String Inverter Market Size, Share & Industry Analysis, By Power Rating (Up to 10 kW, 10-50 kW, 50-150 kW, 150-450 kW, and Above 450 kW), By Installation Type (Rooftop, Ground-Mounted, and Floating Solar {FPV}), By End-Use Industry (Residential, Commercial, Industrial, Utilities, Agriculture, and Infrastructure and Public Facilities), and Regional Forecast, 2026-2034

String Inverter Market Size and Future Outlook

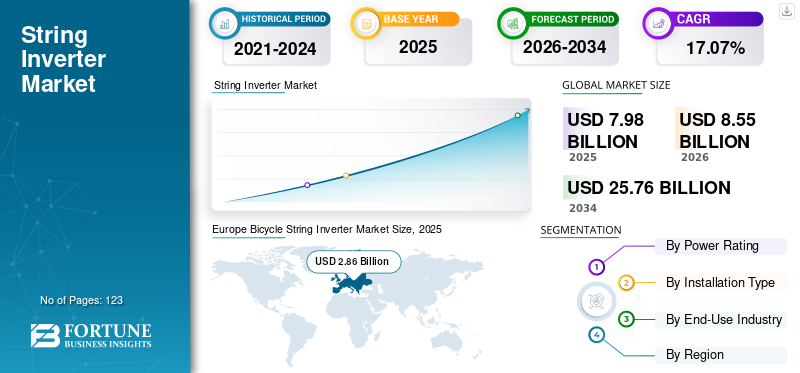

The global string inverter market size was valued at USD 7.98 billion in 2025.The market is projected to grow from USD 8.55 billion in 2026 to USD 25.76 billion by 2034, exhibiting a CAGR of 17.07% during the forecast period. Europe dominated the string inverter market with a market share of 76.44% in 2025.

The string inverter market refers to the segment of the solar Photovoltaic (PV) industry that concentrates on inverters created to convert Direct Current (DC) electricity generated by multiple solar panels connected in a “string” into usable Alternating Current (AC) electricity. The growth of the string inverter industry can be attributed to the rapid expansion of solar PV installations and the growing preference for flexible, low-cost, highly efficient power-conversion solutions. The benefits of string inverters include lower installation costs, ease of installation, modularity, and better system performance monitoring than central inverters; therefore, they are desirable for residential, commercial, and small-to-medium utility solar installations. Strong growth in the market can also be attributed to the significant increase in grid-connected solar panel installations across residential, commercial, and industrial applications. The single phase string inverter sector has grown tremendously over the last few years due to a variety of factors; however, its growth is particularly pronounced as the number of new residential solar systems installed in grid-tied houses increases. Since most residential homes have single-phase electric service, single-phase string inverters are the standard and most complementary solution for residential rooftops.

In September 2025, Sungrow Power Supply Co., ltd displayed a range of innovative products aimed at satisfying the needs of the North American solar market at the 2025 Re+ Conference in Las Vegas. Among these were a new, modular inverter that combines the best features of both central and string inverters and a complete suite of energy storage products. One of their latest offerings is the 4.8 MW SG4800UD-MV-US modular inverter, ideal for large utility-scale PV installations. This inverter comes with innovative diagnostics that enable rapid replacement of individual modules in the field, significantly increasing uptime and reducing balance-of-system costs important steps forward in the evolution of string/modular inverters. To date, Sungrow has installed 870 GW of power electronic converters globally since its founding through June 2025.

String inverter manufacturers include many of the top industry names, such as Sungrow, Enphase Energy, and Huawei. These companies lead the charge in advancing string inverter technologies through their substantial R&D investments and established track records for developing and implementing leading-edge products. As a result, they have a significant global footprint and the ability to mass-produce high-quality string inverters.

Sungrow, Enphase, Ginlong Technologies Co., Ltd., and Huawei Technologies have also invested heavily in developing state-of-the-art, highly efficient, and highly functional string inverters. These cutting-edge string inverter designs utilize advanced technologies (e.g., intelligent monitoring, grid-forming, power density, and energy storage compatibility) that make them ideal solutions for new residential, commercial, and utility-scale solar applications.

Download Free sample to learn more about this report.

STRING INVERTER MARKET TRENDS:

Rapid Growth of Solar PV Installations Globally is Driving Market Growth

The market is being driven by the growth of solar PV installations globally. String inverters remain the preferred type of inverter for residential, commercial, & small to medium utility-scale projects. Rapidly declining solar module pricing, supportive government policies, and international carbon-reduction targets are making the deployment of rooftop solar PV (Distributed Generation) systems increasingly favorable. The advantages of string inverters for these applications include modular design, lower upfront cost, and easy installation compared with central inverters. Further, the rising use of Solar PV in larger commercial and industrial applications has created an increasing need for 3-Phase string inverters, which can be scaled up and provide better system monitoring than can central inverters.

In March 2025, According to the U.S. Energy Information Administration (EIA), there will be 32.5 Gigawatts (GW) of added renewable resource capacity, 18.2 GW of energy storage capacity, and thus, total capacity for new resources will exceed 63 GW, to set a new record for the highest amount of new installed capacity in one calendar year. Solar PV remained the fastest-growing source of new electricity generation in 2025. Thus, as solar PV remains the leading source of new electricity generation in 2025, the global market will continue to have very high and stable demand for string inverters.

MARKET DYNAMICS

MARKET DRIVERS:

Technological Advancements in String Inverter Design to Drive Market Growth

The innovation in designs will expand the string inverter market growth by improving efficiency, reliability, and grid compatibility, thereby reducing the overall cost of all components. To illustrate how modern-day string inverters differ from past models, we now see much higher power ratings, the adoption of advanced Maximum Power Point Tracking (MPPT) algorithms, and improved conversion efficiencies, which enable them to manage larger solar array systems with higher energy output. By adding innovative monitoring capabilities, remote diagnostics, and AI-based fault detection, operators can improve performance and minimize downtime. New designs will also allow for a grid (form and support function) to assist utilities in supporting voltage and frequency stability as solar penetration continues to increase. Additionally, new storage-ready and hybrid string inverters will enable seamless integration with batteries, supporting solar-plus-storage setups.

In January 2026, Sungrow unveiled its next-gen high-power string (modular) inverter systems that provide both utility-scale and C&I solar developers with advanced options. With the following features, higher power density enables larger PV string installations, advanced thermal management, and intelligent fault detection and rapid module replacement.

As a result, this revolutionary technology is reducing the time required to replace modules, ultimately reducing downtime and O&M costs and encouraging greater use of string inverters in large-scale solar plants where central inverters have traditionally dominated.

Download Free sample to learn more about this report.

MARKET RESTRAINTS:

Higher Maintenance Requirements Compared to Central Inverters May Hamper Market

Compared with centralized inverters, the higher maintenance requirements of string inverters can impede the market growth potential of the market. The reason is that most string-inverter systems use multiple individual inverters distributed across the entire solar facility. Although this modular architecture enhances system redundancy, it also requires multiple inverters to undergo regular inspection, monitoring, and maintenance, as opposed to a single centralized inverter. There are also operational complexities inherent in the number of electronic components, cooling systems, and communication interfaces within each string inverter, resulting in additional operational and maintenance expenses throughout the life of these systems.

MARKET OPPORTUNITIES:

Rising Adoption of Distributed and Rooftop Solar Systems to Drive Market Growth

Small commercial and residential rooftop solar systems typically operate at reduced capacity. Still, such projects require a solar inverter that is simple to install, can accommodate various orientations and shading conditions, and is cost-effective. String inverters are suitable for many of these applications, including multiple MPPTs (maximum power point trackers), a compact size, and a simplified system architecture compared to large commercial inverter systems (often referred to as central inverters). Additionally, as demonstrated by government programs, including net-metering, which will help build consumer confidence in rooftop solar, along with electricity tariffs, there is increasing interest in rooftop solar among residential and commercial customers in urban and semi-urban areas.

In November 2025, as per the statistical Review of World Energy, in the nine months leading up to the end of September 2025, India added 4.9 gigawatts of new rooftop solar power, an increase from 1.9 gigawatts during that same time frame in 2024, indicating that the market for distributed/panel PV systems is growing rapidly, resulting in a significant increase (161%) in the number of string inverters produced as a result. Rooftop installations typically utilize string or hybrid-style inverters.

MARKET CHALLENGES:

Exposure to Harsh Environmental Conditions to Hamper Market Growth

The market may be negatively affected by severe environmental conditions, as string inverters (sensitive electronic devices) need to maintain reliable operation outdoors for extended periods. Inverter components such as power semiconductors, cooling systems, and other electronic circuits will degrade and fail faster in areas of extreme heat or humidity, as well as areas characterized by large amounts of dust, sand, excessive rain, or very corrosive environments. High temperatures can decrease the efficiency of inverters and shorten their components' lifespans; dust and moisture can prevent cooling channels from working effectively and cause electrical failures.

Segmentation Analysis

By Power Rating

Up to 10 kW Segment is Ideally Suited for Residential and Small Commercial Rooftop Solar Installation, which Drives Segment Growth

Based on power rating, the market is classified into up to 10 kW, 10-50 kW, 50-150 kW, 150-450 kW, and above 450 kW.

The up to 10 kW segment dominates the market, and the market is growing, with the largest market share of 37.23% in 2025. Due to compatibility with the capacity needs of residential and small commercial solar systems, the largest market segment in terms of the overall global deployments, the <10 kW category is by far the leading segment of the string inverter market. In essence, most roof-mounted PV systems installed in residential homes, small offices, retail stores, and small businesses fall within this power range; therefore, <10 kW string inverters are also the most frequently used configuration.

The 50-150 kW market segment is the fastest-growing. Due to the rapid growth of the 50–150 kW segment in the market, the overall market has grown as well. Commercial and industrial users, as well as small-scale utilities, are using this size of string inverter to support scalability, reliability, and capacity as they continue to grow and develop more solar energy systems. This size of string inverter is ideal for solar rooftop installations, factories, warehouses, data centers, and ground-based distributed solar installations with much higher energy use than a typical home; therefore, a large central string inverter may not be a viable option. The 50-150 kW market segment is projected to grow at a CAGR of 18.27% during the forecast period.

By Installation Type

Majority Use of String Inverters Led to Dominance of Rooftop Segment

By installation type, the market is categorized into rooftop, ground-mounted, and Floating-Solar (FPV).

The rooftop segment dominates the market. The market is growing, with a 67.88% share in 2025. Rooftop installations are a significant component of global PV, and the majority of these installations use string inverters, making rooftop systems the largest segment of the market. Rooftop installations often require cost-effective, modular, and flexible inverters that can handle restrictive areas, varying roof orientations, and partial shading; therefore, string inverters are well-suited for these installations as they feature multiple MPPTs and are compact.

The ground-mounted is the fastest-growing segment in the market. The ground-mounted segment will grow at a CAGR of 17.97% during the forecast period of 2026-2034. As electricity demand from utility companies, industry, and data centers increases due to population growth and technological developments, more ground-based solar power systems are being developed. In some parts of the country, there are many areas available for constructing ground-mounted solar plants that are both environmentally friendly and economically beneficial to the communities where they are created.

By End-Use Industry

Rising Rooftop Solar Adoption by Homeowners Seeking Lower Electricity Bills Drives Growth in Residential Segment

By end-use industry, the global market is segmented into residential, commercial, industrial, utilities, agriculture, and infrastructure and public facilities.

The residential segment dominates the market, with a 30.15% market share in 2025. String inverters provide homeowners with an excellent mix of affordability, efficiency, and reliability for residential solar systems, typically in lower-power ranges. The rising cost of electricity, various government subsidies, favorable net metering regulations, and growing conviction in the need for energy independence are all helping homeowners make the switch to rooftop solar power.

The commercial segment is the second-largest segment in the market. The commercial segment is expected to grow at a CAGR of 18.83% during the forecast period. Mid-size commercial buildings such as office buildings, shopping centers, medical facilities, business warehouses, and others will generally install mid-size solar array systems on their rooftops or on the ground with a three-phase inverter system that offers modularity, increasing number of strings as needed, multiple MPPT options for complex rooftop systems, and a good system efficiency rating.

To know how our report can help streamline your business, Speak to Analyst

String Inverter Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Europe

Europe held the dominant string inverter market share in 2025, valued at USD 2.86 billion, and also led in 2026, with USD 2.97 billion. Due to significant growth occurring in the solar photovoltaic (PV) installation market in Europe, the overall market size today is. Strong expansion in the adoption of rooftop and distributed solar systems across Europe has resulted from projections of future decarbonization goals set by many countries, including those in Europe. Countries throughout Europe are increasing their deployment of solar energy systems to meet their need for alternative sources of energy and decreasing reliance on fossil fuels while increasing energy security; this is especially true for residential, commercial, and community applications, where string inverters are commonly used systems for connecting to these types of renewable energy sources.

Europe String Inverter Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

U.K. String Inverter Market

The U.K. market in 2025 is estimated at around USD 0.18 billion, representing roughly 6.14% market share in the global market.

Germany String Inverter Market

The German market in 2025 is estimated at around USD 0.57 billion, representing roughly 19.89% of the global market.

Asia Pacific

Asia Pacific accounted for USD 2.19 billion in 2025 and is estimated to be valued at about USD 2.36 billion in 2026. In the Asia Pacific region, the market has been growing fast due to rapid growth in the Photovoltaic (PV) space, government policy that supports solar energy development & adoption (including via distributed generation), and owing to nations developing either a rooftop or distributed generation network. All countries in the region have been building both residential, commercial, and utility-scale solar energy facilities to support increasing electricity demand and achieve their goals for reducing carbon emissions. The preference for string inverters stems from their cost-effectiveness, modular design, flexibility in implementing distributed generation & rooftop solar systems, and the wide range of applications.

China String Inverter Market

In 2025, the China market reached USD 0.77 billion. The growth can be attributed to China's continued leadership in the global Photovoltaic (PV) installations (solar), with continued government support for large-scale rooftops as well as rapidly increasing levels of distributed PV installed throughout China. The increased demand for flexible, easy-to-scale string inverter solutions is driving cost-effective solutions with a strong focus on commercial and industrial, residential, and county-level distributed PV projects, as highlighted above, and as China's focus on supporting local county-level distributed PV projects.

In July 2025, Huawei continued developing its Smart String Grid-Forming Energy Storage (ESS) offerings by adding new features, such as integrated String Inverters to Grid Forming capabilities that can both strengthen the energy supply and deliver renewable energy to consumers 24/7. This development reflects Huawei’s commitment to developing next-generation inverter solutions, further extending the capabilities of string inverters to provide reliable energy solutions for both residential and commercial applications.

India String Inverter Market

The Indian market was valued at around USD 0.44 billion in 2025, accounting for roughly 19.89% of the global market.

North America

North America was valued at roughly USD 1.73 billion in 2025 and is estimated to be around USD 1.86 billion in 2026. Factors such as robust growth in solar photovoltaics installations, increased use of rooftop and distributed solar, and rising interest among consumers for low-cost, flexible inverter products will be the driving forces behind continued growth in the North American market for string inverters.

U.S. String Inverter Market

The U.S. market reached a valuation of around USD 1.37 billion in 2025. Rapid growth in Solar Photovoltaic (PV) installations, driven in part by strong federal and state policies, has supported the expansion of the U.S. market. Incentives such as the Investment Tax Credit (ITC), state-set renewable energy targets, and net metering programs have created an environment conducive to the installation of rooftop and Distributed-Generation (DG) solar PV systems. Consequently, most customers are choosing string inverters for their PV installations.

Latin America & Middle East & Africa

Latin America and the Middle East & Africa accounted for USD 0.87 billion and USD 0.34 billion each in 2025, respectively. Due to the rapid growth and expansion of solar photovoltaics in Latin America, increasing demand for electricity, and favorable policies supporting renewable energy use in the region, there is tremendous potential for a growing market for string inverters in Latin America. Brazil, Mexico, Chile, and Colombia have all made significant investments in solar power as part of an overall effort to diversify their energy supply and reduce their dependence on traditional utility services. On the other hand, due to increased investments in solar PV projects, abundant solar resources, and rising demand for reliable, affordable electricity, the demand for solar string inverters is on the rise in the Middle East & Africa. Governments throughout the region are supporting solar initiatives to create cleaner sources of power, reduce reliance on fossil fuels, and provide people access to electricity especially those living in remote or off-grid locations.

GCC String Inverter Market

The GCC market was valued at around USD 0.14 billion in 2025, representing roughly 40.14% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players:

Key Players are Actively Focusing on Product Innovation and Intelligent Monitoring Features

String inverter market vendors are actively innovating and expanding their product portfolios to meet growing global demand for flexible, efficient, and reliable solar power solutions. Major manufacturers including Sungrow, Huawei, Enphase Energy, SMA Solar Technology, and SolarEdge are introducing advanced string inverters with higher power ratings, improved efficiency, enhanced monitoring and diagnostics, and support for energy storage integration.

In February 2025, Huawei's new SUN5000-150K-MG0 class string inverter was explicitly designed for large-scale PV applications and offers all the features necessary (MPPT, high efficiency, etc.) to make it a suitable option for large-scale (commercial or industrial) ground-mounted PV systems.

LIST OF KEY STRING INVERTER COMPANIES PROFILED IN REPORT:

- Huawei (China)

- Cabot Corporation (U.S.)

- Trelleborg AB (Sweden)

- BASF SE (Germany)

- Sungrow (China)

- Fronius (Austria)

- GoodWe China)

- SMA Solar Technology (Germany)

- Delta Electronics (Taiwan)

- Ingeteam (Spain)

KEY INDUSTRY DEVELOPMENTS:

- December 2025: Huawei launched the Huawei FusionSolar 9.0 platform to provide intelligent string inverters and intelligent energy management with control systems to support solar power generation to support the grid and, in turn, provide utility in as much as to provide renewable energy in challenging areas and provide greater stability to frequently unstable grid Conditions.

- November 2025: Fronius launched GEN24, which completed testing and is fully compatible with MidNite Solar's Rosie battery inverter. The two products can be paired, allowing homeowners to use string inverters with low-voltage battery storage for critical backup power and more effective self-consumption. Moving forward, the compatibility between the GEN24 and Rosie improves the appeal of GEN24 string inverters in integrated solar + storage applications.

- September 2025: SMA Solar Technology AG and Create Energy agreed to enter into a memorandum of understanding under which SMA would manufacture its Sunny Highpower PEAK3 string inverters at Create Energy's facility in Portland, Tennessee. This is the first time in over 10 years that SMA has had products manufactured in the U.S., and production is expected to begin in early 2026. By making localized supplies more readily available, shortening delivery lead times, and strengthening SMA's position in the U.S. market, both companies will provide significant benefits to each other's business operations.

- August 2025: GoodWe introduced a 50 kW Commercial & Industrial (C&I) string inverter as part of its SDT series, designed for small- to medium-sized C&I solar installations. This inverter delivers quiet operation (below 50 dB) at full load, supports up to 180% PV oversizing, and offers multiple MPPTs to maximize energy harvest in complex rooftop deployments, underscoring GoodWe’s focus on high-performance string inverter solutions for distributed solar markets.

- July 2025: Cabot Corporation launched the new LITX 95F conductive carbon. This new material was developed for use in lithium-ion batteries for Energy Storage Systems (ESS). The improvements made by the new LITX 95F, including higher battery conductivity, extended cycle life, and improved performance, are significant for renewable energy applications such as solar + storage systems, which rely on string inverters to operate efficiently. By using advanced battery materials such as LITX 95F, PV systems can achieve higher performance when integrated with storage (ESS).

REPORT COVERAGE

The global string inverter market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation:

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 17.07% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Power Rating

By Installation Type

By End-Use Industry

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 7.98 billion in 2025 and is projected to reach USD 25.76 billion by 2034.

The market is expected to exhibit a CAGR of 17.07% during the forecast period (2026-2034).

The residential segment led the market in terms of end-use industry.

Technological advancements in string inverter design to drive the market growth.

Huawei, Cabot Corporation, BASF SE, and other companies are among the prominent players in the market.

Europe held the largest market share in 2025.

Rising adoption of distributed and rooftop solar systems to drive the market growth.

- 2021-2034

- 2025

- 2021-2024

- 123

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us