Solar Panel Recycling Market Size, Share & Industry Analysis, By Type (Monocrystalline, Polycrystalline, and Thin Films), By Process (Thermal, Mechanical, Chemical, and Others), By Application (Residential, Commercial, Industrial, Utility, and Others) and Regional Forecast, 2026-2034

Solar Panel Recycling Market Size

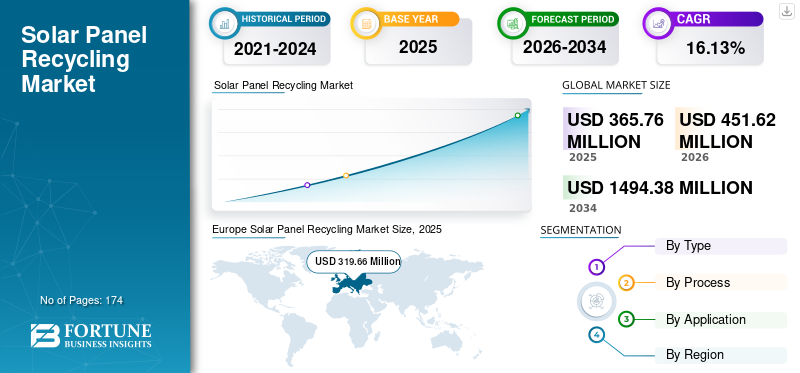

The global solar panel recycling market size was valued at USD 365.76 million in 2025. The market is projected to grow from USD 451.62 million in 2026 and expected to reach USD 1,494.38 million by 2034, exhibiting a CAGR of 16.13% during the forecast period. Europe dominated the global solar panel recycling market with a share of 87.39% in 2025.

Solar panel recycling involves recovering valuable materials from decommissioned or defective solar panels for reuse in manufacturing new panels. In the solar energy industry, sustainability means fulfilling current energy needs while ensuring that future generations can also meet their energy demands. For this, comprehending the life cycle of a solar panel is crucial so as to evaluate its environmental impacts, as each stage, from production to disposal, can impact sustainability.

The combination of rising solar waste, sustainability initiatives, regulatory frameworks, economic incentives, and technological advancements is driving the growth of the market. As the industry matures, effective recycling will play a crucial role in ensuring a sustainable future for solar energy production while mitigating environmental impacts.

Top companies such as First Solar, Veolia, PV Cycle, Echo Environmental and others are shaping the market. They are scaling collection and take back programs, investing in high recovery processes, and building regional recycle capacity to handle the coming wave of demand for end-of-life solar panel modules. Their combined efforts are accelerating the shift toward a more circular supply chain, reducing landfill dependency and improving material recovery economics.

Download Free sample to learn more about this report.

Solar Panel Recycling Market Trends

Shift From Bulk Recycling To High Value Recovery Is One Of The Major Market Trends

The shift from “bulk recycling” to “high value recovery” in solar panel recycling is about moving beyond simple removing frames/junction boxes, and crushing panels mainly for glass and aluminum towards processes that also recover higher value, lower mass materials especially silver and silicon in high purity. Research and industry reviews highlight that decapsulation/ delamination is the critical enabling step, because it frees the cell stack so that downstream thermal/chemical routes can selectively extract metals and upgrade material streams. This matters because high purity recovery of silver and silicon is widely cited as important for improving the economics and circularity of PV recycling, and several emerging industrial players explicitly position their plants as secondary raw materials. Modern PV recycling approaches to combine physical, thermal and chemical treatment and explicitly target recovery of valuable materials.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Rising Government Policies and Projects to Unlock New Potentials for the Industry

With the global shift toward renewable energy sources, the solar energy industry has experienced exceptional growth in recent years. As solar panels reach the end of their lifespan, proper disposal and recycling become crucial to minimize the environmental impact and maximize resource efficiency. This remarkable expansion has been driven by supportive government policies and growing environmental awareness. Consequently, the installation of solar energy systems has surged, leading to a corresponding increase in the number of decommissioned solar panels that require proper disposal or recycling.

Government policies and projects are propelling the growth of the market. These initiatives help reduce the cost of solar energy, increase adoption, and drive technological advancements. Governments offer financial support to reduce the initial cost of solar panel installations for both residential and commercial users. Subsidies, tax breaks, and grants for recycling initiatives can help make the process more economically viable.

Market Restraints

Lack of Regulation Associated with Recycling and Fluctuating Costs Restricts Market Growth

As solar power generation technology becomes more widespread, the number of solar panels in use increases. However, the typical lifespan of a solar panel is around 20 years, after which proper disposal and recycling become critical. Currently, there are no federal regulations in the U.S. mandating Photovoltaic (P.V.) recycling. According to the U.S. National Renewable Energy Laboratory, less than 10% of decommissioned panels in the country are recycled.

In the European Union, where P.V. recycling is mandated by legislation, many recycling facilities focus on recovering valuable materials such as silicon silver and aluminum, which constitute over 80% of a silicon panel's weight.

According to the U.S. Department of Energy, recycling one solar panel costs USD 15 to USD 45 per solar panel, significantly more than the USD 1 to USD 5 per solar panel cost of sending it to a landfill. This economic challenge sometimes makes landfill disposal more attractive, discouraging the development and implementation of recycling programs. While the U.S. lacks federal laws mandating the recycling of solar panels, the government is taking initiatives and implementing laws related to environmental concerns. This lack of federal regulations makes it difficult to incentivize manufacturers and businesses to dispose of modules properly. Despite lacking federal intervention, some U.S. states have policies that classify panels as hazardous materials, ensuring specific components are disposed of with minimal environmental impact.

Market Opportunities

Emergence of Specialized Recycling Pathways for Next-Generation PV technologies

Next generation PV technologies including perovskite and perovskite silicon tandem modules introduce new materials stacks, thinner active layers, and in some cases lead-based compounds, which are not compatible with the conventional crystalline silicon recycling lines designed mainly for (bulk glass and aluminum) material recovery. If processed through traditional shredding routes, these modules risk materials contamination, lower recovery rates, and regulatory challenges. To address this, companies and research centers are developing specialized, design for recycling pathways ahead of mass commercialization. For instance, Germany PeroCycle project led by ZSW with solar materials and Solaveni combines thermo-mechanical separation to preserve high quality glass with targeted chemical processes to safely recover perovskite materials, aiming for an industrially scalable recycling solutions.

Market Challenges

Uneven Policy Frameworks Creating Compliance and Cost Challenges

The uneven policy frameworks create significant compliance and cost challenges in the solar panel recycling market because end-of-life regulations differ widely across regions, forcing companies to operate under multiple, often inconsistent compliance regimes. For example, in the European Union, PV modules fall under WEEE Directive, but implementation is handled at the national level – resulting in different registration fees, reporting formats, and enforcement intensity across countries, while free-riding manufacturers who avoid compliance reduce cost unfairly and disadvantage compliant recyclers. Moreover, in the U.S. the lack of a federal PV recycling mandate has led to a patchwork system. Such as the Washington State requires manufactures to fund and operate approved stewardship and take-back programs, whereas neighboring states have no comparable obligations, allowing modules to be sold or disposed of at lower cost outside regulated jurisdictions.

Segmentation Analysis

By Type

Monocrystalline Segment is Dominating the Market Due to its High Efficiency

Based on type, the market is segmented into monocrystalline, polycrystalline, and thin films.

The monocrystalline type segment is expected to experience the fastest growth and hold the majority market share of 52.27% in 2026. As monocrystalline solar panels are considered under the premium category due to their high efficiency. Both monocrystalline and polycrystalline solar panels serve the same function in a solar P.V. system by capturing sunlight and converting it into electricity. The cells in both are made from silicon, which is a semiconducting material. The difference between these two stems mainly from the production process of the silicon wafers.

The polycrystalline segment is set to record a significant CAGR of 10.99% during the forecast period (2026-2034).

Thin film solar panels are frequently overlooked due to their lower level of efficiency and as they take up more space, and present significant potential for future growth due to their affordability.

By Process

Mechanical Process Holds Leading Position Due to its Physical Separation Efficiency

Based on process, the market is fragmented into thermal, mechanical, chemical, and other.

The mechanical process is expected to boost the PV recycling market as it is projected to capture the solar panel recycling market share of 67.87% in 2026. Mechanical recycling technology uses devices and principles to separate waste solar photovoltaic modules. The main role of this technology is to efficiently recycle the important components of solar cell modules, such as silicon wafers, metal electrodes, and glass substrates.

The thermal process holds the second highest market share as it provides effective recycling solutions by separating glass, metal, and silicon elements from the solar panels, thereby ensuring maximum resource recovery. Chemical recycling is a more complex process that includes using chemicals to separate altered elements in the solar panel. This method is particularly useful for extracting semiconductors and rare metals.

The chemical process expected to registered a fastest CAGR of 19.22% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Utility Segment Accounted for the Highest Share as Utility Scale Projects are Primary Source of PV Waste

Based on application, the market is segmented into residential, commercial, industrial, utility, and others.

The utility segment is expected to lead with the most dominant share of 34.78% in 2026, and is a commercially attractive application for solar panel recycling because it concentrates the largest volume of modules at single site, making collection, dismantling, and transporting far more efficient than small dispersed system. NREL notes utility scale system account for about two-third of U.S. PV capacity installed annually, which directly transcends into the future for largest recycling stream in terms of volume.

Moreover, the residential segment accounted for the second largest segment in the market, the residential PV recycling is characterized by highly dispersed rooftop systems, smaller batch sizes, and higher collection/logistics cost per panel. The residential segment expected to grow at a CAGR of 15.41% during the forecast period.

SOLAR PANE RECYCLING MARKET REGIONAL OUTLOOK

By geography, the market has been studied geographically across North America, Europe, Asia Pacific, and the rest of the world.

Europe

Europe Solar Panel Recycling Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

Europe accounted for USD 263.02 million in 2025, representing 70.78% of the global market share, and is projected to reach USD 319.66 million in 2026. Globally, Europe leads the market for solar energy due to its transition toward clean energy. Photovoltaic technology utilizes highly purified silicon to convert sunlight into electricity. A France startup, ROSI (Return of Silicon), has developed an innovative and economically viable process for recovering and reusing high-purity silicon, along with other valuable materials. The UK market is projected to reach USD 6.71 billion by 2026, while the Germany market is projected to reach USD 81.73 billion by 2026.

Germany Solar Panel Recycling Market

The Germany market continues to expand, projected to reach a market value of USD 67.08 million in 2025. This underscores the progress in sustainable practices within the solar industry, aiming to enhance resource efficiency and reduce environmental impact.

North America

North America contributed 10.84% to the global market in 2025, with a valuation of USD 37.94 million, and is projected to reach USD 48.96 million in 2026. The North America region is a fast-emerging, policy-fragmented market where growth is driven by utility-scale repowering, storm insurance replacements, and expanding commercial PV fleets, while recycling economics are often constrained by long-distance logistics and limited higher value recovery capacity.

U.S. Solar Panel Recycling Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market is around USD 32.77 million in 2025, accounting for roughly 8.96% of the global market size. The U.S. market is projected to reach USD 42.25 billion by 2026.

Asia Pacific

The Asia Pacific market was valued at USD 56.03 million in 2025, capturing 15.80% of global revenue, and is estimated to reach USD 71.37 million in 2026. The Chinese market has been projected to be valued in USD 31.91 million in 2025. In the Asia Pacific region, India is expected to be worth USD 5.17 million in 2025, while Japan is expected to be worth USD 5.78 million in the same year. The Japan market is projected to reach USD 7.33 billion by 2026, the China market is projected to reach USD 40.48 billion by 2026, and the India market is projected to reach USD 6.71 billion by 2026.

Rest of World

The Rest of the World region is generating USD 8.77 million in revenue and is projected to reach USD 11.63 million in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Constant Investment by Market Players in New Solar Technology, Leading to Their Market Positions

The global solar panel recycling market is highly fragmented, with key players and several medium-scale regional players delivering a wide range of recycling processes at local and country levels across the value chain. Numerous companies are actively operating across different countries to cater to the specific needs of their customers.

Reiling GmbH & Co. KG has introduced a new PV recycling film that reflects recent innovations and significant progress in the field of PV recycling as an opportunity to update the existing film. This updated film allows customers to gain a detailed impression of the recycling solutions being tested for reuse and PV recycling at their specialized PV recycling site in Münster.

List of Top Solar Panel Recycling Companies

- Veolia (France)

- First Solar Inc. (U.S.)

- Reiling GmbH & Co. KG (Germany)

- SILCONTEL LTD (Israel)

- HAMADA CO., LTD (Japan)

- Solarcycle, Inc (U.S.)

- Recycle Solar Technologies Limited (England)

- ROSI (France)

- The Retrofit Companies, Inc.s (Canada)

- Rinovasol (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- May 2025: Solarcycle Inc, a U.S. based company signed a major recycling services agreement with RWE Clean Energy, ensuring that panels from several RWE’s utility scale solar facilities will be sustainably recycled at high purity levels, with recovered materials verified by independent labs. This partnership underscores growing acceptance of certified recycling platforms by large renewable energy developers and manufacturers aiming to integrate circular practices into project lifecycles.

- May 2025: JinkoSolar’s EAGLE Program became the first state approved solar panel recycling and takeback initiative under the revised Washington Stewardship framework, making a milestone in industry-led compliance and demonstrating how manufacturers are beginning to operationalize recycling obligations.

- April 2025: Washington State passed Senate Bill 5175, refining its photovoltaic (PV) Module Stewardship and Takeback Program to create a more comprehensive, long term recycling system. The legislation gives manufacturer until January 2030 to submit approved stewardship plans detailing how they will finance collection, transport and recycling of end-of-life modules and mandate that, starting January 2031, no PV panels can be sold in the state without an approved plan in place.

- May 2024: Less than a year after launching its first PV recycling facility in Germany, Reiling made two significant technological breakthroughs in recycling silicon-based PV modules. They substantially enhanced the quality of recovered PV glass and successfully implemented industrial-scale silicon recovery. These advancements represent critical milestones in the processing of PV modules for advancing toward a closed recycling loop for solar panel materials.

- February 2024: Veolia announced plans to launch more than 40 solar projects on its selected non-hazardous restored landfills, aiming for a total installed capacity of 300 MW. These photovoltaic panels would cover approximately 400 hectares, generating enough electricity to power 130,000 households. The initial plants are scheduled to become operational by 2027. Veolia is also studying the feasibility of additional solar power plants on hazardous waste landfills and sites managed for industrial clients, resulting in over 400 MW of renewable energy installations across France.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product process, Porter’s five forces analysis, and leading recycling business. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 16.13% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Type · Monocrystalline · Polycrystalline · Thin Films |

|

By Process · Thermal · Mechanical · Chemical · Others |

|

|

By Application · Residential · Commercial · Industrial · Utility · Others |

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 365.76 million in 2025.

The market is likely to grow at a CAGR of 16.13% over the forecast period.

By process, the mechanical segment is expected to lead the market due to the development of solar panel recycling technology globally.

The market size of Europe stood at USD 263.02 million in 2025.

Shift from bulk recycling to high value recovery is one of the major trends which promoting the market growth.

Some of the top players in the market are Veolia, First Solar Inc, and Reiling GmbH & Co. KG.

The global market size is expected to reach USD 1,494.38 million by 2034.

- 2021-2034

- 2025

- 2021-2024

- 174

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us