Insecticides Market Size, Share & Industry Analysis, By Type (Chemical [Pyrethroids, Organophosphorus, Carbamates, and Others] and Biological), By Formulation (Emulsifiable Concentrates (EC), Wettable Powders (WP), Suspension Concentrate (SC), Oil in Water Emulsions (EW), and Others), By Application Method (Foliar Treatment, Seed Treatment, Soil Treatment, and Others), By Crop Type (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

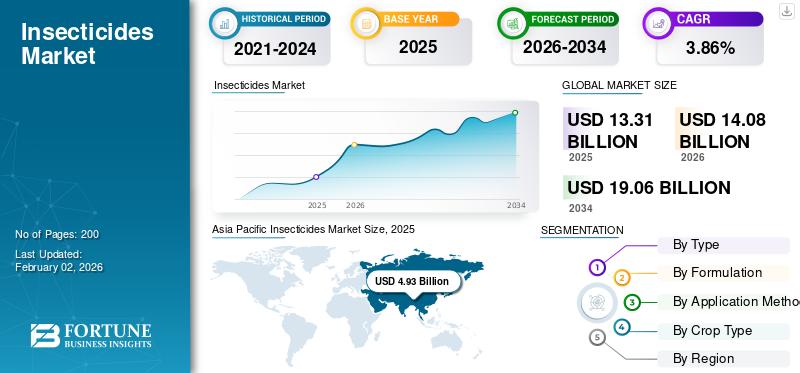

Insecticides Market Size and Industry Overview

The global insecticides market size was valued at USD 13.31 billion in 2025 and is projected to grow from USD 14.08 billion in 2026 to USD 19.06 billion by 2034, exhibiting a CAGR of 3.86% during the forecast period. Asia Pacific dominated the insecticides market with a market share of 37.03% in 2025.

Insecticides are chemicals applied to eliminate or prevent insects from participating in unwanted or harmful activities. Presently, insect pests are known to lower the global crop yields by 20–40% per year. They are grouped according to their structure and action. Insecticides are widely applied in agriculture, public health, and industrial uses, and domestic and commercial purposes. The Food and Agriculture Organization (FAO) projects that to feed an estimated global population of 9.1 billion by 2050, world food production needs to rise by about 70% compared to 2005-07 food levels. This is primarily due to robust population growth and higher per-capita food consumption as incomes rise. This tremendous rise in food requirement primarily drives the demand for crop protection products, including insecticides which protects crops from insect pests.

The industry is dominated by key market players such as Bayer AG, BASF SE, Syngenta AG, Corteva Agriscience, and FMC Corporation. These players invest heavily in R&D to discover novel active ingredients that address pest resistance and improve efficacy. This includes developing new chemical classes and biological insecticides. For instance, in April 2024, Bayer announced its plan to launch the world’s first bioinsecticide for arable crops, targeting cabbage stem flea beetle pests, which cause significant damage in crops such as oilseed rape and cereals. This bioinsecticide, developed in partnership with U.K.-based AlphaBio Control, will be the first biological insecticide specifically tailored for arable farming, offering an environmentally friendly, sustainable alternative to traditional chemical insecticides.

Download Free sample to learn more about this report.

Insecticides MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 13.31 billion

- 2026 Market Size: USD 14.08 billion

- 2034 Forecast Market Size: USD 19.06 billion

- CAGR: 3.86% from 2026–2034

- Asia Pacific dominated the insecticides market with a 37.03% share in 2025.

- The chemical or synthetic segment accounted for 92.83% of the market share in 2026.

- The emulsifiable concentrates (EC) segment held a 35.30% market share in 2026.

North American

North America reached USD 2.84 billion in 2026, driven by advanced farming practices and integrated pest management.

Europe

Europe is projected to reach USD 2.44 billion in 2026, supported by sustainable agriculture and precision pest control technologies.

Asia Pacific

Asia Pacific generated USD 4.93 billion in 2025, supported by extensive agricultural activities and high demand for pest control solutions.

U.S.

The market is projected to reach USD 2.12 billion in 2026, driven by strong demand from corn and soybean cultivation.

Japan

The market is projected to reach USD 0.50 billion in 2026, supported by demand for crop protection across intensive farming systems.

Read More

MARKET DYNAMICS

Market Drivers

Rising Global Food Demand and Population Growth to Drive Market Growth

Increased global food consumption and population growth are major drivers of market expansion in the market because they enhance the demand for greater farm productivity and efficient pest control. Population growth also results in increased agricultural land use and intensified cultivation, which further intensifies pest pressures, leading to an increase in insecticide consumption. Climate change and urbanization further result in the infestation of new pests that need sophisticated and efficient insecticide solutions.

- According to the Food and Agriculture Organization, annually, up to 40% of the world's crop production is lost every year to pests and diseases, which costs the world economy more than USD 220 billion. Insecticides play a key role in reducing these losses and improving yield.

Market Restraints

Regulatory and Safety Burdens to Impede Market Growth

Regulatory and safety burdens are pertinent factors that can hinder the global insecticides market growth. More stringent regulations to safeguard human health and the environment tend to cause higher compliance costs, slower product approval, and limitations on some chemical active ingredients. Furthermore, regulatory institutions such as the Central Insecticides Board and Registration Committee (CIBRC), U.S. Environmental Protection Agency (EPA), and others keep refining guidelines on pesticide residues, safe methods of application, and environmental quality standards. Conformity with such standards usually calls for major investments in testing, research, and monitoring that can delay market development or limit the development of new products. For instance, numerous countries have banned or restricted the use of certain insecticides owing to issues regarding their persistence, bioaccumulation, and effects on non-target species, such as beneficial insects and biodiversity. The European Union, for example, has strict regulations under the Pesticidal Product Regulations, which restrict the use of certain active ingredients.

Market Opportunities

Innovations in Digital Agriculture and Integrated Pest Management to Unlock New Growth Opportunities

Digital agriculture and integrated pest management (IPM) innovations are opening up new opportunities for growth in the market by allowing more efficient, effective, and sustainable pest control solutions. Digital agriculture technologies such as remote sensing, drones, IoT sensors, and artificial intelligence allow the real-time tracking of pest infestations and crop health. These technologies enable farmers to target insecticides more effectively, cutting down on total chemical application per hectare. Recent development in IPM encourages the application of bio-insecticides, pheromone traps, resistant crop varieties, and decision-support systems, which minimize the use of traditional insecticides and postpone resistance development.

- For instance, in February 2024, Syngenta Crop Protection announced a partnership with the Israeli ag-biologicals company Lavie Bio to discover and develop new bio-insecticides. This collaboration aims to create more sustainable and effective pest management solutions that can be integrated with Integrated Pest Management (IPM) practices.

Insecticides Market Trends

Growing Importance of Sustainable Pest Control Aligned with Global Ecological Approaches to Shape Industry

Sustainability efforts focusing on reducing the environmental footprint of pest management by promoting the use of bio-insecticides and integrated pest management (IPM) practices. These approaches aim to minimize chemical residues in soil and water, preserve beneficial insect populations, and prevent pest resistance. International bodies such as the Food and Agriculture Organization (FAO) proactively promote more sustainable plant protection practices that weigh on the efficacy of pest control against the health of ecosystems. Regulatory environments increasingly promote the use of less toxic, more biodegradable insecticides, pushing the industry to move towards more environmentally friendly options.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

High Efficacy and Broad-Spectrum Action to Lead the Chemical Segment’s High Market Proportion

On the basis of the type, the market is segmented into chemical and biological.

The chemical or synthetic segment is projected to dominates the market with a share of 92.83% in 2026, mainly owing to its high efficiency, longer shelf life, and extensive pest management capabilities. In 2025, chemical insecticides captured approximately 92.97% of the market demand, depicting their extensive usage in agriculture for safeguarding varied crops across large areas, notably in the Asia Pacific region. Chemical insecticides such as carbamates, organophosphates, and pyrethroids work highly effectively on a sucking, chewing, and biting pests that pose a risk of major damage to crops. Carbamates are highly used and utilized due to their broad-spectrum activity and organophosphates continue to be used extensively for their pest-killing power.

The biological segment is expected to grow significantly in the market during the forecast period, with a CAGR of 5.45%.

By Formulation

Ease of Handling and Application Leads to Emulsifiable Concentrates Segment Growth and Dominance

On the basis of the formulation, the market is segmented into emulsifiable concentrates (EC), wettable powders (WP), suspension concentrates (SC), oil-in-water emulsions (EW), and others.

The emulsifiable concentrates (EC) segment is anticipated to accquire the most significant proportion in the market with a share of 35.30% in 2026. ECs are comparatively simpler to handle when used for treating vast areas as they have good compatibility with water and are evenly spread, allowing effective pest control. This makes them convenient for extensive agricultural production and applications. ECs possess a comparatively better shelf life and are stable during storage, offering consistency to the farmers and distributors across various regions. The emulsifiable concentrates (EC) market, worth around USD 4.78 billion in 2025, is expected to reach USD 5.66 billion in 2032, while maintaining a CAGR of 2.43%.

The oil in water emulsions (EW) segment is expected to grow significantly with a CAGR of 7.52% during the forecast period.

By Application Method

Quick Absorption and Improved Pest Control Fuels Foliar Treatment Market Leadership

On the basis of application method, the market is segmented into foliar treatment, seed treatment, soil treatment, and others.

Foliar treatment market is expected to hold the most significant portion of the application method segment is projected with a share of 67.54% in 2026, with forecasts estimating to USD 8.54 billion in 2025. The foliar treatment segment leads the market mainly due to insecticides’ effectiveness, targeted application of biting and chewing pest insecticides directly on the leafs, allowing for speedy absorption and better pest control.

The soil treatment segment is anticipated to grow at the fastest growth rate of 6.04% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Crop Type

High Economic Importance and Wide Cultivation Area to Lead the Cereals & Grains Segment’s Market Leadership

Based on the crop type, the market is segmented into cereals & grains, oilseeds & pulses, fruits & vegetables, and others.

The cereals & grains segment is projecte to dominates the global market with a share of 41.48% in 2026, mainly because cereals and grains, including maize, rice, wheat, barley, oats, millet, and rye, are most widely farmed crops globally.The size of the cereals & grains market in 2025 is expected to be around USD 5.56 billion, accounting for approximately 41.81% of global insecticides market. These are resilient staple foods and a major source of food security all over the world, making their need for protection from insect pests paramount. Increased global food requirements, decrease in arable land, and necessity to raise the yield per hectare for crops propel the use of insecticides in this segment.

The oilseeds & pulses segment is expected to grow significantly in the forecast period at a CAGR of 5.57%.

Insecticides Market Regional Outlook

Regionally, the report covers North America, Europe, Asia Pacific, South America, and Middle East & Africa.

Asia Pacific

Asia Pacific Insecticides Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates theinsecticide market with a projected market value of USD 4.93 billion in 2025 and is projected to reach USD 5.24 billion by 2034 at a CAGR of 5.02%. Its dominance is fueled by its major contribution of agriculture to GDP, wide variations in climate and soil favoring the cultivation of variety of crops, and high infestations of pests resulting in loss of yield. The Asia Pacific region, particularly China, India, and Southeast Asia, is characterized by highly extensive cropland and high multi-cropping systems, necessitating regular pest control. According to the Food and Agriculture Organization (FAO), in 2022, Asia was the largest exporter of pesticides, with an estimated 3.5 million tonnes volume. The Japan market is valued at USD 0.50 billion by 2026, the China market is projected to valued at USD 2.30 billion by 2026, and the India market is projected to valued at USD 1.47 billion by 2026.

North America

North America contributed approximately USD 2.69 billion to the global market in 2025, accounting for 20.20% share, and is expected to reach USD 2.84 billion in 2026. The North America insecticide market is growing substantially with well-established agricultural practices emphasizing integrated pest management. Major usage includes advanced insecticides in crops like corn and soy. The market benefits from strong regulatory frameworks and innovations in pest control technologies. The U.S. market is projected to valued at USD 2.12 billion by 2026.

Europe

In 2025, the Europe market stood at USD 2.32 billion, representing 17.40% of global demand, and is projected to grow to USD 2.44 billion in 2026. In Europe, France led with approximately 21.97% market share in 2024, with a boost from bulk production of wheat, barley, and cereals, using carbamates and pyrethroids in favor. Germany is projected to grow at a 3.14% CAGR fueled by pest management difficulties stemming from climate change, with an area of emphasis on grain and cereal crops. These nations focus on sustainable agriculture and precision application to minimize their environmental footprints. The UK market is valued at USD 0.21 billion by 2026, and the Germany market is valued at USD 0.37 billion by 2026.

South America

The market in South America, valued at around USD 2.08 billion in 2025 with a 4.05% CAGR, is driven by Brazil's dominance in soybean and corn farming, while Argentina leads in growth rate of 5.45% due to its precision agriculture.

Middle East and Africa

The Middle East and African market, around USD 1.24 billion in 2024, is expanding with a 2.83% CAGR supported by increasing demand for food grain and growing pest control services, with an emphasis on cost-saving organophosphorus insecticides. In 2025, Middle East & Africa generated USD 1.3 billion, contributing 9.78% to global market revenue, and is projected to grow to USD 1.36 billion in 2026.

Latin America

Latin America recorded a market size of USD 2.08 billion in 2025, capturing 15.59% of the global market share, and is projected to reach USD 2.2 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Significant Merger and Acquisition Activities and Strategic Partnerships to Support Market Presence of of Key Players

The industry is dominated by a few major multinational agribusiness giants such as Bayer AG, Syngenta AG, BASF SE, FMC Corporation, Corteva Agriscience, and ADAMA Agricultural Solutions. These major players have a strong global market share, owing to their wide product portfolios, solid R&D infrastructure, widespread global distribution networks, and high brand recognition. The market structure indicates moderate to high consolidation based on extensive merger and acquisition activities and strategic alliances amongst these giants aimed at strengthening technological abilities and their geographic scope.

Key Players in the Market

|

Rank |

Company Name |

|

1 |

Bayer AG |

|

2 |

BASF SE |

|

3 |

Syngenta AG |

|

4 |

Corteva Agriscience |

|

5 |

FMC Corporation |

List of Key Insecticides Companies Profiled

- BASF SE (Germany)

- Bayer Crop Science (Germany)

- Marrone Bio Innovations (U.S.)

- Sumitomo Chemical (Japan)

- Dow AgroSciences (U.S.)

- Corteva Agriscience (U.S.)

- Valent BioSciences (U.S.)

- Syngenta AG (Switzerland)

- FMC Corporation (U.S.)

- Adama Agricultural Solutions Ltd. (Israel)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Insecticides (India) Limited (IIL) launched a new broad-spectrum insecticide called Sparcle in partnership with Corteva Agriscience. Sparcle is specifically designed for paddy farmers to target the brown plant hopper (BPH), a harmful pest that damages rice crops.

- February 2025: BASF SE launched its new rice insecticide, Valexio, powered by Prexio Active, in India. Prexio Active is a novel Group 4E insecticide specifically designed to control all four major rice hopper species with a unique mode of action that prevents resistance development.

- August 2024: Syngenta AG launched a new insecticide, Mainspring Xtra. It is designed for use in greenhouses, nurseries, and ornamental landscapes and combines two active ingredients: cyantraniliprole and thiamethoxam.

- August 2023: Insecticides (India) Limited acquired an industrial site of approximately 58,000 square meters located in the Industrial Area of Sotanala, Alwar, Rajasthan, to establish a state-of-the-art manufacturing facility. This expansion is part of the company's plan to boost its operational capacity and production capabilities, aligning with its long-term vision for organic growth.

- June 2023: Dhanuka Agritech launched a new biological insecticide product called Nemataxe for the domestic market. Nemataxe is based on the beneficial nematophagous fungus Paecilomyces lilacinus (Strain no. P1-1-MTCC 5175) and is used as a bionematicide to control all types of nematodes, including root knot, cyst knot, root lesion, and burrowing nematodes.

REPORT COVERAGE

The global insecticides market industry report analyzes the market in depth and highlights crucial aspects such as global market trends, market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the report also provides insights into the global insecticides market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.86% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type · Chemical o Pyrethroids o Organophosphorus o Carbamates o Others

|

|

By Formulation · Emulsifiable Concentrates (EC) · Wettable Powders (WP) · Suspension Concentrate (SC) · Oil in Water Emulsions (EW) · Others |

|

|

By Application Method · Foliar Treatment · Seed Treatment · Soil Treatment · Others |

|

|

By Crop Type · Cereals & Grains · Oilseeds & Pulses · Fruits & Vegetables · Others |

|

|

By Region · North America (By Type, Formulation, Application Method, By Crop Type, and Country) • U.S. (By Crop Type) • Canada (By Crop Type) • Mexico (By Crop Type) · Europe (By Type, Formulation, Application Method, By Crop Type, and Country) • Germany (By Crop Type) • Spain (By Crop Type) • Italy (By Crop Type) • France (By Crop Type) • U.K. (By Crop Type) • Rest of Europe (By Crop Type) · Asia Pacific (By Type, Formulation, Application Method, By Crop Type, and Country) • China (By Crop Type) • Japan (By Crop Type) • India (By Crop Type) • Australia (By Crop Type) • Rest of Asia Pacific (By Crop Type) · South America (By Type, Formulation, Application Method, By Crop Type, and Country) • Brazil (By Crop Type) • Argentina (By Crop Type) • Rest of South America (By Crop Type) · Middle East & Africa (By Type, Formulation, Application Method, By Crop Type, and Country) • South Africa (By Crop Type) • Egypt (By Crop Type) • Rest of the MEA (By Crop Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 14.08 billion in 2026 and is anticipated to reach USD 19.06 billion by 2034.

At a CAGR of 3.86%, the global market will exhibit steady growth over the forecast period.

In the formulation segment, emulsifiable concentrates (EC) sub-segment leads the market.

Asia Pacific held the largest market share in 2025.

Rising global food demand and population growth drive the market growth.

Bayer AG, BASF SE, Syngenta AG, Corteva Agriscience, and FMC Corporation are the leading companies in the market.

The growing importance of sustainable pest control, aligned with global ecological approaches.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us