Logging While Drilling (LWD) Market Size, Share & Industry Analysis, By Application (Onshore and Offshore {Shallow Water, Deepwater, and Ultra-Deepwater}), and Regional Forecast, 2026-2034

Logging While Drilling (LWD) Market Size and Future Outlook

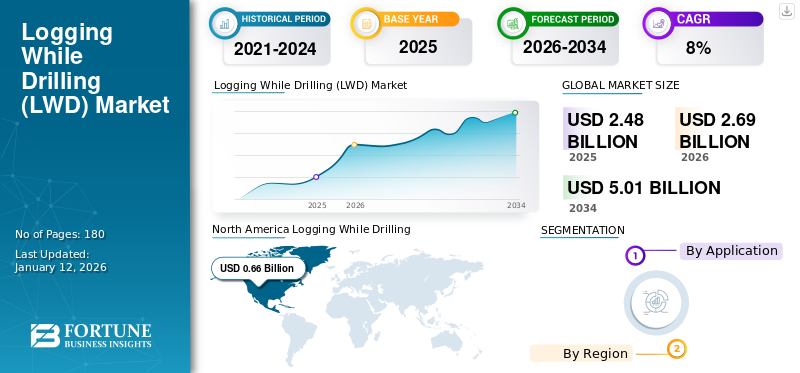

The global logging while drilling market size was valued at USD 2.48 billion in 2025 and is projected to grow from USD 2.69 billion in 2026 to USD 5.01 billion by 2034, registering a CAGR of 8.07% over the forecast period. North America dominated the logging while drilling market with a market share of 26.61% in 2025. The logging while drilling market in the U.S. is projected to grow significantly, reaching an estimated value of USD 971.65 million by 2032.

The Logging While Drilling (LWD) market is a critical segment of the oil and gas industry, providing real-time data acquisition during drilling operations. This technology enhances drilling efficiency, safety, and decision-making processes.

The LWD market is poised for significant growth, driven by technological advancements, increased drilling activities, and the need for real-time data acquisition. Moreover, strategic initiatives by key players and favorable regional developments are expected to propel the market further.

SLB is one of the major players in the market, leveraging advanced technology and extensive industry experience to enhance drilling efficiency and data acquisition. Its innovative solutions from LWD enable real-time geological insights, significantly improving decision-making and reducing operational risks in oil and gas discoveries.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Deepwater and Unconventional Drilling Activities to Meet Energy Demand Propels Market Growth

As conventional reserves become more depleted, exploration and production companies are increasingly turning to challenging environments such as deepwater and unconventional formations to meet global energy demands. These environments necessitate advanced monitoring and data acquisition techniques. Deepwater drilling, in particular, requires precise wellbore placement and a real-time understanding of formation properties to mitigate risks associated with wellbore instability, fluid influx, and complex geological structures.

Similarly, unconventional resources such as shale gas and tight oil require precise hydraulic fracturing operations guided by detailed geological and petrophysical information obtained from LWD tools. The complex nature of these formations demands real-time feedback, allowing operators to adjust drilling parameters and completion strategies on the fly, ultimately maximizing production efficiency.

According to recent data from the International Energy Agency (IEA), global deepwater oil production reached an estimated 7.9 million barrels per day in 2023. It represents close to 8% of the total global oil production, thus marking a substantial upswing from production levels in prior years. Moreover, the average cost of deepwater drilling has decreased by about 25% over the past decade due to technological innovations in the drilling sector.

Increasing Need for Real-time Data Acquisition in Drilling Sector to Drive Market Growth

Traditional wireline logging, conducted after drilling, is time-consuming and costly, especially if problems are encountered during drilling. LWD provides continuous, real-time data on formation resistivity, porosity, lithology, and other crucial parameters while the well is being drilled. This capability allows operators to make immediate decisions to optimize drilling trajectory, identify potential pay zones, and avoid costly mistakes.

LWD has the advantage of detecting and responding to unexpected geological conditions, such as fault zones or changes in formation pressure. The faster feedback loop improves drilling efficiency, enhances well safety, and reduces environmental risks. For instance, real-time pressure measurements from LWD tools can help prevent wellbore instability and fluid influx events, ensuring a safer and more controlled drilling operation.

For instance, in December 2024, SLB launched Neuro autonomous geosteering, an AI-driven technology that dynamically adjusts to subsurface conditions for more efficient drilling, increased well performance, and a reduced carbon footprint. Neuro geosteering uses AI to analyze real-time subsurface data and autonomously guide the drill bit through the reservoir's most productive zone, eliminating the need for geologists to interpret and adjust the drill bit manually.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

High Operational Costs Limits the Adoption of LWD in Drilling

The implementation of LWD involves significant capital expenditure associated with the purchase or rental of LWD tools. While the long-term benefits of LWD, such as improved drilling efficiency and enhanced hydrocarbon recovery, can outweigh the initial investment, the high upfront costs can be a barrier for smaller operators. The costs associated with hiring specialized personnel to operate and interpret LWD data also contribute to the overall operational costs. These factors, combined with the daily rental rates for LWD tools, can make LWD economically unfeasible for some drilling projects.

Despite the high costs, many operators recognize the value of LWD in optimizing drilling performance and enhancing hydrocarbon recovery. To mitigate the financial burden, operators are exploring alternative business models, such as shared services agreements and performance-based contracts. Furthermore, advancements in LWD technology are leading to more cost-effective tools and streamlined operations.

MARKET OPPORTUNITIES

Increased Onshore Drilling Activities Expected to Create Growth Opportunities for the Market

With the resurgence of shale oil and gas production in North America and other regions, the demand for LWD services in onshore projects is on the rise. LWD tools are increasingly being used to optimize horizontal well placements, improve hydraulic fracturing efficiency, and monitor production performance in unconventional reservoirs. The ability to acquire real-time data on formation properties and fracture characteristics allows operators to tailor their completion strategies to specific geological conditions, maximizing hydrocarbon recovery.

Furthermore, the use of LWD in onshore drilling is expanding beyond unconventional resources. LWD is also being used in conventional onshore drilling operations to improve wellbore stability, optimize drilling trajectories, and identify potential pay zones. The advancements in LWD technology, such as improved tool durability and reduced tool size, have made LWD more cost-effective and practical for a wider range of onshore drilling applications. This trend is expected to continue as operators seek to improve drilling efficiency, reduce costs, and enhance hydrocarbon recovery in both conventional and unconventional onshore reservoirs.

According to the International Energy Agency (IEA), the total number of onshore drilling rigs is expected to reach a count of approx. 4,617 in 2028, where countries including China and India will see an increase, whereas countries such as the U.S. and Russia may witness a decline.

MARKET CHALLENGES

Technical Complexities Demanding Expertise Poses a Challenge for the LWD Market

Operating LWD tools in challenging environments, such as deepwater or highly deviated wells, presents technical complexities that require specialized expertise. The harsh conditions in these environments, including high pressures, high temperatures, and corrosive fluids, can impact the performance and reliability of LWD tools. Data interpretation in complex geological settings, such as fractured reservoirs or faulted formations, also requires specialized knowledge and experience. The need for skilled personnel to operate and interpret LWD data can be a limiting factor, especially in regions where access to technical expertise is limited.

To overcome these challenges, LWD service companies are investing in R&D to improve the durability and reliability of LWD tools in harsh environments. They are also developing advanced data processing and interpretation techniques to address the complexities of subsurface geology. Furthermore, training programs and knowledge-sharing initiatives are being implemented to enhance the expertise of LWD personnel. By addressing these technical challenges and ensuring the availability of skilled personnel, the LWD industry can continue to expand its capabilities and applications in even the most demanding drilling environments.

LOGGING WHILE DRILLING (LWD) MARKET TRENDS

Technological Advancements such as Enhanced Data Transmission is the Latest Trend

LWD is essential for efficient drilling, with enhanced data transmission and downhole automation driving its evolution. Improved data rates enable real-time analysis of high-resolution images and complex sensor data, allowing engineers to quickly adapt to subsurface changes, optimize trajectory, and mitigate drilling risks like borehole instability. This speed enhances geosteering, maximizing reservoir contact and production.

Downhole automation integrates processing power within LWD tools, enabling real-time adjustments to drilling parameters based on sensor feedback. This autonomy boosts safety by automatically responding to issues such as pressure spikes and frees engineers to focus on geological analysis and reservoir characterization. This combination optimizes well placement, reduces risks, and enhances reservoir development for more productive drilling operations.

For instance, in November 2024, researchers from Western countries collectively developed a deep convolutional network-based algorithm called Azimuthal Image Super-Resoltion (AzSR). This new technology reconstructs high-resolution borehole images from noisy, low-resolution data, significantly improving the circumferential resolution of LWD azimuthal imaging.

IMPACT OF COVID-19

The COVID-19 pandemic significantly impacted the Logging While Drilling (LWD) market by disrupting global supply chains, leading to delays in equipment delivery and maintenance. Lockdowns and travel restrictions hampered the mobility of technical personnel crucial for LWD operations, slowing down exploration and production activities worldwide. Lower oil prices, triggered by decreased demand during the pandemic, forced many oil and gas companies to reduce capital expenditure and postpone drilling projects, directly affecting the demand for LWD services and equipment and creating challenges for the Logging While Drilling (LWD) market growth of the market.

SEGMENTATION ANALYSIS

By Application

Onshore LWD Segment Dominates Market Due to Lower Operational Costs and Faster Deployment Times

Based on application, the market is segmented into onshore and offshore.

By segmentation, the Onshore segment emerged as the largest sub-segment with a market size of USD 1.93 billion in 2026, representing a 71.78% market share. It is due to several driving factors, which include lower operational costs, simpler logistics, faster deployment times, and a greater number of wells being drilled onshore, particularly horizontal wells in unconventional shale plays. The accessibility and scalability of onshore operations make LWD more economically viable and logistically manageable compared to the complexities and expenses associated with offshore deployments.

The development of Enhanced Oil Recovery (EOR) techniques for offshore reservoirs and the increasing demand for high-resolution data in complex geological settings are driving the growth of the offshore segment. Furthermore, advances in LWD tool technology, such as improved telemetry, higher data transmission rates, and more robust designs, are specifically tailored to the harsh conditions and demanding requirements of offshore drilling.

To know how our report can help streamline your business, Speak to Analyst

LOGGING WHILE DRILLING (LWD) MARKET REGIONAL OUTLOOK

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Logging While Drilling (LWD) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Optimizing Production in Mature Basins Helps North America Lead Global Market

North America contributed 26.61% to the global market in 2025, with a valuation of USD 0.66 billion, and is projected to reach USD 0.72 billion in 2026. North America leads the Logging While Drilling (LWD) market share, driven by the need to optimize production from mature shale plays and deepwater assets. Operators are leveraging LWD technology to target sweet spots precisely, monitor wellbore stability, meet the increasing demand in real time, and maximize hydrocarbon recovery. There is a growing demand for advanced LWD tools capable of handling complex geological formations and unconventional reservoirs. The push for automation and remote drilling operations is further fueling the adoption of LWD solutions in the region.

U.S.

Shale Efficiency Fuels LWD Growth in U.S.

The U.S. market size is likely to account for USD 0.58 billion in 2026. The U.S. remains a dominant force in the North American LWD market, influenced by the continued activity in shale basins such as the Permian and Eagle Ford. The focus is firmly on drilling efficiency, cost reduction, and minimizing environmental impact. LWD is crucial for navigating complex fault systems, optimizing hydraulic fracturing operations, and ensuring compliance with stringent environmental regulations. The advancement of rotary steerable systems with integrated LWD tools is a notable trend in the region.

Europe

Ongoing Exploration Activities in the North Sea Drive Demand for LWD in the Region

Europe accounted for USD 0.33 billion in 2025, representing 13.33% of the global market share, and is projected to reach USD 0.35 billion in 2026. Europe's LWD market is characterized by a focus on maintaining and optimizing production from aging oil and gas infrastructure in the North Sea. The emphasis is on maximizing recovery from existing fields through enhanced reservoir characterization and improved well placement. LWD is also playing a crucial role in decommissioning activities and geological carbon storage projects. Increased investment in advanced LWD tools capable of withstanding harsh environmental conditions is noticeable. The growing demand for environmentally friendly drilling practices favors the use of LWD for real-time monitoring and risk mitigation. The market value in U.K. is expected to be USD 0.02 billion in 2026.

On the other hand, Russia is projecting to hit USD 0.20 billion and Norway is likely to hold USD 0.06 billion in 2025.

Asia Pacific

Exploration of Unconventional Resources, and Increased Offshore Drilling Activities Leading to Increase in Demand

The Asia Pacific market was valued at USD 0.68 billion in 2025, capturing 27.61% of global revenue, and is estimated to reach USD 0.76 billion in 2026. Asia Pacific is experiencing significant growth in the LWD sector, primarily driven by increasing exploration and production activities in offshore regions such as Indonesia, Malaysia, and Australia. Countries in this region are exploring new energy reserves to meet the increasing demand for oil. Government initiatives promoting energy security and encouraging foreign investment in oil and gas exploration are further boosting the market.

For instance, in February 2024, the International Energy Agency (IEA) projected that India will be one of the largest drivers of global oil demand growth through 2030, accounting for over a third of the global increase. India's oil demand is expected to reach 6.6 million barrels per day in 2030, up from 5.5 million in 2023. To meet this rising domestic demand and reduce reliance on imports, India is anticipated to increase its drilling activities.

China

Strategic Focus on Domestic Energy Security Influencing the Market in the Region

The market in China is expected to hit USD 0.50 billion in 2026, whereas India is likely to acquire USD 0.08 billion and Indonesia is projected to reach USD 0.04 billion in 2025. China's LWD market is rapidly expanding due to the government's strategic focus on enhancing domestic energy security and reducing reliance on imports. The country is investing heavily in both onshore and offshore exploration and production, particularly in challenging reservoirs. LWD is becoming increasingly vital for optimizing well placement in complex geological structures and maximizing hydrocarbon recovery. For instance, in July 2024, China announced the formation of a new state entity that combines national oil producers and other state-owned companies to explore ultra-deep oil and gas reserves reaching depths up to 10,000 meters and develop methods for extracting challenging non-conventional resources. This initiative aligns with President Xi Jinping's call to enhance the country's energy security.

Latin America

Offshore Opportunities Drive Adoption for LWD in the Region

Latin America region is to be anticipated as the fourth-largest market with USD 0.36 billion in 2026. Latin America presents significant growth opportunities for the LWD market, driven by the exploration and development of vast offshore reserves, particularly in Brazil's pre-salt region. Deepwater drilling and complex geological formations necessitate the use of advanced LWD technologies for accurate well placement and reservoir understanding. Government policies encouraging foreign investment and promoting energy sector development underpin the market's growth. The region is witnessing the increasing deployment of LWD tools with advanced imaging capabilities for detailed reservoir analysis.

Middle East & Africa

Optimizing Production in Complex Reservoirs Driving Demand for LWD in MEA

The market in Middle East & Africa reached USD 0.47 billion in 2025, representing 19.00% of total market revenue, and is projected to reach USD 0.5 billion in 2026. The MEA region, with its abundant oil and gas reserves, is a significant market for LWD. The need to optimize production from complex reservoirs and maintain export levels drives the demand for advanced LWD technologies. Enhanced reservoir characterization and improved well placement are key priorities. The region also presents opportunities for LWD in unconventional resources and Enhanced Oil Recovery (EOR) projects. An increasing number of National Oil Companies (NOCs) are investing in LWD to improve drilling efficiency and maximize resource utilization. Saudi Arabia is likely to hit USD 0.08 billion in 2025.

Latin America

In 2025, the Latin America market stood at USD 0.33 billion, representing 13.45% of global demand, and is projected to grow to USD 0.36 billion in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Schlumberger, Halliburton, and Baker Hughes Continue to Dominate Market with Their Comprehensive Service Offerings

A mix of large, established players and smaller, specialized companies characterizes the LWD market. Schlumberger, Halliburton, and Baker Hughes are the major integrated oilfield service companies that hold a significant share of the market due to their extensive global presence and comprehensive service offerings. SLB offers a comprehensive range of LWD services and technologies, whereas Halliburton is known for its advanced drilling solutions, including the recent introduction of 3D reservoir mapping services. Similarly, other global players, such as Baker Hughes and Weatherford International Plc, offer innovative LWD solutions tailored to various drilling environments.

List of the Key Logging While Drilling (LWD) Players Profiled

- Schlumberger (U.S.)

- Halliburton (U.S.)

- Baker Hughes (U.S.)

- Weatherford (Switzerland)

- Scientific Drilling (U.S.)

- Nabors Industries (Bermuda)

- National Oilwell Varco (U.S.)

- Kambi Enterprises Inc. (Canada)

- National Energy Services Reunited Corp.(NESR) (U.S.)

- COSL - China Oilfield Services Limited (China)

- APS Technology Inc. (U.S.)

- Jindal Drilling & Industries Ltd (India)

- Cougar Drilling Solutions (Canada)

KEY INDUSTRY DEVELOPMENTS

- January 2025- SLB secured several major drilling contracts from Shell to support energy development in Shell's deep- and ultra-deepwater assets across regions such as the U.K. North Sea, Trinidad and Tobago, and the Gulf of Mexico. Over the next three years, SLB will combine its AI-enabled digital drilling capabilities with its expertise in ultra-deepwater environments to deliver consistent, cost-efficient wells.

- October 2022- Weatherford International plc secured a three-year lump-sum turnkey (LSTK) contract with Saudi Aramco to provide drilling and intervention services. Weatherford's Integrated Services and Projects (ISP) team will manage all operational aspects, utilizing its products and services to deliver 45 wells annually.

- September 2022- NESR secured a long-term contract in Saudi Arabia for directional drilling services, including DD, MWD, performance drilling, well engineering, and LWD, for up to four years. NESR also secured multiple directional drilling contracts exceeding USD 200 million across Saudi Arabia, Oman, and Kuwait. They deployed their integrated RoyaSteer Rotary Steerable System and RoyaStream Measurement-While-Drilling tool, which has already drilled over 70,000 feet in the Americas.

- June 2020- Baker Hughes launched its newest AutoTrak eXact Pro, which is a high-performance Rotary Steerable System (RSS) with Logging While Drilling (LWD) that delivers precise and efficient drilling for high build rates. It combines advanced directional drilling with LWD data to create a smooth wellbore precisely placed in the most productive zone while reducing costs. The system's well-path trajectory control helps to minimize tortuosity, torque, and drag. Additionally, its compatibility with Baker Hughes' suite of LWD services enables accurate formation evaluation and reservoir data acquisition for optimized geosteering.

- June 2019- Halliburton developed a groundbreaking 3D reservoir mapping technology for Logging While Drilling (LWD) that enables precise visualization of subsurface structures. This innovative capability allows operators to understand complex reservoir environments better, optimize well placement, and identify previously overlooked geological features such as faults, water zones, and local structural variations.

Investment Analysis and Opportunities

- Companies such as SLB have been investing in advanced LWD technologies to enhance drilling efficiency and data acquisition. Halliburton has focused on integrating LWD services with other drilling technologies, aiming to provide comprehensive solutions for complex drilling. These developments reflect the industry’s commitment to advancing LWD technologies and other ongoing investments by major companies to drive growth in this sector.

REPORT COVERAGE

The global Logging While Drilling (LWD) market report delivers a detailed insight into the market and focuses on key aspects, such as leading companies in Logging While Drilling (LWD). Besides, it offers insights into the market trends & technology and highlights key industry developments. In addition to the factors above, it encompasses several factors and challenges that contributed to the growth and downfall of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.07% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Application

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 2.69 billion in 2026.

The market is likely to grow at a CAGR of 8.07% during the forecast period.

Based on application, the onshore segment leads the market.

The market size of North America stood at USD 0.66 billion in 2025.

The rising deepwater and unconventional drilling activities and the increasing need for real-time data acquisition in the drilling sector are the key factors driving market growth.

Some of the top players in the market are Schlumberger, Halliburton, Baker Hughes, and others.

The global market size is expected to record a valuation of USD 5.01 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us