Urinary Incontinence Devices Market Size, Share & Industry Analysis By Product Type (Absorbents [Underwear & Briefs, Pads & Guards, Drip Collectors & Bed Protectors] and Non-Absorbents [Urethral Inserts, Slings, Catheters, Stimulation Devices, Drainage Bags, and Others]), By Gender (Male and Female), By Usage (Reusable and Disposable), By End User (Hospitals & ASCs, Clinics, Homecare Settings, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

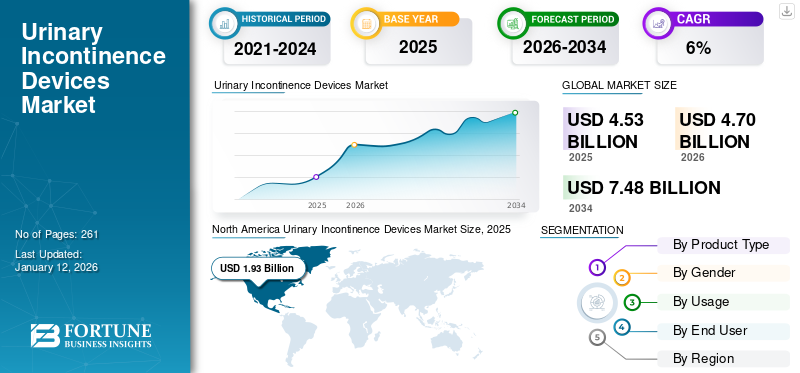

The global urinary incontinence devices market size was valued at USD 4.53 billion in 2025 and is projected to grow from USD 4.7 billion in 2026 to USD 7.48 billion by 2034, exhibiting a CAGR of 6.00% during the forecast period. North america dominated the urinary incontinence devices market with a market share of 42.50% in 2025.

Urinary incontinence devices prevent the leakage of urine, improve comfort, and increase mobility and independence among the general population. The rising risk of diabetes, obesity, and other diseases is increasing the number of cases of urinary incontinence among the patient population. The growing number of urinary incontinence cases, combined with rising awareness about the benefits of absorbents and non-absorbent products, results in the increasing penetration rate of these devices.

- For instance, according to the 2025 data published by ScienceDirect, in Europe about 40% of the population is suffering from urinary incontinence.

Moreover, the efforts toward guidelines and strategies among governmental organizations to raise public and professional awareness, along with the provision of financial assistance for continence products, support product adoption. This, along with key players including Coloplast A/S, Convatec Inc., Essity Aktiebolag, and others, focus on R&D initiatives on developing and introducing novel products.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Increasing Prevalence of Acute and Chronic Conditions Boost Market Growth

The growing prevalence of acute and chronic conditions, including urinary tract infections, diabetes, neurological disorders, and others amongst the patient population, is expected to drive the number of cases of urinary incontinence.

- For instance, according to the 2025 data published by the National Center for Biotechnology Information (NCBI), it was reported that the prevalence of urinary incontinence was around 32.4%.

Furthermore, the growing aging population is also a crucial contributing factor in increasing the number of patients affected by urinary incontinence. According to the 2024 statistics published by the World Health Organization (WHO), it was reported that 1 in 6 people is expected to be aged 60 years and above by 2030 globally.

Therefore, the growing prevalence of various types of urinary incontinence, such as urge incontinence, and others, along with increasing awareness about the benefits of these products, is likely to drive the focus of key players toward R&D activities to launch innovative products.

Other Prominent Drivers

- Higher awareness & reduced stigma: Increasing education, awareness, and destigmatization of incontinence encourages people to seek treatment and device solutions.

- Better reimbursement / regulatory support: Expanding insurance coverage, favorable reimbursement policies, and codes in some markets help adoption.

Market Restraints

Limited Diagnosis and Reimbursement Policies in Developing Nations to Hamper Product Adoption

Chronic conditions such as urinary tract infections and neurological disorders can lead to urinary incontinence. Globally, various governmental and non-governmental organizations are constantly implementing strategies to promote awareness about the benefits of early diagnosis.

However, despite the efforts of these organizations, there is a growing prevalence of delayed diagnosis of various chronic conditions owing to delayed referrals of patients with chronic conditions, along with limited expertise among healthcare providers to identify chronic disorders, especially in emerging countries.

Lack of clinical awareness and limited reimbursement policies, among others, delay specialist care, leading to postponed diagnosis, especially in Brazil, China, and India, among other developing countries.

- For instance, the Brazilian Public Health System does not cover pharmacotherapy for urge urinary incontinence (UUI) in Brazil.

Therefore, the above mentioned factors and the lack of favorable reimbursement policies for patients with chronic conditions are primarily responsible for the limited diagnosis and treatment rates, resulting in a reduced penetration rate of these products.

Market Opportunities

Increasing Technological Advancements among Key Players Boost Market Opportunities

Increasing technological advancements in the absorbent and non-absorbent products are reshaping the industry. Integration of smart sensors, mobile apps for tracking and management, improved non-invasive neuromodulation devices such as sacral nerve stimulation and tibial nerve stimulation, and others is reducing complications and improving the overall patient experience. The increasing number of benefits of these devices is supporting the demand, driving the focus of key players toward R&D activities to develop and introduce novel products.

- In February 2025, UroMems announced that the entire treatment cohort in the clinical feasibility study in female patients of UroActive Smart Implants for stress urinary incontinence treatment had successfully reached the six-month primary endpoints.

Market Challenges

High Cost Associated with Advanced Devices to Limit Market Growth

There is an increasing demand for advanced devices for the management of urinary incontinence. However, the high cost associated with these devices is significantly impacting accessibility and adoption, especially in emerging countries. The advanced products, including smart sensor-embedded wearable devices, stimulation devices, among others, are resulting in the increasing cost associated with these devices, thereby hampering the urinary incontinence devices market growth.

- For instance, the cost of urinary incontinence slings ranges from USD 10.0 to over USD 10,000.0.

Other Prominent Challenges

- Risks/complications: Implant devices can lead to complications such as infection, erosion, and mechanical failure, which may deter adoption.

- Device failure/leakage/durability issues: Failures or malfunctions can erode patient confidence and market reputation.

- Regulatory hurdles/approval timelines: Medical devices require rigorous safety/efficacy testing and regulatory approvals, which slows time to market.

- Competition from alternative treatments: Non-device treatments, such as behavioral therapy and pharmacological therapies, may compete with device adoption.

Urinary Incontinence Devices Market Trends

Shifting Preference toward Minimally Invasive Surgeries to Fuel Product Demand

There is an increasing preference toward minimally invasive surgical procedures owing to faster recovery, limited pain, shorter hospital stays, and other benefits. The shift is primarily attributed to technological advancements in surgical tools, rising availability of robotic-assisted platforms, and improved biomaterials, which are increasing the number of treatment options.

- According to a 2024 study published by the International Continence Society, it was reported that the mid-urethral sling insertion, a minimally invasive therapy, showed reduced post-surgery reoperation rates of 0.8% at 1 year and 2.7% at 5 years among patients.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Product Type

Increasing Number of Product Launches and Discreet Management Boosts Absorbents’ Demand

Based on product type, the market is bifurcated into absorbents and non-absorbents. Additionally, absorbents are further classified into underwear & briefs, pads & guards, and drip collectors & bed protectors. Furthermore, the non-absorbents are divided into urethral inserts, slings, catheters, stimulation devices, drainage bags, and others.

To know how our report can help streamline your business, Speak to Analyst

The absorbents segment is projected to dominate the market with a share of 67.02% in 2026. Absorbents, including underwear & briefs, and others, provide discreet management for urine leakage, provision of efficient absorption, and others among the patient population. This results in growing focus of key players toward R&D activities to develop and introduce novel products.

- In January 2021, Essity Aktiebolag launched TENA Silhouette Washable Absorbent Underwear for urinary incontinence and menstruation with an aim to strengthen its product portfolio globally.

By Gender

Increasing Prevalence of Urinary Incontinence Among Females Support Segment’s Growth

Based on gender, the market is classified into male and female.

The female segment is anticipated to hold a dominant market share of 64.89% in 2026. The segment’s leading market share is attributed to its increasing prevalence of urinary incontinence among the female population, resulting in rising demand. This, along with the growing focus of key players toward incorporating technological advancements in these devices, supports segmental growth.

- For instance, according to 2025 statistics published by Phoenix Physical Therapy, PLC, it was reported that one in four women over the age of 18 experiences some form of urinary incontinence in the U.S.

The male segment is expected to grow at a CAGR of 4.9% over the forecast period.

By Usage

Increasing Product Launches for Disposable Products Contributes to its Leading Position

On the basis of usage, the market is segmented into reusable and disposable.

The disposable segment is projected to dominate the market with a share of 58.30% in 2026. The growth is primarily attributed to the rising prevalence of various forms of urinary incontinence. Furthermore, the increasing number of major players emphasizing the development and introduction of disposable devices, supports the segment’s future growth.

- In October 2023, Friends, a brand of Nobel Hygiene Pt Ltd., launched the slim disposable absorbent underpant – Friends UltraThinz, designed for younger consumers who suffer from light urinary incontinence.

The reusable segment is set to flourish with a growth rate of 5.4% over the forecast period.

By End user

Increasing Preference towards Homecare Settings Led to the Segment’s Dominance

Based on end user, the market is sub-segmented into hospitals & ASCs, clinics, homecare settings, and others.

The home care settings segment dominated the market in 2025 owing to a rapid shift of patients toward home care settings, especially in developed countries, along with adequate reimbursement policies. The segment’s anticipated market share for 2026 is 44.47%.

- In October 2024, Home Health Care News reported that about 95% of respondents prefer in-home care treatment over the traditional hospital setting in the U.S.

The hospitals & ASCs segment is projected to grow at a CAGR of 5.7% during the study period.

Urinary Incontinence Devices Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Urinary Incontinence Devices Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America contributed approximately USD 1.93 billion to the global market in 2025, accounting for 42.50% share, and is expected to reach USD 2 billion in 2026. Increasing prevalence of urinary incontinence, adequate reimbursement policies, growing technological advancements, and rising number of product launches, among other factors support the region’s growth. In 2026, the U.S. market is estimated to reach USD 1.84 billion.

- For instance, in March 2025, Uresta, a female-owned health startup, received USD 3.0 million in funding from BDC Capital with an aim to develop non-invasive solutions for urinary incontinence.

Europe

In 2025, the Europe market stood at USD 1.31 billion, representing 28.90% of global demand, and is projected to grow to USD 1.36 billion in 2026, owing to the growing number of acquisitions and mergers among key players. Backed by these factors, the U.K. is expected to record the valuation of USD 0.26 billion, Germany USD 0.32 billion in 2026 and France USD 0.22 billion in 2025.

Asia Pacific

The Asia Pacific region captured 20.70% of the global market in 2025, generating USD 0.94 billion in revenue, and is projected to reach USD 0.97 billion in 2026. India is estimated to reach USD 0.15 billion while China is estimated to reach USD 0.33 billion and Japan is estimated to reach USD 0.26 billion in 2026.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa would witness moderate growth. In 2025, Middle East & Africa generated USD 0.13 billion, contributing 2.90% to global market revenue, and is projected to grow to USD 0.14 billion in 2026. Latin America recorded a market size of USD 0.22 billion in 2025, capturing 2.90% of the global market share, and is projected to reach USD 0.23 billion in 2026, owing to the rising prevalence of urinary incontinence and demand for advanced products. In the Middle East & Africa, GCC is set to attain the value of USD 0.05 billion in 2025.

Competitive Landscape

Key Industry Players

Increasing Number of Product Launches among Prominent Players Support Their Dominance

A robust and diversified product portfolio of novel urinary incontinence devices, along with a strong geographical presence, is one of the major factors supporting the dominance of key players. Essity Aktiebolag, Medtronic, and Coloplast A/S are prominent players in the industry. The growing emphasis of key players on receiving product approvals for incontinence care products contributes to the market share.

- In September 2025, Medtronic received U.S. FDA approval for its Altaviva device, a minimally invasive neuromodulation therapy for the treatment of urge urinary incontinence.

Other renowned players, including Teleflex Incorporated and BD are also growing owing to their growing initiatives toward collaborations to strengthen their brand presence.

List of Key Urinary Incontinence Devices Companies Profiled

- Coloplast A/S (Denmark)

- Braun SE (Germany)

- BD (U.S.)

- Essity Aktiebolag (Sweden)

- Teleflex Incorporated (U.S.)

- Medtronic (Ireland)

- Convatec Inc. (U.K.)

- Hollister Incorporated (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Boston Scientific Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2025 – Neuspera Medical received U.S. FDA approval for its sacral neuromodulation (iSNM) system for the treatment of patients with urge urinary incontinence (UUI) with an aim to strengthen its product portfolio.

- March 2025 – Caldera Medical acquired Ethicon’s GYNECARE TVT family of products with an aim to develop innovative treatment for stress urinary incontinence among patients.

- September 2024 – Medline Industries LP, launched a new wetness-sensing technology that combines special briefs, a sensor pod, and real-time alerts to provide data for the management of incontinence among the patient population. This helped in increasing the brand's presence globally.

- September 2022 – Attindas Hygiene Partners Group launched its novel adult disposable incontinence underwear product in North America with an aim to strengthen its presence.

- May 2021 – Zorbies launched new washable, reusable incontinence underwear for women with expanded coverage and absorbency, with an aim to widen its product portfolio.

REPORT COVERAGE

The market report provides a detailed global urinary incontinence devices market analysis and focuses on key aspects such as leading companies, product type, gender, usage, and end user of the product. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.0% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Gender, Usage, End User, and Region |

|

By Product Type |

· Absorbents o Underwear & Briefs o Pads & Guards o Drip Collectors & Bed Protectors · Non-Absorbents o Urethral Inserts o Slings o Catheters o Stimulation Devices o Drainage Bags o Others |

|

By Gender |

· Male · Female |

|

By Usage |

· Reusable · Disposable |

|

By End User |

· Hospitals & ASCs · Clinics · Homecare Settings · Others |

|

By Region |

· North America (By Product Type, Gender, Usage, End User, and Country) o U.S. (By Usage) o Canada (By Usage) · Europe (By Product Type, Gender, Usage, End User, and Country/Sub-region) o U.K. (By Usage) o Germany (By Usage) o France (By Usage) o Italy (By Usage) o Spain (By Usage) o Scandinavia (By Usage) o Rest of Europe (By Usage) · Asia Pacific (By Product Type, Gender, Usage, End User, and Country/Sub-region) o China (By Usage) o Japan (By Usage) o India (By Usage) o Australia (By Usage) o Southeast Asia (By Usage) o Rest of Asia Pacific (By Usage) · Latin America (By Product Type, Gender, Usage, End User, and Country/Sub-region) o Brazil (By Usage) o Mexico (By Usage) o Rest of Latin America (By Usage) · Middle East & Africa (By Product Type, Gender, Usage, End User, and Country/Sub-region) o GCC (By Usage) o South Africa (By Usage) o Rest of the Middle East & Africa (By Usage) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 4.7 billion in 2026 and is projected to reach USD 7.48 billion by 2034.

In 2025, North Americas regional market value stood at USD 2 billion.

Growing at a CAGR of 6.00%, the market will exhibit steady growth over the forecast period (2026-2034).

By product, absorbents is the leading segment in the market.

The introduction of novel urinary incontinence devices is one of the major factors driving the markets growth.

Essity Aktiebolag, Medtronic, and Coloplast A/S are the major players in the global market.

North america dominated the urinary incontinence devices market with a market share of 42.50% in 2025.

The increasing prevalence of urinary incontinence and growing technological advancements are anticipated to drive product adoption.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us