Strontium Market Size, Share & Industry Analysis, By Form (Powder, Granular, and Others), By Grade (Technical Grade, Industrial Grade, and Others), By Type (Strontium Carbonate, Strontium Nitrate, Strontium Fluoride, Strontium Sulfate, and Others), By Application (Glass & Ceramics, Pyrotechnics & Fireworks, Electronics & Magnetic Materials, Pharmaceuticals, Chemical Manufacturing, and Others), and Regional Forecast, 2025-2035

STRONTIUM MARKET SIZE AND FUTURE OUTLOOK

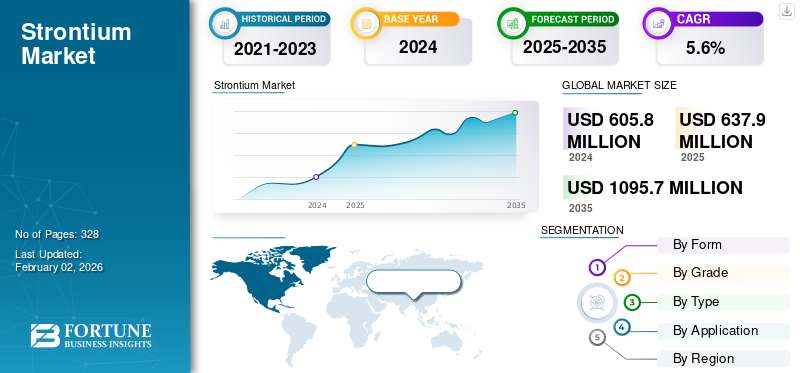

The global strontium market size was valued at USD 605.8 million in 2024. The market is projected to grow from USD 637.9 million in 2025 to USD 1,095.7 million by 2035 at a CAGR of 5.6% during the forecast period, 2025-2035. Asia Pacific dominated the global strontium market with a market share of 56.77% in 2024.

Strontium is a naturally occurring element found in the earth’s crust, known for its bright, clean flame and its role in several everyday products. It is usually obtained from a mineral called celestite, which contains the product in a form that can be processed for different uses. In its purified form, the product appears as a soft, silvery metal, but it is primarily traded and used in the form of various product compounds.

The value of the product continues to increase as new industries discover additional applications for it. Modern research is exploring its role in advanced ceramics, electronics, and specialty materials that require stable performance and reliable properties. Some companies also utilize product compounds in environmental applications, such as treating metals or enhancing the quality of specific products. Hebei Xinji Chemical Group Co., Ltd, Kandelium GmbH, Solvay SA, Joyieng Chemical Limited, and JAM Group Co. are the key players operating in the market.

Download Free sample to learn more about this report.

STRONTIUM MARKET TRENDS

Movement Toward Higher-Purity Grades Across End-Use Industries Boosts Market Growth

Movement toward higher‑purity product grades is a structural demand driver as advanced electronics, optics, defense, and medical applications increasingly specify 99–99.9%+ purity, which cannot be easily substituted or downgraded. This trend deepens the value pool within the market by shifting volumes from bulk technical grades into higher‑margin, specification‑critical products.

High‑purity strontium carbonate and nitrate feed high‑k titanates, ferrites, and luminescent materials used in MLCCs, sensors, 5G/IoT hardware, and advanced displays. Growth in consumer electronics, automotive electronics, and network equipment, therefore, translates into not only higher absolute product demand but also a rising share of demand locked into high‑spec, recurring contracts.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Use of Strontium in Glass and Ceramic Manufacturing Drives Market Growth

The increasing use of product compounds in glass and ceramic manufacturing is becoming an important driver of the global strontium market growth. In glass production, materials such as strontium oxide (SrO) and strontium carbonate help improve durability, thermal resistance, and overall strength. Due to these properties, the product is widely used in high-strength architectural glass, display glass, and technical glass for electronic applications.

According to research published in Silicon (Springer), adding a product to silicate glass changes the structure of the glass network, improves chemical durability, and increases mechanical stability. These benefits make product-enhanced glass suitable for use in medical ceramics, dental materials, and other high-performance applications.

A study available on NCBI found that when some of the calcium in fluorapatite glass-ceramics is replaced with market product, the material forms smaller and more numerous crystals. It also becomes more soluble. These changes help improve the performance of advanced glass and ceramic products.

MARKET RESTRAINTS

Fluctuating Strontium Ore Supply Limits Stable Market Growth

The growing demand for strontium across various applications, including glass, ceramics, magnets, and electronics, continues to expand; however, the market faces steady constraints due to fluctuations in ore supply. The product is mainly extracted from celestite, and only a limited number of countries operate large-scale mining and processing facilities. This concentrated supply base makes the industry vulnerable to disruptions caused by mining delays, regulatory tightening, or logistical challenges. As most downstream manufacturers depend entirely on consistent ore availability to maintain production of strontium carbonate, strontium nitrate, and ferrite materials, any disturbance at the mining stage can affect the entire supply chain.

According to the U.S. Geological Survey (USGS), the U.S. has not mined product ore since 1959. It relies 100% on imports to meet domestic demand, underscoring the limited global production footprint and exposure to supply risk. In addition, global resource distribution further complicates stable supply. Although strontium-bearing minerals are widely present in nature, only a small share is economically viable for commercial extraction. According to Science Direct research, recoverable reserves suitable for mining are far more limited than total natural occurrences, reinforcing the dependency on a handful of producing regions.

MARKET OPPORTUNITIES

Increasing Use of Strontium in Battery and Energy Storage Development Supports Future Growth

Global growth in electric vehicles and large-scale battery storage is creating a clear opportunity for wider use of the product in advanced energy systems. As transportation and power networks shift toward electrification, new materials that offer stability, heat resistance, and long operating life are gaining attention. Product-based compounds are being valued for use as electrode additives, solid electrolyte support, and ceramic components in energy-storage and power-conversion systems. These roles are expected to grow as demand increases for durable and efficient storage technologies.

According to the International Energy Agency (IEA), global electric car sales reached 14 million units in 2023, representing a 35% increase compared with the previous year, and are projected to continue expanding rapidly through 2030. The rise in EV production increases demand for various types of motors, power electronics systems, and batteries. As manufacturers strive to enhance safety, thermal stability, and performance, interest is increasing in alternative and supplementary materials that can support next-generation battery chemistries. Product-based ceramics and additives are being studied for roles in thermal stabilization, electrode support, and component durability, aligning with the needs of expanding EV supply chains.

MARKET CHALLENGES

Price Volatility of Raw Materials is Challenging Factor for Market Growth

Strontium prices are structurally unstable as they are tied to thin, geographically concentrated mining economics and to volatile freight and logistics costs, rather than to any deep, transparent global benchmark. In downturns, high‑cost or small miners exit quickly, shrinking effective supply and amplifying price swings when demand or freight costs turn again.

Mining economics are highly sensitive to ore grade, stripping ratios, and local regulations; as grades decline or environmental compliance costs rise, marginal cash costs per ton increase disproportionately. When demand weakens and prices fall toward or below the marginal cost of high‑cost operations, smaller and less efficient miners quickly curtail output or shut down, tightening supply and setting the stage for abrupt price rebounds once demand normalizes. As new projects require significant upfront capital and permitting time, supply cannot ramp back quickly, so short‑term shortages translate directly into price spikes rather than volume responses.

Regulatory Compliance May Hurdle Market Expansion

Regulatory compliance can significantly slow and constrain the market by increasing costs, lengthening project timelines, and tightening permissible exposure and discharge limits. These hurdles weigh most heavily on new mining projects, high‑volume processors, and applications that face direct environmental or public‑health scrutiny.

Mining of celestite and other strontium‑bearing ores is subject to increasingly stringent environmental‑impact assessments, land‑use restrictions, and community consultation processes, which extend lead times and raise permitting risk for new projects. In sensitive regions, concerns over groundwater, biodiversity, and legacy contamination can lead to denial of permits or tighter conditions, effectively limiting the number of viable new mines and reinforcing supply concentration.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Trade protectionism and geopolitical tensions increase cost, risk, and volatility in the market by disrupting cross‑border flows of ore and chemicals, raising tariffs, and amplifying the impact of China‑centric supply. These forces translate into higher landed prices, more fragile availability for import‑dependent regions, and greater uncertainty for investment decisions.

Global strontium supply is heavily concentrated in a small number of producing countries (notably China and Mexico), so any geopolitical friction, export restriction, or diplomatic tension with key consuming regions magnifies supply‑security concerns.

Moves toward resource nationalism, export licensing, or critical‑minerals control regimes can limit volumes available to the open market, reinforce the pricing power of dominant producing countries, and raise the risk premium embedded in long‑term contracts.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D in the market is moving toward higher‑purity chemistries, new functional materials, and process innovations that reduce cost and environmental footprint. This is being driven by electronics, medical, and specialty materials demand, and by tighter regulatory and ESG expectations. Investments in advanced analytical tools (ICP‑MS, inline sensors, statistical process control) support real‑time quality monitoring and tighter specification windows, especially for high‑purity and medical grades. Data‑driven process optimization and modeling are being used to stabilize product quality across batches, reduce scrap, and speed up scale‑up from lab to pilot to commercial production.

SEGMENTATION ANALYSIS

By Form

Powder Became a Popular Form Due to Its Fine Particles and Widespread Use

Based on form, the market is segmented into powder, granular, and others.

The powder segment held the largest market share in 2024. It is widely utilized in ceramics, pyrotechnics, ferrite magnets, pigments, and electronics, where controlled particle size is critical for formulation stability and technical performance. Powdered strontium carbonate and strontium nitrate remain especially important in advanced ceramics and red flame compositions due to their consistent dispersion characteristics.

The granular segment held a notable market share. Granular product is preferred in metallurgical applications, particularly in aluminum-silicon alloy modification, due to its slower dissolution rate, improved handling safety, and reduced dust emissions. Its larger particle size makes it suitable for foundry environments, where controlled alloying and reduced material loss are essential. The automotive and aerospace sectors are increasingly adopting granular forms for precision casting and weight-optimized components.

The others segment includes solution-based, compressed, and specialty forms used in niche applications such as biomedical coatings, catalysts, laboratory reagents, and R&D-grade product compounds. Although small in market share, this segment benefits from specialized demand in pharmaceuticals, bioceramics, and advanced material research.

By Grade

Others Grade Segment Led Due to Its Broad Applicability Across Various Applications

Based on grade, the market is segmented into technical grade, industrial grade, and others.

The others grade segment based on value held the dominating strontium market share in 2024. The others category includes high-purity grades, pharmaceutical-intermediate grades, and specialized product compounds such as strontium carbonate (ultra-high purity), strontium chloride, strontium nitrate, and strontium titanate. The emerging applications, such as strontium titanate in optoelectronics, dielectric materials in MLCCs, and next-generation semiconductor substrates, are shaping long-term strategic relevance. Pharmaceutical applications (e.g., nutritional supplements) also contribute incremental growth.

Industrial grade registers a significant growth due to its broad applicability across metallurgy, ferrite magnets, master alloys, zinc refining, and polymer stabilizers. The grade benefits from large-scale industrial operations and relatively low production cost compared with high-purity forms.

Technical grade represents a notable share of global consumption and remains closely tied to industries requiring moderate–to–high purity but not ultra-specialized processing. Its demand is strongest in pyrotechnics, pigments, ceramic colorants, and glass modifiers, where consistency and reactivity matter more than extremely high purity.

By Type

Strontium Carbonate Segment Dominates Due to Its Versatility

Based on type, the market is segmented into strontium carbonate, strontium nitrate, strontium fluoride, strontium sulfate, and others.

Strontium carbonate is the dominant product type due to its versatility and large-scale use across pyrotechnics, ferrite magnets, ceramics, and master alloys. Its role as a precursor in producing many other product compounds makes it the backbone of the value chain. Consumption remains strong in product ferrite magnet manufacturing, particularly in China and East Asia, where high-volume appliance and automotive component industries rely on low-cost permanent magnets. The compound’s use in red pigments and ceramic glazes also supports stable long-term demand.

Strontium nitrate has a more specialized use profile, with primary consumption in pyrotechnics and signal flares, where it delivers the characteristic bright red flame. Additional applications include military flares, safety signaling devices, and specialty glass.

Strontium fluoride serves niche but technologically important applications, especially in optical materials, high-performance ceramics, metal refining fluxes, and CVD/epitaxy processes. Its high refractive index and transparency in UV/IR wavelengths make it attractive in photonics and high-end optics. Although volumes are relatively low, the grade commands premium pricing due to purity requirements and specialized production routes.

The others category includes strontium chloride, strontium titanate, strontium oxide, strontium bromide, and high-purity specialty salts. These compounds are increasingly relevant in advanced ceramics, dielectric materials, superconductors, optoelectronics, and pharmaceutical intermediates.

By Application

Electronics & Magnetic Materials Segment Led Due to Its Use in Next-Generation Semiconductor, Photonic, and Magnet Applications

Based on application, the market is segmented into glass & ceramics, pyrotechnics & fireworks, electronics & magnetic materials, pharmaceuticals, chemical manufacturing, and others.

The electronics & magnetic materials segment held a dominating share as it underpins a broad spectrum of high-performance materials used in next-generation semiconductor, photonic, and magnet applications. Electronics & magnetic materials is one of the more critical and evolving segments, which covers strontium ferrite magnets, strontium titanate, and compounds used in dielectric materials, photonics, and optical components.

Glass and ceramics form one of the most stable demand bases for strontium, leveraging its ability to improve thermal shock resistance, color stability, high-temperature strength, and optical properties.

The pyrotechnics & fireworks segment is set to register significant growth during the forecast period. Strontium nitrate and carbonate are central to producing red flames, making pyrotechnics one of the most recognizable applications of strontium.

Chemical manufacturing includes the use of product compounds as intermediates, stabilizers, and catalysts, as well as feedstock for creating more complex strontium salts. Strontium carbonate and sulfate, in particular, are key raw materials in producing strontium nitrate, titanate, chloride, ferrite precursors, and other specialty chemicals.

The others category includes emerging and niche applications such as oil & gas drilling fluids, paints, coatings, and pigments.

To know how our report can help streamline your business, Speak to Analyst

GLOBAL STRONTIUM MARKET REGIONAL OUTLOOK

By region, the market is divided into Asia Pacific, North America, Europe, Latin America, and the Middle East & Africa.

Asia Pacific Strontium Market Size, 2024 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

Asia Pacific accounted for the leading strontium market share in 2024. The market growth is driven primarily by China, India, and Japan. The region dominates both production and consumption, with China being the world’s leading processor of strontium carbonate, nitrate, and ferrite materials. The region’s key demand drivers include fireworks manufacturing, ceramics, ferrite magnet production, consumer electronics, automotive components, and general industrial chemicals. Asia Pacific’s dense manufacturing base ensures that strontium remains a strategically relevant material.

To know how our report can help streamline your business, Speak to Analyst

North America

North America represents a moderate-sized, specialized market with steady consumption in pyrotechnics, electronics, ceramics, and chemical manufacturing. While domestic production of celestite/strontium compounds is limited, the region relies heavily on imports from Mexico and Asia. Within this region, the U.S. registers the dominant share, primarily due to its larger-scale end-use industries, higher consumption intensity in electronic ceramics and advanced material applications, and the greater concentration of specialty chemical manufacturers.

Europe

Europe’s market is highly regulated but diversified, supported by applications in specialty glass, ceramics, pyrotechnics (professional grade), magnets, pigments, and various industrial chemicals.

Latin America

Latin America’s celestite output is exported for processing, making it an important upstream supplier in the global value chain. Local consumption is modest but steady, driven by industries such as pyrotechnics, ceramics, and chemical processing. Brazil contributes to regional demand through its manufacturing and consumer goods sectors.

Middle East & Africa

The Middle East & Africa market remains relatively small but shows selective industrial activity in chemicals, ceramics, construction materials, and oilfield applications. Demand is influenced by construction cycles in GCC economies and industrial expansion in parts of North Africa.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Hebei Xinji Chemical Group Co., Ltd., Kandelium GmbH, Solvay SA, Joyieng Chemical Limited, and JAM Group Co. are the key players in the market. Major investments by companies in developing products that address evolving demands for sustainability and performance.

LIST OF KEY STRONTIUM COMPANIES PROFILED:

- Central Drug House (CDH) Fine Chemicals (India)

- Divjyot Chemicals Pvt Ltd (India)

- Jam Group Co. (Iran)

- Kandelium GmbH (Germany)

- Solvay (Belgium)

- Star Earth Minerals Pvt Ltd (India)

- Suvchem (India)

- Vishnu Priya Chemicals Pvt Ltd (India)

- Joyieng Chemical Limited (China)

- Hebei Xinji Chemical Group Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS:

- August 2025 – Vishnu Chemicals Limited announced that its wholly owned subsidiary, Vishnu Strontium Private Limited, has commenced commercial production of Strontium Carbonate at its manufacturing facility in Atchutapuram, Visakhapatnam, Andhra Pradesh. The company informed the exchanges that the commencement of production marks an important milestone in its specialty chemicals business.

- July 2024 – Vishnu Priya Chemicals Pvt Ltd, a leading manufacturer of high-performance specialty chemicals, announced its acquisition of Jayansree Pharma Private Limited (JPPL). This acquisition, finalized through a Share Purchase Agreement on August 19, 2024, represents a significant strategic expansion for Vishnu Chemicals, reinforcing its market position and operational capabilities.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, Form, Grade, Type, and Application. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2035 |

|

Base Year |

2024 |

|

Forecast Period |

2025-2035 |

|

Historical Period |

2021-2023 |

|

Unit |

Value (USD Million), Volume (Kiloton) |

|

Growth Rate |

CAGR of 5.6% from 2025 to 2035 |

|

Segmentation |

By Form

By Grade

By Type

By Application

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 605.8 million in 2024 and is projected to reach USD 1,095.7 million by 2035.

Recording a CAGR of 5.6%, the market is slated to exhibit steady growth during the forecast period of 2025-2035.

The strontium carbonate segment leads the market.

Asia Pacific held the highest market share in 2024.

Rising use of strontium in glass and ceramic manufacturing drives market growth.

- 2021-2035

- 2024

- 2021-2023

- 328

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us