Offshore Pipeline Market Size, Share & Industry Analysis, By Pipeline Type (Export Pipelines, Trunklines / Transmission Pipelines, and Field Development & Tie-back Pipelines), By Water Depth (Shallow Water, Deepwater, and Ultra-Deepwater), By Application (Natural Gas Pipelines, Oil Pipelines, and CO₂ / Multi-Purpose Pipelines), and Regional Forecast, 2026-2034

Offshore Pipeline Market Size and Future Outlook

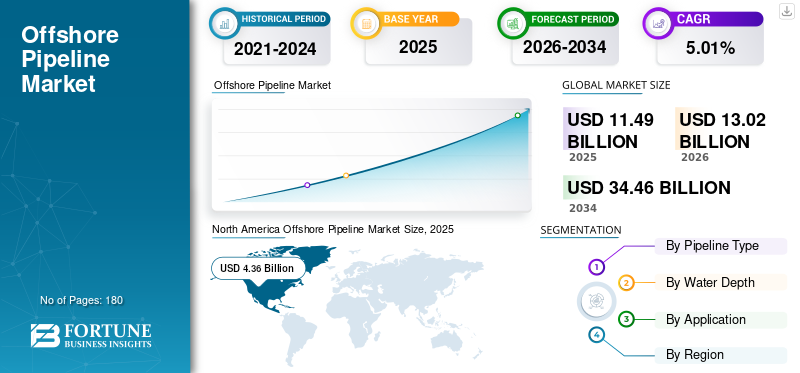

The global offshore pipeline market size was valued at USD 13.21 billion in 2025. The market is expected to grow from USD 13.92 billion in 2026 to USD 20.58 billion by 2034, exhibiting a CAGR of 5.01% during the forecast period. North America dominated the offshore pipeline market with a market share of 33.00% in 2025.

Moreover, the North America region holds the largest market share in terms of revenue, primarily driven by extensive infrastructure in the Gulf of Mexico and significant projects in Canada.

Offshore pipelines are critical infrastructure systems laid on or beneath the seabed to transport oil, gas, and refined products from offshore production facilities (platforms, wells) to onshore processing terminals, or between offshore facilities. As shallow-water reserves deplete, operators are exploring deeper, more complex environments (e.g., Brazil's pre-salt, the Gulf of Mexico, West Africa), requiring advanced, high-strength pipeline technologies.

- In January 2026, Leaders from nine North Sea countries, industry, and grid operators signed an “Investment Pact for the North Seas,” aiming to mobilize around USD 1.3 trillion in offshore wind investments and build 15 GW of offshore wind per year from 2031 to 2040, reinforcing Europe’s clean‑energy and industrial ambitions.

Subsea 7 is a dominant global leader in the offshore pipeline and energy services market, specializing in seabed-to-surface engineering, pipeline construction, and installation (SURF). Saipem and McDermott are also major players in the global market, recognized for their engineering expertise and extensive project portfolios. Other top, highly competitive players include Allseas Group, TechnipFMC, China Petroleum Pipeline Engineering, and L&T Hydrocarbon Engineering.

Download Free sample to learn more about this report.

Offshore Pipeline Market KEY TAKEAWAYS

- 2025 Market Size: USD 13.21 billion

- 2026 Market Size: USD 13.92 billion

- 2034 Forecast Market Size: USD 20.58 billion

- CAGR: 5.01% from 2026–2034

- North America dominated the offshore pipeline market with a 33.00% share in 2025

- The field development & tie-back pipelines segment accounted for the largest market share of 50.4% in 2025

- The shallow water segment accounted for the largest market share of 45.0% in 2025

Asia Pacific

Asia Pacific reached USD 2.60 billion in 2025, driven by LNG projects and offshore gas development.

North America

North America reached USD 4.36 billion in 2025, supported by Gulf of Mexico offshore projects.

Europe

Europe reached USD 2.87 billion in 2025, driven by North Sea oil and gas activities.

U.S.

U.S. reached USD 3.77 billion in 2025, fueled by Gulf of Mexico exploration and production.

Japan

Japan is driven by growing demand for LNG imports and offshore energy infrastructure.

Read More

OFFSHORE PIPELINE MARKET TRENDS

Shift toward Deepwater and Ultra-Deepwater Developments is Shaping Market Trends

The market is undergoing a profound shift toward deepwater and ultra-deepwater developments, driven by the pursuit of untapped hydrocarbon reserves in challenging frontiers. Operators increasingly favor these high-pressure, extended-reach pipelines to connect remote subsea wells to onshore facilities, enhancing production efficiency from complex reservoirs.

Advancements in materials, welding techniques, and installation vessels enable safer, more resilient infrastructure capable of withstanding extreme depths and corrosive environments. This evolution not only expands access to vast resources but also spurs innovations in flexible risers and insulated flowlines, positioning deepwater systems as pivotal to future energy supply security.

MARKET DYNAMICS

MARKET DRIVERS:

Sustained Offshore Oil & Gas Exploration and Production Is Driving Market Growth

Sustained offshore oil & gas exploration and production is a primary driver of the market. Relentless demand for energy fuels ongoing ventures into mature basins and emerging frontiers, necessitating expansive pipeline networks to transport crude, oil & gas, and refined products from subsea wells to processing hubs. This persistent activity underscores the critical role of pipelines in linking remote production sites to global markets, while innovations in subsea tiebacks and multiphase flowlines optimize recovery from aging fields.

- For instance, India’s offshore frontier is shifting from early‑stage hope to tangible momentum, with policy reforms, reduced “no‑go” zones, and renewed exploration campaigns in deepwater basins including Andaman and Mahanadi driving fresh interest from national and international operators in the country’s offshore hydrocarbon potential.

As exploration intensifies, pipeline infrastructure evolves to support higher volumes, reinforcing its foundational status in the offshore energy ecosystem.

MARKET RESTRAINTS:

High Capital and Installation Costs to Restrain Market Growth

High capital and installation costs serve as a significant restraint on offshore pipeline market growth, deterring investment amid volatile energy prices and economic uncertainties. These projects demand massive upfront expenditures for specialized vessels, advanced materials, and deepwater engineering, compounded by lengthy permitting processes and complex supply chains. Installation in harsh marine environments amplifies risks, requiring robust, corrosion-resistant alloys and precise subsea welding, which inflate budgets. For smaller operators or emerging markets, these barriers limit project feasibility, favoring alternatives including floating production units. Consequently, cost pressures slow expansion, prioritizing only high-margin ventures with proven reserves.

MARKET OPPORTUNITIES:

Carbon Capture and Storage (CCS) Infrastructure Development is Expected to Create Lucrative Opportunities

Carbon Capture and Storage (CCS) infrastructure development presents lucrative opportunities for the market, repurposing existing networks and spurring new builds to transport captured CO2 emissions to subsea repositories. As global decarbonization mandates intensify, pipelines become essential for shuttling compressed carbon from industrial emitters and power plants to depleted reservoirs beneath the seabed, leveraging proven offshore expertise. This shift revitalizes idle assets, integrates with hydrogen transport, and aligns with net-zero goals, attracting investments from energy majors. Enhanced designs for CO2 compatibility, including corrosion mitigation, position pipelines as a cornerstone of the sustainable energy transition.

MARKET CHALLENGES:

Technical Complexity in Harsh Offshore Conditions May Create Challenges for Market Growth

Technical complexity in operations poses notable challenges for the market, demanding costly adaptations to handle supercritical CO2's corrosive and erosive properties. Existing hydrocarbon pipelines require extensive retrofits with advanced linings and monitoring systems, while new designs must endure high pressures and phase changes in deepwater settings.

Regulatory hurdles, uncertain viability of storage sites, and integration with fragmented capture networks complicate scalability. Supply chain constraints on specialized materials further escalate costs, test operators' technical prowess, and delay commercialization amid competing energy transition priorities.

Download Free sample to learn more about this report.

Segmentation Analysis

By Pipeline Type

Field development and tie-back pipelines are Dominant Due to their Prominence in Subsea Connections

Based on pipeline type segmentation, the market is classified into export pipelines, trunklines/transmission pipelines, and field development & tie-back pipelines.

In 2025, field development & tie-back pipelines segment dominated and accounted for 50.4% of the offshore pipeline market share, serving as the backbone for connecting subsea wells to central platforms and enabling efficient resource extraction from mature fields.

Meanwhile, export pipelines emerge as the fastest-growing segment with CAGR of 6.08% over the forecast period, driven by surging demand to transport hydrocarbons from offshore hubs directly to onshore markets, supporting expanded oil and gas production amid global energy needs.

By Water Depth

Shallow Water Segment Dominated Due to Established Infrastructure and Cost Effectiveness

Based on water depth segmentation, the market is classified into shallow water, deepwater, and ultra-deepwater.

In 2025, shallow water segment dominated the market, with a 45.0% share, leveraging established infrastructure, lower installation complexity, and proximity to shorelines for cost-effective hydrocarbon transport from prolific basins.

- In February 2026, Allseas started working on a shallow‑water offshore pipeline project off Taiwan, installing a new 36‑inch line that will run parallel to the existing Yongan–Tongxiao route to strengthen natural gas transmission capacity and support Taiwan’s energy‑transition goals.

Meanwhile, deepwater segment emerges as the fastest-growing segment with CAGR of 5.71% over the projected period, fueled by technological advances in subsea engineering and vessels that unlock vast reserves in challenging depths, driving investments despite higher risks.

By Application

Natural Gas Pipelines Segment Emerged as a Growing Segment Owing to Extensive Networks

Based on application segmentation, the market is classified into natural gas pipelines, oil pipelines, and CO₂/multi-purpose pipelines.

In 2025, natural gas pipelines dominated the market, with a 53.91% share, underpinning global energy supply through extensive networks that deliver clean-burning fuel from remote subsea fields to processing terminals and grids.

Meanwhile, CO₂/multi-purpose pipelines are the fastest-growing segment with CAGR of 7.54% during the forecast period, propelled by carbon capture initiatives and versatile designs that accommodate hydrogen or blended flows for the energy transition.

To know how our report can help streamline your business, Speak to Analyst

Offshore Pipeline Market Regional Outlook

By geography, the Market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Offshore Pipeline Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America reached USD 4.36 billion in 2025, securing its position as the largest market, powered by the Gulf of Mexico's prolific reserves, mature infrastructure, and advanced subsea technologies that sustain high-volume hydrocarbon exports.

U.S. Offshore Pipeline Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was valued at around USD 3.77 billion in 2025, accounting for roughly 28.57% of the global market size. The U.S. market thrives in the Gulf of Mexico, with extensive networks that transport oil and gas from deepwater fields to refineries, driven by technological innovation and steady exploration.

Europe

Europe is projected to grow at 4.32% over the coming years, the second-highest among all regions, and reached a valuation of USD 2.87 billion in 2025. Europe’s market is anchored in the North Sea and Mediterranean, where mature fields and new deepwater discoveries drive demand for subsea infrastructure to transport oil and gas to onshore terminals and regional markets.

Germany Offshore Pipeline Market

The German market in 2025 was valued to be around USD 0.19 billion. It is projected to reach USD 0.20 billion by 2026, representing approximately 1.45% of the global revenues.

Asia Pacific

Asia Pacific held the third largest share in 2025, valued at USD 2.60 billion, and is also set to hold a leading share in 2026, with USD 2.78 billion, propelled by Southeast Asian gas giants and Australia's expansive LNG projects, which demand robust subsea networks to export vast reserves to fuel Asia Pacific’s market demand.

China Offshore Pipeline Market

The China market in 2025 was valued to be around USD 1.03 billion, accounting for roughly 7.79% of the global market revenues. China’s market is expanding rapidly, driven by rising domestic energy demand and a strategic push to secure offshore oil and gas reserves in the South China and East China Seas. The country is investing heavily in pipeline infrastructure to connect offshore fields to onshore processing hubs, enhance energy security, and reduce import dependence, supported by technological upgrades and government‑backed exploration programs.

India Offshore Pipeline Market

India’s market is projected to be one of the largest globally, with 2025 revenues valued at around USD 0.28 billion, representing approximately 2.10% of the global market.

Indonesia Offshore Pipeline Market

The Indonesian market in 2025 is estimated to be around USD 0.36 billion, accounting for approximately 2.95% of global revenues.

Latin America

Latin America is expected to witness moderate growth in this market during the forecast period. The Latin America market reached a valuation of USD 1.48 billion in 2025. Latin America’s market is led by Brazil’s prolific pre‑salt fields and Gulf of Mexico operations, where extensive subsea networks transport oil and gas to onshore refineries and export terminals, supporting regional energy supply and export growth.

Brazil Offshore Pipeline Market

Brazil's market reached a valuation of approximately USD 0.99 billion in 2025, accounting very minor share of the global market.

Middle East & Africa

The Middle East & Africa region is expected to witness significant growth in this market during the forecast period. The Middle East & Africa market reached a valuation of USD 1.89 billion in 2025. The market growth is driven by major oil and gas fields in the Persian Gulf, Red Sea, and West Africa, where subsea pipelines connect offshore platforms to onshore processing and export hubs, supporting regional energy exports and domestic supply.

GCC Offshore Pipeline Market

The GCC market reached a valuation of approximately USD 1.08 billion in 2025, accounting for around 8.14% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players:

Vendors are Actively Expanding their Market Share through Business Expansion and Technological Advancements

The market has a fragmented structure, comprising prominent players such as Subsea 7, Saipem, McDermott International, and others. For instance, in December 2025, Allseas announced plans to install a 500‑km deepwater pipeline system for Enbridge in the U.S. Gulf of Mexico, comprising four export lines that will transport crude oil and natural gas from new developments to existing offshore hubs, boosting long‑term export capacity and strengthening subsea infrastructure in the region. Such developments are expected to fuel Market growth over the forecast period.

LIST OF KEY OFFSHORE PIPELINE COMPANIES PROFILED IN REPORT:

- Subsea 7 (U.K.)

- Saipem (Italy)

- McDermott International (U.S.)

- TechnipFMC (U.K.)

- Allseas (Switzerland)

- Boskalis (Netherlands)

- Van Oord (Netherlands)

- Heerema Marine Contractors (Netherlands)

- Petrofac (U.K.)

- Larsen & Toubro (L&T) (India)

- Sapura Energy (Malaysia)

- China Offshore Oil Engineering Co., LTD. (COOEC) (China)

- Hyundai Heavy Industries (South Korea)

- National Petroleum Construction Company (NPCC) (UAE)

- John Wood Group (U.K.)

KEY INDUSTRY DEVELOPMENTS:

- February 2026: Kuwait Petroleum Corporation (KPC) announced plans to invite international oil companies to help develop recently discovered offshore oil and gas fields, aiming to raise national production capacity to 4 million barrels per day by 2035. The move targets three offshore fields found in 2025 and marks a shift toward greater foreign participation in Kuwait’s upstream sector.

- January 2026: The Panama Canal Authority launched bidding for a 76‑km LPG pipeline and two new container‑port terminals on the Atlantic and Pacific coasts, aiming to expand fuel transport and transshipment capacity. The projects are part of a broader strategy to reinforce Panama’s role as a global intermodal hub amid shifting regional trade and energy‑transit dynamics.

- December 2025: Petrobras announced plans to launch a tender in 2026 for a key gas pipeline tied to two FPSOs planned for the Sergipe–Alagoas deepwater basin offshore Brazil. The pipeline is intended to export gas produced by the SEAP FPSOs, supporting the Sergipe Águas Profundas project, with operations targeted to start around 2030.

- September 2025: Norway’s Offshore Directorate approved Equinor’s tie‑in of the Troll B platform to the Kvitebjørn gas export pipeline, enabling gas export to Kollsnes from Q4 2025. The move reduces expected gas‑production decline, adds export flexibility via both Troll A and Kvitebjørn lines, and repurposes former gas‑injection infrastructure, with investments of about USD 116.5 million.

- August 2025: JERA and bp launched JERA Nex bp, a 50:50 global offshore wind joint venture headquartered in London. The company will own, develop, and operate offshore wind assets with a net potential capacity of about 13 GW, including around 1 GW of operating projects and a significant development pipeline across Europe and Asia.

REPORT COVERAGE

The global offshore pipeline market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market report also encompasses a detailed competitive landscape with information on the market share and profiles of key market players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.01% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Pipeline Type, Water Depth, Application, and Region |

|

|

By Pipeline Type

By Water Depth

By Application

|

|

By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 13.21 billion in 2025 and is projected to reach USD 20.58 billion by 2034.

In 2025, the North America’s market value stood at USD 4.36 billion.

The market is expected to exhibit a CAGR of 5.01% during the forecast period of 2026-2034.

The natural gas pipelines sector led the application segment.

Sustained offshore oil & gas exploration and production is driving the market growth.

Subsea 7, Saipem, McDermott International, and others are some of the prominent players in the Market.

North America held the largest market share in 2025.

Increasing global energy consumption, particularly in developing nations, is driving the need for new offshore Exploration and Production Activities (E&P). As nearshore reserves mature, companies are moving toward deep-water and ultra-deep-water, necessitating robust subsea infrastructure.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us