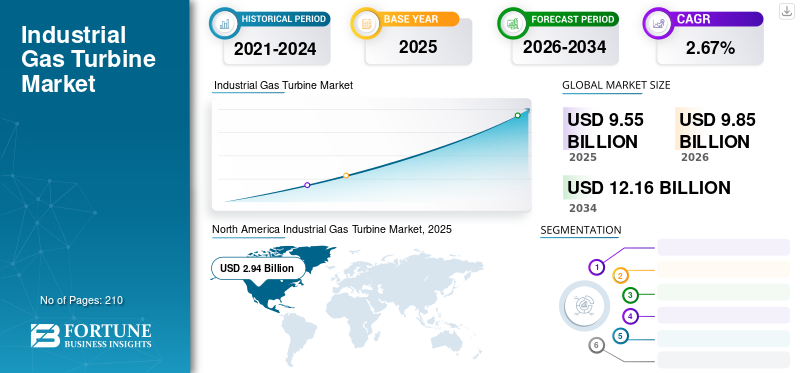

The global industrial gas turbine market size was USD 9.55 billion in 2025 and is expected to grow from USD 9.85 billion in 2026 to USD 12.16 billion by 2034 at a CAGR of 2.67% over the forecast period (2026-2034). North America dominated the industrial gas turbine market with a market share of 30.84% in 2025. The Industrial gas turbine market in the U.S. is projected to grow significantly, reaching an estimated value of USD 2.77 billion by 2032.

An industrial gas turbine is a combustion engine that generates mechanical energy from various fuels such as natural gas or liquid fuels. This mechanical energy is used to drive an integrated generator that produces electric energy. Traditional gas-fired and oil-fired steam power plants have been replaced by efficient combined-cycle power plants using gas turbines to fuel gas or oil. The electricity demand is increasing across the globe, along with the high demand for clean energy, which are the major factors that are expected to propel the global market growth from 2023 to 2032.

Download Free sample to learn more about this report.

Global Industrial Gas Turbine Market Overview

Market Size:

- 2025 Value: USD 9.55 billion

- 2026 Value: USD 9.85 billion

- 2034 Forecast Value: USD 12.16 billion, with a CAGR of 2.67% from 2026–2034

Market Share:

- Regional Leader: North America held a 30.84% market share in 2025, supported by ongoing shale gas exploration and a large number of natural gas–powered turbine plants. The U.S. alone is projected to reach USD 2.77 billion by 2032.

- Fastest-Growing Region: Asia Pacific is expected to grow at a significant CAGR, driven by rapid industrialization, rising energy demand, and clean energy initiatives in China, India, Japan, South Korea, and Australia.

- End-User Leader: The electric power utility segment led the market in 2023, driven by the shift from coal and steam plants to gas turbine–powered stations for cleaner, more efficient power generation.

Industry Trends:

- Broader Scope in Emerging Economies: Growth in industrial hubs and foreign direct investment (FDI) in China, India, Brazil, and Southeast Asia is creating new opportunities.

- Hydrogen Integration: Increasing use of hydrogen-compatible gas turbines, with recent projects achieving 100% renewable hydrogen combustion.

- Combined Cycle Expansion: Strong adoption of combined cycle systems for higher efficiency, effective waste heat use, and lower emissions.

Driving Factors:

- Emission Reduction Technology: Gas turbines emit significantly less CO₂ than coal-fired plants, and hydrogen-fueled turbines offer zero-carbon potential.

- Rising Electricity Demand: Expanding industrial sectors and infrastructure projects are increasing global electricity requirements, boosting turbine installations.

- Clean Energy Shift: Stricter environmental regulations and decarbonization policies are accelerating gas turbine adoption.

- Fuel Flexibility: Ability to run on multiple fuels, including natural gas, oil, and hydrogen, enhances adaptability and resilience.

The coronavirus (Covid-19) was first identified in China’s Hubei province in December 2019 and has since become a global health threat, affecting more than 200 countries. The power sector is one of the most widely affected domains, and the lockdowns have added to the adverse effect of the pandemic. The unavailability of human resources due to lockdown has caused delays in power projects. The lockdown caused supply chain disruptions and issues in project financing. Recently, the Myanmar power plant projects initially scheduled to complete in 2020 were delayed due to COVID-19. The deputy minister for Electricity and Energy (MOEE) said three imported liquefied natural gas (LNG) power projects and a gas power project are still not operational because of the COVID-19 pandemic. Due to commercial flight bans and travel restrictions, the machinery, the power generation equipment, and experts required to install it were unable to reach Myanmar by the deadlines.

The power plant operators in the U.S. continue to change procedures at their facilities, including pushing back scheduled maintenance due to lockdowns imposed due to the coronavirus pandemic. The changes have affected many companies such as Siemens and General Electric (GE), major manufacturers of industrial gas turbines, and service providers to power plants when these global companies are already taking a revenue hit due to COVID-19.

Industrial Gas Turbine Market Trends

Broader Scope in Emerging Economies is the Latest Trend in Market

The rise in the industrial hubs and growing foreign direct investment (FDI) in all major manufacturing sectors across emerging economies such as China, India, Brazil, and Southeast Asian countries are projected to create lucrative growth opportunities for this market during the forecast period. Various foreign developers who intend to set up their businesses through FDI incentive schemes are being focused on emerging economies. This will indirectly boost the economy of the country and enhance industrialization.

Countries such as the US and many Asian countries have evolved and restructured their manufacturing policies and procedures to attract investments and enable growth. Industrialization will boost the automation process to improve the overall efficiency of production and ease operations. Hence, it can be concluded that the growth of the industrial sector, especially in the emerging economies, will create an opportunity for the global market.

Download Free sample to learn more about this report.

Industrial Gas Turbine Market Growth Factors

Gas Turbine Technology Reduces Greenhouse Emissions Fuels the Market Growth

Conventional coal-fired power plants are known to emit large amounts of toxic gases and contribute majorly to heating. Coal-fired power generating plants are one of the largest contributors to emissions. The rising greenhouse gas emissions create the urgency to develop cleaner techniques to get electricity, which is predicted to build up the demand for industrial gas turbines within the coming decade.

Natural gas, a primary fuel of gas turbines, contains very little sulfur, meaning virtually no sulfur dioxide is emitted. CO2 emission from gas turbines burning natural gas is also very low–0.37 kilograms of CO2 per kWh of electricity generated. This compares to 1.01 kg/kWh for lignite and 0.8 kg/kWh for anthracite. Thus, the above factors drive the industrial gas turbine market growth during the forecast period.

The advantage of gas turbines is that they can run on many fuels other than natural gas. Some of these fuels, such as hydrogen (H2), contain no carbon at all and do not emit carbon dioxide when burned. In addition, hydrogen can be deployed in new and existing gas turbines, reinforcing the understanding that solutions to reduce carbon dioxide in the field and equipment waiting to be installed are already available. Oil and gas operations are responsible for about 15% of all energy-related emissions worldwide, which is equivalent to 5.1 billion tons of greenhouse gases. According to the Net Zero Emissions by 2050 scenario of the International Energy Agency, the emission intensity of these activities will decrease by 50% before the end of the decade. Combined with the reduction of oil and gas consumption in this scenario, emissions from oil and gas activities will be reduced by 60% by 2030.

Growing Demand for Electricity Augment the Growth of the Global Market

The high increase across the world, flourishing industrial sector, and growth in infrastructure development activities result in an enormous rise in demand for electricity. As the demand for electricity increases, several countries across the planet are increasing their electricity generating capacity by installing new plants or expanding the capacity of the prevailing one. Due to stringent government norms regarding greenhouse gas emissions, companies are more inclined to adopt industrial gas turbine systems. These factors will augment the growth of the market during the forecast period.

RESTRAINING FACTORS

Volatility in Natural Gas Prices May Hinder Market Growth

Natural gas prices are affected by actions that can disrupt the supply of natural gas. Geopolitical tensions are a disruptive factor that causes uncertainty about the availability or demand for gas. This can cause higher volatility within the prices of gas. The cost of gas within the U.S. has fallen drastically due to shale gas exploitation, but elsewhere within the world, the value remains relatively high. Most of the countries in the Middle East region account for a significant share of natural gas reserves. It is a highly unstable region due to political and cultural issues. Moreover, from the past few months, due to the Covid-19 pandemic, the demand for natural gas decreased significantly. Thus the costs of gas also dropped, which creates a negative impact on market growth.

Industrial Gas Turbine Market Segmentation Analysis

By Capacity Analysis

The 150-300 MW Segment Would Hold the Largest Market Share

Based on capacity, the 150-300 MW segment is projected to dominate the market with a share of 33.49% in 2026. These capacity turbines are primarily used in the power generation industry. As the trend of power generation has shifted to reduce emissions of GHGs, mainly considering the environmental factors, the 300+ MW has gradually acquired a noble market share in the industry.

The small capacity industrial gas turbine segments of 1-2 MW, 2-5 MW, 5-7.5 MW, 7.5-10 MW, 10-15 MW, and 15-20 MW are increasing due to the high availability of gas. These small capacity gas turbines are modular and can operate on two fuels. These small capacity turbines are used for combined heat & power plants and co-generation plants.

By Technology Analysis

Heavy Duty Technology to Carry a Dominant Market Share

Based on technology, the heavy-duty segment is projected to dominate the market with a share of 60.27% in 2026. A growing number of manufacturing plants, coupled with the integration of large-scale economic zones across developing nations, have set up a commendable business platform. Growth within the integration of captive generating power stations to serve the electricity demand across industrial establishments will expand the heavy-duty segment.

Aeroderivative segments have gained significant market share in the global market due to the availability of highly flexible and mobile technologies. Furthermore, the segment finds a diverse application portfolio, including marine propulsion, utility generation, and district heating.

By Cycle Analysis

Combined Cycle Segment Hold Dominant Market Share

Based on cycle, the combined cycle segment is projected to dominate the market with a share of 63.03% in 2026, majorly due to environmental proximity, effective waste heat utilization, and operational efficiency. The combined cycle requires more investment as compared to the straightforward cycle, and thus these plants are inbuilt phases. First, the simple cycle plants are constructed and then are converted to a combined cycle gradually.

The simple cycle segment is likely to grow at a significant pace during the forecast period. The construction of simple cycle plants is easy and more convenient as compared to combined cycle plants and these types of power plants are also cost-friendly as well as efficient. The construction of only simple cycle power plants is increasing across the world. This drives growth in the simple cycle segment during the forecast period.

By Sector Analysis

To know how our report can help streamline your business, Speak to Analyst

Electric Power Utility Sector Held the Highest Market Share

Based on sector, the electric power utility segment is projected to dominate the market with a share of 77.08% in 2026. A growing focus toward the refurbishment of traditional steam and coal-fired power plants with gas or other renewable energy power generating stations will boost the market. The high efficiency in power generation from gas turbines has given this technology a whip hand as compared to the traditional power generation plants.

The oil and gas segment is likely to expand significantly during the forecast period. The exploration and production activities are increasing rapidly, and the volume of gas generation is also increasing. The pipeline projects are also increasing significantly. Thus, drives growth in an oil and gas segment during the forecast period.

REGIONAL INSIGHTS

The global industrial gas turbine market has been analyzed across five key regions, including North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

North America Industrial Gas Turbine Market, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America accounted for USD 2.94 billion in 2025, representing 30.84% of the global market share, and is projected to reach USD 3.04 billion in 2026. The region has a large number of industrial gas turbine plants operating on natural gas because of the ongoing increased shale gas exploration activities in the region. The U.S. Energy Information Administration (EIA) stated that presently more than 40% of the nation’s power comes from coal whereas around 25% from natural gas. The EIA expects natural gas to become the primary fuel for power generation by 2035.

In 2023, the U.S. recorded a growing economy with reduced greenhouse gas emissions due to the use of gas turbines. After two years of rising emissions as the country recovered from the COVID-19 pandemic and related economic disruptions, emissions are set to decline by 1.9% annually in 2023, while the economy grew by 2.4% annually. U.S. emissions remained below pre-pandemic levels, falling 17.2% below 2005 levels. The U.S. market is projected to reach USD 3.02 billion by 2026.

Asia Pacific

In 2025, Asia Pacific held 26.11% of the global market, reaching a valuation of USD 2.48 billion, and is projected to grow to USD 2.57 billion in 2026. Asia Pacific is estimated to grow at a significant CAGR during the forecast period. The market growth in the region can be accredited to several factors such as rapid industrialization, the rising demand for energy, and increasing demand for clean energy technologies. The Asia Pacific region is majorly dependent on coal for power production. Coal combustion causes a significant amount of air pollution. Government initiatives to reduce carbon emissions have given rise to the use of gas turbines in countries like Japan, China, Australia, South Korea, India, etc. Currently, China is drafting its 14th Five Year Plan, which will be most favorable for gas power development. The 14th FYP will implement a robust favorable policy to encourage more and more gas-fired power projects in China. The China market is projected to reach USD 0.62 billion by 2026, and the India market is projected to reach USD 0.26 billion by 2026.

Europe

The Europe market was valued at USD 2.04 billion in 2025, capturing 21.21% of global revenue, and is estimated to reach USD 2.09 billion in 2026. The governments in this region are highly focusing on replacing coal with either gas turbines or other renewable sources to reduce greenhouse gas emissions. The electricity demand in this region is growing exponentially, increasing the power generating capacity within the region. The shifting focus from coal to gas drives growth in the gas turbine market during the forecast period. The UK market is projected to reach USD 0.35 billion by 2026, while the Germany market is projected to reach USD 200.44 billion by 2026.

Rest of the World

Middle East & Africa contributed approximately USD 1.57 billion to the global market in 2025, accounting for 16.38% share, and is expected to reach USD 1.61 billion in 2026. The Latin America region captured 5.46% of the global market in 2025, generating USD 0.52 billion in revenue, and is projected to reach USD 0.54 billion in 2026.

List of Key Companies in Industrial Gas Turbine Market

Key Participants Are Concentrating On New Contracts

The market is highly fragmented with the presence of several large-scale key players across the world. These include a group of 4-5 key companies with a wider geographic presence. Several companies are increasingly participating in organic & inorganic developments to solidify their market position globally. The companies are looking for new contracts to increase their market share. For instance, in February 2021, GE announced that its six 34 MW LM250EXPRESS aero-derivative gas turbine will replace coal at the power plant in Colorado.

In December 2020, Anasoldo Energia announced a contract for the supply of an 80 MW AE64.3 gas turbine and the related maintenance for a value of around 50 million Euro from Synthos. This gas turbine will be installed in the Oswiecim plant and this turbine will replace the coal boiler after an operation.

LIST OF KEY COMPANIES PROFILED:

- GE (U.S.)

- Siemens (Germany)

- Mitsubishi Hitachi Power Systems, Ltd. (Japan)

- Ansaldo Energia (Italy)

- Solar Turbines (U.S.)

- Kawasaki Heavy Industries, Ltd. (Japan)

- Doosan Heavy Industries & Construction (South Korea)

- Bharat Heavy Electrical Limited (India)

- OPRA Turbines (Netherlands)

- Rolls-Royce (U.K.)

- Vericor Power Systems LLC (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- In October 2023: The HYFLEXPOWER consortium, led by Siemens Energy AG, has successfully commissioned a gas turbine using 100% renewable hydrogen. The demonstration project is located at packaging group Smurfit Kappa's paper mill in Saillat-sur-Vienne, France. It will produce hydrogen with an on-site 1 MW electrolyzer, store it in a nearly one-ton tank and use it to fuel a Siemens Energy SGT-400 industrial gas turbine.

- In September 2023: Kawasaki Heavy Industries, Ltd. announced the start of sales of the 1.8 MW class gas turbine cogeneration system GPB17MMX equipped with the world's first burner capable of 100% hydrogen dry combustion. Kawasaki overcame these shortcomings by successfully developing 100% hydrogen dry combustion engine that uses a proprietary combination of micro mixture combustion and afterburning.

- In April 2023: GE announced that it had entered into an agreement with UCED Group (UCED), the energy division of Czech investment group CREDITAS Group, which focuses mainly on long-term investments in conservative industries. GE supplies an LM6000 PC Sprint aeroderivative gas turbine for the expansion of the UCED Prostějov backup power plant, which will help stabilize the grid and support the growth of renewable energy sources in the Czech Republic.

- In April 2021: Siemens signed an agreement with an EPC Contractor TSK to supply F-class as a turbine to a new combined cycle power plant in Jacqueville, named Côte d'Ivoire. The power plant will have a capacity of 390 MW, and it is likely to begin operation in 2022

- August 2020: General Electric has secured an 858 MW CCGT power plant order to supply its 9HA.02 gas turbine and related equipment for the Zainskaya State District Power Plant. Of 858 MW, the upgrade project will include a 577 MW gas turbine plant.

REPORT COVERAGE

The global industrial gas turbine market report provides a detailed analysis of the market and focuses on key aspects such as leading companies and leading waste type, and services of the product. Besides this, the report offers insights into the market trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the advanced market over recent years.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) and Volume (MW) |

|

Segmentation

|

By Capacity

|

|

By Technology

|

|

|

By Cycle

|

|

|

By Sector

|

|

|

By Region

|

Frequently Asked Questions

As per a study by Fortune Business Insights, the global market size stood at USD 9.55 billion in 2025.

The global market is projected to grow at a CAGR of 2.67% over the forecast period.

The market size of North America stood at USD 2.94 billion in 2025.

The global market size is anticipated to reach USD 12.16 billion by 2034, growing at a substantial CAGR of 2.67% during the forecast period (2026-2034).

Based on sector, electric power utility is the leading segment in the market.

Growing concerns to reduces greenhouse emissions is the major factor driving the growth of the market, whereas volatility in natural gas prices may hinder the market growth

The major players in the market are GE, Siemens, Doosan Heavy Industries & Construction, and Bharat Heavy Electrical Limited.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us