Unconventional Gas Market Size, Share & Industry Analysis, By Type (Shale Gas, Tight Gas, and Coal Bed Methane), By Application (Power Generation, Industrial, Commercial, and Others), and Regional Forecast, 2026-2034

Unconventional Gas Market Size and Future Outlook

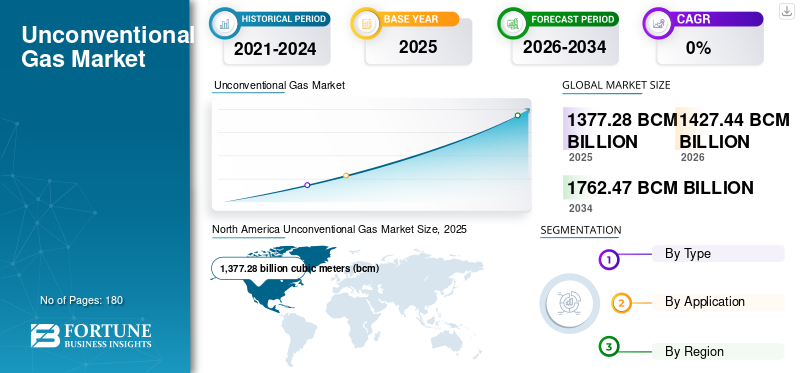

The global unconventional gas market size was valued at 1,377.28 billion cubic meters (bcm) in 2025. The market is projected to grow from 1,427.44 billion cubic meters (bcm) in 2026 to 1,762.47 billion cubic meters (bcm) by 2034, exhibiting a CAGR of 2.67% during the forecast period.

The production of unconventional gas has become a critical driver of global natural gas supply, primarily due to its role in energy security and production resilience. In the U.S., shale gas accounted for nearly 78% of total dry natural gas production in 2023, transforming the country into the world’s largest gas producer and a major LNG exporter. China has also accelerated development, producing over 25 bcm of shale gas annually, supported by state-led investment to reduce import dependence. Additionally, large-scale tight gas projects in the Middle East, such as Saudi Arabia’s Jafurah field (targeting ~2 Bcf/d by 2030), are reshaping regional gas supply. Such gases are produced from tight formations using advanced techniques such as hydraulic fracturing and horizontal drilling to unlock trapped hydrocarbons.

- For instance, in February 2024, Saudi Aramco announced major progress on its Jafurah unconventional tight gas project, awarding over USD 25 billion in engineering, procurement, and construction contracts as part of Phase 1 development. Jafurah is expected to produce around 2 billion cubic feet per day (Bcf/d) of sales gas by 2030, making it one of the world’s largest unconventional gas developments. The project highlights the growing role of such gas in meeting domestic power and industrial demand while reducing reliance on oil-fired generation.

Some of the leading companies operating in the exploration and production of such gases in the industry include ExxonMobil, Chevron, ConocoPhillips, and EOG Resources, among others. ExxonMobil is a leading global player in the market, with major shale gas operations in the U.S., particularly in the Permian Basin, Marcellus, and Haynesville plays. The company leverages large-scale horizontal drilling and advanced completion technologies to enhance recovery. ExxonMobil also integrates unconventional gas into its LNG supply chain, supporting export-oriented growth and long-term energy security.

Download Free sample to learn more about this report.

UNCONVENTIONAL GAS MARKET TRENDS

Expansion of Large-Scale Tight Gas Projects Outside North America is Key Market Trends

The expansion of large-scale tight gas projects outside North America reflects a strategic shift by energy-importing regions to strengthen domestic gas supply and energy security. Countries in the Middle East and Asia are investing heavily in tight gas resources to offset declining conventional reserves and reduce reliance on LNG imports. For example, Saudi Arabia’s Jafurah field is one of the world’s largest tight gas developments, with planned output of around 2 Bcf/d by 2030, supporting power generation, industrial use, and hydrogen production. Similarly, Oman’s Khazzan and Ghazeer fields have demonstrated that tight gas can be produced economically outside the U.S. with advanced drilling and completion technologies.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Infrastructure Expansion and Improved Monetization to Drive Market Growth

A key driver for these resources is the rapid expansion of supporting infrastructure, which has significantly improved the ability to monetize production. Investments in gas processing plants, pipeline networks, and LNG export facilities have reduced bottlenecks that previously constrained unconventional output. In several regions, new transmission pipelines are enabling gas to move from inland shale and tight gas basins to demand centers, power plants, and export terminals. Additionally, the growth of LNG liquefaction capacity has created international outlets for surplus unconventional gas, improving price realization and project economics.

MARKET RESTRAINTS:

Environmental and Regulatory Constraints to Hamper Market Demand

A major restraint on these industries is the growing environmental and regulatory scrutiny associated with shale, tight gas, and coalbed methane operations. Concerns related to water usage, wastewater disposal, induced seismicity, and methane emissions have led to stricter permitting requirements and, in some regions, outright bans on hydraulic fracturing. Several European countries have limited or suspended unconventional gas development due to public opposition and environmental considerations. In addition, increasingly stringent methane emission regulations and monitoring requirements raise compliance costs for operators, particularly in mature basins.

MARKET OPPORTUNITIES

Gas-to-Power, LNG Expansion, and Emerging Low-Carbon Applications to Present Excellent Market Opportunities

The market presents significant opportunities driven by expanding gas-to-power projects, LNG capacity additions, and emerging low-carbon applications. Rapid growth in electricity demand across developing regions is increasing reliance on gas-fired power plants, creating a stable long-term demand for such gas supply. At the same time, new LNG liquefaction terminals and export infrastructure are opening international markets for gas produced from shale and tight formations, improving price realization and market diversification. It is also increasingly used as a feedstock for blue hydrogen production, where carbon capture can reduce lifecycle emissions, and in petrochemical manufacturing, supporting unconventional gas market growth.

MARKET CHALLENGES

Cost Volatility and Operational Complexity in Gas Development Present Significant Challenges

One of the key challenges facing the development of unconventional gas is cost volatility combined with operational complexity. Development of shale, tight gas, and coalbed methane resources requires intensive drilling programs, advanced completion techniques, and continuous capital investment to offset rapid production decline rates. Fluctuations in drilling, service, and labor costs can significantly impact project economics, particularly during periods of inflation or supply chain disruption.

Segmentation Analysis

By Type

Shale Gas is Dominant Owing to High Productivity and Extensive Infrastructure

Based on type, the market is classified into shale gas, tight gas, and coal bed methane.

In 2025, shale gas dominated the market share. Shale gas accounted for the largest unconventional gas market share primarily due to its high productivity, scalability, and well-established infrastructure. Large shale basins benefit from advanced horizontal drilling and multi-stage hydraulic fracturing, enabling high initial production rates and rapid development at scale. In addition, extensive pipeline networks, gas processing capacity, and LNG export facilities allow shale gas to reach domestic and international markets efficiently.

The tight gas segment is experiencing significant growth and is expected to grow at a CAGR of 4.17%.

To know how our report can help streamline your business, Speak to Analyst

By Application

Power Generation is Dominant Owing to Reliable and Flexible Electricity Supply

Based on application, the market is classified into power generation, industrial, commercial, and others.

In 2025, the power generation segment dominated the global market. Power generation is the dominant application as it provides a reliable, flexible, and cost-competitive fuel source for electricity production. Gas-fired power plants can ramp output quickly, making them well-suited to balance intermittent renewable energy sources such as wind and solar. It has significantly increased gas availability in many regions, supporting a shift away from coal and oil in power generation while maintaining grid stability.

The industrial segment is expected to grow at a CAGR of 2.70%.

Unconventional Gas Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America held the highest share in 2025, valued at 1,032.80 billion cubic meters (bcm), and also took a significant share in 2026 with 1,066.32 billion cubic meters (bcm). North America is dominant in the market due to its early technology adoption, vast resource base, and mature infrastructure. The U.S. alone accounts for the majority of global output, with shale gas contributing nearly 78% of total U.S. dry natural gas production in 2023, driven by prolific basins such as the Permian, Marcellus, and Haynesville. Canada further strengthens regional dominance through large-scale tight gas and shale production in the Montney and Duvernay formations. The region benefits from extensive pipeline networks, gas processing capacity, and LNG export terminals, enabling efficient monetization of production.

North America Unconventional Gas Market Size, 2025 (Billion Cubic Meters (bcm))

To get more information on the regional analysis of this market, Download Free sample

U.S. Unconventional Gas Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market analytically approximated at around 915.80 billion cubic meters (bcm) in 2025, accounting for roughly 66.49% of the global market size.

Europe

Europe is projected to record a growth rate of 2.07% in the coming years and reportedly reach a valuation of 27.06 billion cubic meters (bcm) by 2025. Europe plays a limited but strategic role in the market due to regulatory constraints, environmental concerns, and public opposition to hydraulic fracturing. While the region holds technically recoverable shale and tight gas resources, commercial production remains minimal and is largely concentrated in parts of Eastern Europe. Most European countries rely on assessments rather than large-scale development, focusing instead on imports and energy diversification.

Ukraine Unconventional Gas Market

The Ukraine market size in 2025 was recorded to be around 15.30 billion cubic meters (bcm) and is estimated at around 15.84 billion cubic meters (bcm) in 2026, representing roughly 1.11% of the global revenues.

Asia Pacific

Asia Pacific reached 177.53 billion cubic meters (bcm) in 2025 and secured the second-largest position in the market. In the region, India and China both reached 9.35 billion cubic meters (bcm) and 131.11 billion cubic meters (bcm), respectively, in 2025.

Asia Pacific represents a growing region in the market, driven by efforts to enhance energy security and reduce dependence on imports. China dominates regional activity with commercial shale gas, tight gas, and coalbed methane production supported by state-led investment. Australia contributes through large-scale coal seam gas production linked to LNG exports, while countries such as India and Indonesia continue to develop CBM resources.

Indonesia Unconventional Gas Market

The Indonesia market size in 2025 is estimated at around 6.35 billion cubic meters (bcm), accounting for roughly 0.46% of the global revenues.

Indonesia is developing coalbed methane resources to support domestic gas supply and reduce reliance on conventional gas imports.

China Unconventional Gas Market

China’s market is projected to be significant worldwide, with 2025 revenues recorded at around 131.11 billion cubic meters (bcm), representing 9.52% of the global market.

India Unconventional Gas Market

The Indian market value in 2025 was recorded at around 9.35 billion cubic meters (bcm), accounting for 0.68% of the global revenues.

Latin America

Latin America is expected to witness moderate growth in this market space during the forecast period. The Latin America market reached a valuation of 48.42 billion cubic meters (bcm) in 2025.

Latin America’s market is largely driven by Argentina, where shale gas production from the Vaca Muerta formation has transformed regional supply dynamics. The country has significantly increased domestic gas output, reducing import dependence, supporting power generation and industrial demand.

Argentina Unconventional Gas Market

Argentina's market was valued at around 41.06 billion cubic meters (bcm) in 2025, representing roughly 2.98% of the global market.

Middle East & Africa

The Middle East & Africa are expected to witness significant growth in this market space during the forecast period. The Middle East & Africa market reached a valuation of 91.46 billion cubic meters (bcm) in 2025. Further, the region is emerging in development, led by large-scale tight gas projects in the GCC, while activity in Africa remains limited and largely at the exploratory stage.

GCC Unconventional Gas Market

The GCC market was valued at around 65.98 billion cubic meters (bcm) in 2025, representing roughly 4.79% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Vendors Actively Expanding Market Share via Partnerships, Business Expansion, and Technological Advancements

The global market holds a consolidated market structure, constituting prominent players such as ExxonMobil, Chevron, ConocoPhillips, and EOG Resources, among others. Companies operating in the industry are adopting targeted growth strategies focused on strengthening their product portfolio, technical capability, expanding manufacturing presence, and other areas.

- For instance, in June 2025, Saudi Aramco provided an update on the phased development of its Jafurah unconventional gas field, highlighting progress in drilling and surface facility construction. The company reiterated that Jafurah will supply gas for power generation, industrial use, and future low-carbon initiatives. Aramco positioned such gases as a long-term pillar of Saudi Arabia’s domestic energy transition strategy.

Other key players in the global market include Pioneer Natural Resources, CNPC (PetroChina), Sinopec, and Saudi Aramco, among others. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY UNCONVENTIONAL GAS COMPANIES PROFILED

- ExxonMobil (U.S.)

- Chevron (U.S.)

- ConocoPhillips (U.S.)

- EOG Resources (U.S.)

- Pioneer Natural Resources (U.S.)

- CNPC (PetroChina) (China)

- Sinopec (China)

- Saudi Aramco (Saudi Arabia)

- YPF (Argentina)

- BP (U.K.)

KEY INDUSTRY DEVELOPMENTS

- February 2025: BP highlighted the stable performance of its unconventional tight gas operations in Oman, including the Khazzan and Ghazeer fields. The company emphasized operational reliability and production efficiency in supplying gas to domestic power and industrial sectors. BP noted that large-scale tight gas projects remain a strategic example of successful unconventional gas development outside North America.

- October 2024: CNPC reported progress in expanding gas production in China, with continued shale gas development in the Sichuan Basin and tight gas output growth in the Ordos Basin. The company emphasized advancements in drilling and fracturing technologies tailored to complex geological conditions. CNPC highlighted unconventional gas as central to China’s strategy to enhance domestic gas supply and reduce import dependence.

- August 2024: Pioneer Natural Resources discussed the role of associated unconventional gas production from its Permian Basin shale operations. The company emphasized coordination between oil and gas development to ensure efficient gas handling and takeaway. Pioneer highlighted infrastructure investments as a key factor in managing gas volumes and maintaining production reliability across its unconventional resource base.

- May 2024: Sinopec announced continued stable production from its major shale gas projects, including the Fuling shale gas field. The company focused on improving recovery efficiency and lowering development costs through technology upgrades. Sinopec emphasized that unconventional gas supports regional energy security and plays an increasing role in meeting industrial and power sector gas demand in China.

- April 2024: Chevron reported steady output from its Permian Basin operations, supported by disciplined drilling activity and infrastructure readiness. The company focused on reducing methane emissions and flaring across its shale assets while maintaining a reliable gas supply for domestic use. Chevron highlighted unconventional gas as an important component of its North American portfolio, particularly in supporting flexible power generation and LNG-linked demand.

REPORT COVERAGE

The global unconventional gas market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and the market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 2.67% from 2026 to 2034 |

| Unit | Volume (Billion Cubic Meters (bcm)) |

| Segmentation | By Type, Application, and Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at 1,377.28 billion cubic meters (bcm) in 2025 and is projected to reach 1,762.47 billion cubic meters (bcm) by 2034.

In 2025, the market value stood at 1,032.80 billion cubic meters (bcm).

The market is expected to exhibit a CAGR of 2.67% during the forecast period.

The shale gas segment led the market by type.

Key factors driving the market include rising energy security needs, growing power generation demand, expansion of gas infrastructure and LNG capacity, technological advancements in drilling and completions, and the shift toward cleaner fuels to replace coal.

ExxonMobil, Chevron, ConocoPhillips, and EOG Resources, among others are some of the prominent players in the market.

North America dominated the market in 2025.

Major factors expected to favor product adoption include increasing electricity demand, coal-to-gas substitution, improved drilling and completion technologies, expanding LNG export infrastructure, and government support for domestic gas production.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us