Microgrid Market Size, Share & Industry Analysis, By Capacity (Less than 5 MW, 5 MW - 10 MW, 10 MW - 20 MW, 20 MW - 50 MW, and Above 50 MW), By Power Source (Diesel Generators, Natural Gas, Solar PV, CHP, and Others), By Application (Educational Institutes, Remote Areas, Military, Utility Distribution, Commercial & Industrial, and Others), and Regional Forecast, 2026-2034

Microgrid Market Size & Share

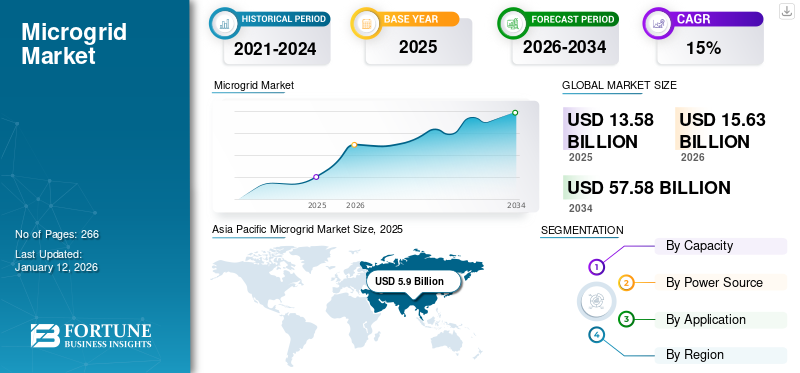

The global microgrid market size was valued at USD 13.58 billion in 2025 and is projected to grow from USD 15.63 billion in 2026 to USD 57.58 billion by 2034, exhibiting a CAGR of 17.70% during the forecast period. Asia Pacific dominated the global market, accounting for 31.35% market share in 2025.

Some of the major factors contributing to the growth of the market include increasing emphasis on decarbonization by end-users and governments, increasing use of microgrids for rural electrification, and the need for a growing supply of reliable and uninterrupted power. Additionally, increasing cyber-attacks on energy infrastructure and government initiatives to encourage the development will drive the industry's growth in the near future. The considerable impact of COVID-19 has been observed on the microgrid market growth due to supply chain disruption of raw materials and hindrance in activities due to social distancing norms. Due to several other factors, such as a lack of skilled professionals to operate the technology, along with the shutdown of manufacturing units around the world, the market had registered a decline in revenue.

The microgrid market is evolving into a strategic infrastructure segment supporting decentralized energy systems, resilience planning, and energy cost optimization. Adoption is accelerating as utilities, governments, and industrial operators respond to grid instability, electrification pressures, and renewable energy variability. Microgrids increasingly function as operational reliability assets rather than experimental distributed generation projects.

Microgrid market growth is primarily influenced by rising demand for localized energy independence across commercial, industrial, and critical infrastructure environments. Energy-intensive industries are prioritizing uninterrupted operations amid increasing outage frequency and transmission constraints. Simultaneously, renewable penetration is encouraging the deployment of flexible distributed energy management architectures capable of balancing intermittent generation sources. Investment momentum reflects structural transformation within electricity systems. Traditional centralized grids face modernization challenges, particularly in aging transmission networks. Microgrid deployment provides an alternative pathway enabling localized generation, storage integration, and intelligent load management.

Download Free sample to learn more about this report.

MICROGRID MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 13.58 billion

- 2026 Market Size: USD 15.63 billion

- 2034 Forecast Market Size: USD 57.58 billion

- CAGR: 17.70% from 2026–2034

- Asia Pacific dominated the global microgrid market with a 31.35% share in 2025.

- The less than 5 MW segment is projected to lead the market with a 38.00% share in 2026.

- The solar PV segment is projected to dominate the market with a 42.74% share in 2026.

Asia Pacific

Asia Pacific is projected to reach USD 6.84 billion in 2026, fueled by rising energy infrastructure spending, urbanization, and strong adoption of renewable-powered microgrids.

Europe

Europe is projected to reach USD 1.87 billion in 2026, supported by decarbonization targets, renewable energy integration, and growing investments in distributed energy systems.

North America

North America is projected to reach USD 4.90 billion in 2026, driven by grid modernization initiatives, resilience investments, and increasing deployment across commercial and industrial facilities.

U.S.

The market is expected to reach USD 3.38 billion by 2026.

Japan

The market forecast to reach USD 0.12 billion by 2026.

Read More

Associations, such as the Solar Energy Industries Association (SEIA), Advanced Energy Economy (AEE), Institute for Local Self-Reliance (ILSR), and Alliance for Rural Electrification (ARE), are taking steps to put microgrid projects back on rails. The clean energy and microgrid development proposals by these associations came at a time when nearly 100,000 advanced energy workers in the U.S. are unemployed. However, proposals to bolster distributed power are emerging as the U.S. government formulates a stimulus package in response to COVID-19-induced unemployment.

Key Market Dynamics

Microgrid Market Trends

Growing Requirement of Clean Energy is Promoting the Adoption of Smart Grid Initiatives

Future power grids must be flexible, accessible, reliable, and economically viable to achieve the goals of the smart grid initiative. With the rising initiatives in reducing greenhouse gas (GHG) emissions, research on various configurations or architectures of microgrid systems is gaining attention to control equipment malfunctioning. Additionally, growing environmental concerns and the adoption of renewable energy are creating a lucrative opportunity for the market.

This is happening alongside the increasing penetration of Renewable Energy Sources (RES) such as solar, wind, and other micro-sources. The growing demand for combined or hybrid integrated grid networks is expected to drive the global hybrid microgrid network. The majority of installations are united with CHP systems, including other technologies such as solar PV and energy storage. CHP is most often used to supply baseload power and thermal energy for continuous microgrids.

Although there is a substantial amount of deliberate deployments for CHP-based microgrids, solar presently leads the way for deliberate capacity of microgrids. Most operational grid systems are located in the Northeast, with a large portion also positioned in California, Hawaii, and Alaska.

Thunderstorms and unpredictable weather in the Northeastern states, similar to Massachusetts and New York, have raised the demand for better-quality resistance devices to power cuts that microgrids provide. California anticipates more installations as the PUC responds to the new microgrid bill. Microgrids in Hawaii and Alaska are usually mandatory for islands and remote communities or off-grid. On the West Coast, renewable energy policy has driven California microgrids.

Rising Government Initiative for Providing Reliable and Efficient Power Supply Spurs Product Demand

Microgrid technology is becoming increasingly cost-effective and provides a reliable and efficient power supply for various verticals. Governments have made investments in microgrids from different countries. For example, in June 2020, the Australian government supported 17 projects with over USD 19 million in grants under the first round of the Regional and Remote Communities Reliability Fund. In October 2019, the federal government launched Australia's USD 50 million funding program. Of this amount, USD 20 million in funding has been allocated for feasibility studies in the country. Such government initiatives are expected to provide growth opportunities for the market over the forecast period.

Download Free sample to learn more about this report.

Microgrid Market Drivers

Increasing Demand for Energy Resilience and Reliability to Drive Microgrid Market Growth

Microgrids offer enhanced energy resilience and reliability by incorporating the local energy generation, storage, and distribution capabilities. They can operate autonomously or in conjunction with the main grid, thereby providing backup power during grid outages or disruptions caused by natural disasters, extreme weather events, or infrastructure failures. The growing need for a reliable energy supply, particularly in regions prone to power outages or with unreliable grid infrastructure, is a significant driver of the global microgrid market. As businesses, communities, and big infrastructure sectors seek to mitigate the impact of power disruptions and ensure continuous operations, the demand for microgrids will increase. Additionally, the increasing frequency and severity of extreme weather events, coupled with aging grid infrastructure, will further accelerate the market’s growth.

Government Initiatives to Reduce Carbon Footprint and Offer Reliable Power Supply Will Promote the Utilization of Microgrids

The demand for energy storage systems is increasing due to the high demand for a constant and secure power supply globally. This is why governments are introducing various initiatives to lower the carbon footprint, which is likely to propel the demand for energy storage systems. Several other factors, such as extensive industrialization and the introduction of IoT in microgrid connectivity to manage and control distributed energy resources, have spurred the demand for the product. Utilities generally consider these systems as a primary block for a smart grid and focus on R&D as a severe focus area.

For instance, according to SmartGrid Consortium (NYS), the New York government has been implementing microgrids. Consequently, 20 projects were nominated from an extensive candidate list in New York. Detailed analysis of these projects is based on various parameters, including regulations, energy delivery, technology, and development.

Market Restraints

Monumental Installation and High Costs of Maintenance are Hindering the Market

The initial cost of these systems is significantly higher than that of conventional power grids, typically between 25% and 30%. The infrastructure costs include everything from deploying communication systems to installing smart meters and maintaining them. In addition, the installation of smart meters costs about 50% more than the installation of electricity meters. The Distributed Energy Resources (DERs) used in microgrids are also more expensive than those used in traditional power plants.

Building a new microgrid or transforming a current system into a hybrid system can cost around 10,000 or even hundreds of millions. The most expensive generation assets include batteries, solar photovoltaic collections, and combined heat and power systems. Additionally, a significant amount of capital is required for grid automation and control systems that can intelligently monitor and manage all components, controlling the microgrid power efficiently. These systems can store and convert energy and provide improved reliability and power quality over traditional grids, but their costs are enormous. This factor is limiting the growth of the market.

Market Opportunities

A significant opportunity exists in emerging economies experiencing rapid electricity demand growth, combined with grid infrastructure limitations. Microgrids provide scalable alternatives to large transmission expansion projects. Industrial decarbonization initiatives represent another major opportunity. Manufacturing facilities seeking emissions reduction targets increasingly adopt renewable-powered microgrids supported by storage systems.

Remote mining and energy extraction operations also present strong deployment potential. Fuel transportation costs often exceed localized generation investment over long operating periods. Urban resilience planning introduces additional opportunities across metropolitan regions vulnerable to grid disruption. Municipal governments are evaluating microgrids for hospitals, emergency services, and transportation hubs.

Integration with hydrogen production and advanced storage technologies may further expand future applications. Flexible energy ecosystems capable of supporting multiple energy vectors could redefine deployment economics.

Microgrid Market Segmentation Analysis

By Capacity Analysis

Less Energy Cost of above 50 MW will Amplify Market Growth

Based on capacity, the market is segmented into less than 5 MW, 5 MW -10 MW, 10 MW- 20 MW, 20 MW -50 MW, and above 50 MW.

Less than 5 MW

Microgrids below five megawatts represent the most widely deployed capacity category in terms of project volume. These systems primarily serve localized facilities such as educational campuses, healthcare institutions, commercial buildings, and remote communities.

Deployment decisions in this segment are typically driven by resilience requirements rather than large-scale energy trading opportunities. Solar photovoltaic integration combined with battery storage is common due to declining equipment costs. Installation timelines remain shorter compared with larger systems, improving investment feasibility.

This segment contributes substantially to overall microgrid market growth because distributed energy adoption continues expanding across small institutional users. Financing models such as energy service agreements also support adoption among organizations seeking reduced capital exposure.

5 MW – 10 MW

The five to ten megawatt segment represents a transition toward commercial and industrial optimization deployments. Manufacturing facilities, logistics hubs, and medium-scale industrial parks commonly adopt systems within this range. Energy cost management becomes a stronger investment driver at this capacity level. Operators utilize microgrids to balance grid electricity purchases with onsite generation. Integration of combined heat and power systems frequently improves efficiency outcomes.

This segment contributes meaningfully to microgrid market size expansion due to repeatable deployment models across industrial clusters. Project developers increasingly standardize system architecture, reducing engineering complexity. Growth prospects remain strong as industrial electrification accelerates globally.

10 MW – 20 MW

Microgrids within this capacity range typically support large industrial operations or regional infrastructure assets. Mining operations, refineries, and large commercial campuses often require sustained high-load reliability. Hybrid configurations combining renewable energy, natural gas generation, and storage systems dominate deployments. Operators seek fuel diversification while maintaining operational continuity.

Capital investment requirements increase substantially at this level, yet long-term operational savings often justify deployment. These projects significantly influence microgrid market share due to higher contract value and extended lifecycle service agreements. Grid support functionality also becomes more prominent, allowing operators to provide demand response or ancillary services.

20 MW – 50 MW

Systems between twenty and fifty megawatts increasingly resemble localized utility-scale networks. Utility distribution support and community resilience projects frequently operate within this capacity band. Governments and utilities deploy such systems to stabilize vulnerable grid regions or integrate renewable energy penetration. Advanced control systems coordinate multiple generation assets across distribution nodes.

Although deployment volumes remain lower, revenue contribution is substantial. Infrastructure modernization initiatives strongly influence adoption across this segment. The segment represents a strategic expansion area within the microgrid market as utilities explore decentralized grid architecture.

Above 50 MW

The above 50 MW segment holds a dominant share of the market due to the low electrification rate of grid connectivity compared to the other capacity segments. The components used in every system are the same irrespective of their capacity, for example, a solar panel, a charge controller, and a battery, which can absorb more charge and result in the long run. The less than 5 MW segment is projected to dominate the market, with a 38% share in 2026.

Microgrids exceeding fifty megawatts serve large metropolitan districts, defense infrastructure, or remote industrial energy ecosystems. These deployments often function as semi-independent power networks. Investment decisions involve complex regulatory coordination and long development timelines. However, operational benefits include energy independence and large-scale renewable integration capability. This segment contributes disproportionately to the total microgrid market size despite limited installation numbers. Growth potential remains tied to national resilience planning and large infrastructure modernization programs.

By Power Source Analysis

Rising Application of CHP Bolstered the CHP Segment

By power source, the market is segregated into diesel generators, natural gas, solar PV, CHP, and others.

Diesel Generators

Diesel generation historically formed the foundation of early microgrid deployments, particularly in remote environments. Reliability and rapid dispatch capability remain key advantages. Remote mining operations and isolated communities continue relying on diesel-supported systems where fuel logistics are established. However, environmental concerns and fuel price volatility are gradually reducing long-term dependence. Diesel increasingly functions as backup capacity rather than primary generation. Hybridization with renewable energy sources is becoming standard practice.

Natural Gas

Natural gas holds a significant market share due to its versatility and abundant characteristics, which power microgrids with relatively less impact on the environment. Natural gas is available in adequate quantities and adaptable to many different functions, propelling the demand for CHP in the global market.

Natural gas-powered microgrids are gaining adoption in regions with reliable gas infrastructure. Gas turbines and reciprocating engines provide stable baseload generation while supporting emissions reduction relative to diesel systems. Industrial users favor natural gas due to operational efficiency and predictable fuel pricing. Combined heat utilization further enhances economic performance. This segment contributes significantly to microgrid market growth within urban and industrial environments where pipeline access exists. Gas-based systems often act as transitional solutions supporting gradual renewable integration.

Solar Photovoltaic (Solar PV)

Solar photovoltaic generation represents the fastest-growing power source within the microgrid market. Declining installation costs and supportive policy frameworks continue accelerating adoption. Solar integration improves long-term operating economics while supporting decarbonization goals. Energy storage systems compensate for intermittency challenges. Commercial campuses, utilities, and remote communities increasingly deploy solar-driven microgrids. The segment plays a central role in shaping future microgrid market trends toward low-carbon energy systems.

Combined Heat and Power (CHP)

The CHP segment holds a dominant market share as it saves total energy costs for consumers. The solar PV segment is projected to dominate the market with a share of 42.74% in 2026. Combined heat and power systems provide dual energy output through electricity generation and thermal recovery. Industrial facilities with continuous heating requirements benefit significantly from CHP integration. Efficiency advantages improve return on investment compared with standalone generation systems. Hospitals and manufacturing plants frequently deploy CHP-supported microgrids.

The energy storage system in a microgrid can operate in control mode, but only a single power source is permitted when it is remotely operated. In other words, if links with the grid are cut off, the grid can work under a single source when diesel generators are the most suitable option.

By Application Analysis

High Utilization in Educational Institutions Will Lead to the Domination of the Segment

Based on application, the market is segmented into educational institutes, remote areas, military, utility distribution, commercial & industrial, and others.

Educational Institutes

A paradigm shift toward adopting safe and reliable power generation units and the continued adoption of innovative technologies to ensure a resilient power supply against grid instability surge the demand for microgrids in educational institutions. University campuses increasingly deploy microgrids to ensure uninterrupted operations and manage energy expenditure. Research facilities require a stable electricity supply for sensitive equipment. Campus-scale renewable integration also supports sustainability objectives. Educational institutions often act as early adopters, demonstrating operational feasibility.

To know how our report can help streamline your business, Speak to Analyst

Remote Areas

Remote area electrification remains one of the strongest adoption drivers globally. Extending centralized grid infrastructure often proves economically impractical. Microgrids enable localized power generation, improving energy access reliability. Renewable integration reduces fuel transportation costs over time. This application contributes significantly to microgrid market growth across developing economies.

Military

Military installations prioritize operational resilience and energy independence. Microgrids enable mission continuity during external grid disruption. Defense modernization programs increasingly incorporate renewable-powered systems combined with advanced control platforms. Security considerations strongly influence system architecture. Military deployments frequently adopt advanced technologies that are later commercialized across civilian markets.

Utility Distribution

Utilities increasingly deploy microgrids to stabilize distribution networks and manage renewable variability. Community microgrids improve outage recovery capability. These systems support peak demand management while enhancing grid flexibility. Utility participation significantly expands the overall microgrid market size potential.

Commercial & Industrial

Commercial and industrial industries comprise significant heating and cooling demands with good cost reduction opportunities and the potential to reduce emissions. The commercial & industrial segment will account for 27.96% market share in 2026. They are usually large areas and may double up as emergency shelters during extreme events such as cyclones, forest fires, and earthquakes, which is expected to grow the market for commercial & industrial rapidly.

Commercial and industrial users represent the largest revenue-generating application segment. Manufacturing facilities require continuous power availability to avoid production losses. Energy optimization and carbon reduction commitments further accelerate adoption. Integration with electric vehicle infrastructure strengthens long-term demand outlook.

REGIONAL INSIGHTS

The global market has been analyzed across major regions, including North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia-Pacific Microgrid Market Analysis

Asia Pacific Microgrid Market Size, 2025

To get more information on the regional analysis of this market, Download Free sample

Currently, most of the world's microgrids are in the Asia Pacific, with most of the capacity being in the People's Republic of China and Japan. There is a high demand for robust and continuous network connectivity to provide seamless support to large enterprises, facilitating the outlook for the Asia Pacific microgrid market share. The regional government's initiatives have driven the construction of innovative yet dependable telecom infrastructure, which is impacting the market.

Asia-Pacific represents the fastest-expanding microgrid market, driven by electrification demand and infrastructure gaps across developing economies. Rapid industrialization and remote energy access requirements support deployment growth. Governments increasingly promote renewable-powered distributed systems to reduce transmission investment pressure. Market expansion remains particularly strong across island economies and industrial growth corridors.

International Data Corporation (IDC) states that spending on Asia Pacific accounted for USD 5.9 billion in 2025, representing 43.41% of the global market share, and is projected to reach USD 6.84 billion in 2026. Asia Pacific spending has also increased, reaching USD 1,566 billion in 2021, up by 1.6% yearly. The Japan market is forecast to reach USD 0.12 billion by 2026, the China market is set to reach USD 4.01 billion by 2026, and the India market is likely to reach USD 0.99 billion by 2026.

Japan Microgrid Market

Japan’s microgrid market development reflects long-term resilience planning following historical grid disruption events. Energy security and disaster preparedness strongly influence deployment strategy. Advanced battery storage integration supports renewable balancing capability. Commercial districts and municipal infrastructure increasingly deploy microgrids to strengthen operational continuity while supporting national decarbonization objectives.

China Microgrid Market

China demonstrates strong microgrid market growth supported by industrial expansion and renewable energy integration policies. Smart energy infrastructure investment enables deployment across industrial parks and remote regions. Government-backed distributed energy initiatives accelerate adoption. Microgrids increasingly support grid stability objectives while enabling localized renewable utilization across manufacturing-intensive provinces.

Europe Microgrid Market Analysis

Europe contributed 12.06% to the global market in 2025, with a valuation of USD 1.64 billion, and is projected to reach USD 1.87 billion in 2026. In the European market, microgrids play a vital role in the electricity ecosystem of the future, with decarbonization, digitalization, decentralization, and non-wires solutions being its key attributes. It helps transform industries from all sectors, increasing production capacities; this increases the dependence on the continuous power supply to keep the system running. A few seconds of a power outage can interrupt industrial processes and cause significant economic loss. Microgrids also relate to the transportation sector, which consumes over 30% of primary energy. Electrifying only a small percentage of this would translate to significant capacity in the coming years.

Europe demonstrates steady microgrid market growth supported by decarbonization targets and renewable penetration expansion. Energy security concerns following supply disruptions have accelerated localized generation investment. Industrial operators increasingly deploy hybrid systems integrating storage and combined heat and power assets. Regulatory alignment supporting distributed generation continues influencing microgrid market share expansion across several European economies.

Germany Microgrid Market

The German market is anticipated to reach USD 0.39 billion by 2026. Germany remains a key contributor within the European microgrid market due to strong renewable integration policies and industrial electrification initiatives. Manufacturing facilities prioritize energy optimization and emissions reduction through localized energy systems. Advanced grid digitalization supports operational coordination between distributed assets. Adoption remains closely linked to industrial sustainability commitments and long-term energy transition planning.

United Kingdom Microgrid Market

The UK market is estimated to reach USD 0.28 billion by 2026. The United Kingdom microgrid market is expanding through commercial infrastructure resilience planning and distributed renewable deployment. Universities, healthcare facilities, and urban energy districts increasingly evaluate microgrid integration. Energy cost volatility continues to influence adoption decisions. Government-supported net-zero initiatives and flexible grid programs support the gradual expansion of localized energy systems across commercial environments.

North America Microgrid Market Analysis

The North America market generated USD 4.26 billion in 2025, representing 31.35% of the global market landscape, and is expected to reach USD 4.9 billion in 2026. North America is likely to maintain its significant hold in the global market due to the availability of reliable, stable, and affordable power. Rising attention to technological advancement by key manufacturers, scaling up existing infrastructure with advanced systems, and increasing demand for a stable and secure global power supply are some factors contributing to the market growth. The U.S. market is expected to reach USD 3.38 billion by 2026.

North America represents a leading microgrid market driven by grid resilience investment, renewable integration mandates, and aging transmission infrastructure modernization. Commercial and industrial users increasingly deploy microgrids to mitigate outage risks and energy price volatility. Utility participation and defense infrastructure programs further support adoption. Strong digital energy management capability continues to strengthen regional microgrid market growth across institutional and industrial applications.

United States Microgrid Market

The United States dominates the regional microgrid market size due to advanced distributed energy deployment and supportive state-level resilience policies. Military installations, university campuses, and industrial facilities remain primary adopters. Increasing wildfires and extreme weather disruptions accelerate investment decisions. Utility-led community microgrids are expanding as grid modernization strategies increasingly prioritize decentralized energy reliability solutions.

Latin America Microgrid Market Analysis

Latin America contributed approximately USD 0.49 billion to the global market in 2025, accounting for 3.68% share, and is expected to reach USD 0.56 billion in 2026. The Latin American market has gained momentum in recent years. Advanced technologies such as IoT, Big Data, and AI are increasingly deployed in the region. The introduction of the cloud is also accelerating rapidly in this area. In addition to setting up microgrids and local power generation, the operators are procuring redundant power infrastructure.

Latin America shows increasing microgrid market potential driven by remote electrification needs and mining sector demand. Energy reliability challenges encourage localized generation investment. Renewable hybrid systems reduce diesel dependency across isolated operations. Adoption remains project-driven but demonstrates steady growth as infrastructure modernization and private energy investment increase.

Middle East & Africa Microgrid Market Analysis

In 2025, Middle East & Africa held 9.50% of the global market, reaching a valuation of USD 1.29 billion, and is projected to grow to USD 1.46 billion in 2026. In the Middle East & Africa, increasing investment in the commercial sector with several ambitious government visions in the region, such as Saudi Vision 2030, Turkey Vision 2023, and South Africa Vision 2030, would drive significant development activities to advance power demand backup solutions.

The Middle East and Africa microgrid market is supported by remote energy demand, industrial operations, and expanding renewable deployment. Mining, oil infrastructure, and off-grid communities drive adoption. Solar-powered hybrid systems increasingly replace fuel-dependent generation. Growth depends on financing availability and continued investment in distributed energy infrastructure development.

Microgrid Industry Competitive Landscape

ABB and Eaton Lead with Wide Product Profile and Established Brand Name to Capture Market

The market has several players focused on providing microgrids. Market players are developing various technological advancements, with the adoption of AI platforms and leveraging solar energy and battery storage to support the facility. The majority of market players focus on these technologies. A growing commodity and energy market will create profitable opportunities for mining companies as the mining industry expands.

The microgrid industry demonstrates a mixed competitive structure combining large energy technology providers, power system integrators, and specialized distributed energy developers. Competitive differentiation increasingly depends on system integration capability rather than individual equipment supply.

Leading participants focus on delivering end-to-end solutions combining generation assets, energy storage, digital control platforms, and lifecycle services. Integrated deployment capability reduces operational complexity for customers managing distributed energy environments.

Technology providers increasingly expand through partnerships with utilities and infrastructure developers. Collaboration enables access to large-scale resilience and community microgrid projects. Digital platform capability has become a major differentiator. Intelligent controllers capable of predictive load balancing and automated dispatch improve operational economics. Vendors investing in analytics-driven optimization strengthen competitive positioning.

Emerging developers are focusing on energy-as-a-service delivery models. These approaches reduce customer capital investment while securing long-term operational contracts. Financing innovation, therefore, plays a growing role in market share expansion. Regional engineering firms also maintain influence in project execution, particularly within emerging economies where regulatory navigation and infrastructure customization remain essential.

LIST OF TOP MICROGRID COMPANIES:

- ABB (Switzerland)

- Eaton Corp (Ireland)

- Honeywell (U.S.)

- Schneider Electric (France)

- Siemens (Germany)

- Spirae, LLC (Colorado)

- Power Analytics Corporation (U.S.)

- Toshiba Corporation (Japan)

- GE (U.S.)

- HOMER Energy (Colorado)

- S&C Electric (Chicago)

- Caterpillar (U.S.)

KEY INDUSTRY DEVELOPMENTS:

January 2024: Schneider Electric expanded integrated microgrid solution deployment platforms – to strengthen distributed energy optimization capability across commercial infrastructure – incorporating advanced energy management software and battery storage coordination systems.

- April 2024: Siemens Energy launched modular microgrid architecture programs – to accelerate deployment across industrial facilities – utilizing digital grid control systems and hybrid renewable integration technologies.

- August 2024: Hitachi Energy partnered with regional utilities to deploy community microgrids – to enhance grid resilience and renewable balancing capability – integrating advanced automation platforms and distributed energy resource management systems.

- February 2025: ABB introduced next-generation microgrid control solutions – to improve real-time operational optimization – deploying artificial intelligence-enabled forecasting and adaptive load management capabilities.

- May 2025: Eaton expanded energy-as-a-service microgrid projects across commercial sectors – to reduce customer capital barriers – combining distributed generation integration, storage systems, and long-term operational performance monitoring platforms.

- March 2023: ABB entered a strategic partnership with Direct Energy Partners (DEP), a start-up using digital technology to accelerate the adoption of Direct Current (DC) microgrids. The partnership involved a minority investment in Direct Energy Partners through ABB’s venture capital unit, ABB Technology Ventures (ATV).

- September 2023: The Canadian government announced plans to invest more than CAD 175 million (USD 130 million) in 12 clean energy projects across Alberta, including a microgrid that aims to provide a reliable electricity supply to the Montana First Nation. The funding would come from Canada’s Smart Renewables and Electrification Pathways Program (SREPs), which will invest up to CAD 4.5 billion (USD 3.31 billion) in smart renewable energy and grid modernization projects by 2035.

- May 2022: Caterpillar purchased Tangent Energy Solutions, an energy-as-a-service (EaaS) company that enables Caterpillar to work directly with utilities and energy providers to deliver distributed energy resources. Tangent Energy's proprietary software solution is a DERMS platform that monitors, manages, and monetizes onsite energy assets, including natural gas and renewable energy generation, storage, and microgrids.

REPORT COVERAGE

The research report highlights regional and country-level analysis to understand the user better. Furthermore, the reports provide insights into the latest market trends and market analysis of technologies deployed rapidly globally. It further highlights some drivers and restraints, helping the reader gain in-depth knowledge about the industry.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 17.70% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Capacity

|

|

By Power Source

|

|

|

By Application

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 13.58 billion in 2025 and is projected to reach USD 57.58 billion by 2034.

In 2025, the Asia Pacific market was valued at USD 5.9 billion.

The market is likely to record a CAGR of 17.70%, exhibiting substantial growth during the forecast period of 2026-2034.

In the forecast period, educational institutes segment is expected to maintain its position as the dominant application segment.

ABB and Eaton Corp. are some of the key players operating across the industry.

Asia Pacific dominated the market in terms of share 43.41% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 266

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us