Surgical Robots Market Size, Share and Industry Analysis By Application (General Surgery, Gynecology, Urology, Orthopedics, Others), By End User (Hospitals, Ambulatory Surgery Centers, Others) and Regional Forecast, 2026 - 2034

Last Updated: June 15, 2026

| Format: PDF

| Report ID:

FBI100948

Thank you for your interest in the

"United States Medical Devices Market!"

To receive a sample report, please provide the following details:

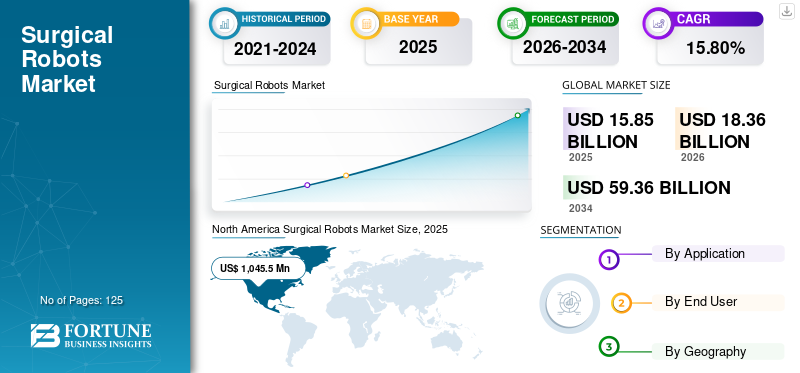

The global surgical robots market size was valued at USD 15.85 billion in 2025. The market is projected to grow from USD 18.36 billion in 2026 to USD 59.36 billion by 2034, exhibiting a CAGR of 15.80% during the forecast period. North America dominated the surgical robots market with a market share of 71.46% in 2025. Growing demand for minimally invasive surgery, the aging population, and the increasing prevalence of chronic diseases are key drivers for the market.

The global surgical robots market is driven by rising procedural volumes, increasing demand for precision-driven interventions, and continuous technological advancement across healthcare systems. The market has transitioned from early adoption toward broader clinical integration, particularly in high-income regions with advanced healthcare infrastructure. Adoption remains strongest in tertiary hospitals, academic medical centers, and specialized surgical facilities.

Market momentum has accelerated as robotic-assisted procedures demonstrate measurable clinical value through reduced complication rates, shorter hospital stays, and improved procedural consistency. Surgical robots are increasingly viewed as strategic capital investments rather than experimental technologies. This shift reflects growing confidence among healthcare providers, payers, and regulators in the long-term clinical and economic benefits of robotic-assisted surgery.

From a lifecycle perspective, the market is moving from early commercialization toward structured expansion. Growth is supported by rising procedure volumes, expanding surgeon training programs, and gradual cost optimization across platforms. While capital intensity remains a constraint, broader reimbursement acceptance and technology standardization are improving accessibility.

The market growth is expected to remain robust. Demand will be driven by expanding surgical indications, particularly in minimally invasive and complex procedures. Emerging economies are expected to contribute incremental growth as healthcare infrastructure matures and access to advanced surgical technologies improves. The long-term outlook reflects sustained investment, gradual democratization of robotic platforms, and continued clinical validation across multiple specialties.

Surgery has evolved from open-surgery to robotic surgery. Surgical robots can perform complex procedures with geometrical precision, even in anatomical areas that are difficult to reach by human surgeons. This is resulting in increased demand and adoption of the minimally invasive surgeries is one of the key drivers for the growth of the surgical robots industry.

The increasing need for automation in healthcare, increasing geriatric population, increasing prevalence of chronic diseases, and highly complex surgical procedures are some of the major factors driving the surgical robotics market growth. The da Vinci surgical system manufactured by Intuitive Surgical Inc., is one of the well-known and widely used robotic surgical devices in the world.

North America dominated the surgical robots market with a 71.46% share in 2025.

General Surgery held the largest application segment share in 2025.

Hospitals accounted for the leading end-user segment share in 2025.

Key Regional Highlights

North America

North America led the global market, supported by strong adoption of robotic-assisted surgeries.

North America

Asia Pacific is projected to register the fastest growth during the forecast period.

Europe

Europe is witnessing steady market expansion through hospital modernization and clinical research.

U.S.

U.S. High prevalence of chronic diseases and strong healthcare infrastructure continue to drive market growth.

Japan

Japan Rising adoption of advanced robotic surgical technologies supports continued market expansion.

Read More

What major trends are shaping the surgical robots market?

The surgical robots market is undergoing structural transformation driven by rapid technological convergence and evolving clinical expectations. One of the most significant trends is the integration of artificial intelligence and advanced analytics into robotic platforms. These capabilities support real-time decision assistance, motion optimization, and enhanced surgical precision, improving procedural consistency and outcomes.

Another defining trend is the shift toward minimally invasive and image-guided procedures. Hospitals increasingly favor robotic systems that reduce patient recovery time, lower complication rates, and enable complex interventions through smaller incisions. This shift aligns with value-based care models that prioritize clinical efficiency and long-term patient outcomes.

Platform modularity is also gaining traction. Manufacturers are designing scalable systems that allow hospitals to add capabilities incrementally, lowering entry barriers and extending system life cycles. Alongside this, cloud connectivity and data interoperability are expanding, enabling remote diagnostics, performance monitoring, and predictive maintenance.

The rise of specialized robotic systems tailored for orthopedics, urology, and soft-tissue surgery further reflects market segmentation. These focused solutions address workflow-specific demands while improving cost efficiency. Collectively, these trends are reshaping competitive dynamics and redefining how robotic surgery integrates into modern healthcare delivery.

What Are the Strongest Growth Drivers Shaping This Market Today?

"Technological Advancements and Development of Procedure-Specific Surgical Robotic System Is Anticipated to Drive the Market"

Recently, Intuitive Surgical Inc. received U.S. Food and Drug Administration approval for its Ion system. The robotic endoluminal system is designed to permit doctors to conduct minimally invasive biopsies deep within the lung. The development of procedure-specific robotic system is one of the major factor driving the growth of the market. The increasing preference of minimally invasive robotic-assisted surgery is one of the factors anticipated to drive the market growth.

Additionally, the increasing adoption and demand for surgical robots by medical professionals is expected to propel the growth of the market during the forecast period. However, the high cost of installation and lack of skilled professional are some of the factors that are likely to restrain this market’s growth to an extent.

The surgical robots market is being propelled by a convergence of clinical demand, technological advancement, and systemic healthcare transformation. A primary growth driver is the rising preference for minimally invasive procedures, which reduce surgical trauma, shorten recovery periods, and lower postoperative complication rates. These clinical advantages continue to influence hospital investment strategies and surgeon adoption patterns.

Demographic shifts further strengthen demand. Aging populations and the growing prevalence of chronic conditions such as cardiovascular disease, cancer, and degenerative joint disorders are increasing procedural volumes worldwide. Surgical robotics enables greater procedural precision in complex cases, supporting consistent outcomes across diverse patient profiles.

Technological innovation also plays a decisive role. Advances in robotic articulation, machine vision, and real-time data analytics are expanding the scope of robot-assisted procedures. Integration with artificial intelligence improves intraoperative decision support and enhances procedural consistency, reinforcing clinical confidence.

What are the key constraints and challenges?

The surgical robots market faces several structural and operational constraints that influence adoption pace and long-term scalability. High upfront capital investment remains a primary barrier, as advanced robotic platforms require substantial expenditure for acquisition, installation, and ongoing system upgrades. This cost burden limits accessibility for mid-sized hospitals and emerging healthcare systems, reinforcing market concentration among well-funded institutions.

Regulatory complexity also presents persistent challenges. Surgical robotic systems must meet stringent safety, cybersecurity, and performance standards across different jurisdictions. Lengthy approval cycles and evolving compliance frameworks can delay commercialization and increase development costs, particularly for newer entrants and smaller innovators.

Operational risks further constrain market expansion. Surgical robots demand specialized training, and the availability of skilled surgeons and technical staff remains uneven across regions. Inadequate training infrastructure can reduce utilization rates and affect procedural outcomes. Additionally, system interoperability issues with existing hospital infrastructure create integration challenges.

Data security and liability concerns are growing as robotic systems become more software-driven and connected. Cybersecurity vulnerabilities, data ownership questions, and accountability in case of system malfunction introduce legal and reputational risks. Collectively, these constraints require strategic investment, regulatory alignment, and workforce development to sustain long-term market growth.

How is the market segmented?

The surgical robots market is segmented across multiple dimensions that reflect differences in clinical use, purchasing behavior, and technology adoption. These segmentation layers reveal where value is being generated, how competitive intensity varies, and where future growth is most likely to emerge. Understanding these distinctions is essential for assessing market maturity, investment potential, and long-term scalability.

Segmentation by Application

Surgical robotics adoption varies significantly by clinical specialty, shaped by procedural complexity, reimbursement structures, and surgeon familiarity.

General Surgery remains the largest application segment. Procedures such as colorectal surgery, hernia repair, and bariatric interventions increasingly rely on robotic assistance to enhance precision and visualization. Hospitals favor robotic platforms that improve procedural consistency while reducing postoperative complications and length of stay.

Urology represents one of the most technologically mature segments. Robotic-assisted prostatectomies and kidney procedures have become standard in many advanced healthcare systems. High procedure volumes, strong clinical evidence, and established surgeon training pipelines support sustained adoption.

Gynecology continues to expand as robotic platforms enable minimally invasive hysterectomies and complex pelvic surgeries. Precision, ergonomics, and reduced blood loss remain key value drivers in this segment.

Orthopedic and spine surgery are emerging growth areas. Robotic assistance improves implant positioning accuracy and procedural planning, particularly in joint replacement and spinal alignment. Adoption is accelerating as systems demonstrate measurable outcome improvements.

Cardiothoracic and neurosurgical applications remain niche but expanding. High capital costs and specialized training requirements limit widespread use, yet technological advancements are gradually improving accessibility.

Segmentation by End User

Hospitals represent the dominant end-user segment, driven by their capital capacity, case volume, and ability to integrate robotic systems into complex surgical workflows. Large academic medical centers and tertiary hospitals lead adoption due to their focus on innovation, research, and specialized care.

Ambulatory surgical centers are emerging as a high-growth segment. As minimally invasive procedures shift toward outpatient settings, compact and cost-efficient robotic systems are gaining traction. These facilities prioritize operational efficiency, shorter procedure times, and rapid patient turnover.

Specialty clinics and private surgical centers contribute modest but growing demand, particularly in orthopedics and urology. Their adoption is influenced by reimbursement structures and local patient demographics.

Segmentation by Technology Architecture

Robotic systems vary significantly in design and technological architecture. Integrated systems that combine imaging, navigation, and instrument control are preferred for complex procedures requiring high precision. Modular platforms, which allow upgrades and customization, are increasingly favored by cost-conscious providers.

Open-console systems are gaining attention for improving surgeon ergonomics and team communication, while closed-console designs remain preferred for precision-intensive applications. Software-driven enhancements, including artificial intelligence–assisted navigation and data analytics, are becoming key differentiators.

The Ecosystem

Value creation in the surgical robots market extends beyond device sales. Recurring revenue from software updates, service contracts, instrument replacements, and training programs contributes significantly to long-term profitability. Manufacturers increasingly emphasize lifecycle value rather than upfront system pricing.

Hospitals derive value through improved surgical outcomes, reduced complication rates, and shorter hospital stays. These benefits translate into operational efficiencies and stronger patient satisfaction metrics. For payers, improved outcomes support cost containment and long-term care optimization.

From an innovation perspective, collaboration between robotics developers, healthcare providers, and academic institutions is accelerating product refinement. These partnerships enhance clinical validation, support regulatory approvals, and drive broader market acceptance.

To know how our report can help streamline your business, Speak to Analyst

Regional Analysis

The global surgical robots market displays significant regional variation shaped by healthcare infrastructure maturity, regulatory frameworks, reimbursement systems, and clinical adoption patterns. While adoption levels vary, each region contributes distinct growth drivers and innovation dynamics that collectively shape global market expansion.

"Increased Research and Development and Use of Surgical Robots for The Treatment of Cancer to Exhibit Highest CAGR in the Asia Pacific"

North America

North America generated maximum revenue of US$ 1,045.5 Mn in 2018 and is expected to dominate the surgical robots market throughout the forecast period. The American Heart Association, in its publication Heart Disease and Stroke Statistics, 2016, estimated that 98 million American adults are suffering from different types of cardiovascular diseases. The increasing number of cardiovascular disease is anticipated to increase demand for minimally invasive surgeries, subsequently giving rise to demand for the robotic surgical systems in the region.

North America remains the most mature and technologically advanced regional market. High healthcare expenditure, early adoption of minimally invasive surgery, and strong reimbursement frameworks support sustained demand. The United States accounts for the majority of regional revenue due to extensive hospital networks and established robotic surgery programs. Canada follows with steady uptake, driven by public healthcare investments and expanding surgical automation initiatives. The region benefits from close collaboration between manufacturers, academic institutions, and healthcare providers.

The Asia Pacific is anticipated to grow at a significantly higher CAGR during the forecast period. The increased research and development and use of surgical robots for the treatment of cancer and other oncology segment are some of the major factors anticipated to drive the growth of the surgical robot’s market in the Asia Pacific. Europe is projected to lose market share during 2019-2026, while Middle East & Africa is projected to gain market share during the forecast period. Latin America is poised to register moderate growth during 2019-2026.

Asia-Pacific is the fastest-growing regional market, fueled by expanding healthcare infrastructure, rising surgical volumes, and increasing investment in medical technology. Japan remains a technological leader, leveraging advanced robotics expertise and strong government backing. China is rapidly scaling deployment across tertiary hospitals, supported by domestic manufacturing and favorable policy incentives. India and Southeast Asia present high-growth potential, driven by rising healthcare demand and expanding private hospital networks.

Europe

Europe represents a diversified and steadily expanding market. Western European countries lead adoption, supported by strong clinical research infrastructure and regulatory clarity. Germany and the United Kingdom drive regional growth through hospital modernization initiatives and increasing acceptance of robotic-assisted surgery. Southern and Eastern European markets show gradual uptake as cost barriers decline and training infrastructure improves. Regulatory harmonization across the European Union continues to shape procurement strategies and innovation pathways.

Latin America

Latin America represents an emerging opportunity characterized by gradual adoption of surgical robotics in urban healthcare centers. Brazil and Mexico lead regional uptake, supported by private hospital investments and growing awareness of minimally invasive procedures. Budget constraints and uneven access remain challenges, but ongoing healthcare modernization programs are improving market accessibility.

Middle East and Africa

The Middle East and Africa region shows selective but increasing adoption. Gulf countries invest heavily in advanced healthcare infrastructure, positioning robotic surgery as part of national modernization strategies. In contrast, adoption across Africa remains limited due to infrastructure and cost barriers, though pilot programs in leading medical centers indicate long-term potential.

Across all regions, regulatory clarity, surgeon training capacity, and reimbursement alignment remain decisive factors influencing adoption pace. Regional disparities persist, yet the overall trajectory indicates broadening global acceptance and deeper integration of robotic surgery into mainstream clinical practice.

How competitive is the market?

The surgical robots market exhibits a moderately concentrated competitive structure, defined by a small group of global leaders and a growing ecosystem of specialized innovators. Market leadership is anchored by established manufacturers with broad product portfolios, strong intellectual property positions, and long-standing relationships with hospital systems. These players benefit from scale advantages, regulatory experience, and deep integration into clinical workflows, which collectively raise entry barriers for new participants.

Competition increasingly centers on technological differentiation rather than hardware alone. Leading vendors compete on system precision, ergonomic design, software intelligence, and procedural versatility. Continuous upgrades in imaging integration, artificial intelligence–enabled assistance, and data analytics have become central to maintaining competitive relevance. Vendors are also prioritizing modular system architectures to allow hospitals to expand capabilities without replacing entire platforms.

Mid-sized and emerging companies are carving positions through specialization. Many focus on niche surgical indications, cost-efficient platforms, or portable systems designed for ambulatory and outpatient settings. These firms often emphasize agility, faster innovation cycles, and targeted clinical outcomes to offset the scale advantages of larger incumbents. Strategic partnerships with academic hospitals and regional distributors are common routes to market penetration.

Competition increasingly extends beyond hardware into ecosystems. Software updates, data analytics platforms, surgeon training ecosystems, and long-term service agreements now play decisive roles in vendor selection. As hospitals evaluate total cost of ownership rather than upfront system pricing, lifecycle value has become a central differentiator.

Mergers, acquisitions, and strategic alliances remain frequent as companies seek to broaden technology portfolios, access new geographies, and accelerate regulatory pathways. Overall, the competitive environment continues to intensify, driven by innovation speed, clinical evidence generation, and the ability to demonstrate measurable procedural and economic value.

Key Market Players

"Intuitive Surgical Inc. accounted for Highest Market Share in Terms of Revenue in 2018"

Intuitive Surgical Inc., is a leading player as per the market report. Intuitive Surgical Inc. is likely to retain its position during the forecast period owing to its diversified product portfolio and strong distribution network globally. In order to strengthen the market position, key surgical robots market players are focusing the introduction of the procedure specific robotic system. Other players operating in the global surgical robot’s market are Medtronic, Stryker, Smith & Nephew, Zimmer Biomet.

What role do innovation and emerging technologies play in shaping future growth?

Innovation remains the primary catalyst reshaping the surgical robots market, with technology advancement directly influencing adoption rates, clinical outcomes, and competitive positioning. Artificial intelligence is increasingly embedded within robotic platforms to support intraoperative guidance, tissue differentiation, and adaptive motion control. These capabilities enhance precision, reduce variability across procedures, and support surgeon decision-making in complex environments.

Advancements in machine vision and sensor fusion are also expanding the functional scope of robotic systems. Enhanced imaging integration enables real-time visualization of anatomical structures, improving accuracy during minimally invasive procedures. Cloud-enabled architectures now allow remote performance monitoring, predictive maintenance, and software updates, extending system lifecycles and reducing downtime.

Robotic platforms are increasingly designed around modular architectures. This approach allows healthcare providers to scale functionality over time, adopt new tools without full system replacement, and tailor capabilities to specific procedural needs. Such flexibility is particularly valuable in cost-sensitive healthcare systems.

Emerging technologies such as haptic feedback, digital twins, and simulation-based training are reshaping surgeon education and proficiency development. These tools shorten learning curves and support standardized procedural outcomes. Combined, these innovations are accelerating clinical acceptance, supporting broader procedural adoption, and strengthening the long-term growth trajectory of the surgical robotics market.

What are the opportunities for growth?

Growth opportunities within the surgical robots market are increasingly concentrated in areas where unmet clinical needs intersect with operational efficiency gains. One of the most compelling opportunities lies in expanding robotic adoption beyond tertiary hospitals into ambulatory surgical centers and regional healthcare facilities. These settings seek compact, cost-efficient systems that support high procedure volumes without complex infrastructure requirements.

Emerging economies represent another high-potential avenue. Improving healthcare infrastructure, rising surgical demand, and supportive government initiatives are creating favorable conditions for robotic system adoption. Manufacturers that adapt pricing models, training programs, and service support to local market conditions are better positioned to scale in these regions.

Procedure-specific robotics presents further opportunity. Systems designed for orthopedics, soft tissue surgery, and minimally invasive interventions continue to attract investment due to strong clinical demand and clear efficiency benefits. Additionally, the integration of robotics with digital health platforms opens pathways for data-driven optimization, remote monitoring, and outcome-based care models.

Strategic partnerships across the healthcare ecosystem spanning device manufacturers, software developers, and care providers are increasingly important. These collaborations accelerate innovation, reduce development risk, and improve time to market. As value-based healthcare expands, solutions that demonstrate measurable clinical and economic benefits are likely to command sustained investor and customer interest.

High investment by market players in the development of the procedure specific surgical robotic system is one of the major factors driving the growth of the global surgical robot’s market. Increasing cardiovascular diseases and increased demand for minimally invasive surgeries are also some of the major factors propelling the growth of the global market during the forecast period.

The surgical robots market report provides qualitative and quantitative insights on the surgical robots industry trends and detailed analysis of surgical robots industry size and growth rate for all possible segments in the market. The market is segmented by application and end user. On the basis of product, the market is segmented into general surgery, gynecology, urology, orthopedics, and others. On the basis of the end user, the surgical robots market is categorized into hospitals, ambulatory surgery centers, and others. Geographically, the market is segmented into five major regions, which are North America, Europe, Asia Pacific, and Rest of World. The regions are further categorized into countries.

Along with this, the report analysis includes market dynamics and competitive landscape. Various key insights provided in the report are the prevalence of key disease, by region; pricing analysis, key players; technology advances in medical robotic systems; key mergers and acquisitions; new product launches; among others.

Market Segments

ATTRIBUTE

DETAILS

By Application

General Surgery

Gynecology

Urology

Orthopedics

Others

By End User

Hospitals

Ambulatory Surgery Centers

Others

By Geography

North America (USA and Canada)

Europe (UK, Germany, France, Italy, Spain, Scandinavia and Rest of Europe)

Asia Pacific (Japan, China, India, Australia, Southeast Asia and Rest of Asia Pacific)

According to Fortune Business Insights, the global surgical robots market size was valued at USD 18.36 billion in 2026, projected to reach USD 59.36 billion by 2034 at a CAGR of 15.80% during 2026–2034.

Surgical robots are widely used in general surgery, gynecology, urology, and orthopedics. The gynecology segment is projected to hold a significant market share during the forecast period.

Technological advancements, development of procedure specific surgical robots and application for treatment of cancer and new product launches will drive the growth of the market.

Increased technological advancements, development of procedure specific surgical robots, increased safety, increasing applications and new product launches would drive the adoption.

Adoption of advanced surgical robots, safer surgical robots, and new launches of products, advances in R&D leading to significant improvement of technological features and new applications, and increased awareness regarding precision of surgical robots are the hyper-market trends.

Seeking Comprehensive Intelligence on Different Markets?Get in Touch with Our Experts

Speak to an Expert

The global surgical robots market size is valued at USD 18.36 billion in 2026, projected to reach USD 59.36 billion by 2034 at a CAGR of 15.80% during 2026–2034.