Machine Automation Controller Market Size, Share & Industry Analysis, By Controller Type (Programmable Logic Controllers, Programmable Automation Controllers, Distributed Control Systems, Industrial PC-Based Controllers (IPC / Soft PLC), Dedicated Motion Controllers, and CNC Controllers), By Machine Operation Type (Discrete Manufacturing, Batch Process, and Continuous Process), By End Use Industry (Automotive, Electronics & Semiconductors, Food & Beverage Processing, Chemicals & Petrochemicals, Oil & Gas, Pharmaceuticals & Biotechnology, & Others), and Regional Forecast, 2026-2034

Machine Automation Controller Market Size and Future Outlook

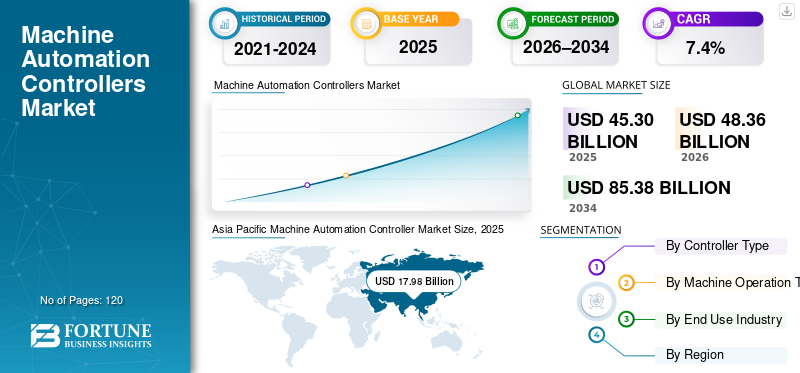

The global machine automation controller market size was valued at USD 45.30 billion in 2025. The market is projected to grow from USD 48.36 billion in 2026 to USD 85.38 billion by 2034, exhibiting a CAGR of 7.4% during the forecast period. Asia Pacific dominated the machine automation controller market with a market share of 39.69% in 2025.

Machine automation controllers are witnessing steady growth driven by rising industrial automation adoption, increasing deployment of smart factories, and the modernization of legacy manufacturing infrastructure. Factors such as growing demand for flexible and scalable automation systems, deeper integration with industrial IoT and edge platforms, and the shift toward Industry 4.0 architectures are accelerating market expansion. In parallel, wider use of predictive maintenance and analytics to improve productivity and efficiency, reduce operational cost, and strengthen product quality is increasing controller adoption across complex production processes, including motion control and distributed control system (DCS) environments.

- For instance, in March 2025, Siemens AG expanded its SIMATIC controller portfolio with enhanced edge-ready automation controllers designed to support real-time analytics, cybersecurity, and seamless integration with digital manufacturing platforms, addressing the evolving requirements of smart and connected factories.

Siemens AG, Rockwell Automation, Inc., Schneider Electric SE, ABB Ltd., and Emerson Electric Co. are among the key players holding a significant share of market. Strong technology expertise, comprehensive controller portfolios spanning PLC, PAC, DCS, IPC, and motion control, continuous investments in software and digital capabilities, and long-standing relationships with industrial end users and system integrators underpin the competitive strength of leading manufacturers.

Download Free sample to learn more about this report.

Machine Automation Controller Market Key Takeaways

- 2025 Market Size: USD 45.30 billion

- 2026 Market Size: USD 48.36 billion

- 2034 Forecast Market Size: USD 85.38 billion

- CAGR: 7.4% from 2026–2034

- Asia Pacific dominated the machine automation controller market with a 39.69% share in 2025.

- Distributed Control Systems (DCS) held the largest share of the market in 2025.

- Process-intensive industries represented a major application segment for automation controllers in 2025.

Asia Pacific

Asia Pacific was the largest and fastest-growing regional market, generating USD 17.98 billion in revenue in 2025.

North America

North America generated over USD 10.32 billion in revenue in 2025, supported by strong industrial automation adoption.

Europe

Europe witnessed steady growth driven by smart manufacturing, renewable energy investments, and industrial digitalization.

U.S.

Dominated the North American market and is expected to generate about USD 9.20 billion in revenue by 2026.

Japan

The market is projected to reach approximately USD 2.86 billion by 2026.

Read More

MACHINE AUTOMATION CONTROLLER MARKET TRENDS

Migration from Monolithic Control Architectures to Modular, Software-Defined Controller Platforms is a Market Trend

Industrial facilities are increasingly challenged by aging automation infrastructure, obsolete controller hardware, and unsupported control software. Many legacy Programmable logic controller (PLC) and distributed control system (DCS) installations are reaching end-of-life, driving demand for controller replacement and phased modernization, particularly in brownfield plants where uptime is critical. In response, manufacturers are introducing migration-friendly platforms with backward compatibility, extended lifecycle support, and simplified engineering tools to improve productivity and efficiency while reducing operational cost and safeguarding product quality across critical production processes.

- For example, in January 2025, Schneider Electric expanded its EcoStruxure automation controller portfolio with migration-focused controller solutions aimed at simplifying upgrades from legacy PLC and DCS systems while minimizing operational disruption.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Advanced Manufacturing and Process Industries Increasing Demand for High-Performance Automation Controllers

The expansion of advanced manufacturing and process industries is a key driver of the market. Automotive electrification, semiconductor fabrication, pharmaceuticals, chemicals, energy, and food processing are adopting increasingly complex, multi-stage operations that require precise, scalable process controlling and automation systems. Growing production volumes, stricter quality requirements, and real-time visibility needs are increasing controller density per facility, sustaining demand for high-performance PLCs, PACs, DCS, and IPC-based controllers.

- For instance, in October 2025, Rockwell Automation expanded its ControlLogix controller lineup to support higher processing capacity and expanded I/O scalability, enabling automotive and industrial manufacturers to manage increasingly complex production systems with improved performance and reliability.

MARKET RESTRAINTS

High Initial Investment and Integration Complexity Limiting Controller Adoption

Machine automation controllers often require substantial upfront investment due to advanced hardware specifications, bundled software licenses, and engineering configuration requirements. In addition to controller costs, integration with existing automation infrastructure, control networks, and legacy systems can increase overall implementation expenses. For small and mid-sized manufacturers, these high capital and integration costs can delay automation upgrades, particularly in cost-sensitive industries. As a result, adoption of advanced machine automation controllers may be constrained in facilities with limited automation budgets or low return-on-investment tolerance.

MARKET OPPORTUNITIES

Expanding Automation Adoption Beyond Large Enterprises Creating New Growth Avenues

Automation adoption is expanding beyond large enterprises into small and mid-sized manufacturing across food processing, packaging, building materials, water treatment, and specialty chemicals. These industries require cost-effective, scalable, and easy-to-deploy controllers to improve productivity and reduce labor dependency. In response, manufacturers are offering compact PLCs, entry-level PACs, and simplified software platforms, enabling automation adoption in applications previously considered uneconomical, particularly across emerging and decentralized manufacturing environments.

- For instance, in February 2024, Omron Corporation expanded its compact PLC portfolio with controllers designed for simplified programming and scalable automation, targeting small and mid-sized manufacturers seeking to automate discrete production processes.

MARKET CHALLENGES

High System Integration Complexity and Skill Requirements Increasing Deployment Time and Costs

System integration complexity remains a major challenge in the machine automation controller market, as controllers must interface seamlessly with diverse field devices, legacy I/O systems, industrial communication networks, and plant-level software platforms. Even minor configuration or protocol mismatches can result in production disruptions, longer commissioning cycles, and operational inefficiencies. Integrating new controllers into brownfield environments often requires extensive system re-engineering, validation, and testing to maintain process continuity. Additionally, advanced controllers demand specialized expertise in programming, networking, cybersecurity, and diagnostics. The shortage of skilled automation engineers and technicians, particularly in emerging and remote industrial regions, further increases deployment timelines and operational costs, limiting adoption in complex, multi-vendor automation environments.

Segmentation Analysis

By Controller Type

High-Value Process Automation Requirements Driving Dominance of Distributed Control Systems

Based on controller type, the market is segmented into Programmable Logic Controllers (PLC), Programmable Automation Controllers (PAC), Distributed Control Systems (DCS), Industrial PC-Based Controllers (IPC/Soft PLC), Dedicated Motion Controllers, and CNC Controllers.

Distributed Control Systems (DCS) account for the largest share of the global market due to their extensive deployment across high-value, process-intensive industries and their significantly higher average system value compared to other controller types, particularly where increasing production requires continuous, highly reliable control. DCS offer centralized control, high system availability, and advanced process optimization, making them well suited for large-scale, continuous industrial operations. These systems enable integrated control of complex processes, safety functions, and real-time diagnostics, which is critical in industries such as oil & gas, chemicals, power generation, and water & wastewater treatment to improve productivity efficiency and reduce downtime.

Programmable Logic Controllers (PLC) continue to witness widespread adoption owing to their flexibility, reliability, and suitability for discrete manufacturing environments. PLCs enable fast, deterministic control of machinery and production lines and are extensively used in automotive manufacturing, packaging, food & beverage processing, and material handling.

- For instance, in July 2025, Emerson Electric Co. expanded its DeltaV DCS platform with enhanced controller redundancy and advanced process analytics capabilities designed for large-scale process industry applications.

Industrial PC-Based Controllers (IPC/Soft PLC) are projected to witness strong machine automation controller market growth due to their advantages in computing performance, software flexibility, and seamless IT-OT integration.

To know how our report can help streamline your business, Speak to Analyst

By End Use Industry

Expansion of Process-Intensive and Discrete Manufacturing Industries Driving Broad Adoption of Automated Controllers

Based on end use industry, the market is segmented into automotive, electronics & semiconductors, food & beverage processing, chemicals & petrochemicals, oil & gas, pharmaceuticals & biotechnology, power generation & utilities, metals & mining, packaging, water & wastewater treatment, and others.

Process-intensive industries, particularly oil & gas, chemicals & petrochemicals, and power generation, account for a significant machine automation controller market share due to their high reliance on distributed control systems (DCS) and the higher value of controller installations per facility.

Machine automation controllers play a critical role in managing complex, continuous, and safety-critical operations across these industries. In sectors such as oil & gas and chemicals, controllers are essential for real-time process control, system redundancy, safety integration, and operational optimization. Increasing investments in refinery upgrades, petrochemical capacity expansion, power generation assets, and water infrastructure are driving sustained demand for high-performance automation controllers, particularly in large-scale and brownfield industrial facilities.

The automotive and electronics & semiconductors industries are expected to witness the fastest growth in demand for machine automation controllers. The transition toward electric vehicles, advanced driver-assistance systems (ADAS), and semiconductor fabrication expansion is increasing automation intensity across production lines. These industries require high-speed, flexible, and data-driven control systems, driving increased adoption of PLCs, PACs, IPC-based controllers, motion controllers, and CNC controllers. As investments in electrification, advanced manufacturing, and high-precision production continue to accelerate, controller demand from these end-use industries is expected to grow at a faster pace than the overall market.

Machine Automation Controller Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Machine Automation Controller Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific remains the fastest-growing market, generating revenue of USD 17.98 billion in 2025 globally. Within the region, China and Japan are projected to reach approximately USD 7.97 billion and USD 2.86 billion, respectively, by 2026. Market growth is driven by the strong concentration of manufacturing, electronics, automotive, and process industries across China, Japan, South Korea, Taiwan, and ASEAN countries. Rapid expansion of electronics manufacturing, automotive electrification, and industrial infrastructure is driving large-scale adoption of PLCs, DCS, IPC-based controllers, and motion control systems. In addition, government initiatives supporting industrial automation, smart manufacturing, and domestic production capabilities continue to reinforce Asia Pacific’s market leadership.

China Machine Automation Controller Market

China’s market is projected to remain the dominant in the Asia Pacific region, with 2026 revenues estimated at around USD 7.97 billion, representing roughly 16.5% of global machine automation controller sales.

Japan Machine Automation Controller Market

The Japan market value in 2026 is estimated at around USD 2.86 billion, accounting for roughly 5.9% of the global market.

India Machine Automation Controller Market

The India market value in 2026 is estimated at around USD 2.40 billion, accounting for roughly 5.0% of global machine automation controller revenues.

North America

The North America market accounted for over USD 10.32 billion revenue generated in 2025, supported by strong demand from advanced manufacturing and process industries. The region benefits from high automation maturity, a large installed base of industrial facilities, and the presence of leading automation OEMs and system integrators. Increasing investments in semiconductor manufacturing, automotive electrification, pharmaceuticals, food & beverage processing, and energy infrastructure are driving controller adoption. Additionally, stringent safety, quality, and reliability standards, along with ongoing brownfield modernization initiatives, continue to support sustained market growth across North America.

U.S. Machine Automation Controller Market

U.S. to dominate the North American market with a revenue of about USD 9.20 billion in 2026, driven by its large industrial base and high automation spending. Strong demand from process industries, automotive manufacturing, semiconductor fabrication, pharmaceuticals, and food & beverage processing supports market leadership. The presence of major automation OEMs, advanced R&D infrastructure, and early adoption of digital manufacturing technologies further strengthen controller demand. In addition, ongoing modernization of brownfield facilities and stringent safety, quality, and reliability requirements continue to accelerate adoption of advanced PLCs, PACs, DCS, and IPC-based controllers across the U.S.

Europe

The European market is supported by strong demand from automotive manufacturing, process industries, renewable energy, and advanced industrial machinery. The region’s emphasis on sustainable manufacturing, energy efficiency, and compliance with stringent safety and environmental regulations is driving adoption of advanced automation controllers across production facilities. Ongoing investments in smart factories, electrification, and industrial digitalization, particularly across countries such as Germany, France, Italy, and Netherlands, are further contributing to steady market growth.

U.K. Machine Automation Controller Market

The U.K. market value in 2026 is estimated at around USD 1.51 billion, representing roughly 3.1% of global machine automation controller revenues.

Germany Machine Automation Controller Market

Germany’s market is projected to reach approximately USD 2.70 billion in 2026, equivalent to around 5.6% of global machine automation controller sales.

Middle East & Africa

The Middle East & Africa market is driven by increasing industrialization and government-led initiatives aimed at diversifying economies beyond oil and gas. Rising investments in power generation, water & wastewater treatment, chemicals, mining, and manufacturing automation are supporting controller adoption across the region. In addition, infrastructure modernization, renewable energy projects, and the gradual digitization of industrial facilities are creating new opportunities for PLC, DCS, and industrial PC-based controller deployments, particularly across GCC countries and South Africa.

GCC Machine Automation Controller Market

The GCC market is projected to reach around USD 1.46 billion in 2026, representing roughly 3.0% of the global market.

South America

The South America market is supported by increasing investments in industrial automation, energy infrastructure, and manufacturing modernization, particularly in countries such as Brazil and Argentina. While large-scale advanced manufacturing remains limited, growing adoption of automation in oil & gas, mining, food & beverage processing, and utilities is driving steady controller demand.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on emerging and Innovative sectors to scale Machine Automation Controller

The market is moderately consolidated, characterized by the presence of a limited number of global automation vendors offering comprehensive controller portfolios spanning PLC, PAC, DCS, IPC-based, motion, and CNC control platforms. Key players such as Siemens AG, Rockwell Automation, Schneider Electric, ABB Ltd., Emerson Electric Co., and Honeywell International are focusing on continuous technology innovation to strengthen their market positions. Product development efforts are centered on improving controller performance, software integration, cybersecurity, and compatibility with digital manufacturing and industrial IoT ecosystems.

Leading manufacturers are also expanding their competitive advantage by enhancing software and lifecycle service offerings, including system migration tools, remote diagnostics, and long-term support programs. Strategic partnerships with system integrators, OEMs, and end users are being leveraged to increase deployment across both discrete and process industries. In addition, companies are pursuing selective acquisitions, regional expansion, and platform consolidation strategies to balance a large installed base with innovation-led growth, enabling them to address both brownfield modernization projects and next-generation automation requirements.

- For instance, Siemens AG announced a new generation of SIMATIC S7-1200 G2 programmable logic controllers as part of its automation portfolio expansion, offering improved motion control, enhanced performance, flexible machine safety features, and seamless integration with the TIA Portal engineering environment for modern industrial automation applications.

LIST OF KEY MACHINE AUTOMATION CONTROLLER COMPANIES PROFILED

- Siemens AG (Germany)

- Rockwell Automation, Inc. (U.S.)

- Schneider Electric SE (France)

- ABB Ltd. (Switzerland)

- Emerson Electric Co. (U.S.)

- Honeywell International Inc. (U.S.)

- Yokogawa Electric Corporation (Japan)

- Mitsubishi Electric Corporation (Japan)

- Omron Corporation (Japan)

- Bosch Rexroth AG (Germany)

KEY INDUSTRY DEVELOPMENTS

- April 2024: Siemens AG announced the launch of the SIMATIC S7-1200 G2 programmable logic controller at Hannover Messe, featuring higher processing performance, integrated motion control, enhanced machine safety functions, and improved engineering efficiency through the TIA Portal platform.

- February 2024: ABB Ltd. expanded its AC 800M controller portfolio with updates focused on improved redundancy, cybersecurity, and lifecycle support, targeting large-scale process industries such as oil & gas, chemicals, and power generation.

- March 2024: Rockwell Automation introduced enhancements to its ControlLogix 5580 controller platform, expanding scalability, real-time data handling, and integration with FactoryTalk software to support complex discrete and hybrid automation applications.

- November 2023: Schneider Electric announced upgrades to its EcoStruxure Foxboro DCS controllers, strengthening system reliability, advanced process control capabilities, and migration support for brownfield process automation environments.

- October 2023: Mitsubishi Electric expanded its iQ-R series automation controllers, introducing higher-speed processing and enhanced networking capabilities to address growing demand from automotive manufacturing, electronics production, and precision machinery applications.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.4% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Controller Type, Machine Operation Type, End Use Industry, and Region |

|

By Controller Type |

· Programmable Logic Controllers (PLC) · Programmable Automation Controllers (PAC) · Distributed Control Systems (DCS) · Industrial PC-Based Controllers (IPC / Soft PLC) · Dedicated Motion Controllers · CNC Controllers |

|

By Machine Operation Type |

· Discrete Manufacturing · Batch Process · Continuous Process |

|

By End Use Industry |

· Automotive · Electronics & Semiconductors · Food & Beverage Processing · Chemicals & Petrochemicals · Oil & Gas · Pharmaceuticals & Biotechnology · Power Generation & Utilities · Metals & Mining · Packaging · Water & Wastewater Treatment · Others |

|

By Region |

· North America (By Controller Type, By End Use Industry, and Country) o U.S. (By Controller Type) o Canada (By Controller Type) o Mexico (By Controller Type) · Europe (By Controller Type, By End Use Industry, and Country/Sub-region) o Germany (By Controller Type) o U.K. (By Controller Type) o France (By Controller Type) o Spain (By Controller Type) o Italy (By Controller Type) o BENELUX (By Controller Type) o Nordics (By Controller Type) o Russia (By Controller Type) o Rest of Europe · Asia Pacific (By Controller Type, By End Use Industry, and Country/Sub-region) o China (By Controller Type) o Japan (By Controller Type) o India (By Controller Type) o South Korea (By Controller Type) o ASEAN (By Controller Type) o Oceania (By Controller Type) o Rest of Asia Pacific · South America (By Controller Type, By End Use Industry, and Country/Sub-region) o Brazil (By Controller Type) o Argentina (By Controller Type) o Rest of South America · Middle East & Africa (By Controller Type, By End Use Industry, and Country/Sub-region) o GCC Countries (By Controller Type) o South Africa (By Controller Type) o North Africa (By Controller Type) o Israel (By Controller Type) o Rest of the Middle East & Africa (By Controller Type) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 45.30 billion in 2025 and is projected to reach USD 85.38 billion by 2034.

In 2025, the market value stood at USD 10.32 billion.

The market is expected to exhibit a CAGR of 7.4% during the forecast period.

By end use industry, the electronics & semiconductors are expected to dominate the market.

The rising process complexity and automation intensity across industries driving demand for advanced machine automation controllers.

Siemens AG, ABB Ltd., Emerson Electric Co., Schneider Electric SE, Rockwell Automation, Inc., and Mitsubishi Electric Corporation are the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us