Lung Cancer Screening Market Size, Share & Industry Analysis, By Cancer Type (Non-small Cell Lung Cancer (NSCLC), and Small Cell Lung Cancer); By Diagnosis Type (Low Dose Spiral CT Scan, and Chest X-ray), By End-user (Hospitals & Clinics, and Diagnostic Centers), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

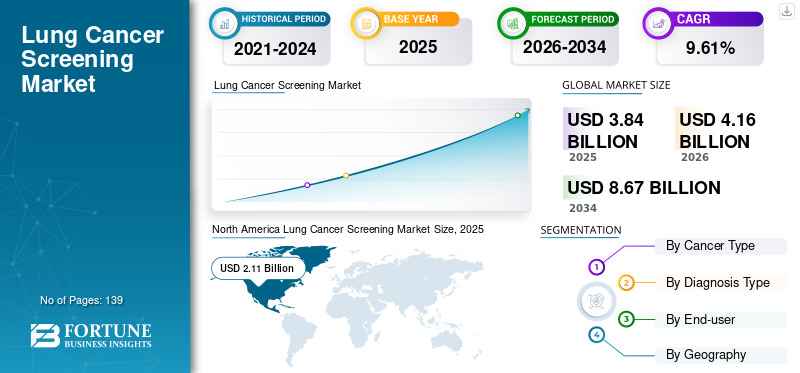

The global lung cancer screening market size was valued at USD 3.84 billion in 2025. The market is projected to grow from USD 4.16 billion in 2026 to USD 8.67 billion by 2034, exhibiting a CAGR of 9.61% during the forecast period. North America dominated the lung cancer screening market with a market share of 55.13% in 2025. Moreover, the U.S. lung cancer screening market size is projected to grow significantly, reaching an estimated value of USD 3.83 billion by 2032, driven by growing incidence of lung cancer and strong implementation of screening programs.

Lung cancer is one of the major types of cancer. It is caused by the uncontrolled growth of cells in the lungs. The occurrence of this cancer is closely related to the consumption of tobacco. In the majority of the cases, tobacco consumption is the primary reason for growing incidence of this type of cancer among general population.

The market is thriving owing to the surge in the incidence of this type of cancer due to the increasing smoking population, technological advancements in screening, and increasing government support for the early detection of cases. Moreover, strategic collaborations and updated recommendations and guidelines on screening are also likely to boost the market growth in the near future.

- For instance, in 2019, Genentech and Roche partnered up to explore biomarker screening for lung cancer treatment and detection. According to the companies, this genome-based testing could soon replace invasive tissue biopsies of the lungs.

The emergence of the pandemic initially impacted the screening programs globally, especially in the developed countries, owing to travel restrictions and lockdowns imposed by governments. This led to a decline in the number of people screened for this type of cancer. However, resumption of services during later stages of Q2 and in H2 2020 led to an increase in the number of patients screened. This increase compensated for the decline in patients during H1 2020. The market returned to the pre-pandemic growth trends in 2021 and 2022.

Download Free sample to learn more about this report.

Global Lung Cancer Screening Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 3.84 billion

- 2026 Market Size: USD 4.16 billion

- 2034 Forecast Market Size: USD 8.67 billion

- CAGR: 9.61% from 2026–2034

Market Share:

- North America dominated the lung cancer screening market with a 55.13% share in 2025, driven by the rising incidence of lung cancer, robust implementation of screening programs, and increasing adoption of advanced diagnostic technologies.

- By diagnosis type, the low-dose spiral CT scan segment is expected to retain its largest market share owing to favorable reimbursement policies, growing preference for low-dose CT over traditional X-rays, and increasing awareness of its mortality benefits.

Key Country Highlights:

- United States: The market is driven by the growing incidence of lung cancer, strong nationwide screening programs, and continuous technological advancements in diagnostic tools.

- Europe: The rising smoking population, well-established healthcare infrastructure, and supportive guidelines for early detection are fueling market growth.

- China: Government initiatives to implement screening frameworks, high tobacco consumption rates, and rapid adoption of AI-based diagnostics are propelling the market.

- Japan: Increasing focus on non-invasive diagnostic methods, advancements in nanoparticle-based screening technologies, and proactive healthcare policies are supporting market expansion.

Lung Cancer Screening Market Trends

Technological Advancements in Screening Techniques is a Prominent Trend

Key players in the medical devices industry are engaged in the development of advanced products. The screening and diagnosis sector is going through significant technological advancements to cater to the unmet needs of customers. Major players operating in the market along with research-based start-ups are seeking funding for research and clinical testing of screenings solutions for lung cancer. The growing incidence and prevalence is responsible for influencing market players to develop efficient and cost-effective diagnostic and screening tools.

- For Instance, in September 2020, researchers from the University of Otago conducted a research study on the diagnosis of lung cancer by the use of low-dose computerized tomography (LDCT). The study, which used scientific modeling to estimate the benefits of low cast LDCT screening, was published in BMJ Open medical journal.

Furthermore, in recent years, there have been notable technological advancements in lung cancer screening, primarily aimed at enhancing early detection with accuracy. Several innovations are changing the concept of cancer detection, including liquid biopsies, AI analyzers, and synthetic biopsies. To support these facts, several research institutes and industry players are developing advanced technologies for cancer detection at an early stage.

- For instance, in January 2024, the Massachusetts Institute of Technology developed a nanoparticle sensor that an inhaler can deliver for lung cancer diagnosis. This technology could replace current methods of diagnosis, specifically in low-income countries, where patients have limited access to CT scanners.

- Similarly, in October 2023, Delfi Diagnostics introduced its first liquid biopsy test for screening lung cancer.

In addition, the burden of radiologists is reduced, and the use of artificial intelligence-based lung cancer screening increases the sensitivity of cancer detection. These developments can improve outcomes for patients in the long run. Additionally, the strong growth of the medical devices industry is pushing existing leading players and domestic companies to expand their product portfolio. This is creating huge competition between market players to gain a competitive advantage over other players by introducing innovative solutions for segments, including lung screening.

Download Free sample to learn more about this report.

Lung Cancer Screening Market Growth Factors

Rising Prevalence of Lung Cancer and Surging Use of Cigarettes to Fuel Market Growth

The rising prevalence of cancer across the globe, increasing healthcare expenditure, and growing diagnosis present a large patient pool undergoing screening procedures. These are the factors responsible for the growth of the market in the near future.

- For instance, According to the American Society of Clinical Oncology (2020), lung cancer is the second most common cancer in women and men is estimated to affect over 235,000 adults in the U.S in the year 2020.

- Similarly, According to Globocan (Global Cancer Observatory), 64,804 new cases were diagnosed in Germany for the year 2020. The report also states that over 50,000 individuals died due to lung cancer in the country, making it the number one cause of death among cancer.

Also, due to the rising prevalence of lung cancer, several cancer institutes are launching campaigns to create awareness regarding early detection of lung cancer.

- For instance, in November 2023, the Barbara Ann Karmanos Cancer Institute, cancer centers, and various organizations nationwide celebrated November as lung cancer awareness month.

The burden of this diseases is rising globally, owing to various factors such as obesity, smoking, and lifestyle changes. Smoking and vaping are expected to increase the incidences of lung cancer among the general population. The surge in the incidence is anticipated to increase the demand for effective screening tests and solutions globally.

RESTRAINING FACTORS

High Cost of Tests to Restrict Market Growth

The cost of screening is higher, which makes it unaffordable for the general population, especially in the low-income category. Moreover, the lack of awareness regarding screening in developing economies is also likely to hamper market growth.

- For instance, the average cost of a CT scan in the United States is around USD 300, and the insurance providers offer coverage only to patients with a high risk of developing lung cancer.

In addition, the high costs associated with screening tests, such as Computed Tomography (CT), and accessibility issues, especially in rural areas, can hinder widespread adoption. Also, several individuals cannot access screening facilities for these tests.

- For instance, as per the data published by the National Center for Biotechnology Information in January 2020, CT screening for lung cancer resulted in a 60.0% increase in the mean total annual healthcare expenses, with a significant portion (52%) attributed to indirect costs.

Moreover, the scarcity of radiologists, radiology technicians, laboratory practitioners in developing and underdeveloped countries is anticipated to hamper the number of screening tests in the forecast period.

Hence, all the above factors restrict the adoption of lung screening solutions and are expected to hamper further the growth of the market in the forecast period.

Lung Cancer Screening Market Segmentation Analysis

By Cancer Type Analysis

Non-small Cell Lung Cancer (NSCLC) Segment to Hold Dominant Share Market

Based on cancer type, the global market is segmented into non-small cell lung cancer (NSCLC) and small cell lung cancer.

The non-small cell lung cancer (NSCLC) segment generated the highest revenue worldwide, driven by the increasing awareness about screening in developed and developing countries combined with the growing cases of NSCLC across the globe. As a result, the segment is expected to register an 8.2% CAGR during the forecast period. The non-small cell lung cancer (NSCLC) segment is projected to dominate the market with a share of 87.8% in 2026.

- For instance, according to the American Cancer Society, in general, about 84% of all lung cancers are non-small cell, and 13% are SCLC. Additionally, according to Cancer.Net, the five-year survival rate for NSCLC is 24%, compared to 6% for SCLC.

On the other hand, the small cell lung cancer segment held a significant market share during the forecast period. The surge in the increasing prevalence combined with the rising initiatives by government and non-profit organizations towards early screening and diagnosis, are expected to support the market growth.

To know how our report can help streamline your business, Speak to Analyst

By Diagnosis Type Analysis

Rising Adoption of Low Dose Spiral CT Scan to Help This Segment Dominate

Based on diagnosis type, the global market is segmented into low-dose spiral CT scans and chest x-ray.

The low dose spiral CT scan segment dominated the global market in 2023. The segment's dominance is due to the favorable reimbursement policies about cancer screening and the growing adoption of low dose spiral CT scan in the screening of this type of cancer. Additionally, increasing awareness about mortality benefits associated with low dose spiral CT scan screening. It is anticipated to influence the market growth during the forecast period. The low dose spiral CT scan segment is projected to dominate the market with a share of 93.94% in 2026.

- For instance, the National Cancer Institute’s Division of Cancer Prevention conducted the National Lung Screening Trial in 33 screening centers across the U.S. and 53,456 participants. The trial indicated that the screening with the use of low-dose CT reduced mortality by 20%.

- Similarly, trials such as Dutch-Belgian Randomized Lung Cancer Screening Trial (NELSON study) and U.K. Lung Cancer Screening (UKLS) were conducted in Europe, which revealed the benefits of low dose spiral CT scan compared to the traditional screening techniques such as chest X-ray.

On the other hand, the chest x-ray segment is anticipated to register lower CAGR during the forecast period due to customers' growing preference towards low dose spiral CT scans.

By End-user Analysis

Hospitals & Clinics Segment Held a Dominant Share in 2023

Based on end-user, the market is segmented into hospitals & clinics and diagnostic centers based on end-user. The hospitals & clinics held the largest market share during the forecast period due to the growing preference of patients towards hospitals for cancer screening, the rising number of hospitals in emerging countries, along the strong network of hospitals in the developed countries. Additionally, the growing awareness among general population, and the growing number of screening programs in healthcare facilities, are also likely to support the lung cancer screening market growth in the near future. The hospitals & clinics segment is expected to lead the market, contributing 70.79% globally in 2026.

Moreover, the diagnostic centers segment is anticipated to register a comparatively higher CAGR attributed to the growing collaborations between healthcare providers & payers with diagnostic facilities to offer screening programs and the rising number of diagnostic centers in developed countries worldwide.

REGIONAL INSIGHTS

North American

North America Lung Cancer Screening Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America contributed approximately USD 2.11 billion to the global market in 2025, accounting for 55.13% share, and is expected to reach USD 2.31 billion in 2026. The growing cases of lung cancer, strong implementation of screening programs, and rising adoption of technologically advanced solutions are some of the factors responsible for the dominance of North America in 2023. The U.S. market is estimated at USD 2.18 billion by 2026.

Europe

In 2025, the Europe market stood at USD 1.15 billion, representing 30.09% of global demand, and is projected to grow to USD 1.24 billion in 2026. Europe held the second-largest share in the global market. The presence of a well-established healthcare sector in European countries, the rising prevalence of this condition, with an increasing smoking population, and the accessibility to advanced screening devices in the healthcare facilities would aid growth. The UK market is projected to reach USD 0.2 billion by 2026, while the Germany market is expected to amount to USD 0.31 billion by 2026.

- According, to the European Society for Medical Oncology, 2020 data, it was reported that smoking was responsible for NSCLC in around 85% of the total patients.

Asia-pacific

The Asia Pacific region captured 9.83% of the global market in 2025, generating USD 0.38 billion in revenue, and is projected to reach USD 0.41 billion in 2026. On the other hand, Asia-pacific recorded a significant share in the market, and registered the highest CAGR during the forecast period. The high rate of smoking and tobacco consumption among the Asian population, increased initiatives by market players and government institutes to endorse the adoption of screening devices, and efforts of national government agencies to establish a strong framework for lung cancer screening are responsible for the market growth. The Japan market is forecast to reach USD 0.23 billion by 2026, the China market is anticipated to total USD 0.05 billion by 2026, and the India market is poised to attain USD 0.02 billion by 2026.

Latin America

Latin America recorded a market size of USD 0.16 billion in 2025, capturing 4.13% of the global market share, and is projected to reach USD 0.17 billion in 2026. Latin America is projected to hold a comparatively lower share in the global market due to the lack of awareness and limited access to screening. The strong focus on hospital and healthcare infrastructure development in the gulf region, rising government investments for the development of healthcare facilities, and entry of private players in the healthcare sector in the Middle East and Africa are set to provide favorable conditions for the growth of the market during the forecast period.

Middle East & Africa

In 2025, Middle East & Africa generated USD 0.03 billion, contributing 0.82% to global market revenue, and is projected to grow to USD 0.03 billion in 2026.

List of KeyCompanies in Lung Cancer Screening Market

Strong Distribution Network, Robust Portfolio, and New Product Launches to Help Key Players Lead

The global market is consolidated with key players, including General Electric Company, Koninklijke Philips N.V., Siemens Medical Solutions, and Canon Medical Systems Corporation. These players hold a significant share in the global lung cancer screening market. The dominance of these companies is attributed to the robust distribution network, strong product portfolio of screening devices, mergers and acquisitions, and introduction of new products in the market.

- In September 2020, Koninklijke Philips N.V. announced the introduction of Azurion Lung Edition, an advanced 3D imaging and navigation platform to accelerate the diagnosis and treatment of this type of cancer.

Moreover, other providers such as FUJIFILM Holdings Corporation, Volpara Solutions Limited, PenRad Technologies, Inc., Eon, Nuance Communications, Inc., are continuously engaged in strategic expansion initiatives to establish their footprints in emerging regions. A few players, such as Qiagen N.V., are also involved in developing companion diagnostic tests for lung cancer. These players are collaborating with leaders in the cancer diagnostics market to develop an efficient workflow from screening to diagnosis and personalized medicine for patients suffering from cancer.

LIST OF KEY COMPANIES PROFILED:

- Koninklijke Philips N.V. (Amsterdam, Netherlands)

- Siemens Healthineers AG (Munich, Germany)

- Canon Medical Systems Corporation (Tochigi, Japan)

- GE Healthcare (Chicago, U.S.)

- FUJIFILM Holdings Corporation (Tokyo, Japan)

- Medtronic (Dublin, Ireland)

- Nuance Communications, Inc. (Burlington, U.S.)

- Eon (Denver, U.S.)

- PenRad Technologies, Inc. (Minnesota, U.S.)

- Volpara Solutions Limited. (Wellington, New Zealand)

KEY INDUSTRY DEVELOPMENTS:

- January 2024 – Nova Scotia initiated a new cancer screening program for individuals at risk of developing lung cancer.

- December 2023 – Freenome, a biotechnology company, initiated a new clinical trial to receive U.S. FDA approval for its new lung cancer screening tool.

- May 2020 – Fujifilm announced that the company's Artificial Intelligence (AI)-based lung nodule detection technology had received approval for use in Japan

- November 2018 - Nuance Communications, Inc., in collaboration with Baptist Health South Florida’s Miami Cancer Institute (MCI), announced the establishment of a Lung Cancer Screening Program for conducting imaging tests for early diagnosis and effective treatment of the disease.

- March 2018 –Koninklijke Philips N.V. launched Ingenia Elition, an innovative 3.0T MRI solution, which enables a 50% reduction in scanning time and also furthermore helps in the betterment of the patient’s condition.

REPORT COVERAGE

The global lung cancer screening market research report provides a detailed analysis of the market. It focuses on key aspects such as competitive landscape, cancer type, and diagnosis type. Besides this, it offers insights into the market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.61% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Cancer Type

|

|

By Diagnosis Type

|

|

|

By End User

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 3.84 billion in 2025 and is projected to reach USD 8.67 billion by 2034.

In 2025, the market size in North America was USD 2.11 billion.

The market will exhibit strong growth at a CAGR of 9.61% during the forecast period (2026-2034).

By cancer type, the non-small cell lung cancer (NSCLC) segment will lead the market.

The rising prevalence and advancements in screening tests and partnerships & strategic collaborations among industry players are set to fuel growth.

General Electric Company, Koninklijke Philips N.V., Siemens Medical Solutions, and Canon Medical Systems Corporation are the top players in the market.

- 2021-2034

- 2025

- 2021-2024

- 139

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us